The SEC approved 11 spot Bitcoin ETFs on Thursday. Unlike the supportive messaging on most new products the SEC approves, Bitcoin ETFs were accompanied by plenty of caution. For starters, in his approval press release, SEC Chair Gary Gensler states the following: Though we’re merit neutral, I’d note that the underlying assets in the metals ETPs have consumer and industrial uses, while in contrast, bitcoin is primarily a speculative, volatile asset that’s also used for illicit activity including ransomware, money laundering, sanction evasion, and terrorist financing. The more damming Bitcoin ETF warnings came from the dissenting opinion written by Commissioner Caroline A. Crenshaw. Her complete statement can be found HERE.

Crenshaw leads her article by emphasizing that underlying the Bitcoin ETFs are Bitcoin markets marred with “fraud and manipulation” and a lack of adequate oversight. She claims that the SEC’s action “departs from well-grounded precedent, that bears characteristics of arbitrary decision-making, and that will restrict our future ability to protect investors.” Crenshaw also questions the correlation between spot Bitcoin and its futures. She warns that with unproven correlation, their ability to detect fraud is limited. Her final paragraph, shown below, does an excellent job of summarizing her concerns about Bitcoin ETFs.

What To Watch Today

Earnings

Economy

Investing Summit: Early Bird Registration Available Now

January 27th, we are hosting a live event featuring Greg Valliere to discuss investing in the 2024 presidential election. What will a new president mean for the markets, the risks, and where to invest through it all? Greg will be joined by Lance Roberts, Michael Lebowitz, and Adam Taggart for morning presentations covering everything you need to know for the New Year.

Register now, as there are only 150 seats. The session is a LIVE EVENT, and no recordings will be provided.

Market Trading Update

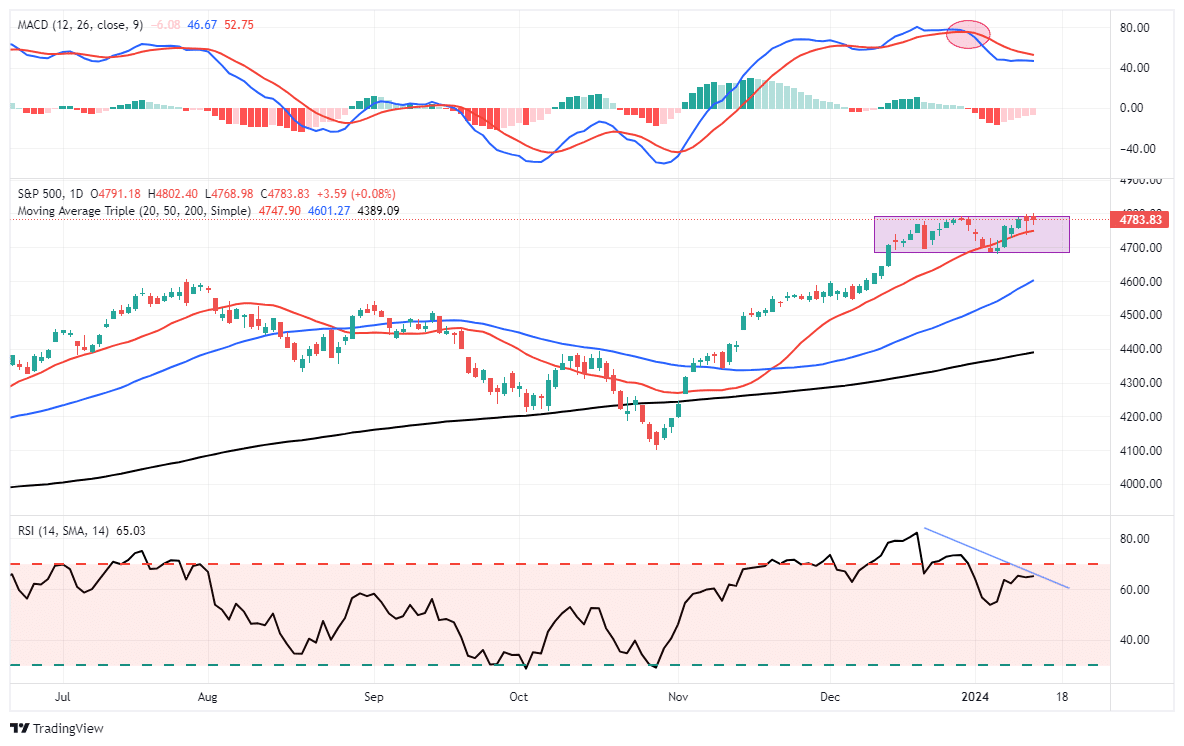

The market was closed yesterday in observance of Martin Luther King. As discussed in last week’s newsletter, the S&P 500 index failed the Santa Claus Rally. To wit:

“With the Santa Claus Rally a no-show, we will now focus on the return for the first five days and the entire month. The old Wall Street axiom says, ‘So goes the first five days of January, so goes the month, so goes the year.’ Since 1950, there have been only three occurrences when the Santa Rally failed, and the first five days and the month of January were positive. Two out of three years were up over 20%, and 1994 was flat, at -1.5%. The average gain for those 3-years was 14.8%.

Next week, we will know how the first five days turn out.“

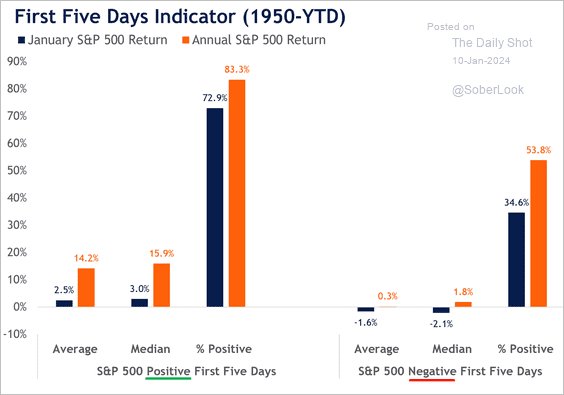

Unfortunately, the S&P 500 Index failed that initial test of the New Year by providing a negative return over those first five trading days. As shown in the chart below, the implications of the failure are potentially lower returns for the entire year.

When the S&P 500 index is negative during the first 5 days of the year, it substantially lowers the odds of the year being positive. Not only do the odds of a positive year decrease, but also the average annual rates of return. However, with that said, while the start of the year has been challenging, we still have a long way to go this year, and many possible outcomes still lie ahead. As such, the markets will focus on the return for the month of January, which, historically, can save the dismal start to the New Year. As Stocktraders Almanac notes:

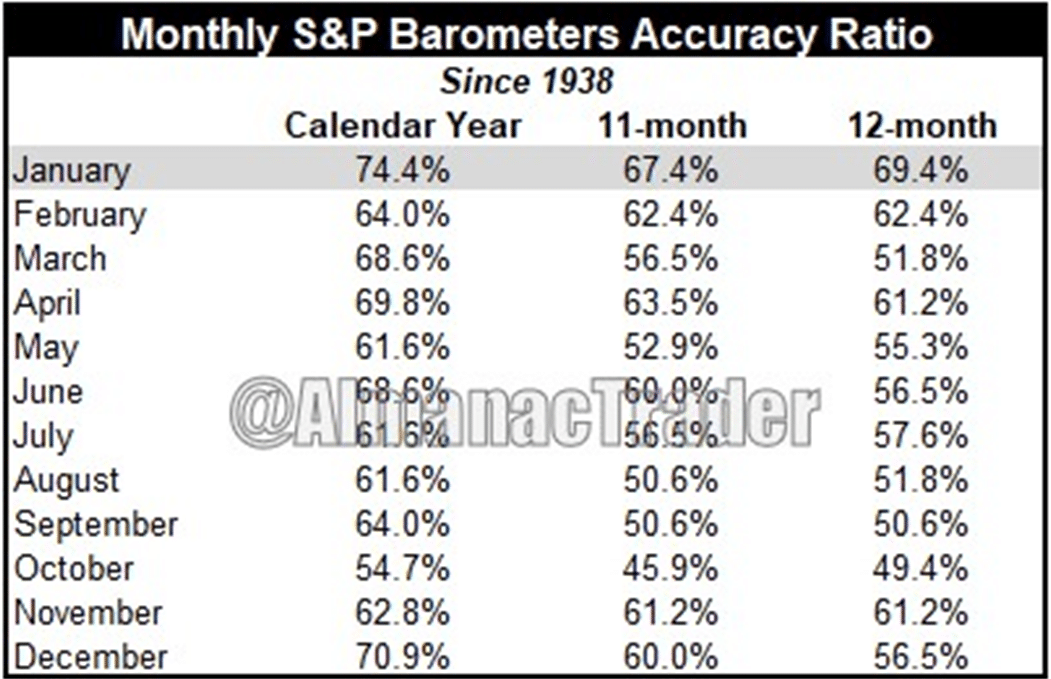

“Here’s what we found going back to 1938. There were only 13 major errors. Using these 13 major errors, the accuracy ratio is 84.9% for the full 86-year period. Including the 9 flat year errors (less than +/– 5%) the ratio is 74.4% — still effective. For the benefit of the skeptics, the accuracy ratio calculated on the performance of the following 11 months is still solid. Including all errors — major and flat years — the ratio is still a decent 67.4%.

Now for the even better news: In the 52 up Januarys there were only 4 major errors for a 92.3% accuracy ratio. These years went on to post 16.2% average full-year gains and 11.6% February-to-December gains.”

Nonetheless, the market has remained rangebound since the highs of December. The market remains on a sell-signal while the overbought conditions, as the RSI shows, are slowly being reduced. Notably, the S&P 500 index has held support at the 20-DMA, which keeps the bullish trend intact.

So, with that bit of optimism, we begin this week with a barrage of earnings as Q4 earnings season gets underway.

The Week Ahead

With the latest round of inflation data behind us, the markets will focus on retail sales on Wednesday and corporate earnings throughout the week. Due to the amplified seasonal effects, retail sales for December are always tricky to make sense of. We caution not to read too much into this number, regardless of whether it’s well above or below expectations. The data, while also faulty due to seasonals, may get interesting in the coming months. Will there be a Christmas spending hangover, or will consumers continue to consume at an above-average rate?

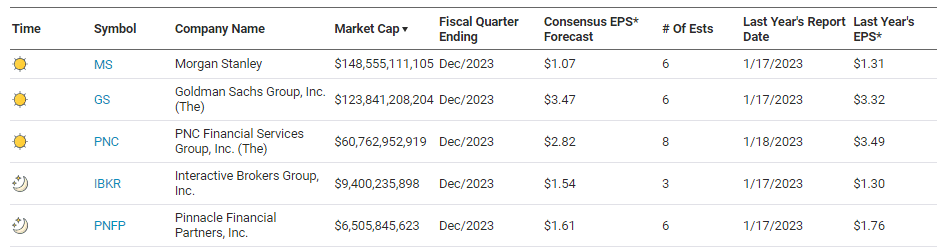

Earnings season, which kicked off on Friday, will continue this week, with regional banks reporting early in the week. A handful of smaller manufacturing companies will report through the week. Many larger companies and the well-followed Magnificent 7 will report in the following week.

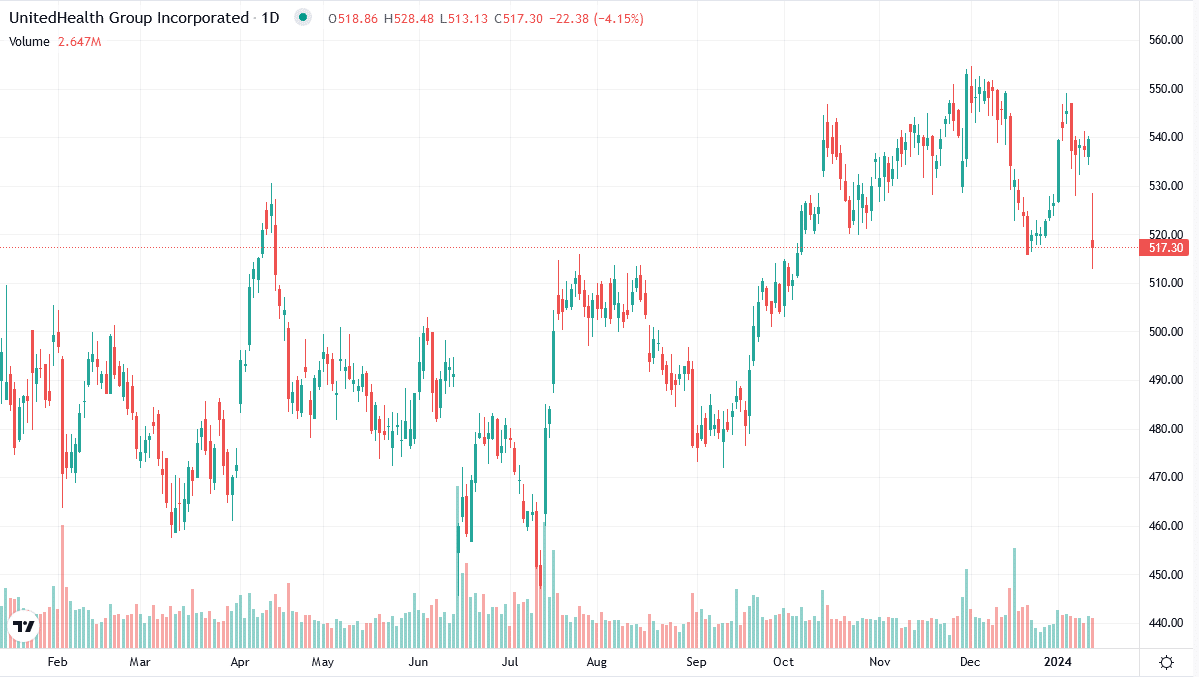

UNH Slips On Earnings

UNH reported better-than-expected earnings and revenues, but its share price opened 5% lower on Friday. The culprit was a higher-than-expected medical cost ratio. The ratio, a subset of its profit margin, measures medical costs to revenue. It rose to 85% from 82.8%. Analysts were expecting 84% based on increased expenses from changes in Medicare. Despite the higher ratio, UNH’s EPS was $6.16, .18 cents above expectations. Revenue was $2.2 billion more than the street expected. The company also reiterated its guidance for 2024. We had been looking to add to our position, so we took advantage of the lower price to buy more UNH.

We published our thoughts on UNH in our introductory weekly Friday Favorites in SimpleVisor. The article reviews their fundamental and technical situation and outlook. We share the UNH SimpleVisor report with you to bring to your attention one of the many benefits of subscribing to SimpleVisor. For $29.99 a month, SimpleVisor subscribers get access to Friday Favorites as well as all of our technical and fundamental tools. Subscribers can also follow our portfolios and get real-time trading information, including text messages on transactions in the models. Give it a try with a 30-day free trial. If you don’t like it, cancel within the trial period, and you will not be charged.

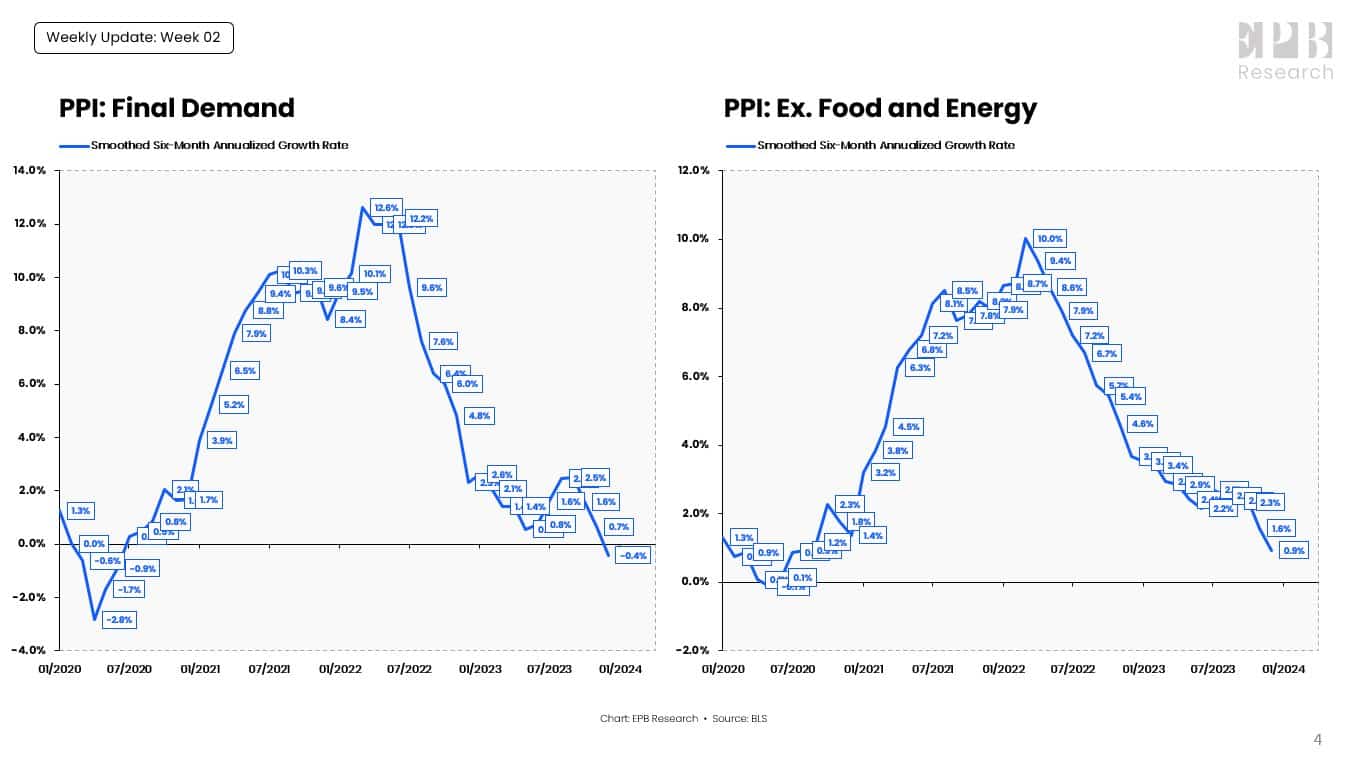

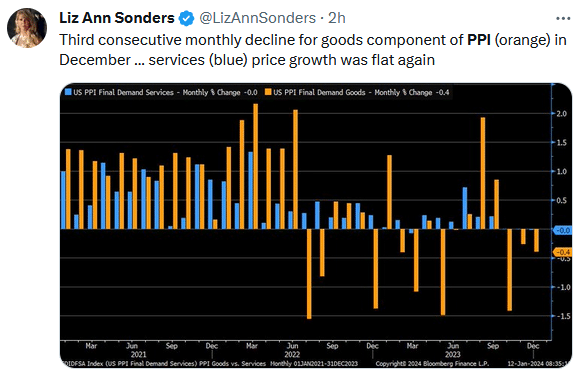

PPI, Unlike CPI, Is Better Than Expected

CPI was a little hot, and PPI was a little cold. Headline PPI fell by 0.1%, while the core number was flat. Headline PPI is now down to 1% year over year. Despite the hotter-than-expected CPI print on Thursday, the PPI report should provide comfort that the recent disinflation trends remain intact.

To this end, the graphs below, courtesy of EPB Research, show the six month trends in headline and core PPI are moving from disinflation toward deflation. CPI tends to follow PPI, so Friday’s PPI report bodes well for lower CPI inflation. Further, the Fed uses PCE to gauge inflation. Per Renaissance Macro Research, the soft PPI number should not cause PCE to rise unexpectedly like CPI. To wit:

The message from PPI is that core PCE will not come in nearly as firm as core CPI did. Using the inputs from CPI/PPI, we estimate core PCE of 0.2% MoM. Over the last 12 months, it is core PCE inflation is likely to come in below 3.0%.

Tweet of the Day

“Want to have better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read