I recently discussed putting market corrections into perspective, in which we looked at the financial impact of a 10-60% correction. But what happens afterward?

During strongly advancing, and very long bull markets, investors become overly complacent about the potential risks of investing. This “complacency” shows up in the resurgence of “couch potato,” “buy and hold,” and “passive indexing” portfolios. While such ideas work as long as markets are relentlessly rising, when the inevitable reversion occurs, things go “sideways” very quickly.

“While the current belief is that such declines are no longer a possibility, due to Central Bank interventions, we had two 50% declines just since the turn of the century. The cause was different, but the result was the same. The next major market decline will be fueled by the massive levels of corporate debt, underfunded pensions, and evaporation of ‘stock buybacks,’ which have accounted for almost 100% of net purchases since 2018.

Market downturns are a historical constant for the financial markets. Whether they are minor or major, the impacts go beyond just the price decline when it comes to investors.”

It is the last sentence I want to focus on today, as it is one of the most important and overlooked consequences of market corrections as it relates to long-term investment goals.

There are a litany of articles touting the massive bull market advance from the 2009 lows, and that if investors had just held onto the portfolios during the 2008 decline, or better yet, bought the March 2009 low, you would have hit the “bull market jackpot.”

Unfortunately, a vast majority of investors sold out of the markets during the tail end of the financial crisis, and then compounded their financial problems by not reinvesting until years later. It is still not uncommon to find individuals who are still out of the market entirely, even after a decade long advance.

This is what brutal bear markets due to investors psychologically.

“Bear markets” push investors into making critical mistakes:

- They paid premium prices, or rather excessive prices, for the companies they are investing in during the “bull market.” Ultimately, overpaying for value has a cost of lower future returns, as “buying high” inevitably turns into “selling low.”

- Investors Panic as market values decline. It is easy to forget during sharply rising markets the money we invest is the “savings” we are dependent on for our family’s future. Many investors who claim to be “buy and hold” change their mind after large losses. There is a point, for every investors, where they are willing to “get out at any price.”

- Volatility is ignored. Volatility is not always a bad word, but rising volatility coupled with large declines, eventually feeds into investor “fear and panic.”

- Ignoring Market Analysis. When markets are trending strongly upwards, investors start to “rationalize” why they are overpaying for value in the market. By looking for “confirmation bias,” they tend to ignore any “market analysis” which contradicts their “hope” for higher prices. The phrase “this time is different” is typically a hallmark.

“The underlying theory of buy and hold investing denies that stocks are ever expensive, or inexpensive for that matter, investors are encouraged to always buy stocks, no matter what the value characteristics of the stock market happen to be at the time.” – Ken Solow

The primary problem with “buy and hold” investing is ultimately, YOU!

The Pension Problem

During raging bull markets, individuals do two things which ultimately lead to their financial distress.

- Start treating the market like a casino in hopes to “getting rich quick,” and

- Reduce their “contributions” given expectations that high returns will “fill the gap.”

Unfortunately, this is the same problem that plagues pension funds all across America today.

As I discussed in “Pension Crisis Is Worse Than You Think,” it has been unrealistic return assumptions used by pension managers over the last 30-years, which has become problematic.

“Pension computations are performed by actuaries using assumptions regarding current and future demographics, life expectancy, investment returns, levels of contributions or taxation, and payouts to beneficiaries, among other variables. The biggest problem, following two major bear markets, and sub-par annualized returns since the turn of the century, is the expected investment return rate.

Using faulty assumptions is the linchpin to the inability to meet future obligations. By over-estimating returns, it has artificially inflated future pension values and reduced the required contribution amounts by individuals and governments paying into the pension system

Pensions STILL have annual investment return assumptions ranging between 7–8% even after years of underperformance.”

However, why do pension funds continue to have high investment return assumptions despite years of underperformance? It is only for one reason:

To reduce the contribution (savings) requirement by their members.

This is the same problem for the average American faces when planning for 6-8% average annual returns on their investment strategy. Why should you save money if the market can do the work for you? Right?

This is a common theme in much of the mainstream advice. To wit:

“Suze Orman explained that if a 25-year-old puts $100 into a Roth IRA each month, they could have $1 million by retirement.”

The problem with Ms. Orman’s statement is that it requires the 25-year old to achieve an 11.25% annual rate of return (adjusting for inflation) every single year for the next 40-years.

That certainly isn’t very realistic.

However, under-saving is one of the primary problems which leaves investors well short of their financial goals by retirement.

The other problem, as noted above, is the most important part of the analysis overlooked by promoters of “buy and hold” investing.

Let me explain.

Getting Back To Even, Isn’t Even

Here is the common mainstream advice.

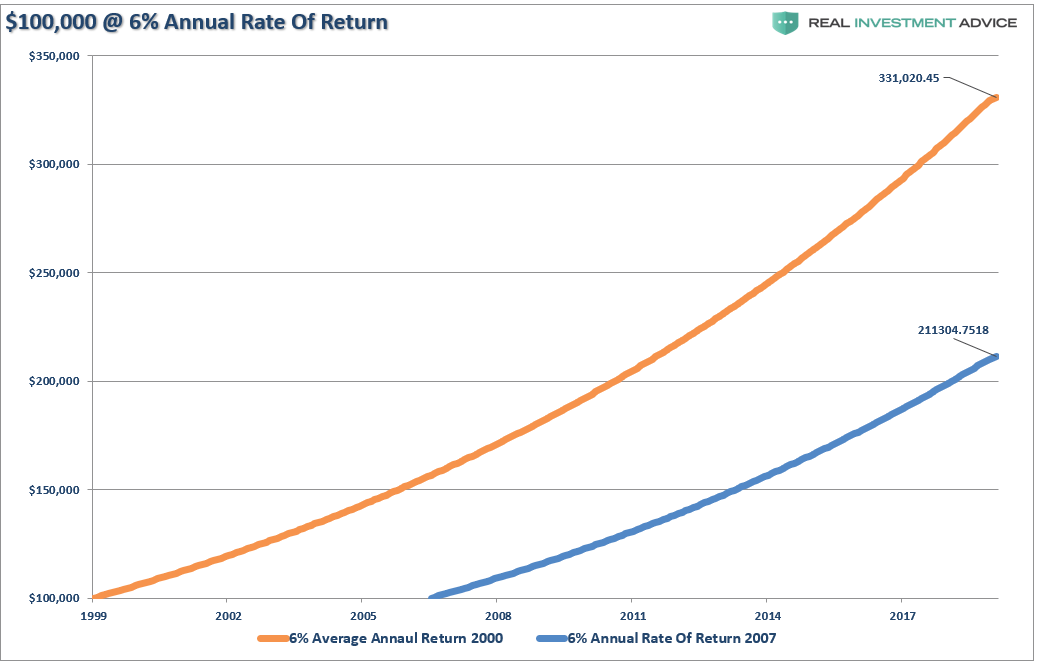

“If you had invested $100,000 at the market at the peak of the market in 2000, or in 2007, your portfolio would have gotten back to even in 2013. Since then, your portfolio would have grown to more than $200,000.

Here is the relative chart proving that statement is correct. (Real, inflation-adjusted, total return of a $100,000 investment.)

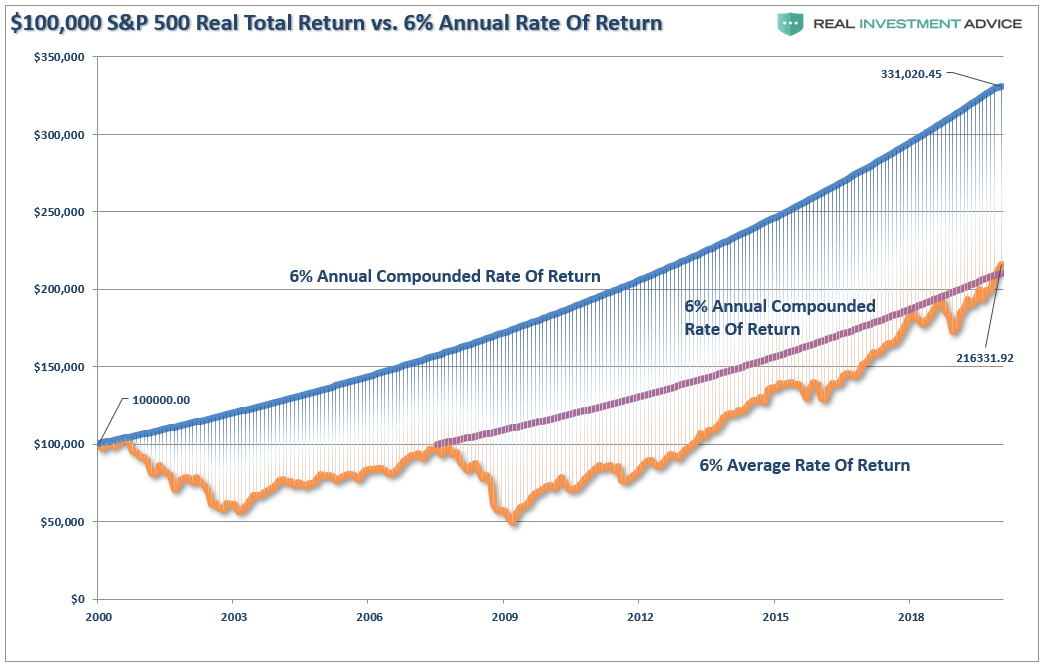

No one talks much about investors who have been in the market since the turn of the century, but it is one of the problems why so many Americans are underfunded for retirement. While Wall Street claims the market delivers 6% annual returns, or more, the annual rate of return since 2000, on an inflation-adjusted, total return basis, is just shy of 4%.

However, since most analysis used to support the “buy and hold” thesis starts with the peak of the market in 2007, that average return does indeed come in at 6.64%.

Here is the problem.

While your portfolio got back to even, on a total return basis, 6 or 13-years after your initial investment, depending on your start date, you DID NOT get back to even.

Remember your investment plan? Yes, that plan touted by the mainstream media, which says to assume a return of 6% annually?

The chart below shows $100,000 invested at 6% annually from 2000 or 2007.

So, what’s wrong with that?

An investor tripled their money from 2000 and doubled it from 2007.

Unfortunately, you didn’t get that.

Let’s overlay our two charts.

If your financial plan was based on reduced saving rates, and high rates of return, you are well short of you goals for retirement if you started in 2000. Fortunately, for investors who started in 2007, congratulations, you are now back to even.

Unfortunately, there are few investors who actually saw market returns over the last 12-years. As noted, a vast majority of investors who were fully invested into the market in 2007, were out of the market by the end of 2008. After such a brutal beating, it took years before they returned to the markets. Their returns are vastly different than what the mainstream media claims.

While there is a case to be made for “buy and hold” investing during rising markets, the opposite is true in falling markets. The destruction of capital eventually pushes all investors into making critical investment mistakes, which impairs the ability to obtain long-term financial goals.

You may think you have the fortitude to ride it out. You probably don’t.

But even if you do, getting back to even isn’t really an investment strategy to reach your retirement goals.

Unfortunately, for many investors today who have now reached their financial goals, it may be worth revisiting what happened in 2000 and 2007. We are exceedingly in the current bull market, valuations are elevated, and there is a rising belief “this time is different.”

It may be worth analyzing the risk you are taking today, and the cost it may have on “your tomorrow.”