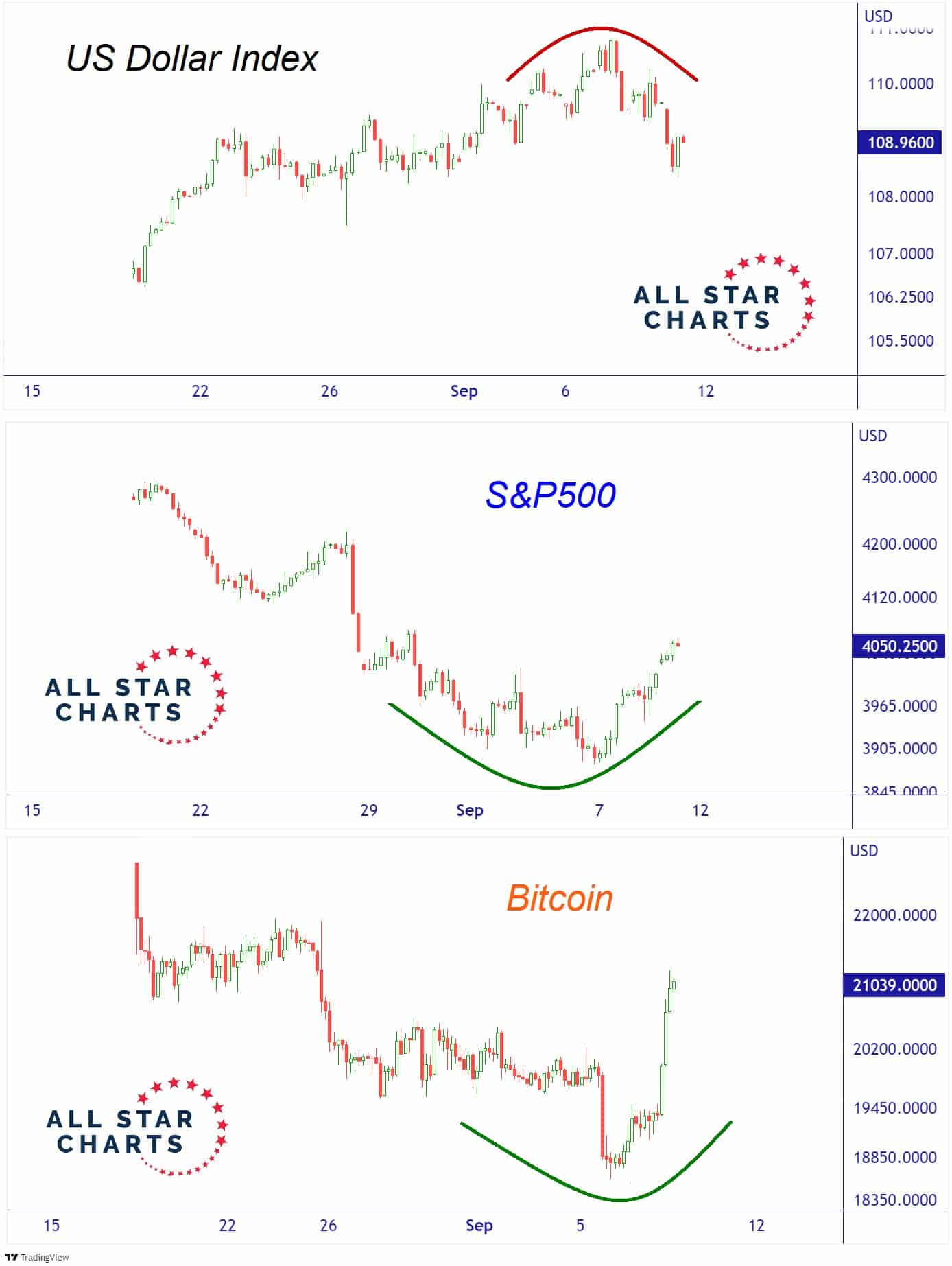

Traders dumped the U.S. dollar on Friday, and most asset classes rallied. It is becoming increasingly obvious that dollar strength is problematic for many asset classes. While investors may applaud Friday’s “risk on” market stance associated with the dollar dump, the Fed may have other ideas. While not a current Fed member, ex-New York Fed President Bill Dudley stated: “the Fed wants a stronger dollar because it reduces inflation.” To his point, if the dollar continues to dump, inflation will not decline as quickly. However, he fails to mention how the stronger dollar negatively affects our allies in Europe and Japan. Nor is he considering that these nations may be partially responsible for higher yields as they sell U.S. bonds to support their currencies.

What To Watch Today

Economy

- No notable reports are scheduled for release

Earnings

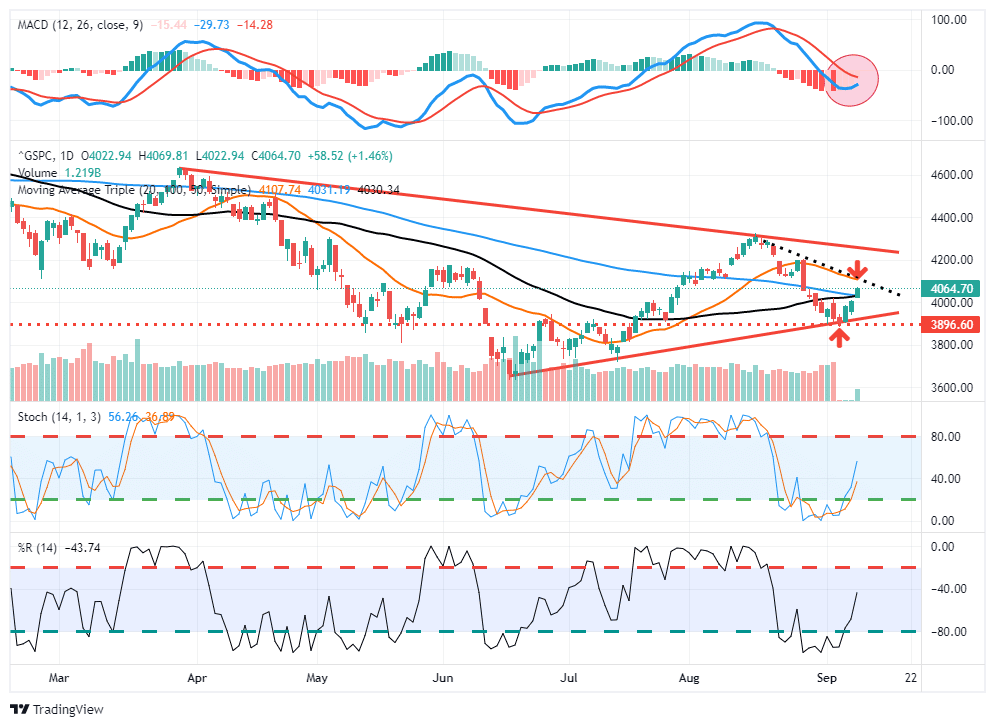

Market Trading Update

Last week, that reflexive rally started on Wednesday and carried through into Friday as the bulls took charge, ignoring warnings from Central Bankers that tighter monetary policy was coming. Notably, the market is setting up a more bullish posture short term, as shown below. First, the market held support at the rising bullish trend line and managed to climb through resistance at the 50- and 100-day moving averages (dma), which now sets up a potential rally to the 20-dma. With markets still oversold, there is fuel for an additional rally into next week, and importantly, the market is very close to flipping the MACD onto a “buy signal.”

With inflation raging, the economy slowing, and the Fed tightening monetary policy, it isn’t easy to process the more bullish undertones of the market. However, we must trade the market for what it is rather than what we wish it to be. As such, we are looking opportunistically to add exposure to portfolios in a controlled manner, and if the bullish trend continues over the next few weeks, we will slowly put cash back to work.

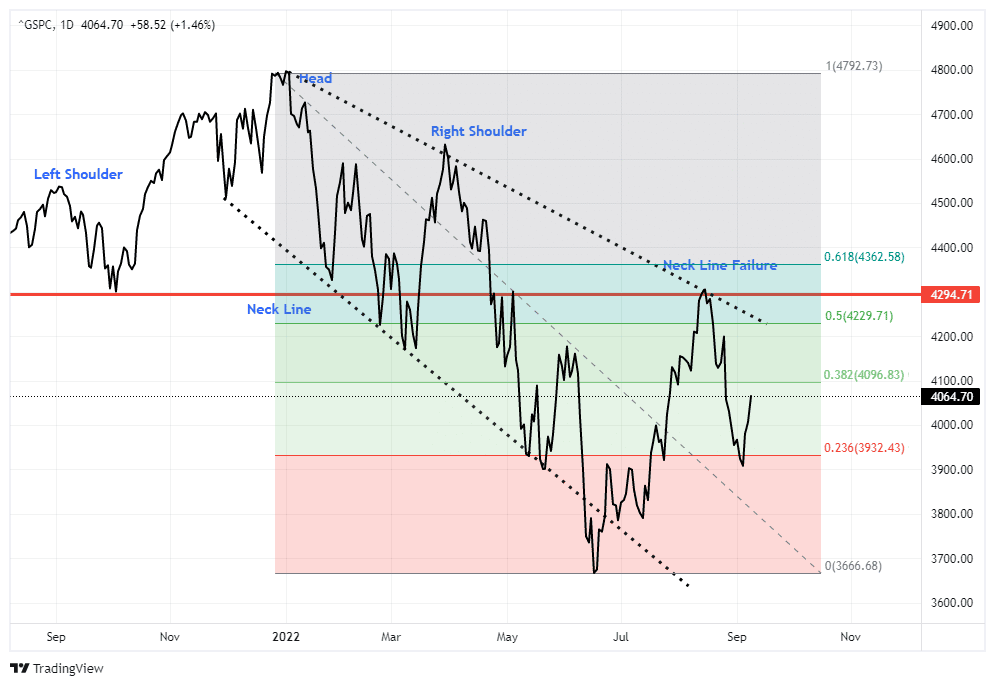

However, with that stated, we also recognize the overall risk. Therefore, if we decide to increase equity exposures, we will do so in a very controlled manner with very tight stop-loss levels and size limitations. There is also the issue of the confirmed “head and shoulder” pattern which suggests there is still downside risk to the market. Therefore, while we may add exposure for a short-term rally, we will likely “sell” any rally to 4250 for the time being.

The media often states that investors should not “fight the Fed.” Notably, surging stock markets are the last thing the Fed wants.

The Week Ahead

Bonds will be in the spotlight today and Tuesday as the U.S. Treasury auctions off ten and 30-year bonds. These auctions typically result in volatility before and after the auctions as the dealers set up for the auction and then react to the results. Traders will be more cautious around these auctions as CPI will be released tomorrow. The current expectation is for the monthly rate to increase from 0.3% to 0.4%. The year-over-year rate should decline from 8.5% to 8.1%. Likely, traders will take their cue from the core inflation rate as that seems to have the most Fed interest. More inflation news will follow on Wednesday with the release of the PPI report.

Thursday offers retail sales and a glimpse at the health of consumers. Expectations are for a .1% increase. Another gauge of the consumer will come on Friday with the University of Michigan consumer sentiment data.

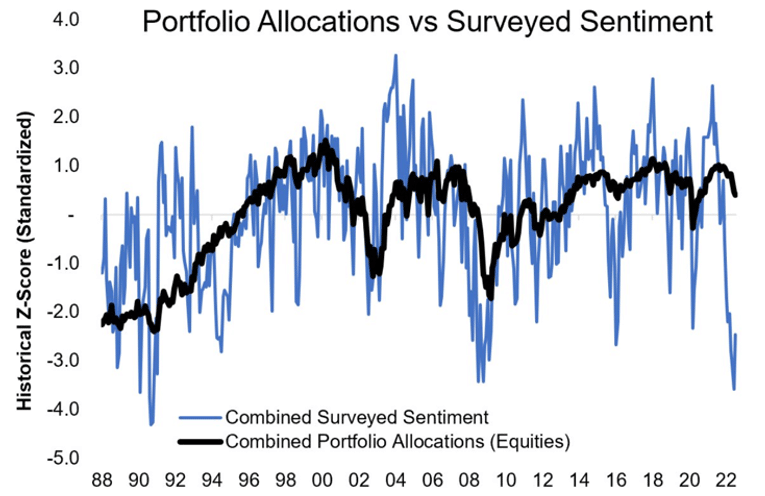

Equity Positioning, Sentiment, and Disposition

Interesting chart from Kailash Concepts

“Recently, the wonderful Topdown Charts put out a fantastic thread on the dispersion between equity positioning, sentiment, and cash balances. The chart below is terrific, and the subsequent walk-through is illuminating. Their thread highlighted how equity sentiment was at 2009 lows, but equity positioning had fallen slightly. A later chart in the thread shows much of that selling appears in increased cash balances.

Investor pessimism appears to have manifested itself in one of the most pernicious applications of behavioral finance – the disposition effect. This is when we sell our winners and hold our losers to avoid the mental pain of taking a loss.”

Why The Fed Wants Higher Unemployment

The Federal Reserve has been outspoken about its desire to reduce inflation. They are also transparent that the cost to do so may be jobs. To wit, the WSJ led with the following statement in a recent article describing the tradeoff:

Federal Reserve officials are beginning to signal that higher unemployment rates might be a necessary consequence of their efforts to damp inflation by raising interest rates.

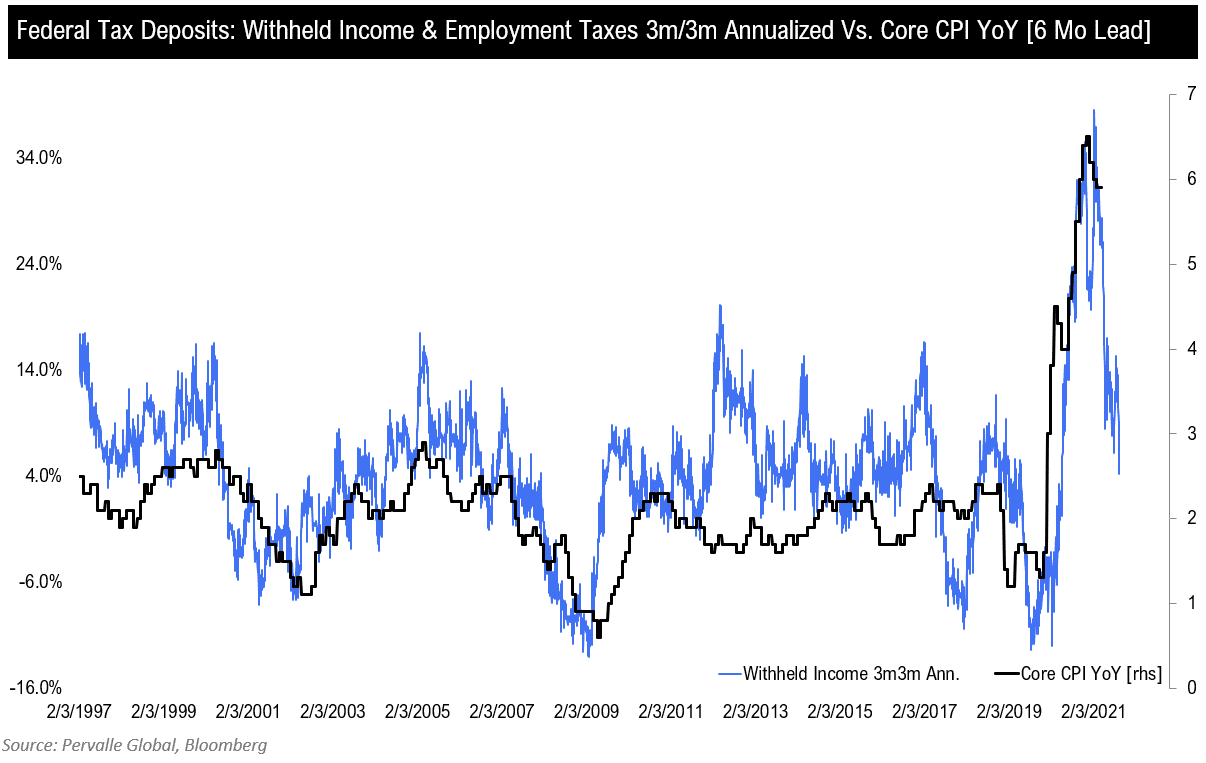

The graph below from Pervalle Global shows the relationship between jobs and inflation. As it shows, withheld income taxes, a good proxy for the labor market, tends to lead CPI by about six months. If the correlation holds up in the coming months, inflation will fall sharply along with job growth. It is for this reason the Fed keeps using the term “soft landing.” They want to reduce demand which will slow the economy, job growth, and hopefully inflation. However, they do not want to slow it too much and cause a deep recession. On Thursday, Jerome Powell summed up the Fed’s task:

“We need to act now, forthrightly, strongly as we have been doing. It is very important that inflation expectations remain anchored. What we hope to achieve is a period of growth below trend.”

Soft Landing Insurance

The question facing investors is, what if the Fed does not achieve a “soft landing?” To help answer the question, we share advice from Lance Roberts. In his latest article, Recession Signals Abound as Fed Hikes Rates, he states:

While there is a possibility that the economy could avoid a “recession,” those odds are slim at best. Therefore, as investors, we should at least prepare for a storm and then cross our fingers and hope for the best. The guidelines are simplistic but ultimately effective.

- Raise cash levels in portfolios

- Reduce equity risk, particularly in high beta growth areas.

- Add or increase the duration in bond allocations which tend to offset risk during quantitative tightening cycles.

- Reduce exposure to commodities and inflation plays as economic growth slows.

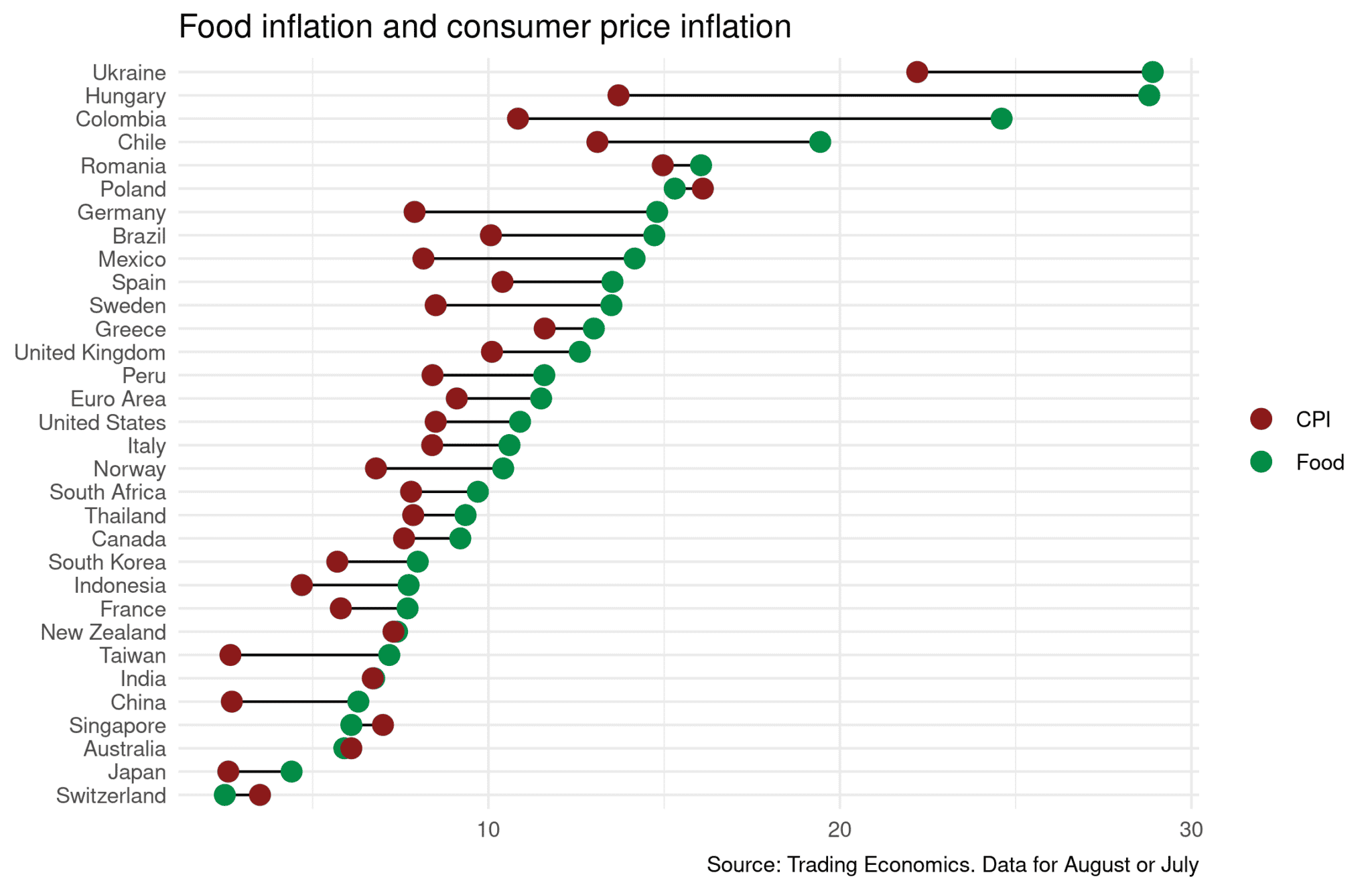

Global Food Inflation

The graph below shows that food inflation is running much hotter than broader inflation in almost all countries. Switzerland, Singapore, and Poland are the only three countries in which food inflation is less than CPI, and in those cases, it is only by a narrow margin. Food constitutes a large percentage of purchases for poorer people and nations. As such, if high food inflation persists, we should become increasingly concerned about the geopolitical ramifications of mass riots and political unrest, similar to what we see in Sri Lanka.

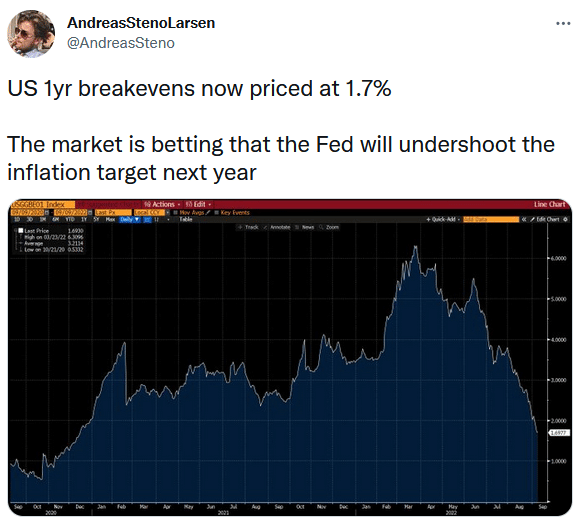

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read