At the Jackson Hole Summit, Jerome Powell made it clear the Federal Reserve remains focused on combatting inflation despite recession signals rising in tandem. To wit:

“Restoring price stability will take some time and requires using our tools forcefully to bring demand and supply into better balance. Reducing inflation is likely to require a sustained period of below-trend growth. Moreover, there will very likely be some softening of labor market conditions. While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses. These are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain.”

While the Federal Reserve is focused on fighting inflation and willing to cause “some pain” to achieve victory, they hope to do so without evoking a recession. Such may be a challenge for two primary reasons:

- The Fed remains focused on lagging economic data, such as employment, which are highly subject to future revisions, and;

- Changes to monetary policy do not show up in the economy until roughly 9-12 months in the future.

The second challenge is the most important.

There is little doubt we are amidst an economic slowdown. With the Federal Reserve focused on combatting inflation by tightening monetary policy, thereby slowing economic demand, logic suggests that economic data trends will continue to decline.

As the Fed continues to hike rates, each hike takes roughly 9-months to work its way through the economic system. Therefore, the rate hikes from March 2020 won’t show up in the economic data until December. Likewise, the Fed’s subsequent and more aggressive rate hikes won’t be fully reflected in the economic data until early to mid-2023.

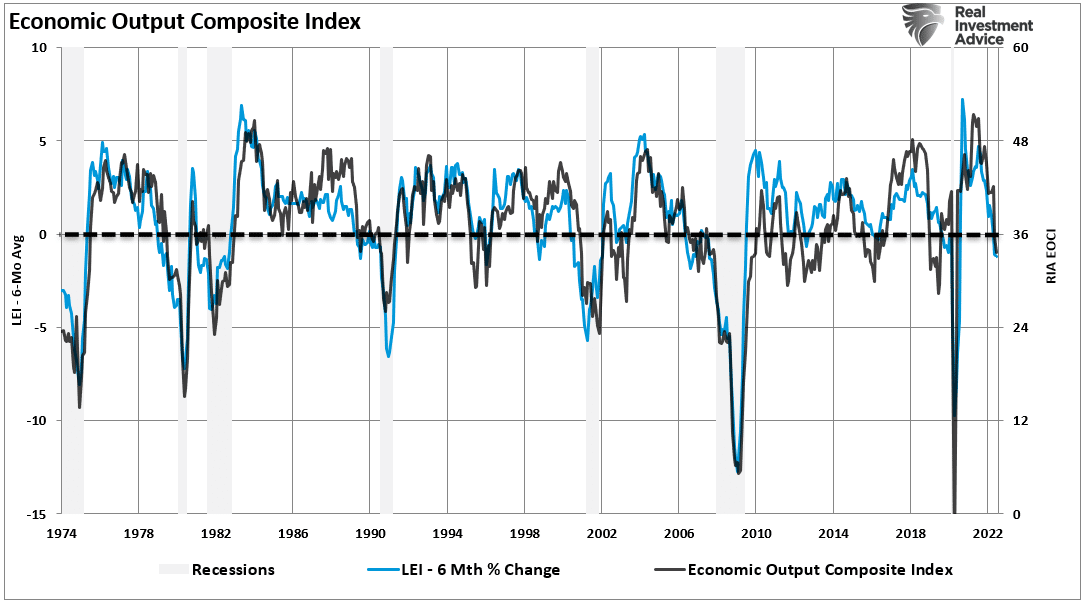

Given the Fed manages monetary policy in the “rear view” mirror, more real-time economic data suggests the economy is rapidly moving from economic slowdown toward recession. The signals are becoming more apparent, as shown by the 6-month rate of change of the Leading Economic Index.

As the Fed hikes at subsequent meetings, those hikes will continue to compound their effect. We will review three other recession signals that suggest the Fed will make a policy mistake.

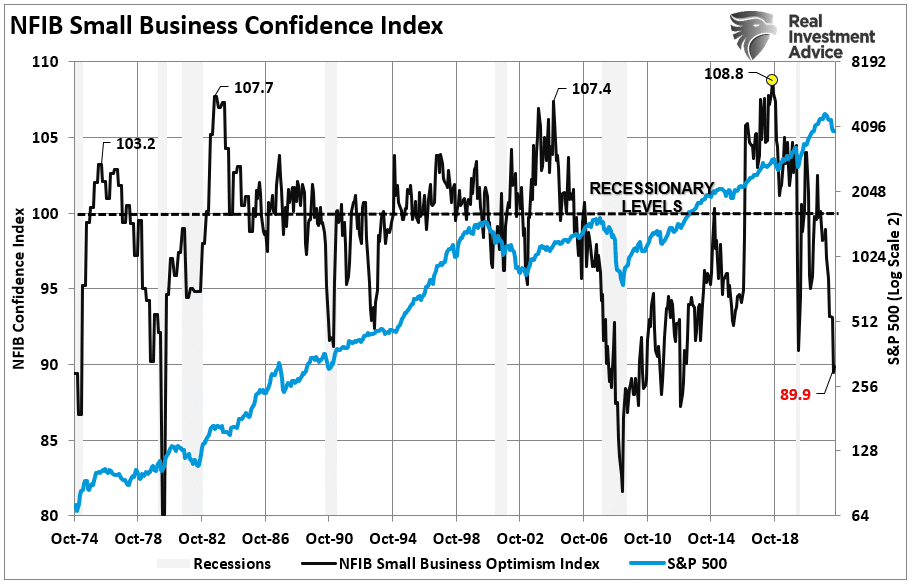

NFIB Survey

Small business sales are the lifeblood of the economy. We have written previously about the importance of small businesses relating to employment, incomes, economic growth, and even the stock market.

Since the last update in June, the NFIB Small Business sales and sentiment measures have only deteriorated further. Despite a surging stock market in July and August, along with suggestions the economy will avoid recession, the data continues to suggest differently if historical precedents hold.

For example, overall confidence expressed by the members of the National Federation of Independent Business (NFIB) owners is at levels historically associated with deep recessions and bear markets.

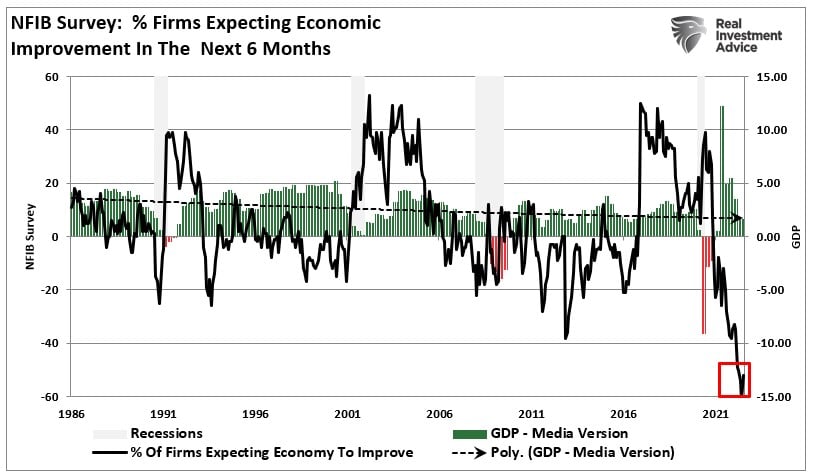

Since small businesses drive the economy, employment, and wages, what the NFIB says is highly relevant to the actual economy. Furthermore, their “confidence” in the economy is critical to the ongoing support of employment, capital expenditures, and wages. As shown, the economic view of NFIB members over the next 6-months has plummeted to record low levels. Such does not bode well for additional employment, capital expenditures, or increased wages.

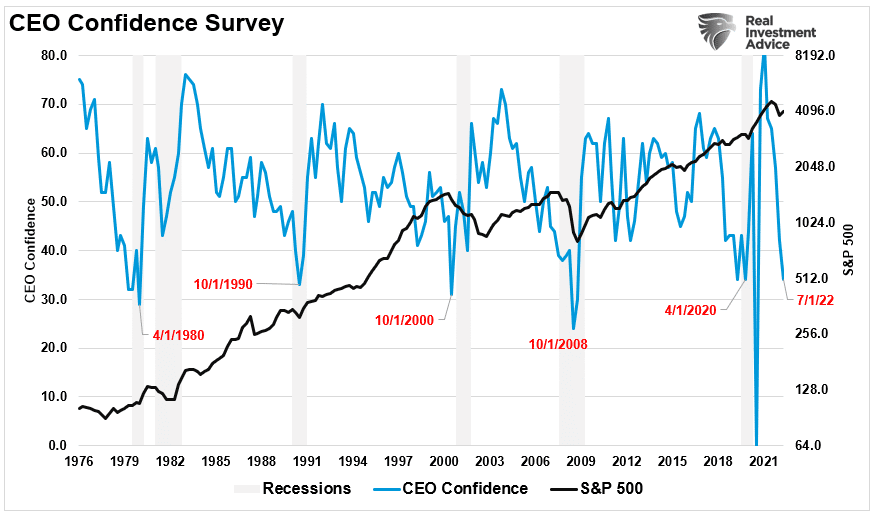

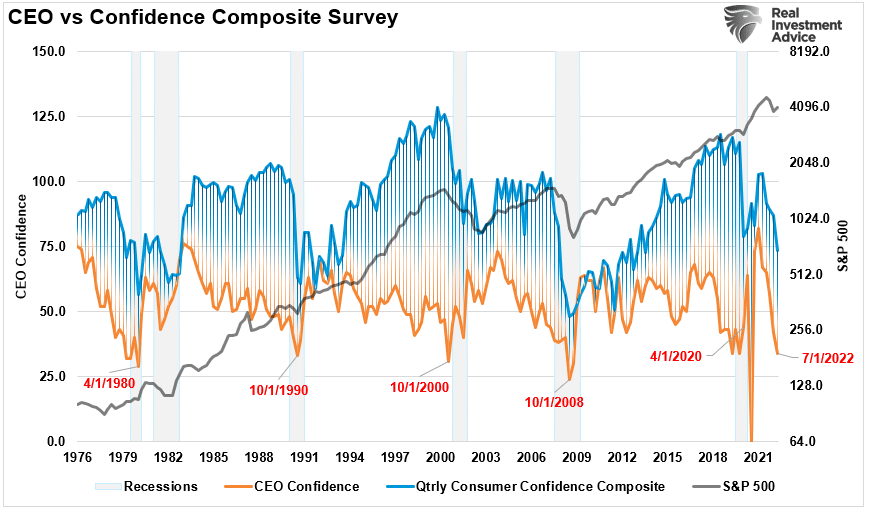

But it is not just small business confidence that is a recession signal. CEO confidence of the world’s largest multinational corporations across all industry sectors has soured.

CEO Confidence

“The Conference Board Measure of CEO Confidence™ in collaboration with The Business Council declined for the fifth consecutive quarter in Q3 2022. The Measure now stands at 34, down from 42 in Q2. The Measure has fallen deeper into negative territory, to lows not seen since the start of the COVID-19 pandemic in 2020, but consistent with prior contractionary periods. (A reading below 50 points reflects more negative than positive responses.)

“CEOs are now preparing for the near-inevitability of a US recession by year-end or in 2023.” – The Conference Board

Given that corporate revenues and earnings come from the consumption of individuals, it should be of no surprise there is a high correlation between the CEO and Consumer Confidence Composite indices. As the economy weakens, CEOs will try and retain employment as long as possible until they eventually must reduce workers. Such is why there is a lag between the consumer confidence composite and the CEO survey. However, that lag is a pre-recessionary indicator and currently suggests the risk of an impending recession.

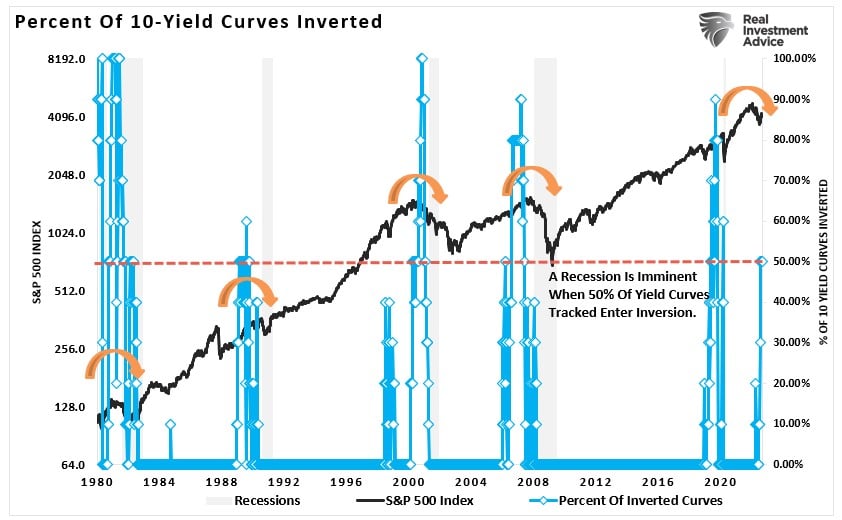

Yield Curve Inversion

As noted above, both recession signals are sending a warning. Both have near-perfect track records.

However, yield curve inversions are another indicator with a new perfect track record of recession predictions. Currently, 50% of the 10-spreads we track are inverted. As such, it is worth paying attention to the data. If the number of inversions increases, such will confirm that a recession is more likely. However, crucially, the inversion is only the warning of a recession. When the yield curves UN-invert, such will be the recognition of the recession. Such will occur as money shifts from short-term risk assets to the safety of long-duration treasury bonds.

Crucially, as the Fed hikes rates, more curves will invert.

Most importantly, with economic growth slowing rapidly, inflation running at the highest levels since 1980, and consumers tapped out, recession risk is likely higher than many realize.

However, it is worth noting that using the “yield curve” as a “market timing” tool is unwise, but dismissing the message entirely is just as foolish.

Preparing For A Policy Mistake

From our perspective, the risk of recession remains elevated, particularly as the Fed aggressively hikes rates and restricts monetary accommodation.

While there is a possibility that the economy could avoid a “recession,” those odds are slim at best. Therefore, as investors, we should at least prepare for a storm and then cross our fingers and hope for the best. The guidelines are simplistic but ultimately effective.

- Raise cash levels in portfolios

- Reduce equity risk, particularly in high beta growth areas.

- Add or increase the duration in bond allocations which tend to offset risk during quantitative tightening cycles.

- Reduce exposure to commodities and inflation plays as economic growth slows.

If a recession occurs, the preparation will allow you to survive the impact. Protecting capital from the inherent destruction will mean less time spent getting back to even after the storm passes.

Alternatively, it is relatively straightforward to reallocate funds to equity risk if we avoid a recession or if the Fed does revert to monetary accommodation.

Investing during a recession can be dangerous, mainly when elevated valuations are present across all asset classes. However, you can take some steps to ensure that increased volatility is survivable.

- Have excess emergency savings so you are not “forced” to sell during a decline to meet obligations.

- Extend your time horizon to 5-7 years, as buying distressed stocks can get more distressed.

- Don’t obsessively check your portfolio.

- Consider tax-loss harvesting (selling stocks at a loss) to offset those losses against future gains.

- Stick to your investing discipline regardless of what happens.

While the media tries to pick the next market bottom, it is better to let the market show you. You will be late, but you will have confirmation the selling is over.

But, if I am correct, we have more work to do first.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read