In this 12-17-21 issue of “The Countdown To The Next Bear Market.”

- Sell Mortimor Sell…But Then Buy

- Did The Fed Just Start The Countdown

- Portfolio Positioning

- Sector & Market Analysis

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Is It Time To Get Help With Your Investing Strategy?

Whether it is complete financial, insurance, and estate planning, to a risk-managed portfolio management strategy to grow and protect your savings, whatever your needs are, we are here to help.

Schedule your “FREE” portfolio review today.

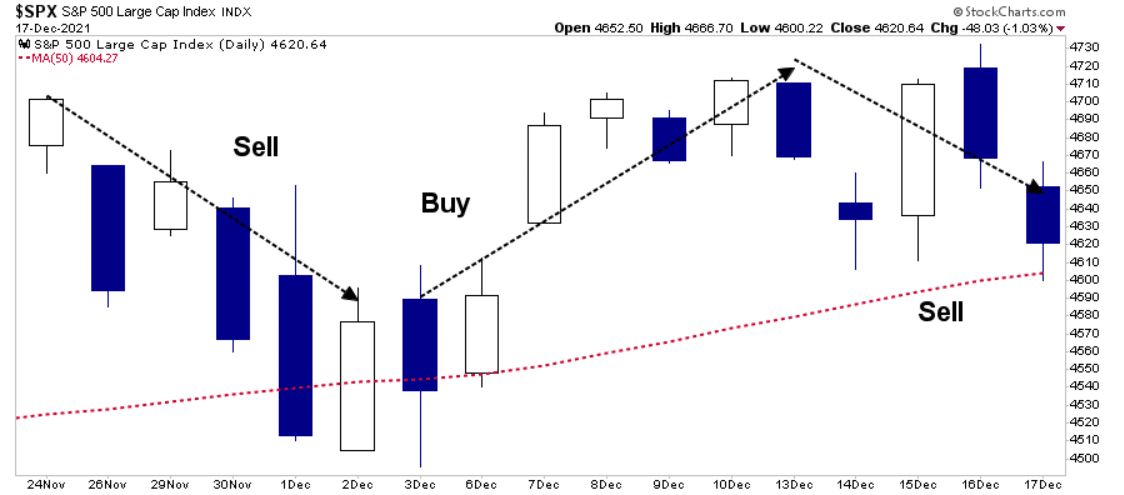

Sell Mortimor Sell

Notably, while the previous week was marked by panic selling, with stocks like DocuSign (DOCU) dropping 40% in a single session, this week was the exact opposite. Starting on Monday, there was almost a palpable “panic” to buy stocks.

Did anything fundamentally change to support the panic buying? No. If you paid attention to the headlines, the Federal Reserve has become considerably more “hawkish” in the stance. The acceleration of tapering liquidity and hiking interest rates will prove unkind to investors chasing highly overvalued securities.

During the previous three weeks, the market action has been brutal to trade at best and nauseating at worst. As shown in the chart below, stock prices have been all over the place.

However, while the S&P 500 index managed to hold its 50-dma reasonably well, the damage below the surface was much more considerable. A rather large contingent of the S&P 500 index is well off their 52-week highs, which accounts for much of the poor breadth we repeatedly discussed this year.

We also suspect much of the “sloppiness” in the market over the last week remains a function of portfolio managers’ mutual fund distributions, options expiration, and tax-loss selling. With most of that concluding on Friday, we will likely see some buying interest as fund managers “window dress” for year-end reporting.

As discussed last week:

“This week’s rally continues to follow the seasonality chart we discussed last week. Such also suggests that we will see some additional “sloppy” action next week heading into options expiration next Friday. However, that weakness should provide the base for the year-end rally to commence from.”

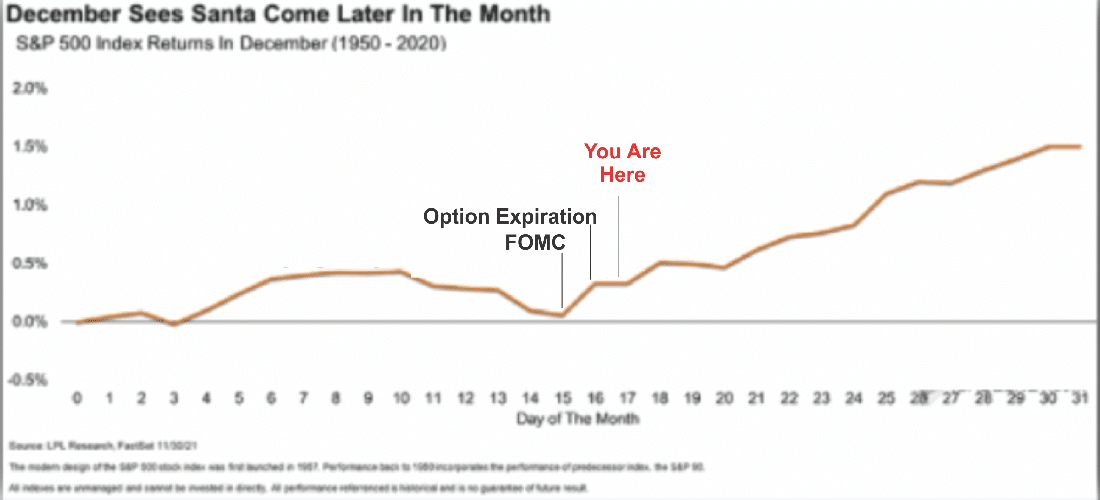

Will Santa Still Visit Broad And Wall?

Next week tends to start the seasonally strong period of the year.

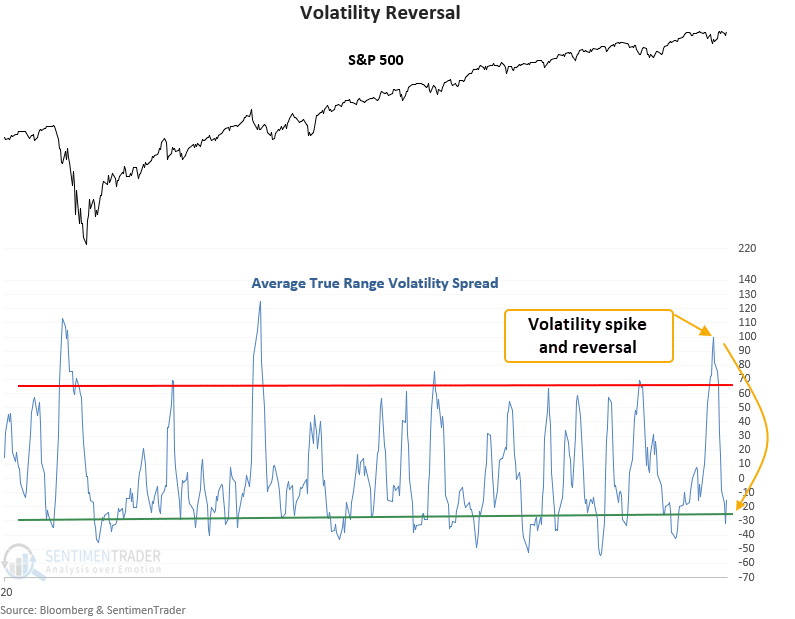

As noted by Sentiment Trader, the recent price volatility is not necessarily a bad sign. As they note:

“The S&P 500 has now cycled from a period of elevated volatility to a period of relative calm. This type of behavior often signals higher prices as investors become more comfortable with new buys.

This signal has triggered 25 other times over the past 28 years. After the others, future returns and win rates were excellent on medium and long-term time frames. Consistency was outstanding in the 2 and 6-month time frames, with 21 out of 24 winners. And, the 6-month time frame is currently riding a 13 signal win.”

However, I do want to suggest some caution. Yes, there are reasons to be optimistic heading into year-end, which is why we increased equity exposures on recent weakness (discussed below). However, there is NO guarantee that “Santa Will Visit Broad & Wall.”

With new lows outpacing new highs, bullish breadth declining, and volume light, there is more risk relative to reward in the short-term. Furthermore, with the Fed’s more aggressive stance on monetary policy starting a countdown to the next potential bear market, we remain cautious on some of the more speculative areas of the market.

Such was a point I discussed with Charles Payne on Fox Business News last week. As we move into 2022, we will likely need to focus on value over growth, fundamentals versus technicals, and stability over momentum.

The reason is that history suggests the Fed just started the countdown to the next market downturn.

This Week’s MacroView

Did The Fed Just Start The Countdown?

In August, I penned an article discussing the “3-Things That Signal Bear Markets.”

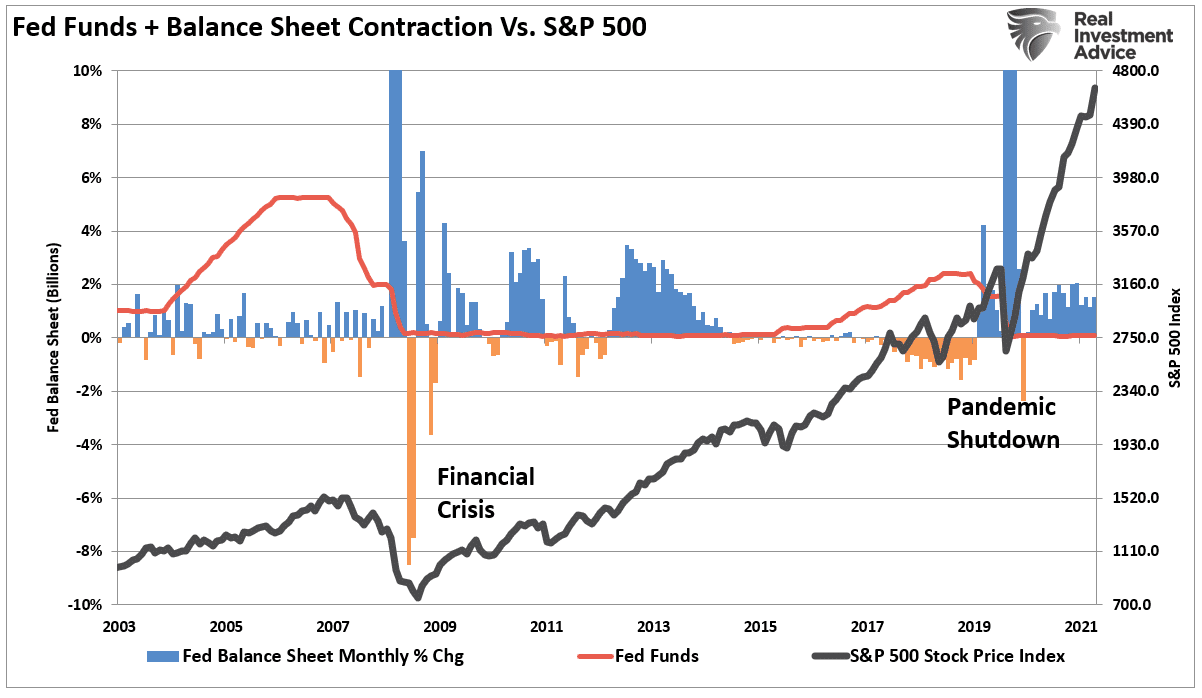

There is currently no indication of a recession. Nevertheless, the Fed continues to purchase $120 billion a month in bonds keeping the “psychological Fed put” in place. The Fed is also keeping the overnight lending rate at zero, and the yield curve is nowhere close to inverting just yet.

However, these items will change quickly, and when they do, the countdown will start towards the next recession and bear market.

While the market sold off after the Fed announcement, historically speaking, it takes roughly 9-months before changes to Fed policy impact the financial markets. Such is the “countdown” we are referring to.

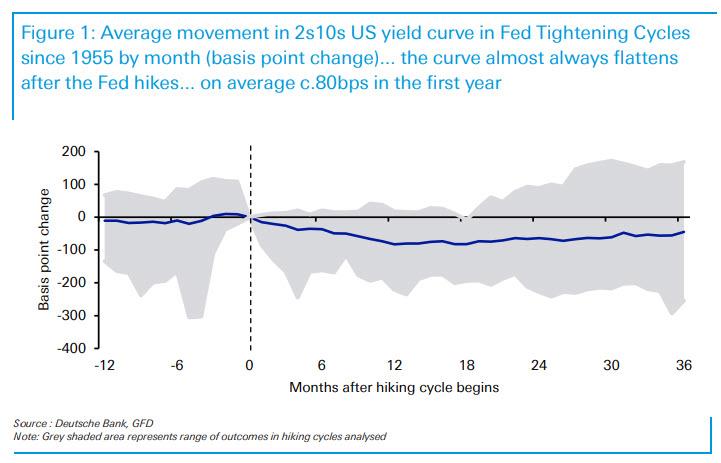

Pay attention to the yield curve.

“So given that the Fed tightening eventually contributes to recessions, when should the next one occur?

A look at the table in a recent DB note “When the Fed hike: what happens next?” suggests the median and average time to the next recession is 37 and 42 months after the first hike. So that takes us to July 2025 and December 2025 respectively. That said, the earliest gap over 13 cycles is 11 months and that would take us to May 2023.

Alternatively, if we go a different route and look at the yield curve, today’s CoTD shows that the 2s10s pretty much always flattens after the first hike. By an average of 80bps over the next 12 months. So a June 2022 first hike may bring an inversion by June 2023 given the 2s10s currently sits at just under 80bps. Obviously that assumes a flat curve from now until June next year which is a big assumption.” – Zerohedge

Slowly At First

There are two important takeaways from that analysis.

- Historically there was much less leverage in the system, which means it takes fewer rate hikes to trigger an event.

- It is likely the countdown to the next economic/market event could be sooner than historic averages.

Regardless, the countdown to the next bear market has started as the monetary accommodation that supported the previous bull market gets removed. The only issue is when “bullish psychology” turns negative.

The problem, as always, is predicting the next market peak. Over the last few years, the stock market has detached from virtually all underlying fundamental measures. The rationalization supporting bullish psychology was “don’t fight the Fed” and “liquidity trumps all.” If the Fed is reversing those monetary supports, then so are those supports for the bullish bias.

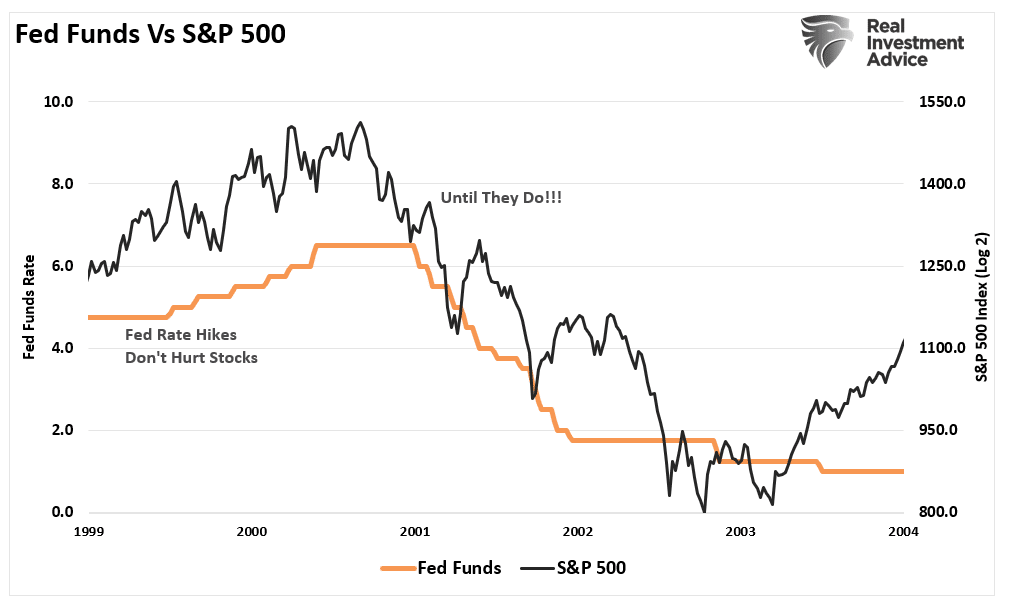

However, initially, since bulls will continue to be bullish, the rationale shifts to “stocks do well when the Fed initially hikes rates.” Such is a true statement, and many point to the initial rate hikes of 1998 to prove their point. However, they forget to tell you what happened roughly 18-months later when the Dot.com crash ensued.

The Fed Will Be Back

The point is that initially rate hikes, and tighter monetary policy, do not cause an immediate “bear market.” As noted in Slowly At First:

“Understanding that change is occurring is what is essential. But, unfortunately, the reason investors ‘get trapped’ in bear markets is that when they realize what is happening, it is far too late to do anything about it.

Bull markets lure investors into believing ‘this time is different.’ When the topping process begins, that slow, arduous affair gets met with continued reasons why the ‘bull market will continue.’ The problem comes when it eventually doesn’t. As noted, ‘bear markets” are swift and brutal attacks on investor capital.’”

It is essential to pay attention to these indicators.

- The Fed is tapering QE.

- The yield curve is flattening.

- And, the Fed will hike rates next year.

These are all actions that started the countdown to previous market topping processes.

Of course, as soon as one countdown ends, we will start discussing the countdown to the Fed’s next round of monetary accommodation.

“Incidentally, the market seems to agree because as we showed recently, traders are now pricing in an inverted 4Y1Y – 2Y1Y forward swap curve, meaning that fed funds in 2025 are seen below 2023, suggesting at some point in the interim, the Fed’s next easing cycle will begin.” – Zerohedge

As is always the case, “bear markets begin slowly, and then all at once.”

Does this mean you should be all in cash? No. As discussed on Friday, such also can be very detrimental to your financial health.

All we are suggesting is that you should be aware that the countdown to the next market-related event has likely started. As such, it is worth paying attention to the risk you are taking in your portfolio.

Portfolio Update

As noted last week, we have been using weakness opportunistically to boost our trading positions for the potential year-end rebalancing of portfolios. As reported on Wednesday on my Twitter feed:

In the short-term, expect that the setup for a short-term rally into year-end is likely between those higher than expected cash levels and the more extreme bearish sentiment shown below. As such, we have suggested positioning for that opportunity.

Our model allocation weights are currently slightly overweight target equity levels (Target: 60% stocks / 40% bonds and cash.)

We will unlikely make any further increases at this juncture unless we get sufficient weakness that does not violate market support levels. However, please make no mistake assuming we are bullish going into 2022. There is a significant level of risk to the markets with the recent Fed actions starting the countdown to the next market event. As such, we continue to maintain tight stops on all positions. Furthermore, we will use any “Santa Rally” to lock in profits once the market returns to overbought levels.

We remain optimistic, but we also remain well aware of the risks.

See you next week.

By Lance Roberts, CIO

Market & Sector Analysis

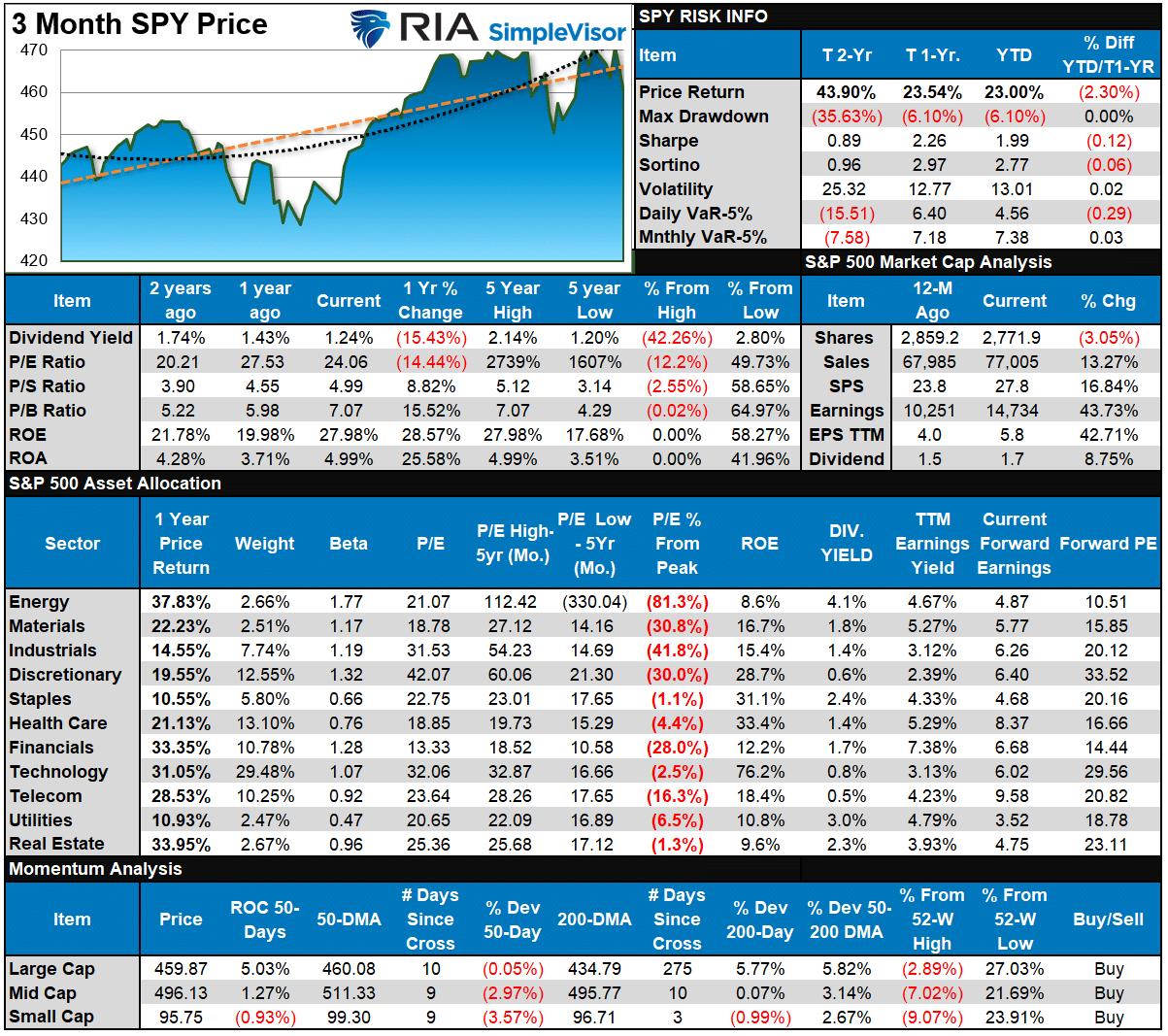

S&P 500 Tear Sheet

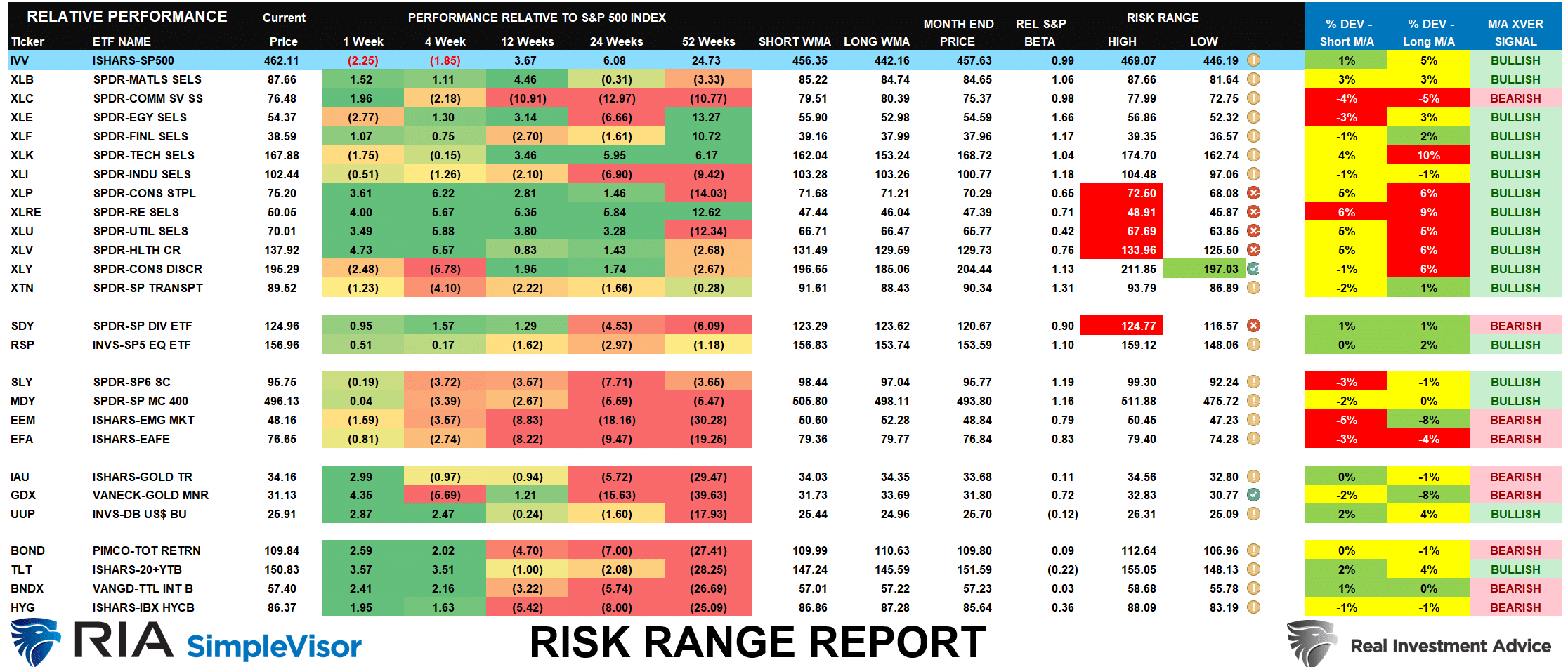

Relative Performance Analysis

Technical Composite

The technical overbought/sold gauge comprises several price indicators (RSI, Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. The current reading is 69.20 out of a possible 100.

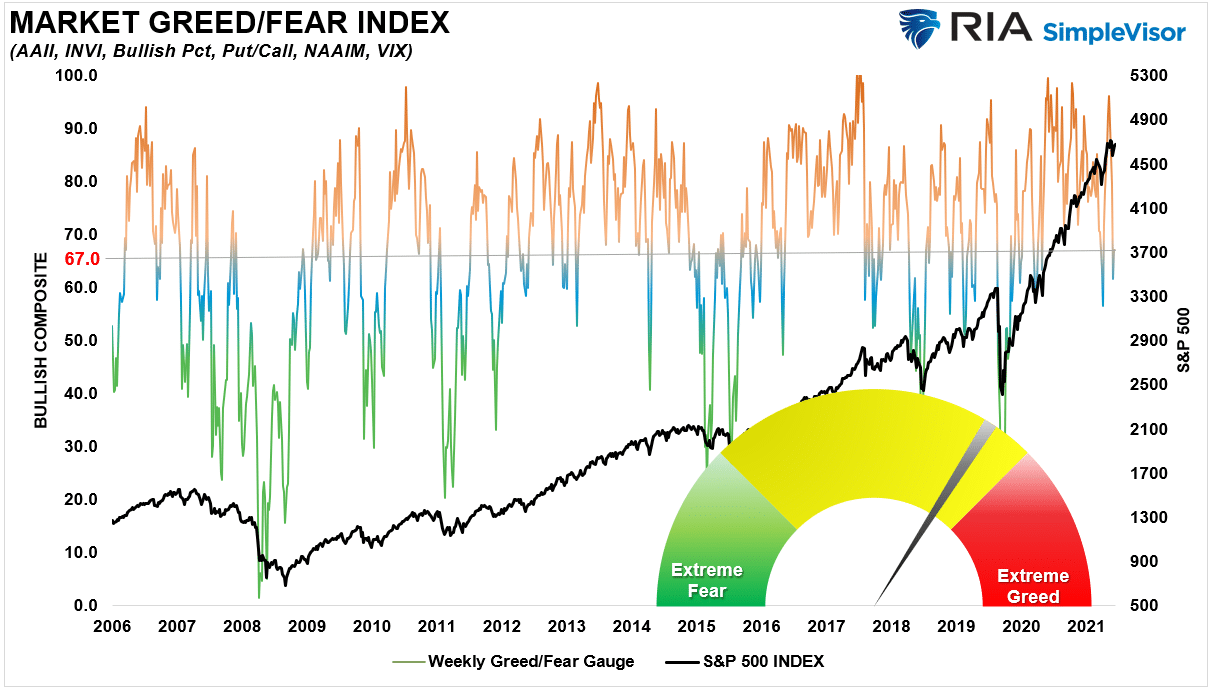

Portfolio Positioning “Fear / Greed” Gauge

Our “Fear/Greed” gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, to more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0-100. It is a rarity that it reaches levels above 90. The current reading is 67 out of a possible 100.

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares each sector and market to the S&P 500 index on relative performance.

- “MA XVER” is determined by whether the short-term weekly moving average crosses positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- Table shows the price deviation above and below the weekly moving averages.

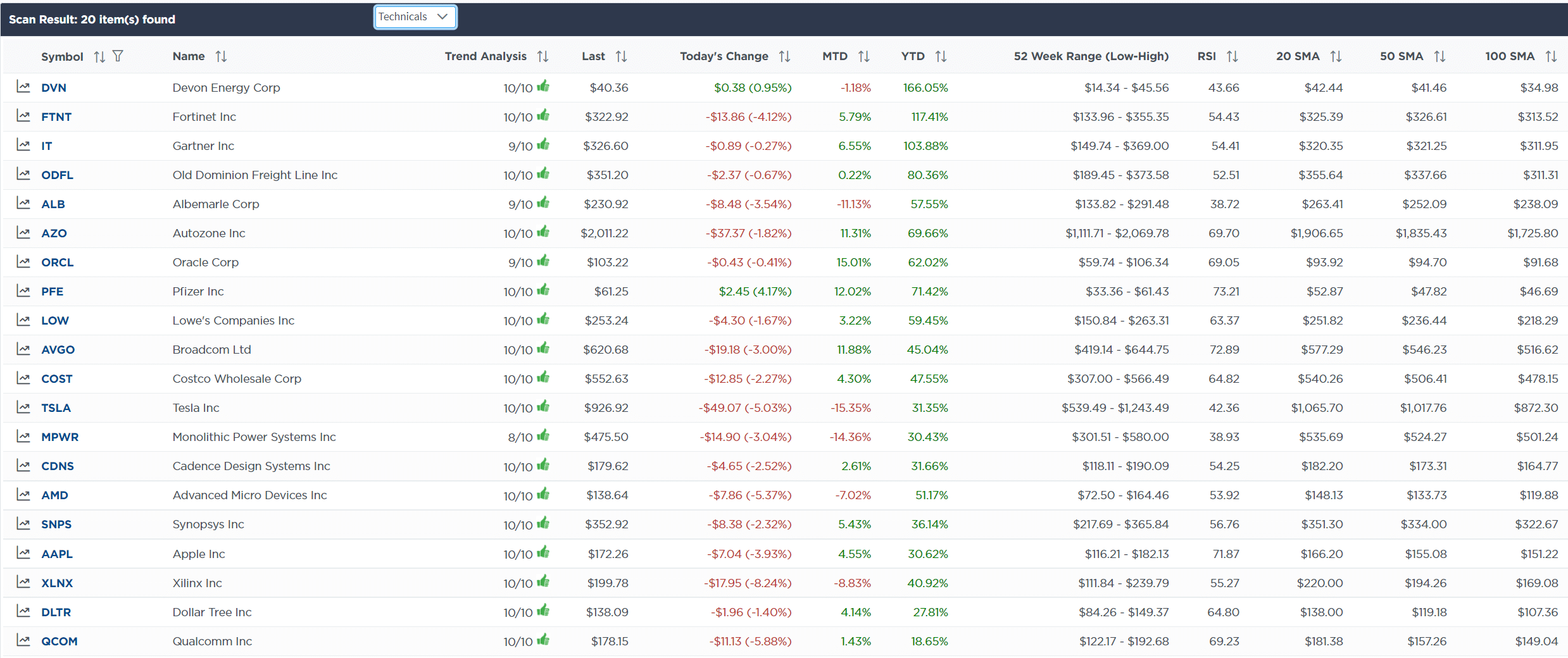

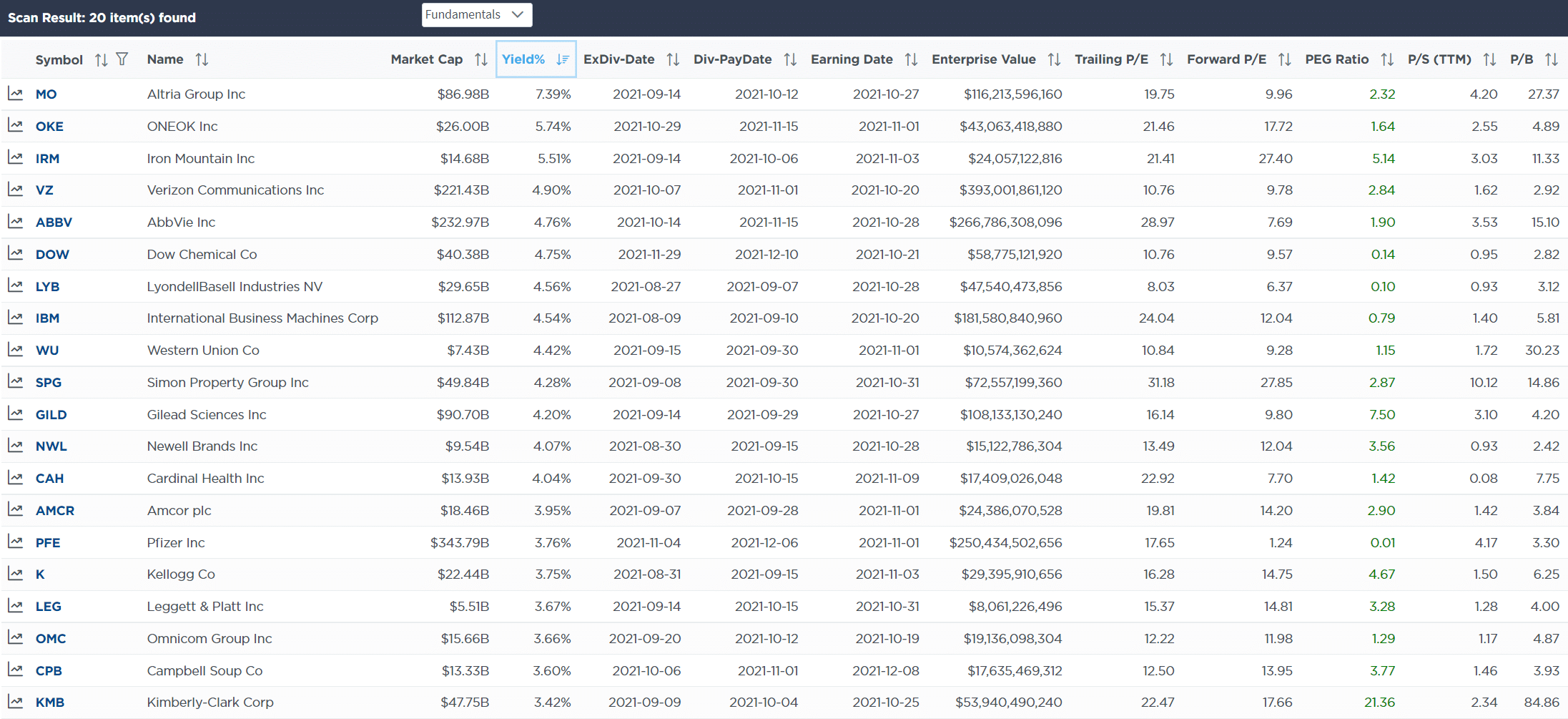

Weekly Stock Screens

Each week we will provide three different stock screens generated from SimpleVisor: (RIAPro.net subscribers use your current credentials to log in.)

This week we are scanning for the Top 20:

- Relative Strength Stocks

- Momentum Stocks

- Dividend Stocks

These screens generate portfolio ideas and serve as the starting point for further research.

(Click Images To Enlarge)

RSI Screen

Momentum Screen

Dividend Screen

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

“With the Fed meeting now behind us, and just options expiration left on Friday, we are using the weakness from the last couple of trading days to fill out the rest of our portfolio for the Santa Claus rally into year-end.

As such we are making 2-key adjustments. First, we are adding slightly to our equity holdings mostly by adding to our S&P 500 index trading position. Secondly, we are rebalancing our bond portfolio to lower volatility and increase yield as we head into 2022.” – 12-16-21

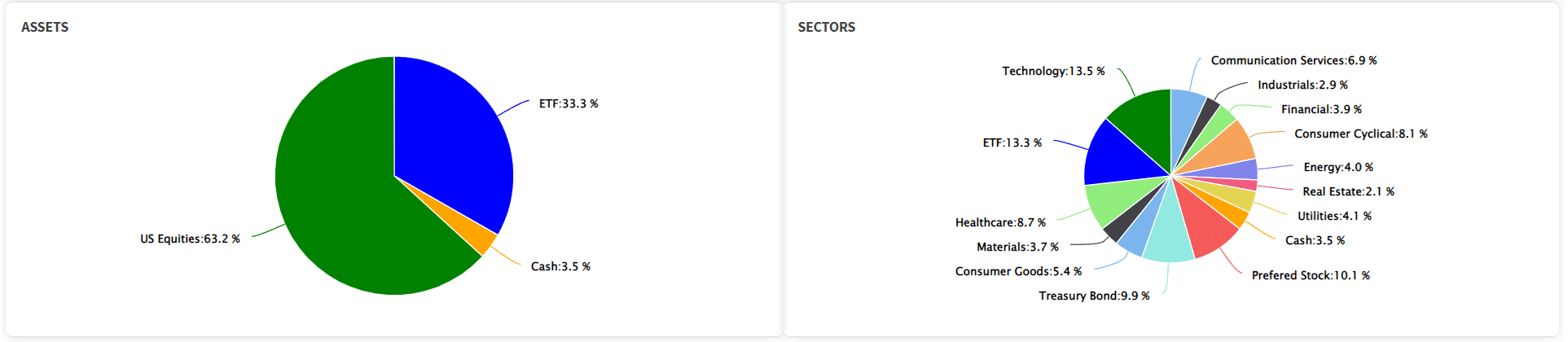

Equity Portfolio

- Sell 100% of GSY (Short-Duration Bond Portfolio)

- Add 6% of TFLO (Floating Treasury Bonds)

- Increase IEF (Intermediate Treasury Bonds) to 4% of the portfolio.

- Increase Preferred ETF (PFF) to 10% of the portfolio

- Reduce Apple (AAPL) by 0.5% to take profits.

- Add 0.5% to Adobe (ADBE) on earnings-related weakness this morning.

- Initiate a 1% position of Asana (ASAN) to the portfolio following its recent correction.

- Add 2% of the portfolio to the S&P 500 Index ETF (SPY) bringing the trading position to 7%.

ETF Portfolio

- Sell 100% of GSY (Short-Duration Bond Portfolio)

- Add 10% of TFLO (Floating Treasury Bonds)

- Increase IEF (Intermediate Treasury Bonds) to 4% of the portfolio.

- Increase Preferred ETF (PFF) to 10% of the portfolio

- Add 1% to Technology Select ETF (XLK) bringing total weight to 14%

- Add 2% of the portfolio the S&P 500 Index ETF (SPY) bringing the trading position to 7%.

Lance Roberts, CIO

Have a great week!