Bullish or bearish? What is the case for the market now?

As we noted previously, having a proper market perspective is essential in avoiding investing mistakes over time. However, another trap we potentially fall into is “confirmation bias,”

“Experts in the field of behavioral finance find that confirmation bias applies to investors in notable ways. Because investors seek out information that confirms their existing opinions and ignore facts or data that refutes them, they may skew the value of their decisions based on their own cognitive biases. This psychological phenomenon occurs when investors filter out potentially useful facts and opinions that don’t coincide with their preconceived notions.” – Investopedia

With the Russia/Ukraine conflict raging, energy prices soaring, inflation spiking, the Fed hiking rates, and pressure on asset prices, it is reasonable to have a more “bearish” view. The problem is getting trapped into that view to the point we miss the eventual turn to a more “bullish” outlook.

One of the biggest challenges investors always face is allocating capital to markets once a correction occurs. The concern is purely emotional as investors worry the market may continue to decline. While specific reasons suggest a deeper correction is possible, other factors support a more positive outcome.

The emotional biases of being either bullish or bearish, primarily driven by the media, keep you from truly focusing on long-term outcomes. Instead, you either worry about the next downturn or are concerned you are missing the rally. Therefore, you wind up making short-term decisions that negate long-term views.

Understanding this is the case, let’s look at the markets from a bullish and bearish perspective. We can balance our views on potential outcomes and investment allocations.

The Bullish Case

Sentiment

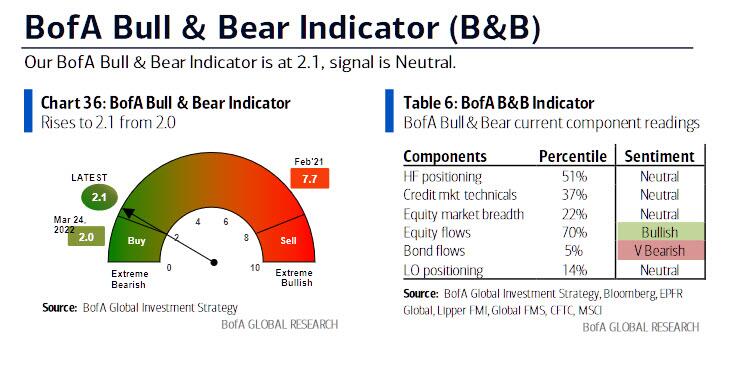

Even after a 10% rally from the March lows, BofA’s sentiment indicator is still pushing more extreme bearish conditions. Which, ironically, is bullish as it tends to be a contrarian indicator.

However, when it comes to that sentiment, it tends to change quickly. Such was summed up well by my colleague Channing Smith, CFA of Jackson Hole Capital Partners. To wit:

“For years when we have had these bouts of volatility or scares, however, we inevitably see these frantic bullish reversals with a new bullish narrative quickly rising from the ashes. The negatives somehow get spun into positives each time the markets rally.

- Yield Curve Inversion – This is bullish. Stocks are up an average of 11.5% one year after an inversion

- Inflation is now good for stocks because equities are the best hedge against inflation

- Higher interest rates are good for stocks because asset flows into equities will increase

- The Fed balance sheet is now over $9 trillion and despite talking about a reduction, they haven’t done so yet.

- The war in Ukraine resulted in international flows coming into US markets which is a positive

- The economic slowdown isn’t evident as both consumer and corporate balance sheets are flush with cash.

- Selling of equities is not an option given no alternative to low yields.

Channing is correct. The bullish narrative is back and could support higher asset prices as that overall negative sentiment gets reversed.

Markets Are Back Above Resistance

That negative sentiment and positioning provided the “fuel” for a robust counter-trend rally. That market rally pushed prices above respective 50- and 200-dma’s, again frustrating the bears. If the market can work off the overbought condition without violating support, the bulls will regain control of the narrative. At least for now.

As noted in “Inverted Yield Curve History:”

“As we head into the end of the month, a further push to the upside is not out of the question as mutual funds, pensions, and investment firms rebalance portfolios for the end of the quarter. The recent surge in interest rates has decreased the bond side of allocation funds. Also, the decline in the markets since the beginning of the year has fund managers at reduced equity levels, overweight cash, and negatively biased.”

Historical Performance

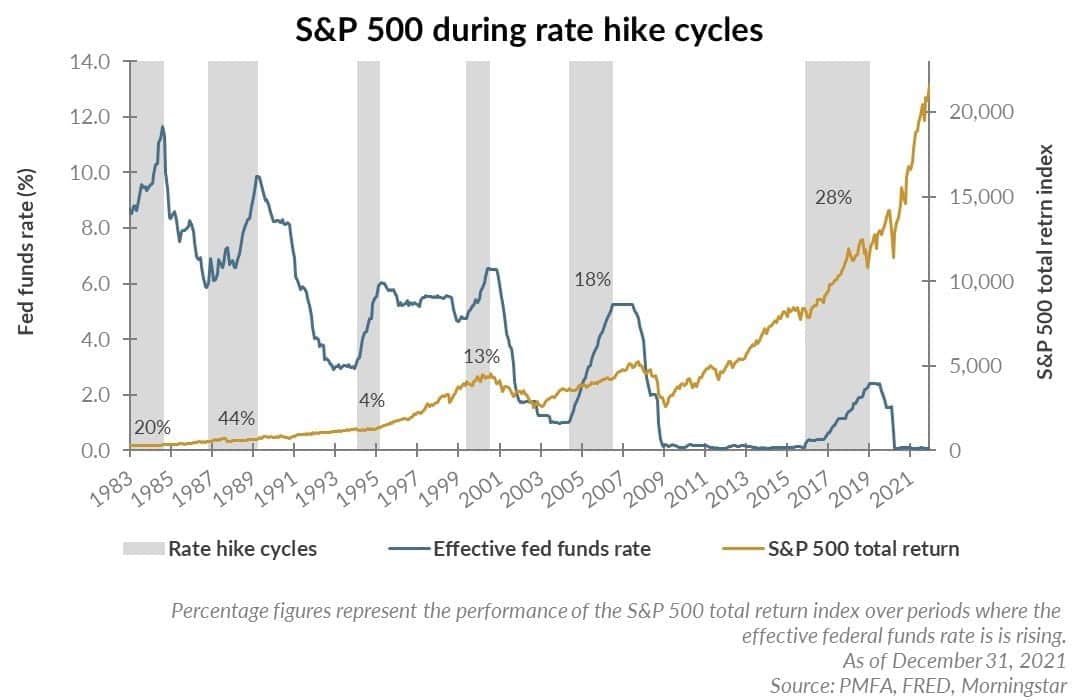

“This time is always different” in terms of the economy, inflation, politics, and many other variables that potentially affect market outcomes. However, as shown in the chart below via Plante Moran, stock performance tends to be positive during periods of Fed rate hikes.

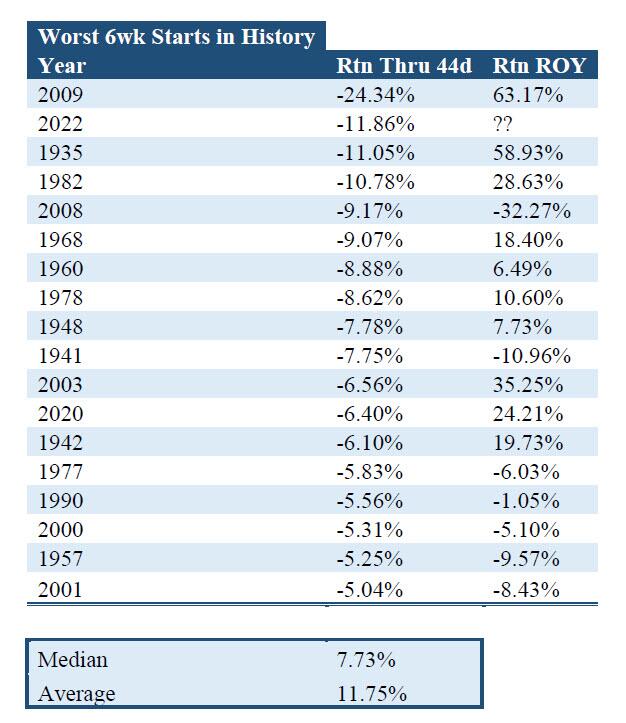

Furthermore, given the weakness since the start of the year, as noted by Goldman Sachs, returns following weak starts are biased to the upside.

Other issues that feed into the bullish case are:

- High investor cash levels

- Corporate stock buybacks are pushing a record

- Global equity fund flows remain strong.

- Earnings expectations remain very positive.

While there is no guarantee that stocks will continue to rise, the bulls currently carry solid arguments for being long equities.

However, the bears have an equally compelling case for remaining cautious.

The Bearish Case

Liquidity Reversal

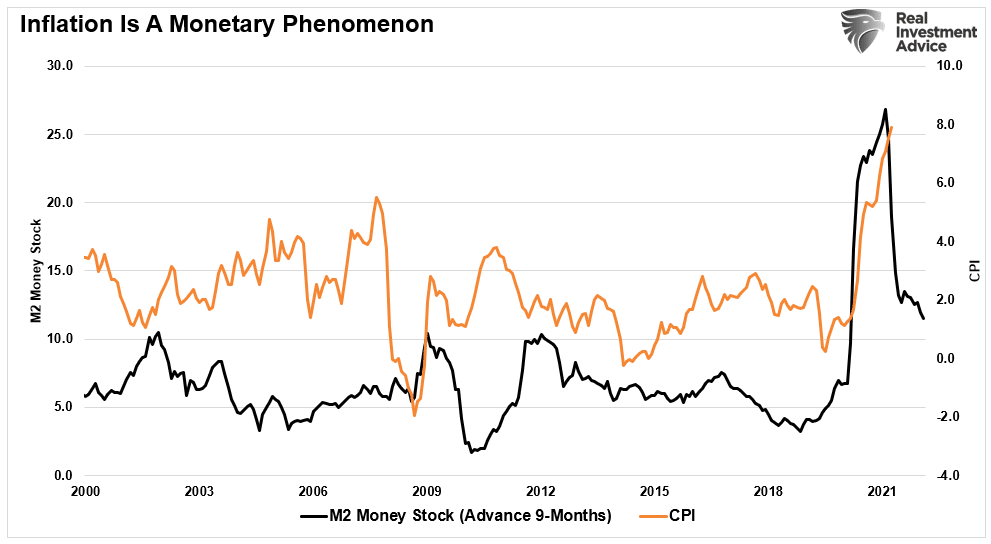

The massive surge of liquidity poured into the economy from $5 trillion in government spending has now ended. That enormous surge in M2 (money supply) created the inflationary surge we are seeing now and supported rampant market speculation.

The problem is that liquidity, which pulled forward roughly 3-years of consumption, is reversing. As such, consumption will slow as savings are depleted, slowing economic growth and deflationary pressures.

Earnings Recession

As economic growth and inflationary pressures slow, earnings will fall. Given that valuations are still elevated by historical measures, stock prices will have to adjust for slowing expectations. Already, forward estimates are on the decline as current economic data weakens. Given the high level of inflation that companies are finding more challenging to pass on, bottom-line earnings will erode.

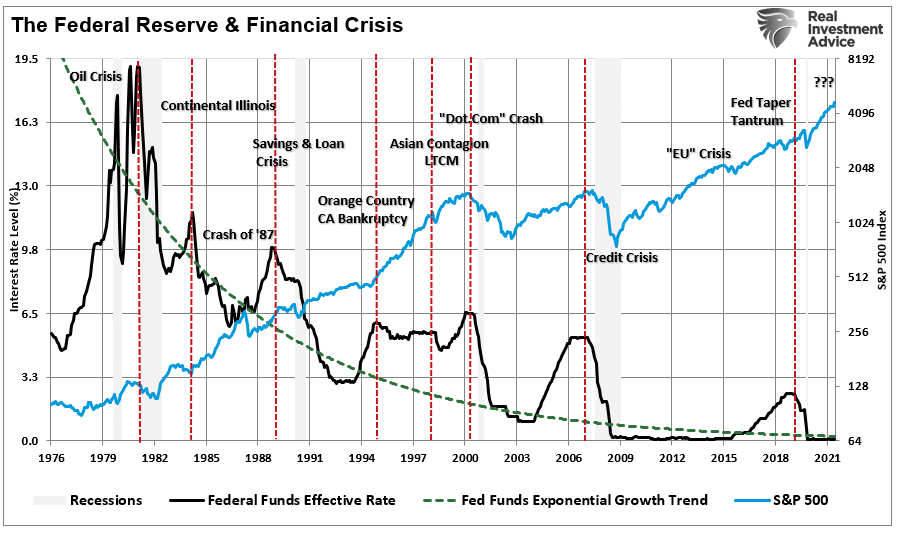

The Fed Is Tightening Monetary Policy

One of the bullish points was that markets tend to do well in the early stages of the rate hiking cycle. That is true, but there is a caveat. Each time the Fed started rate hikes previously, economic growth was strong, and inflation was nascent. This time, inflation is rampant and economic growth is weak. While historically, Fed rate hikes coincided with rising markets, such as the case until those rate hikes “broke” something economically. As noted recently, there is no historical precedent to the contrary.

Other issues that feed into the bearish case are:

- Inflation is surging

- There are many “trapped longs” in the market.

- Geopolitical risk remains high.

- High probability of a Fed “policy mistake.“

- Interest rates are rising, which will slow economic growth.

- Market liquidity remains low

- The Fed has ended Q.E., and they will reduce their balance sheet.

- Consumer confidence (specifically the spread between current and future expectations).

While there is no guarantee that stocks will continue to fall, the bears have a solid foundation for being cautious about the markets.

You Don’t Have To Pick A Side.

So what do you do?

We believe there is enough to the bullish case to warrant a short-term rally, as discussed previously. However, the longer-term dynamics are bearish.

But here is the crucial point – you don’t have to “choose.”

While many think you have to be either “bullish” or “bearish,” the reality is you don’t. In the short term, we can be “bullish” with our equity positioning. However, we can also be “bearish” in our longer-term views.

Regardless of whether you are bullish or bearish, there are some guidelines you can follow.

- Tighten up stop-loss levels to current support levels for each position. (Provides identifiable exit points when the market reverses.)

- Hedge portfolios against significant market declines. (Non-correlated assets, short-market positions, index put options, bonds.)

- Take profits in positions that have been big winners (Rebalancing overbought or extended positions to capture gains but continue participating in the advance.)

- Sell laggards and losers. (If something isn’t working in a market melt-up, it most likely won’t work during a broad decline. Better to eliminate the risk early.)

- Raise cash and rebalance portfolios to target weightings. (Rebalancing risk regularly keeps hidden risks somewhat mitigated.)

Notice, nothing in there says, “sell everything and go to cash.”

We remain more optimistic about the markets due to negative sentiment, seasonality, and high cash levels by fund managers. However, we remain cautious due to the broader macro risks.

There is little value in trying to predict market outcomes. The best we can do is recognize the environment for what it is, understand the associated risks, and navigate cautiously.

Leave being “bullish or bearish” to the media.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read