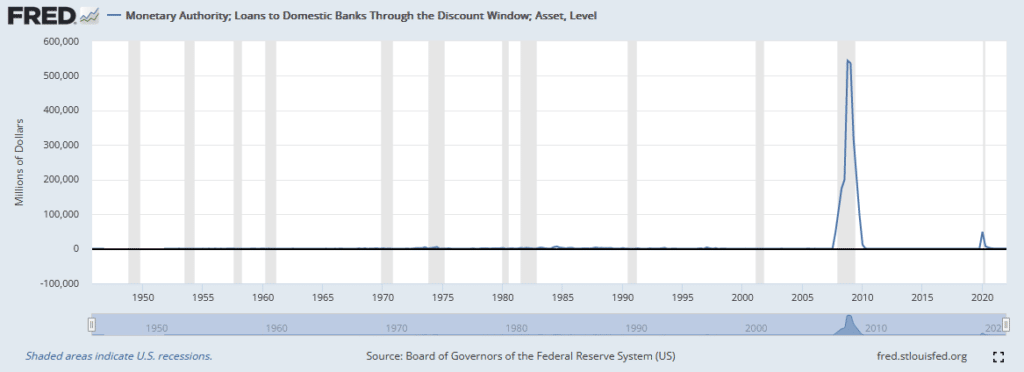

The recent market uptrend is stalling. The culprit is most likely the coming annual Jackson Hole Federal Reserve Conference. Investors appear apprehensive that Powell and his colleagues will not back down on raising rates or QT. Further, they may try to debunk the pivot narrative driving stocks higher. Also, supporting the pre-Jackson Hole Conference jitters, we learned that two Fed members voted to raise the discount rate by 100bps in July. The discount rate is the interest rate for emergency loans from the Fed to banks. The window has only been used on a larger scale twice since 1945, as shown below. Given that the discount rate is somewhat irrelevant, we think the two voters are likely sending investors a cautionary message heading into the conference at Jackson Hole.

What To Watch Today

Economy

- Initial jobless claims (252,000 expected, 250,000 previously)

- Second quarter GDP, second estimate (-0.8% expected; -0.9% previously)

- Kansas City Fed manufacturing activity, August (13 previously)

Earnings

Market Trading Update

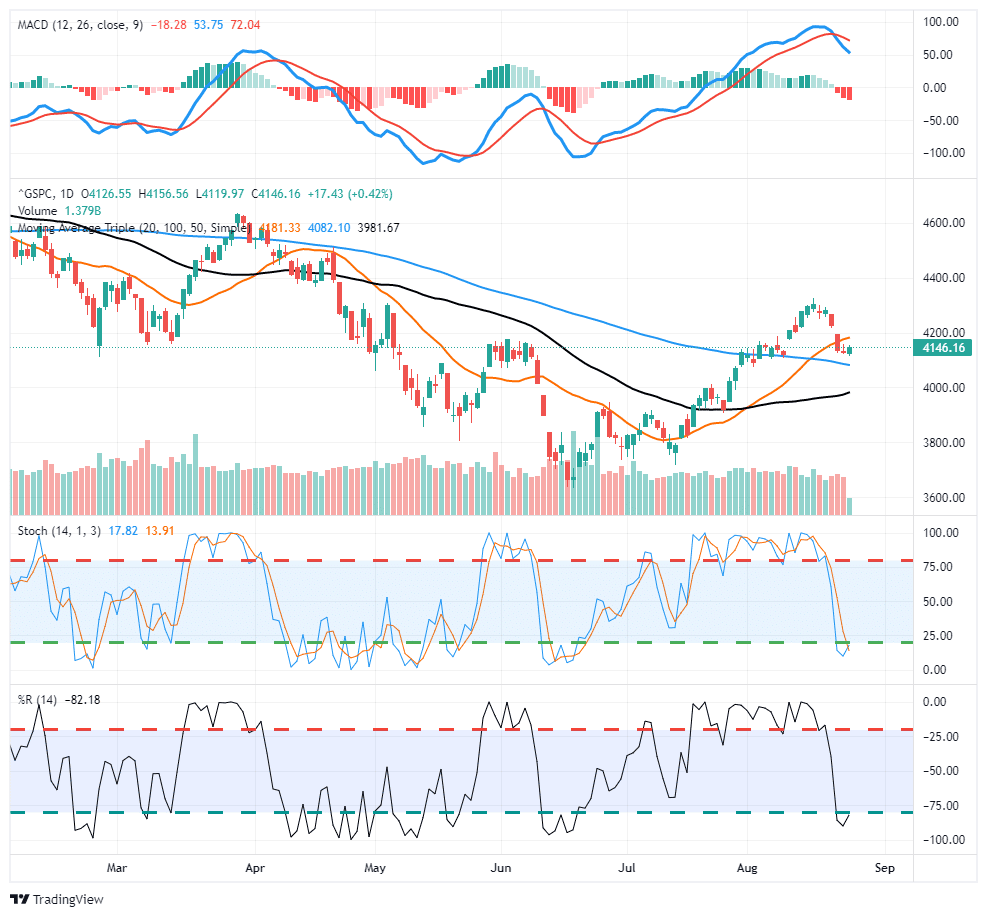

As discussed in yesterday’s 3-minutes video, the rebound in the market yesterday, while very weak, was not surprising after 3-days of selling. The 20-dma, along with the previous resistance levels at 4160, will provide fairly stiff resistance to any increase short term. However, the market is oversold enough on a short-term basis that a reflexive bounce is likely. We suggest using that bounce to rebalance portfolio risks accordingly as the MACD signal is still on a “sell,” suggesting lower prices near term. Again, be patient and wait for the MACD to give us a buy signal to start adding more equity exposure.

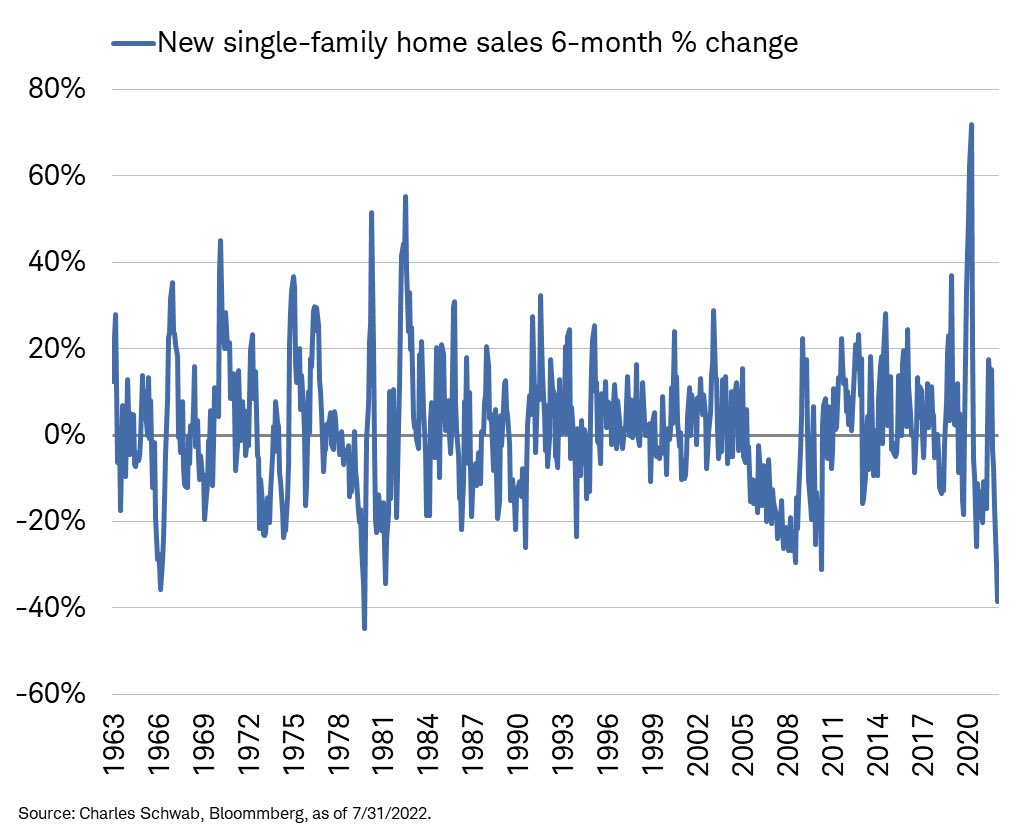

New Home Sales Plummet

Higher mortgage rates are starting to punish new home builders. As we show below, the six-month change in new single-family home sales fell by 38.5%, the worst since 1980. Our Tweet of the Day below shows more evidence of mounting problems. As Lance’s tweet points out, the inventory of new homes for sale, as measured in time on the market, is now 10.9 months, the worst since the financial crisis in 2008 (12.2 months). Before that, one has to go back to 1980 to find as high a supply of new homes for sale. Further, the graph in the tweet shows the enormous disconnect between the still very high prices of new homes and the mounting supply. New home prices will inevitably fall.

To help understand how higher mortgage rates and home prices are problematic for new home sales, consider the following from Charlie Bilello:

In Jan 2021, the 30-yr mortgage rate was 2.65% and average new home price in the US was $401,700.

Today the 30-yr mortgage rate is 5.65% and average new home price is $546,800.

Assuming a 20% down payment, that’s a 95% increase in the monthly payment (from $1,294 to $2,525).

Short Homebuilders?

We hear many pundits telling investors to sell or even short homebuilders. The news on new home sales is certainly grim but do they warrant selling? In our weekly SimpleVisor Five for Friday report, in late July, we shared a stock scan seeking companies that may already be priced for a recession. Our scan started with 29 stocks from a Goldman Sachs list of companies whose earnings are least vulnerable to a recession. To wit:

For example, NVR is the least vulnerable stock on their list. Consensus EPS estimates forecast that NVR’s net profit margin will fall by 1.85%. Over the last three recessions, their net profit margin only fell by .42%. They also show that NVR’s expected profit margin is 39% below its 20-year average profit margin.

From the Goldman list, we screened for the cheapest valuations. Homebuilder NVR did not make our final list, but two other homebuilders did. D.R. Horton (DHI) was one of them. The SimpleVisor table below shows that DHI is exceptionally cheap. While your gut may want to sell homebuilders like DHI, its valuations should at least warrant a consideration that maybe the time to buy is when everyone is selling.

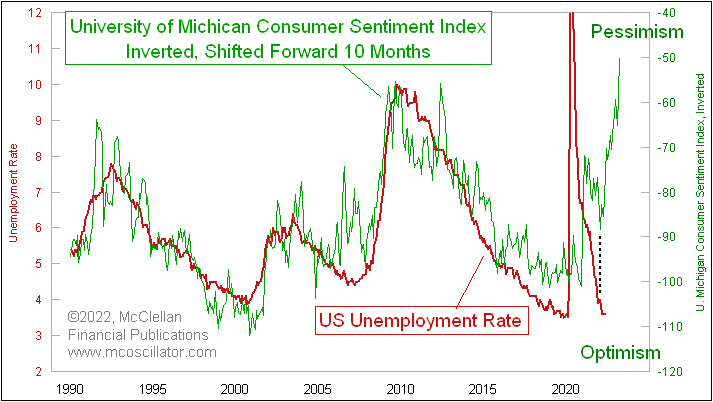

Consumer Sentiment and Unemployment

The following graph from Tom McClellan shows the strong correlation between consumer sentiment and the unemployment rate. Unemployment tends to lag sentiment by about ten months. Either this time is different, and the startling divergence will stick, or unemployment will shoot higher.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read