As we have noted, the Fed will often use the media, and in particular, Nick Timiraos of the WSJ, to float trial balloons to prepare investors of coming Fed speeches or policy actions that may be different than the market’s current collective thinking. It appears the Fed floated a trial balloon yesterday morning. Jerome Powell’s Dilemma warns that Jerome Powell’s Jackson Hole speech may be more hawkish than expected. To wit:

Several former Fed officials who have worked closely with Mr. Powell say he is likely to err on the side of raising rates too much, rather than too little, because tolerating excessive inflation would represent a much greater institutional failure for the central bank.

The basis for the Fed’s concern is a possible new inflation regime. Nick’s article starts as follows: “Central bankers worry that the recent surge in inflation may represent not a temporary phenomenon but a transition to a new, lasting reality.” We have also written about these same inflationary factors. For more, please read Deglobalization and Persistent Inflation.

What To Watch Today

Economy

- 8:30 a.m. ET: Personal income, July (+0.4% expected, +0.6% previously)

- 8:30 a.m. ET: Personal spending, July (+0.6% expected, +1.1% previously)

- 8:30 a.m. ET: Whole inventories, July (+1.4% expected, +1.8% previously)

- 8:30 a.m. ET: Retail inventories, July (+2% previously)

- 8:30 a.m. ET: PCE, month-on-month, July (+0.1% expected, 1% previously)

- 8:30 a.m. ET: PCE, year-on-year, July (+6.4% expected, +6.8% previously)

- 8:30 a.m. ET: Core PCE, month-on-month, July (+0.3% expected, +0.6% previously)

- 8:30 a.m. ET: Core PCE, year-on-year, July (+4.7% expected; +4.8% previously)

- 10:00 a.m. ET: University of Michigan consumer sentiment, August (55.2 expected, 55.1 previously)

Earnings

- No major earnings releases today

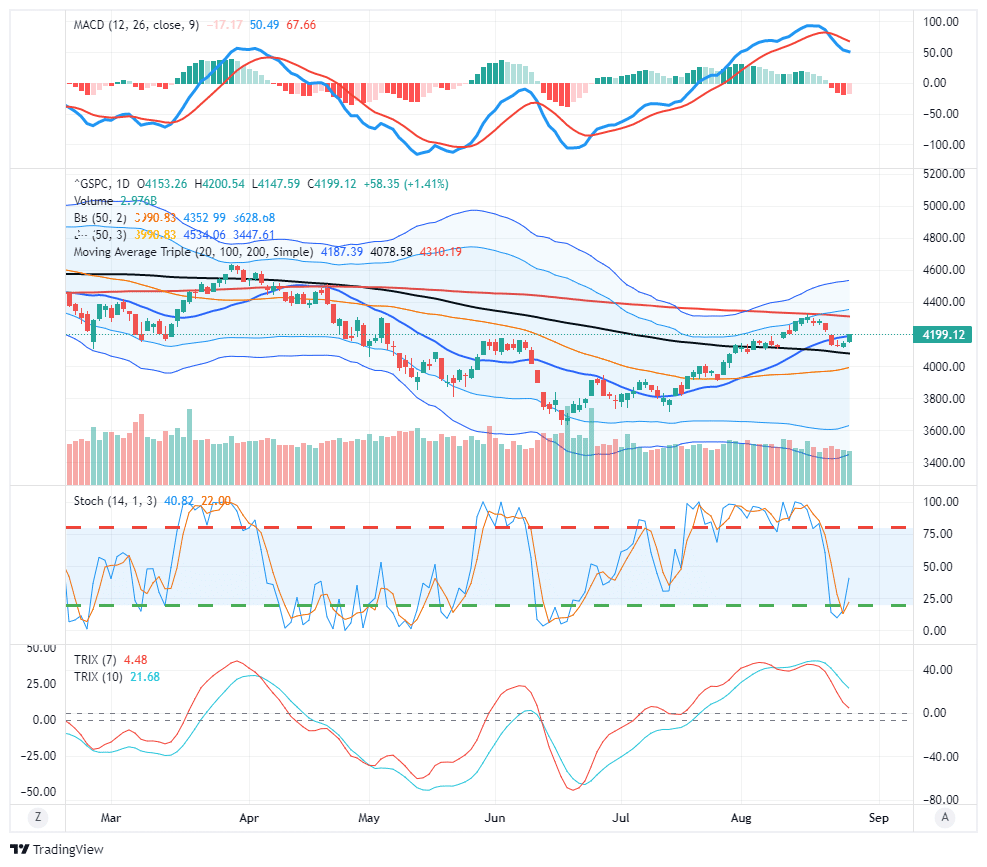

Market Trading Update

“The 20-dma, along with the previous resistance levels at 4160, will provide fairly stiff resistance to any increase short term. However, the market is oversold enough on a short-term basis that a reflexive bounce is likely.”

That reflexive rally came with a vengeance yesterday as the market rallied sharply higher on expectations the Fed will lean “dovish” this weekend at the Jackson Hole summit. Jerome Powell is on deck to speak today. If he tows the company line, he is expected to note that the Fed remains dependent on incoming data to judge policy decisions.

For the bulls – the market cleared overhead resistance at the 20-dma yesterday. Such now clears the way for another attempt at the 200-dma, and with markets short-term oversold, there is “fuel” to support that rally. For the bears – the MACD “sell signal” remains in place, suggesting that markets may have more “consolidative” work to do before the next leg of the market move (up or down) can commence. If the market can break above the 200-dma, we will need to be more bullish on markets, particularly with easing financial conditions.

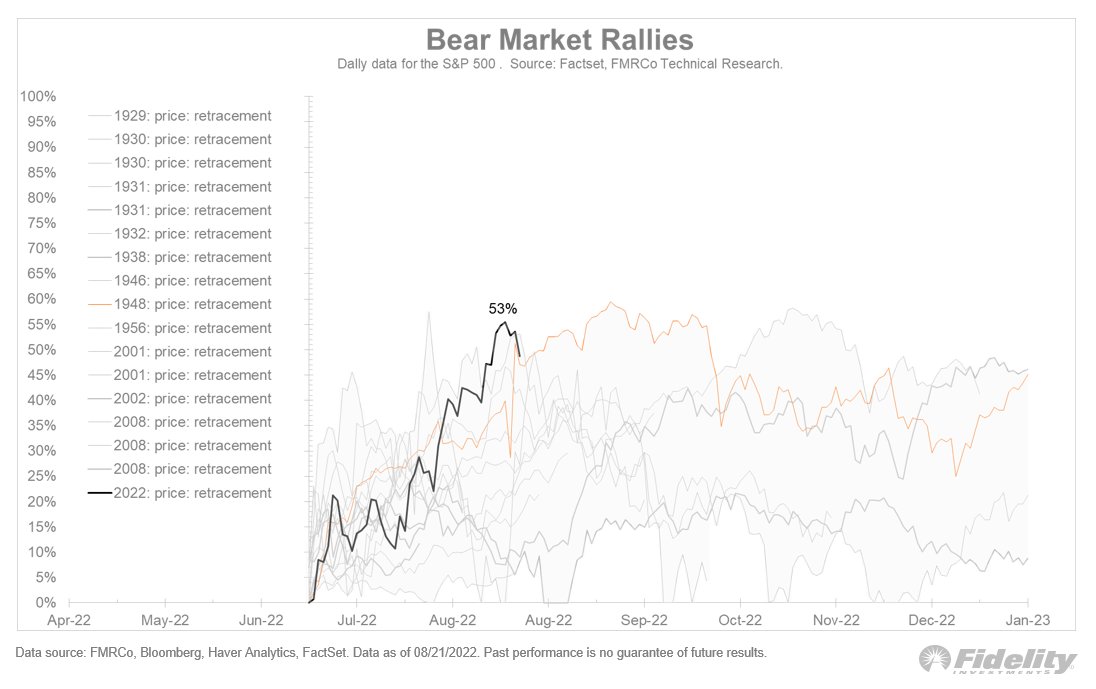

Bull or Bear Market?

The following chart from Fidelity provides both warning and hope. Based on the graph, if the current stock market rally is a bear market rally, it has probably peaked, or will so, in the next few weeks. The logic is based on 16 other bear market rallies since 1929. Basically, a 50% retracement rally has capped the upside in bear market rallies. On the flip side, if the market can continue higher, we may not be in a bear market rally. The recent downturn may be just a brief stumble on the path to new record highs.

Baron’s Says Brace for a Bad September

The opening paragraph in September is Usually a Bad Month for Stocks, This One Could be Ugly is as follows:

The stock market’s worst month—September—is approaching. This one could be particularly bad.

Despite the fearful headline, the following paragraph states that the S&P has only averaged a 1% loss in September going back to 1928. The graph below also shows that September tends to be tough but not “ugly.” To help justify using the word “ugly,” the author offers the following reasons to be concerned:

- “The stock market has already ripped higher recently, with both indexes up double digits in percentage terms since their lowest levels of the year in mid-June.”

- The probably of the Fed hiking by .75% at its September meeting

- Bond yields moving higher

- Oil prices perking back up

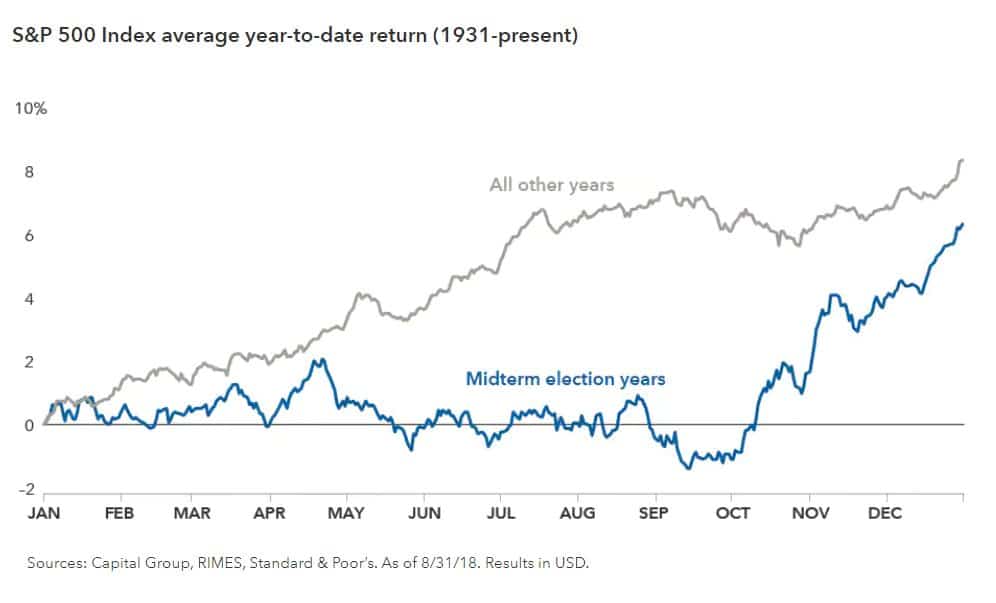

Despite the author’s concerns, the chart below shows that the market’s behavior in midterm election years is very different than in non-midterm election years. Based on the average for midterm years, we should expect a weak start to September and then a strong run higher for the remainder of the year.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.