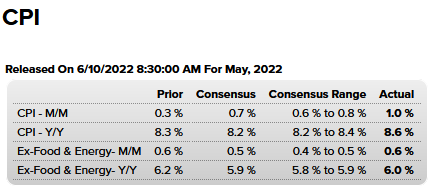

The BLS CPI Inflation report surprised the markets, coming in hotter than expected. The surprises were in the monthly and annual CPI numbers, as shown below. Interestingly, however, the core CPI data, which excludes food and energy, was in line with expectations and lower for the second month in a row. The Fed prefers core inflation data as it views food and energy prices as volatile and not representative of longer-term inflation trends. Below are a few key statistics worth sharing.

- 71% of the items in the CPI report are increasing at an annualized rate of 4% or greater.

- Real wages are now falling by 3% and have been negative for 14 months running.

- The lower-income classes are suffering as necessities like food, energy, and shelter led the CPI index higher.

- Shelter represents about a third of the CPI number and is now up 5.5% yearly. It still pales in comparison to other rent and home price measures.

- Used car prices are retreating. They are now up 16.1 annually versus a high of 45% six months ago.

Bottom line: inflation is stubborn, and the Fed has no choice but to hike rates by at least 50bps next week and in July. A stall in September is very unlikely.

What To Watch Today

Economy

- No notable reports are expected for release.

Earnings

Pre-market

- No notable earnings are expected for release.

Post-market

- Oracle (ORCL) to report $1.37 in profits with revenue growth of 7% per share.

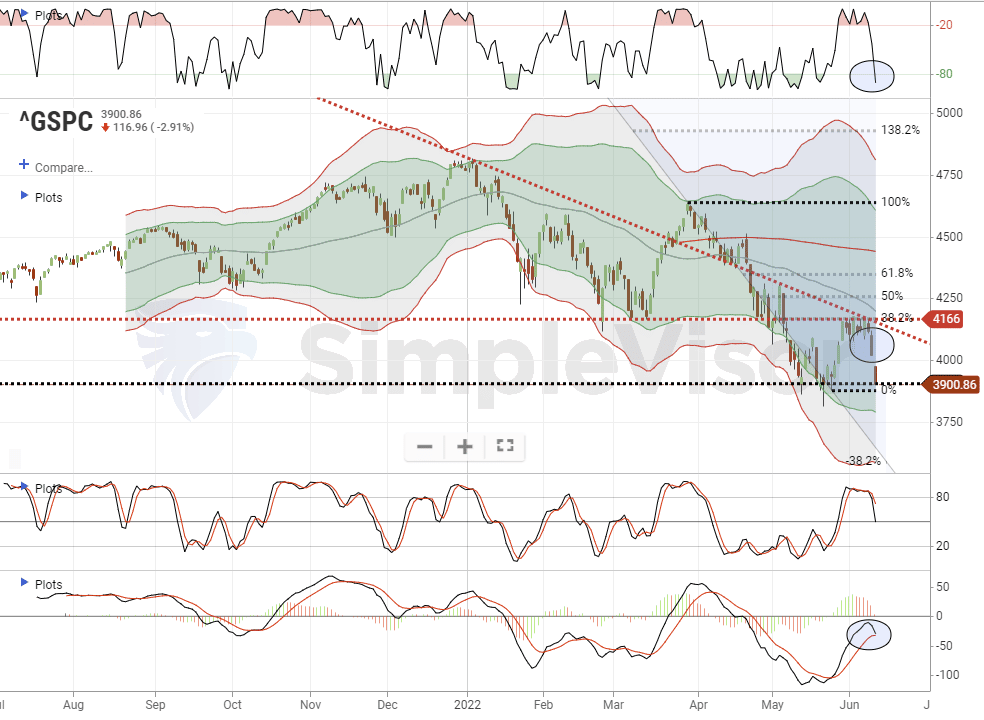

Market Fails At Important Resistance

Last week, we discussed how the reflexive rally that started mid-May ran into resistance at the first levels from the recent low. To wit:

“While the market did clear the 20-dma, the “trapped longs” headed to the exits at the initial 38.2% Fibonacci retracement level from the March highs. That level was also where previous important support for the February and April lows got broken.”

Unfortunately, the rally failed as recession risks from continued high inflation became evident.

We previously reviewed the market’s technical backdrop from a bullish and bearish perspective. While the short-term backdrop favored the bulls, the longer-term signals were bearish. Adding to the bearish backdrop is the tighter Fed policy and the reduction of market support as “quantitative tightening” begins.

Furthermore, the economic backdrop of high inflation and slowing economic growth certainly doesn’t give the bulls much to work with.

As shown above, our concern was that the longer the market remained in a tight trading range, the risk of a failed rally increased. While there was certainly room for the market to break to the upside, the multiple levels of resistance immediately overhead limited any advance. The failed rally now adds additional downward pressure on prices near term.

Therefore, from a risk management perspective, we continue to suggest using rallies to reduce exposure and raise cash. Given the failed rally, it is important the retest of the previous lows holds. A break of those lows will confirm the “bear market” is fully engaged.

The Week Ahead

The week ahead should be interesting. We get a break from data on Monday. On Tuesday, the BLS will release producer prices (PPI). Expectations are for an increase from last month. Wednesday features retail sales, which are expected to rise by .3%. While positive, such a reading is negative .7% when adjusted for the latest CPI report. At 2 pm, the Fed will release the statement from its FOMC meeting and new economic projections. Jerome Powell will follow it up with a press conference at 2:30.

Given Friday’s CPI report, we believe the Fed will hike rates by 50bps and continue with very hawkish rhetoric. The only possible surprise would be a decision to hike rates by 75bps or discuss it as a possibility for the late July meeting. Given the stubbornness of inflation, the economic damage it’s inflicting on much of the population, and growing political pressures, we now think 75bps may be appropriate at either meeting.

Jerome Powell will also speak on Friday. Markets will be on alert for anything that deviates from what we learn on Wednesday.

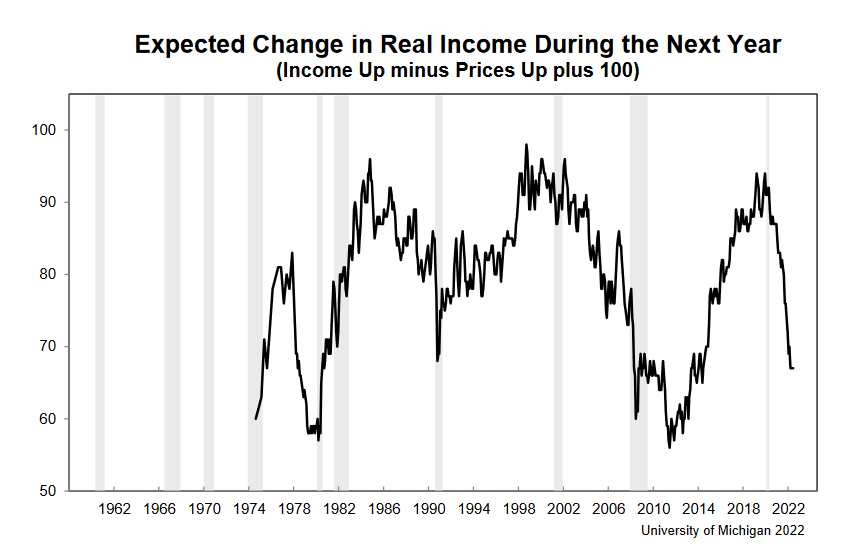

Consumer Sentiment is Plunging

The University of Michigan Consumer Sentiment Index fell to a record low of 50.2 versus a prior reading of 58.4 and expectations for a slight uptick. Driving the decline is an increase in one and five-year inflation expectations. Consumers now expect 3.3% inflation over the next five years, up from 3%. Per the report:

Consumer sentiment declined by 14% from May, continuing a downward trend over the last year and reaching its lowest recorded value, comparable to the trough reached in the middle of the 1980 recession. All components of the sentiment index fell this month, with the steepest decline in the year-ahead outlook in business conditions, down 24% from May. Consumers’ assessments of their personal financial situation worsened about 20%. Forty-six percent of consumers attributed their negative views to inflation, up from 38% in May; this share has only been exceeded once since 1981, during the Great Recession.

The report’s featured chart shows the sharp drop in real income expectations, which obviously weighs heavily on the ability to consume.

Yet Another Recession Warning

We apologize for the recent spate of grim recession forecasts but think its important to stay abreast of economic conditions as this time is different. As a result of high inflation, the investment environment has risks that were not present in prior recessions. Typically, in a slowing economy, like today, the Fed would start spewing more dovish rhetoric. For instance, if inflation were tame, they would likely take 50bps of rate hikes off the table and say future rate hikes are contingent on economic growth. However, the Fed is stuck administering aggressive rate hikes and balance sheet reductions because of high inflation. Less hawkish rhetoric is unlikely until the economy weakens considerably and inflation retreats. Today’s CPI report does not help matters. Simply, the Fed’s ability to “save” the market is compromised.

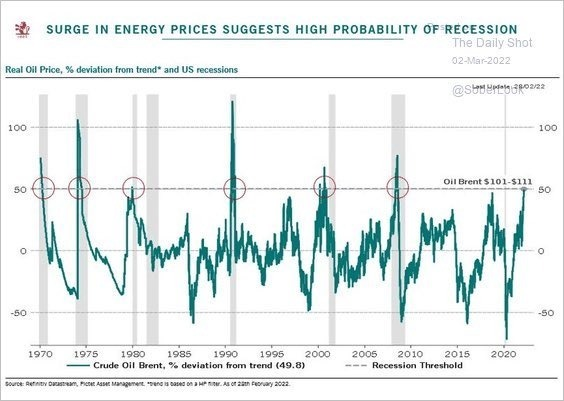

With the understanding that this time is different, we share another recession warning. The graph below from Pictet Asset Management and the Daily Shot shows that when the real price of oil is 50% or more above its trend, a recession has occurred or was about to happen. Based solely on this graph, we should expect a recession within the next year.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read