We have written many articles and commentaries forecasting interest rates. The analysis has used prior and current inflation and economic activity. Additionally, we have looked at market data on inflation expectations, Fed Funds futures, and other factors that influence interest rates. Today, we add an unorthodox factor to the list: cash cows.

This article introduces a unique way to imply where dividend investors think interest rates will be in the future. The impetus for this article came from a recent SimpleVisor Friday Favorites article in which we reviewed the Campbell Soup Company (CPB). Friday Favorites typically analyzes a company’s fundamental and technical conditions and valuations.

This time, however, because the company was a cash cow, we took it further and studied its dividend yield. In the process, we arrived at an implied ten-year U.S. Treasury yield based on the current and historical spread between Campbell’s dividend yield and the ten-year U.S. Treasury yield.

Implying future interest rates based on CPB is somewhat laughable. However, implying future interest rates on a larger population of cash cows may be more telling.

What Is A Cash Cow?

Cash cow is a term dairy farmers use to describe mature cows that generate milk regularly with minimum maintenance.

Wall Street adopted the term cash cow to label companies that deliver reliable cash flows (milk), require little investment (maintenance), and have little to no sales and earnings growth (mature).

CPB is a good example of a cash cow. Not surprisingly, the soup business is a low-growth venture; therefore, it has negligible earnings and sales growth. Moreover, it has consistently paid dividends since 1989 and produces plenty of excess cash flow that should ensure future dividend payments.

While CPB lives up to the definition of a cash cow, we do not analyze it in this article as its dividend yield is below our threshold dividend yield. However, we did find fifteen other cash cows, which we will share.

Screening For Cows

In this analysis, we used the following screening criteria:

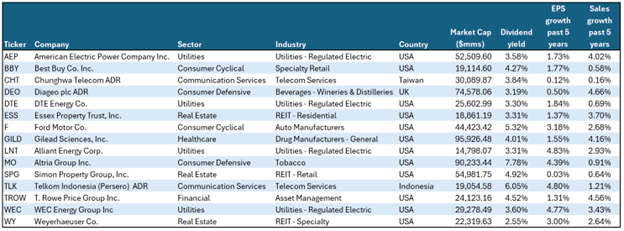

- Market Cap > $10 billion

- Five-Year EPS Growth < 5%

- Five-Year Sales Growth < 5%

- Dividend Yield > 2.50%

- Ten Years of Consecutive Dividend Payments

The table below shows the fifteen stocks that met the screening criteria.

What Can We Imply With Dividend Yields?

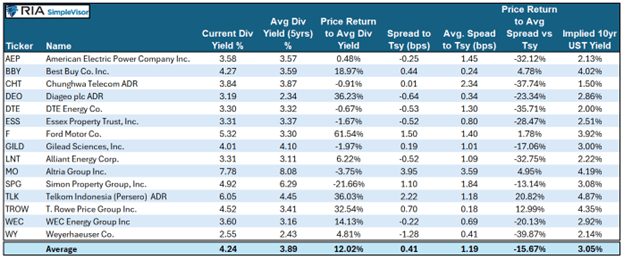

The following table shares our analysis of the fifteen companies.

After the ticker and name of each respective stock, we show the current dividend yield and the average dividend yield over the last five years. The next column, “Price Return to Avg. Div. Yield”, quantifies how much the stock price would have to change to bring the current dividend yield in line with the five-year average. Obviously, a company can increase its dividend or cut it, which would change the return.

The first set of analyses, which we just described, helps us compare the current dividend yield to recent yield history on an absolute basis.

Since some investors consider bonds a substitute for dividend stocks, we must also do a relative analysis of dividend yields. In other words, has the dividend yield risen accordingly with interest rates? To do this, we calculate the current dividend yield minus the current ten-year yield (“Spread to Tsy”). We also compute the average Spread to Tsy. for the last five years. With this data, we can calculate how much the stock price would have to change to make the dividend yield equal to its five-year average spread to Treasury yields.

Lastly, assuming the dividend yield reasonably predicts where rates are headed, we can imply where the ten-year U.S. Treasury yield may be in the near future. We share this in the column furthest to the right.

Cash Cow Conclusions

While there are many stories within the table, we focus on the averages of the fifteen stocks in this article. The current dividend yields are slightly higher than average. This is primarily a function of investors shunning dividend stocks in favor of higher-yielding bonds or stocks with better performance. Declining stock prices push the dividend yield higher, helping them stay competitive with bonds. Dividend yield is only one of many factors determining the price; however, it is a much more critical price determinant for cash cows than other stocks.

While the dividend yield may be higher than its norm for the last five years, it has not kept up with Treasury yields. Based solely on the yield spread, prices, on average, would need to fall by about 15% to bring the meager .41% spread over the 10-year UST back to normal.

But might stock investors be locking in higher dividend yields, anticipating a lower interest rate/yield environment? If so, our cash cows imply the 10-year UST yield would need to fall to 3.05%. Doing so will bring the average dividend yield spread versus Treasury yields back to its average.

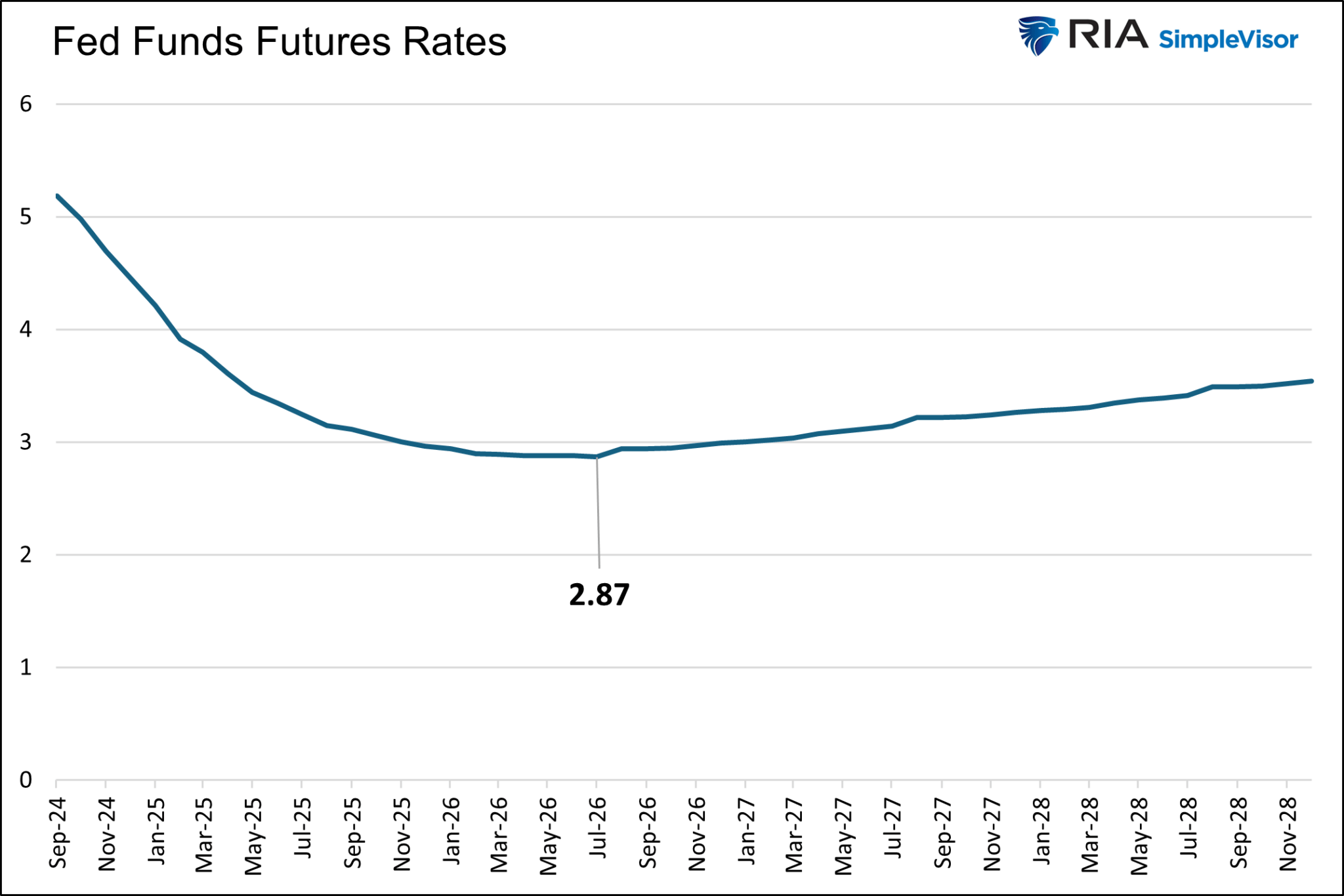

Coincident or not, the market also thinks that the Fed Funds rate will trough at 2.87% when the coming rate-cutting cycle ends.

Summary

Between our article Fed Funds Futures Offer Bond Market Insights and the cash cows we highlight, the Fed Funds futures market and stock market appear to be on the same page regarding future interest rates.

Some may find comfort in their similar predictions. However, caution is warranted. The bond market often underappreciates how much the Fed will cut interest rates. Furthermore, it has been proven to be a poor judge of where long-term Treasury bond yields will fall. Quite often, yields fall much more than anticipated. If this is again the case, some of our cash cows may see decent price appreciation if their dividend yield declines with lower bond yields.