Stock investors are screaming “AAUGH!” as Jerome Powell duped them again. In one of the more iconic scenes in Charlie Brown, his sister Lucy holds a football for him to kick. Charlie Brown runs up to kick the ball, and Lucy pulls it away. Charlie Brown vows never to trust her again, yet he always does.

Investors are falling for the same trick. Investors get bulled up after each of the last few Fed meetings. They expect the Fed to relent on its super-hawkish policy. They presume that they must be near the end because the Fed has hiked so much. However, they fail to listen to the Fed. The Fed is demanding concrete proof that inflation is falling rapidly. It is not! They want the labor market to loosen up and crush a potential price-wage spiral. It is not! Until Powell sees evidence of consistently lower prices and a higher jobless rate, the Fed will continue to pull the pivot ball from investors. Don’t be Charlie Brown and presume the next meeting will be different solely because the Fed is closer to its terminal Fed Funds rate.

What To Watch Today

Economy

- 8:30 a.m. ET: Change in Nonfarm Payrolls, October (195,000 expected, 263,000 prior)

- 8:30 a.m. ET: Change in Private Payrolls, October (200,000 expected, 288,000 prior)

- 8:30 a.m. ET: Change in Manufacturing Payrolls, October (12,000 expected, 22,000 prior)

- 8:30 a.m. ET: Unemployment Rate, October (3.6% expected, 3.5% prior)

- 8:30 a.m. ET: Average Hourly Earnings, month-over-month, October (0.3% expected, 0.3% prior)

- 8:30 a.m. ET: Average Hourly Earnings, year-over-year, October (4.7% expected, 5.0% prior)

- 8:30 a.m. ET: Average Weekly Hours All Employees, October (34.5 expected, 34.5 prior)

- 8:30 a.m. ET: Labor Force Participation Rate, October (62.3% expected, 62.3% prior)

- 8:30 a.m. ET: Underemployment Rate, October (6.7% prior)

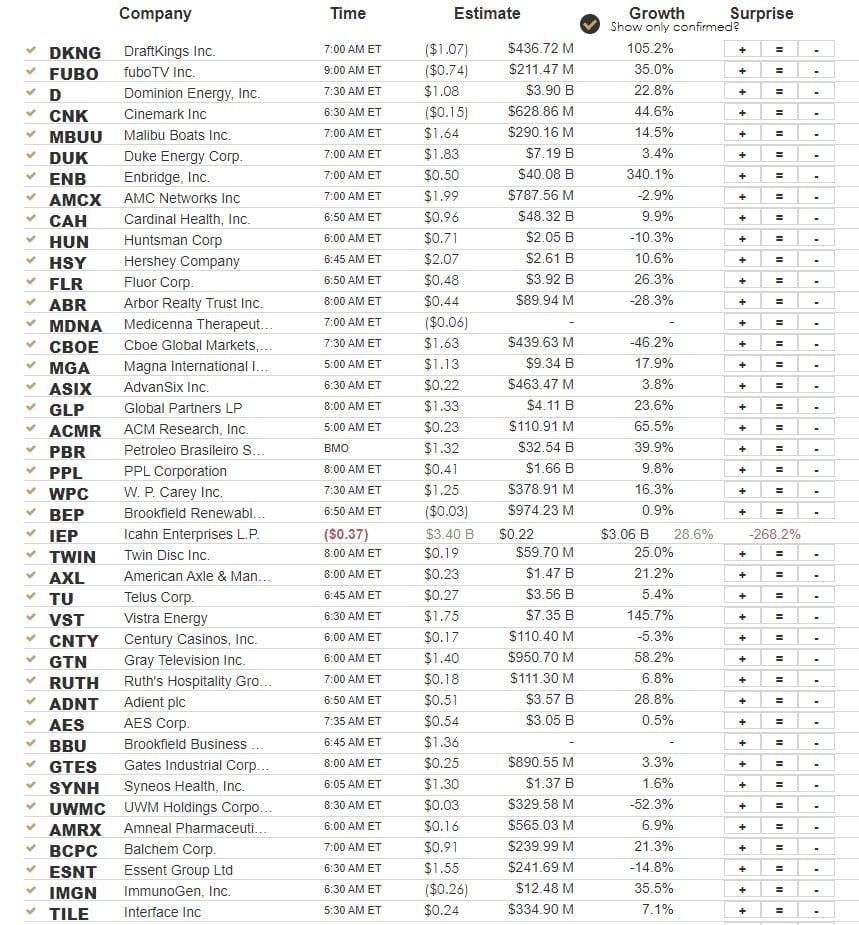

Earnings

Market Trading Update

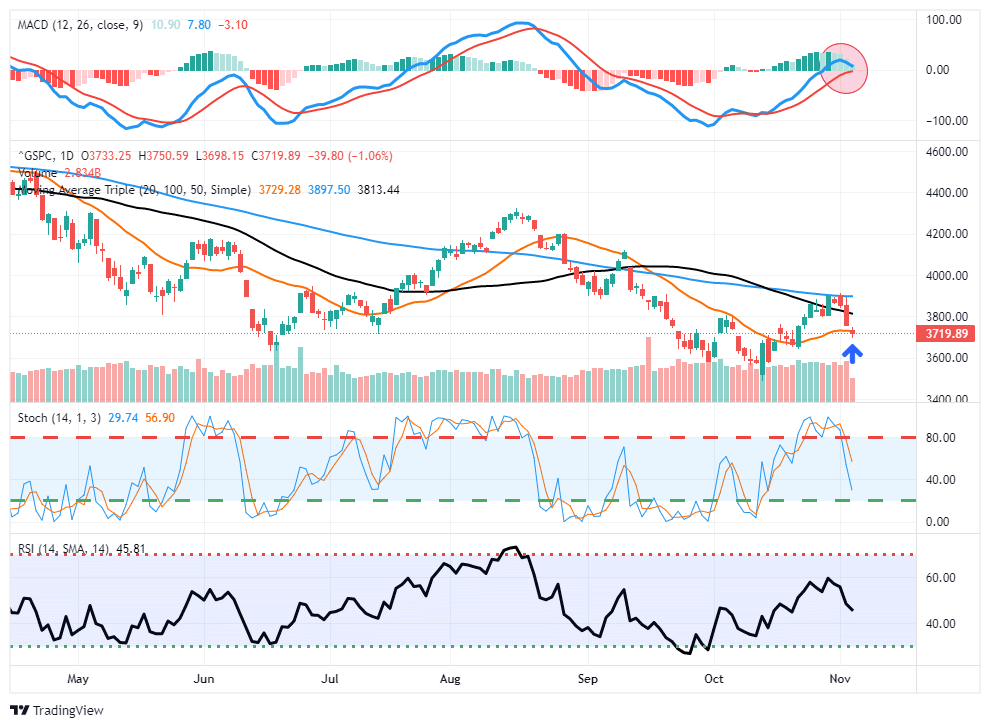

The market traded off yesterday as concerns over a continued “hawkish” Fed put the bears back in charge of the market. After the recent 4-week bullish rally, the trade is currently lower. The good news, at the moment, is the market managed to hold onto the 20-dma yesterday, although just barely. If the market sells off again today, the retest of recent lows becomes increasingly likely. This morning we have the jobs report, which will further incite the Fed to remain aggressive on rate hikes if it comes in exceptionally strong. We reduced equity exposure again yesterday, and depending on what happens following this morning’s employment report, may take further actions.

Also concerning is the MACD signal, which is set to trigger a “sell signal” if market weakness continues. Today will be a critical day for the bulls if they are going to maintain control.

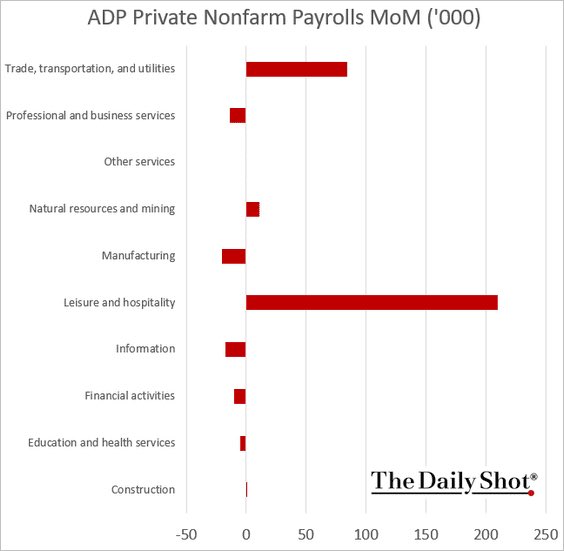

The ADP Jobs Report is Strong, But…

The ADP jobs report, a precursor to today’s BLS labor report, was stronger than expected at +239k. However, looking beneath the surface of the data leaves much to be desired. Nearly 100% of job growth came from the leisure and hospitality sectors. Most jobs in those sectors are low-paying and quite often temporary jobs. Of the other nine sectors, five were lower, and two were slightly higher. While labor data, in general, remains robust, there should be concerns that the quality of job growth is poor.

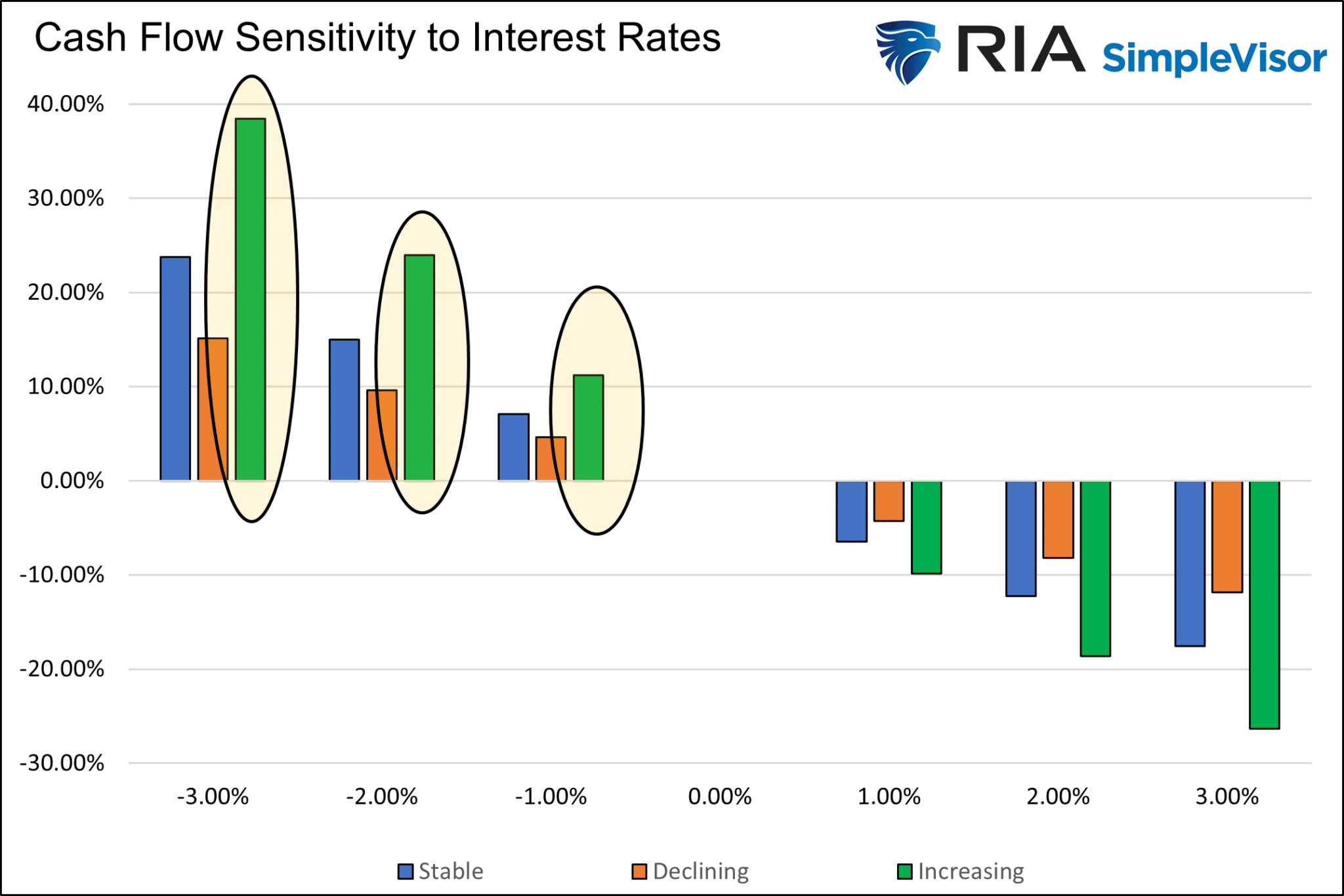

Measuring Stock Sensitivity to Interest Rates

On Wednesday, we published Finance is at Fault. The article quantifies how higher interest rates weighed on stock prices this year. Understanding the relationship between stock prices and interest rates helps us better formulate what type of stocks may do better when interest rates reverse course.

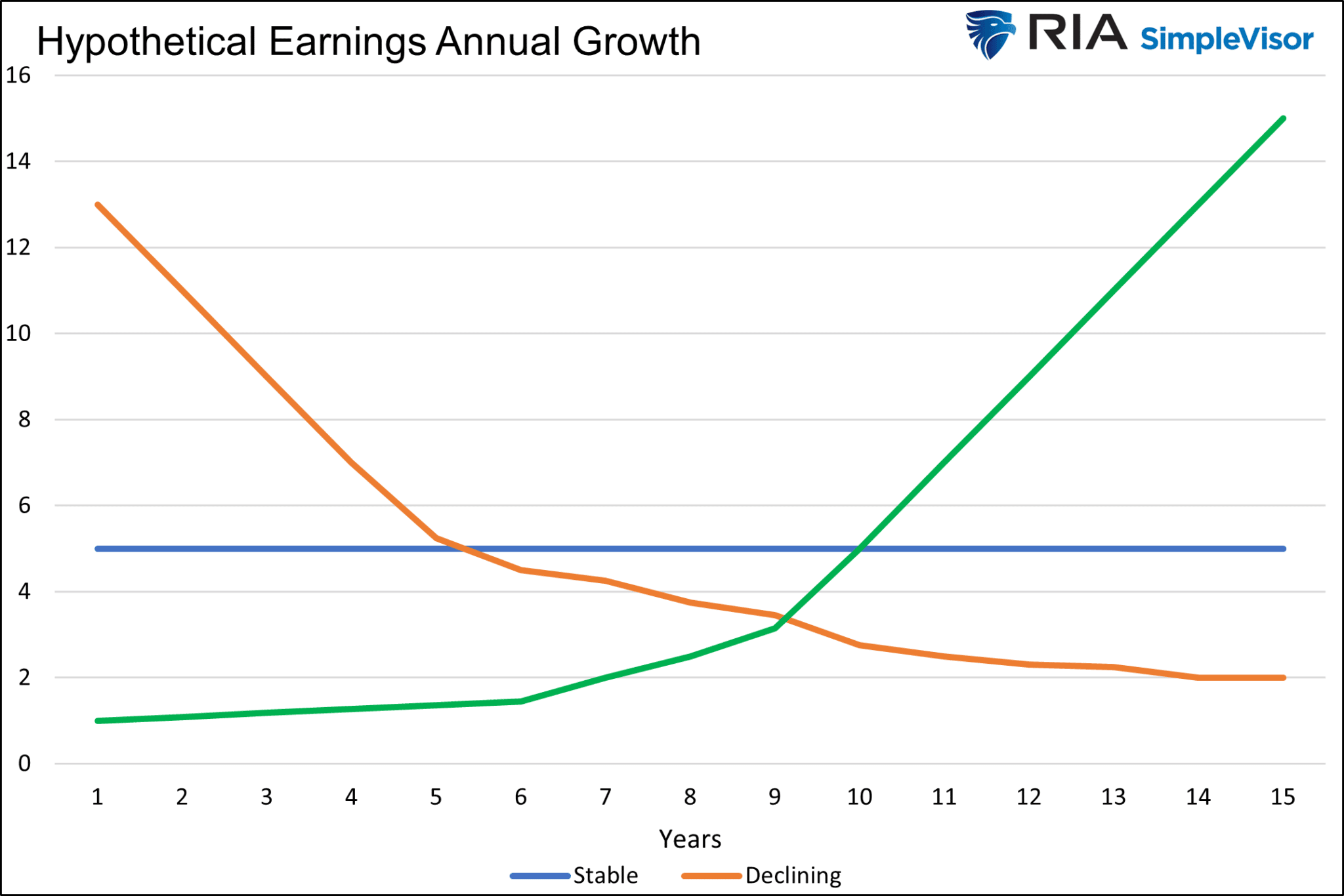

The trajectory of future earnings (cash flows) plays a critical role in calculating how sensitive stock prices are to changes in interest rates. Simply, the more front-loaded the earnings, the less sensitive. This helps explain why many value stocks outperformed growth stocks as interest rates rose this year. To further clarify this point, we compare three hypothetical companies with vastly different projected growth rates.

With interest rates likely peaking, and the probable path over the coming year lower, what type of stocks will benefit most from lower interest rates? Per the graph below using our hypothetical companies shown above, growth companies with increasing and longer-dated cash flows should rise the most in a lower-rate environment.

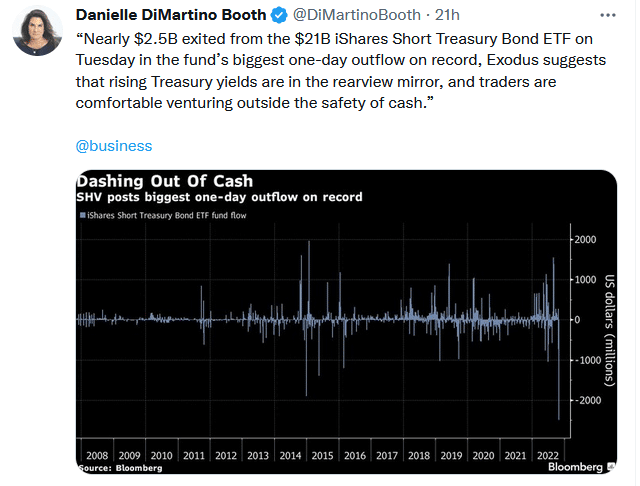

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read