As was widely expected, the Fed hiked rates by 50bps to 4.25% – 4.50%. Currently, implied Fed Funds futures project the terminal Fed Funds rate for the cycle will peak at 4.85%. The market is pricing a total of 50bps (25bps each) at the next two meetings and a 50/50 chance of another 25bps at the following meeting. As we share below, all Fed members think the terminal rate will be higher than the market implies. Barring surprises that may prompt another 50bps rate hike, future hikes will be in 25bps increments.

Powell makes it clear the Fed is far from pivoting toward stimulative policies. Their updated quarterly projections allude that Fed Funds will likely be north of 5.00% through next year. Powell emphatically states that inflation needs to be nearing its 2% objective and have confidence inflation has not “become entrenched” before they reverse course. Equally important, after botching its transitory inflation call in 2021, the Fed is seeking to regain credibility and can ill afford another round of higher inflation by pivoting too early. Powell is willing to risk recession for the sake of price stability. Markets seem to think the Fed will backtrack quickly.

What To Watch Today

Economy

- 8:30 a.m. ET: Empire Manufacturing, December (-0.9 expected, 4.5 prior)

- 8:30 a.m. ET: Retail Sales Advance, month-over-month, November (-0.2% expected, 1.3% prior)

- 8:30 a.m. ET: Empire Manufacturing, December (-0.9 expected, 4.5 prior)

- 8:30 a.m. ET: Retail Sales Advance, month-over-month, November (-0.2% expected, 1.3% prior)

- 8:30 a.m. ET: Retail Sales excluding autos, month-over-month, November (0.2% expected, 1.3% prior)

- 8:30 a.m. ET: Retail Sales excluding autos and gas, MoM, November (0.1% expected, 0.9% prior)

- 8:30 a.m. ET: Retail Sales Control Group, November (0.1% expected, 0.7% prior)

- 8:30 a.m. ET: Initial jobless claims, week ended Dec. 10 (232,000 expected, 220,000 prior)

- 8:30 a.m. ET: Continuing claims, week ended Dec. 3 (1.668 million expected, 1.671 prior)

- 8:30 a.m. ET: Philadelphia Fed Business Outlook Index, December (-10.0 expected, -19.4 prior)

- 9:15 a.m. ET: Industrial Production, month-over-month, November (0.1% expected, 0.1% prior)

- 9:15 a.m. ET: Capacity Utilization, November (79.8% expected, 79.9% prior)

- 9:15 a.m. ET: Manufacturing (SIC) Production, November (-0.1% expected, 0.1% prior)

- 10:00 a.m. ET: Business Inventories, October (0.4% expected, 0.4% prior)

- 10:00 a.m. ET: Net Long-Term TIC Flows, October ($118.0 billion prior)

- 10:00 a.m. ET: Total Net TIC Flows, October ($30.9 billion prior)

- 8:30 a.m. ET: Retail Sales excluding autos, month-over-month, November (0.2% expected, 1.3% prior)

- 8:30 a.m. ET: Retail Sales excluding autos and gas, MoM, November (0.1% expected, 0.9% prior)

- 8:30 a.m. ET: Retail Sales Control Group, November (0.1% expected, 0.7% prior)

- 8:30 a.m. ET: Initial jobless claims, week ended Dec. 10 (232,000 expected, 220,000 prior)

- 8:30 a.m. ET: Continuing claims, week ended Dec. 3 (1.668 million expected, 1.671 prior)

- 8:30 a.m. ET: Philadelphia Fed Business Outlook Index, December (-10.0 expected, -19.4 prior)

- 9:15 a.m. ET: Industrial Production, month-over-month, November (0.1% expected, 0.1% prior)

- 9:15 a.m. ET: Capacity Utilization, November (79.8% expected, 79.9% prior)

- 9:15 a.m. ET: Manufacturing (SIC) Production, November (-0.1% expected, 0.1% prior)

- 10:00 a.m. ET: Business Inventories, October (0.4% expected, 0.4% prior)

- 10:00 a.m. ET: Net Long-Term TIC Flows, October ($118.0 billion prior)

- 10:00 a.m. ET: Total Net TIC Flows, October ($30.9 billion prior)

Earnings

Market Trading Update

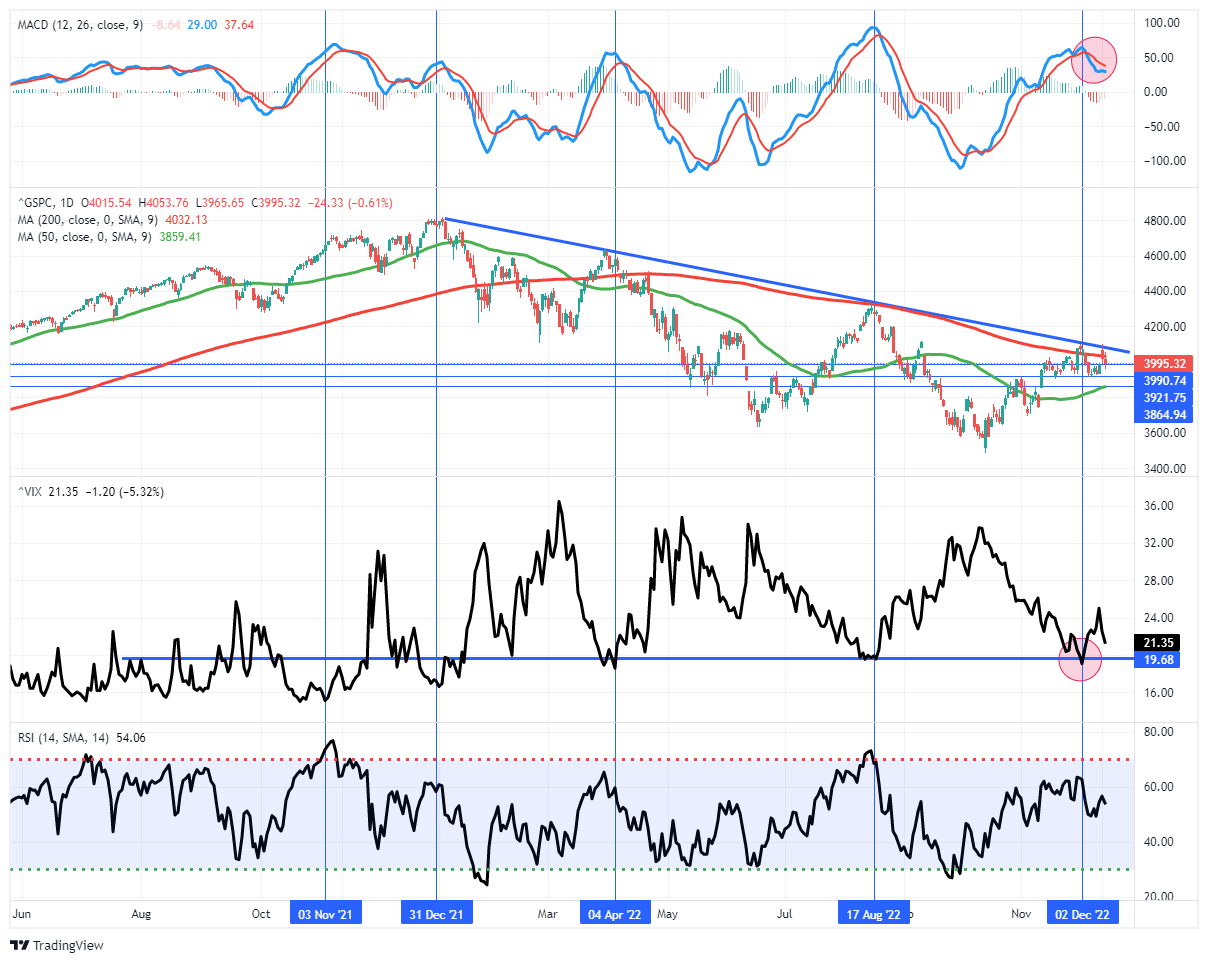

As we discussed in yesterday’s 3-Minutes On Markets & Money, Jerome Powell did indeed deliver a hawkish message to investors suggesting that the terminal rate for rate hikes remains above 5%. That hawkish message sent stocks tumbling into negative territory yesterday, giving up all of the CPI gains from Tuesday. The good news is the market did hold support at 20-DMA, and remains within the consolidation range from early November. With Friday being a massive $3.2 Trillion options expiration day, there is no telling where the market will trade over the next couple of days. Our repeated warnings over the last few days not to try and front-run the Fed proved salient. We suggest remaining cautious through Friday as well.

The MACD sell signal remains intact, and the market is not oversold. We still think there may be a tradeable rally into year-end but prefer to wait through Friday to potentially take on any risk exposure.

What is the Fed Thinking?

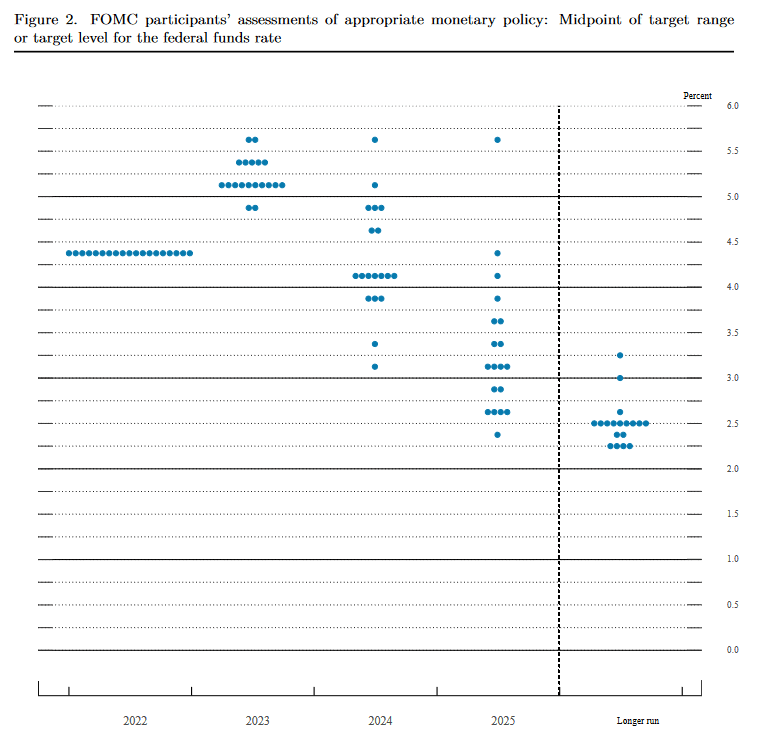

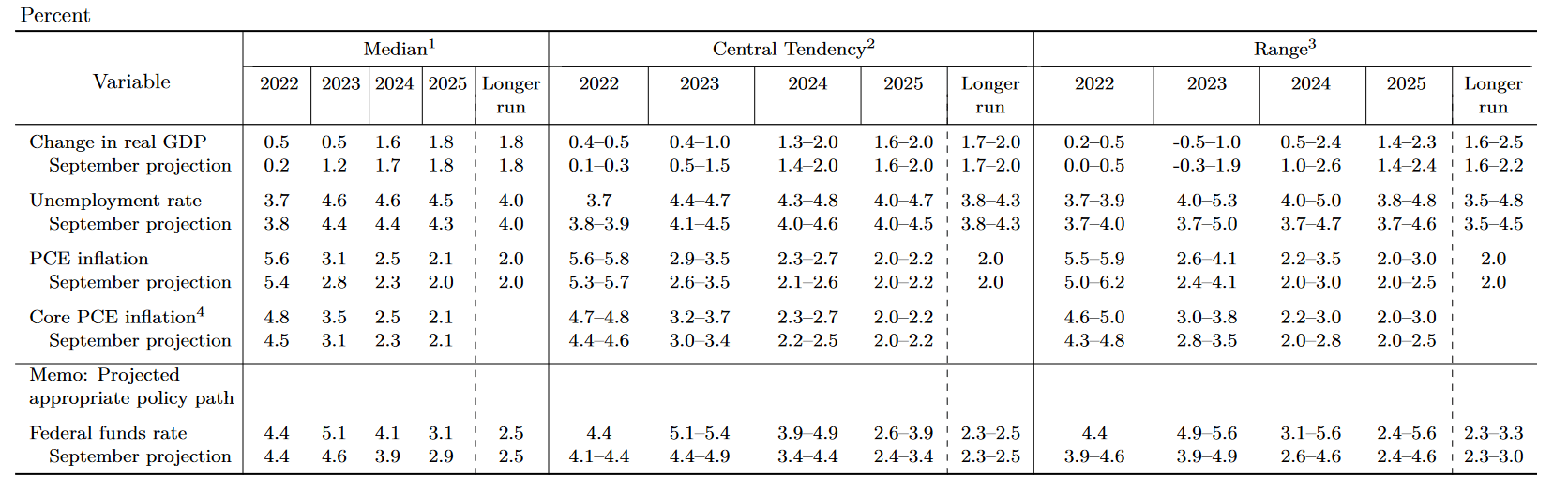

Every quarter the Fed publishes its voting members’ outlook for the economy, inflation, and Fed Funds. The table below shows the current median and range of forecasts for GDP, unemployment, PCE, core PCE, and Fed Funds. The Fed reduced its GDP forecast for 2023 and increased its inflation outlook. Their longer-run forecasts did not change since September. It collectively thinks the unemployment rate will jump to 4.6% in 2023 and stay there for three years.

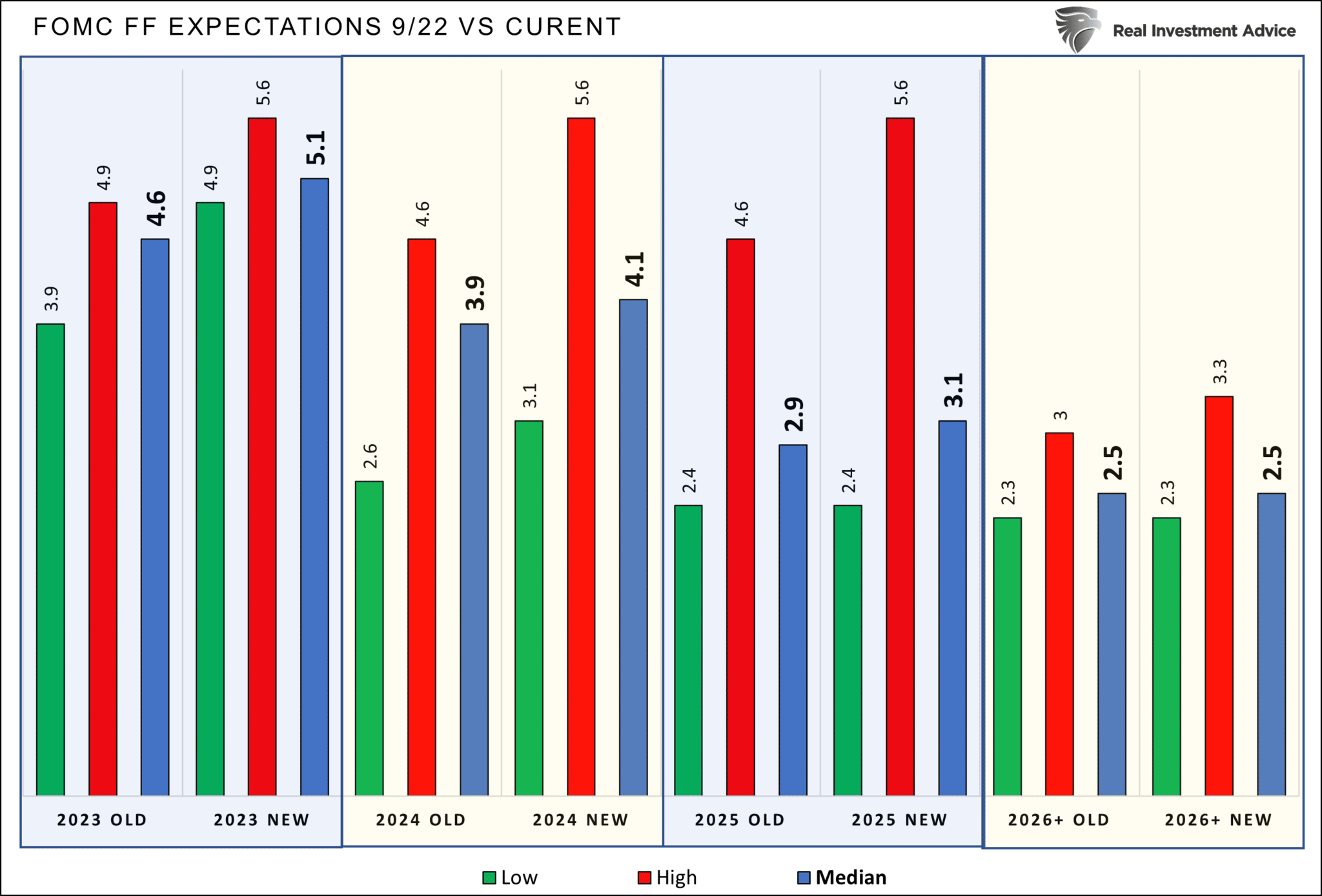

Fed watchers compare the latest projections to the prior projections to gain insight into how the Fed’s mindset may change. The bar chart below compares the September range and median of Fed Funds forecasts to those released yesterday. As it shows, after having just raised rates by 50bps following four 75bps increases, the Fed is not forecasting a pivot to lower rates anytime soon. Interestingly, at least one Fed member thinks Fed Funds will rise to 5.6% next year and stay there through 2025. Only two members believe the Fed Funds rate will be as low as 4.9% next year.

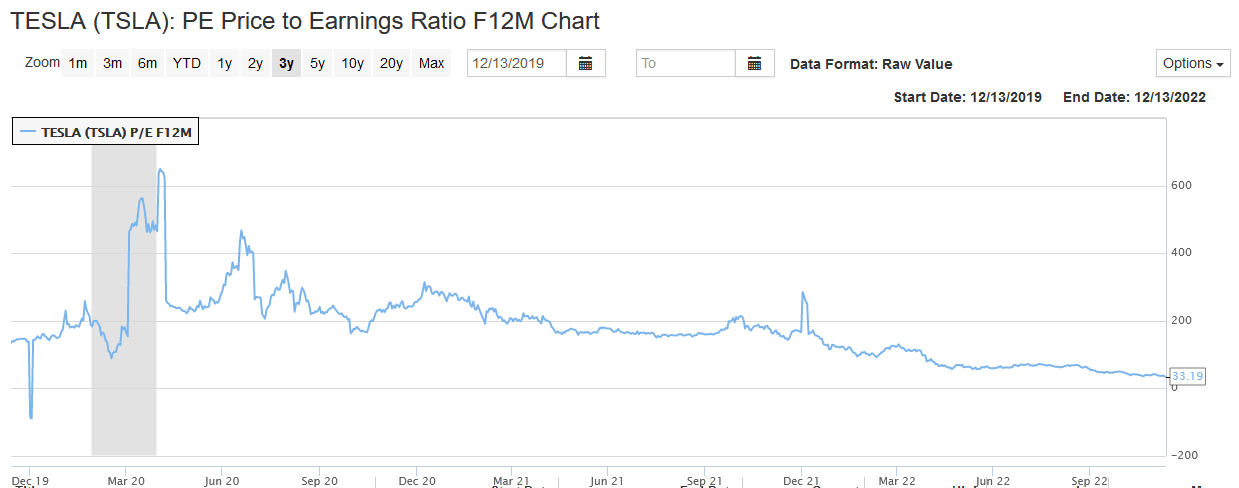

Tesla is Cheaper But Far From Cheap

We are starting to hear a few analysts claim that the 60% decline in Tesla’s stock price this year is finally bringing its forward P/E valuation to fair value. As shown below, the forward P/E has fallen to 33 from as high as 600 three years ago.

We differ. For starters, the S&P 500 has a forward P/E of 19. More importantly, the auto industry tends to have lower than market valuation ratios. For example, Ford has a forward P/E of 7, and GM’s is 6. Tesla is growing more rapidly than other automakers, so analysts can correctly claim that Tesla’s valuation should be higher.

However, one must consider that Tesla has a market cap of over $500 billion, about $450 billion more than Ford. This is despite the fact that Ford generates twice the sales of Tesla. Given the preponderance of new EV vehicles hitting the market and the potential damage Elon Musk, via his Twitter purchase, is doing to the Tesla brand, we suggest the odds of Tesla’s market cap falling in line with other traditional automakers is a distinct possibility. If so, Tesla may be cheaper, but it is far from cheap.

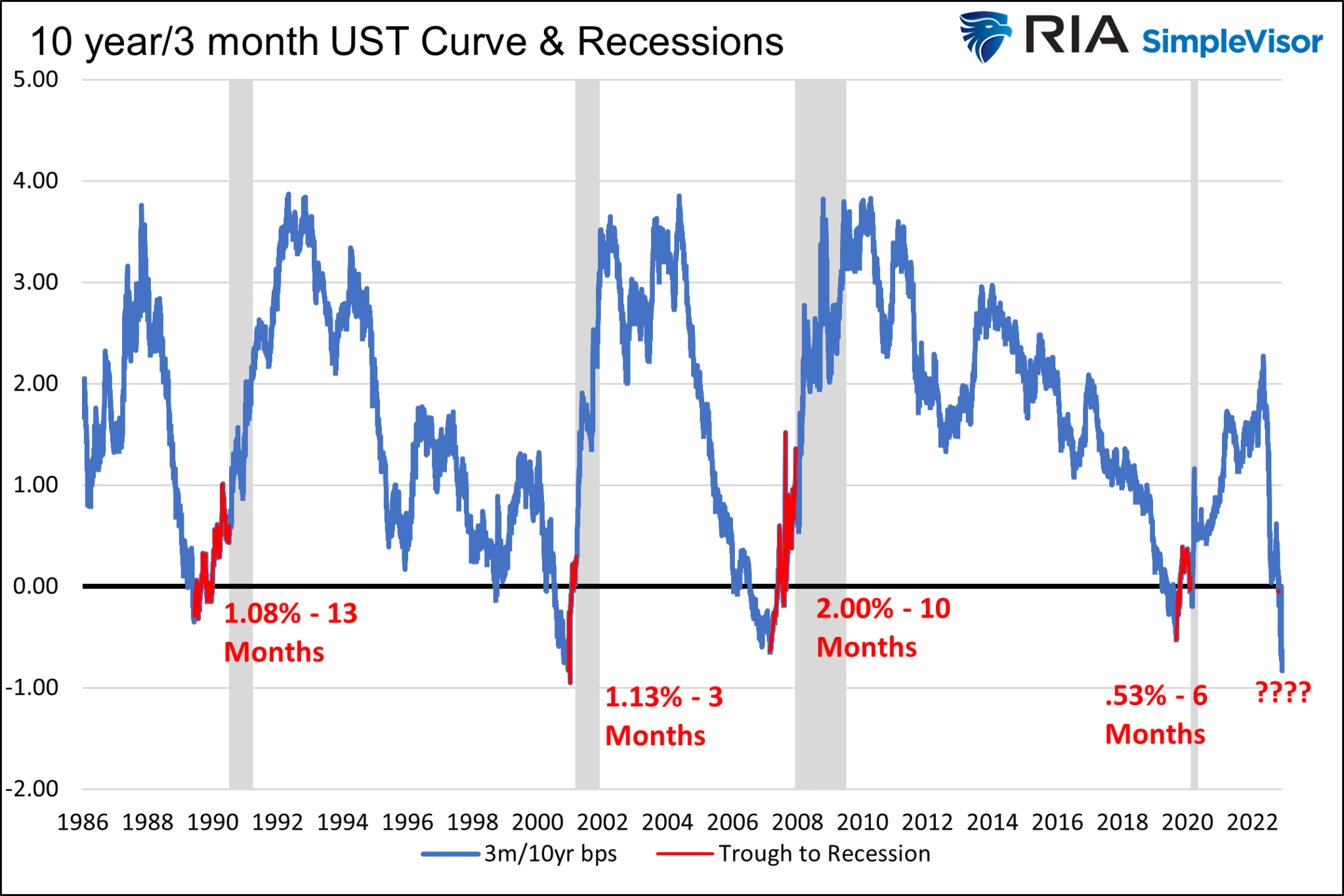

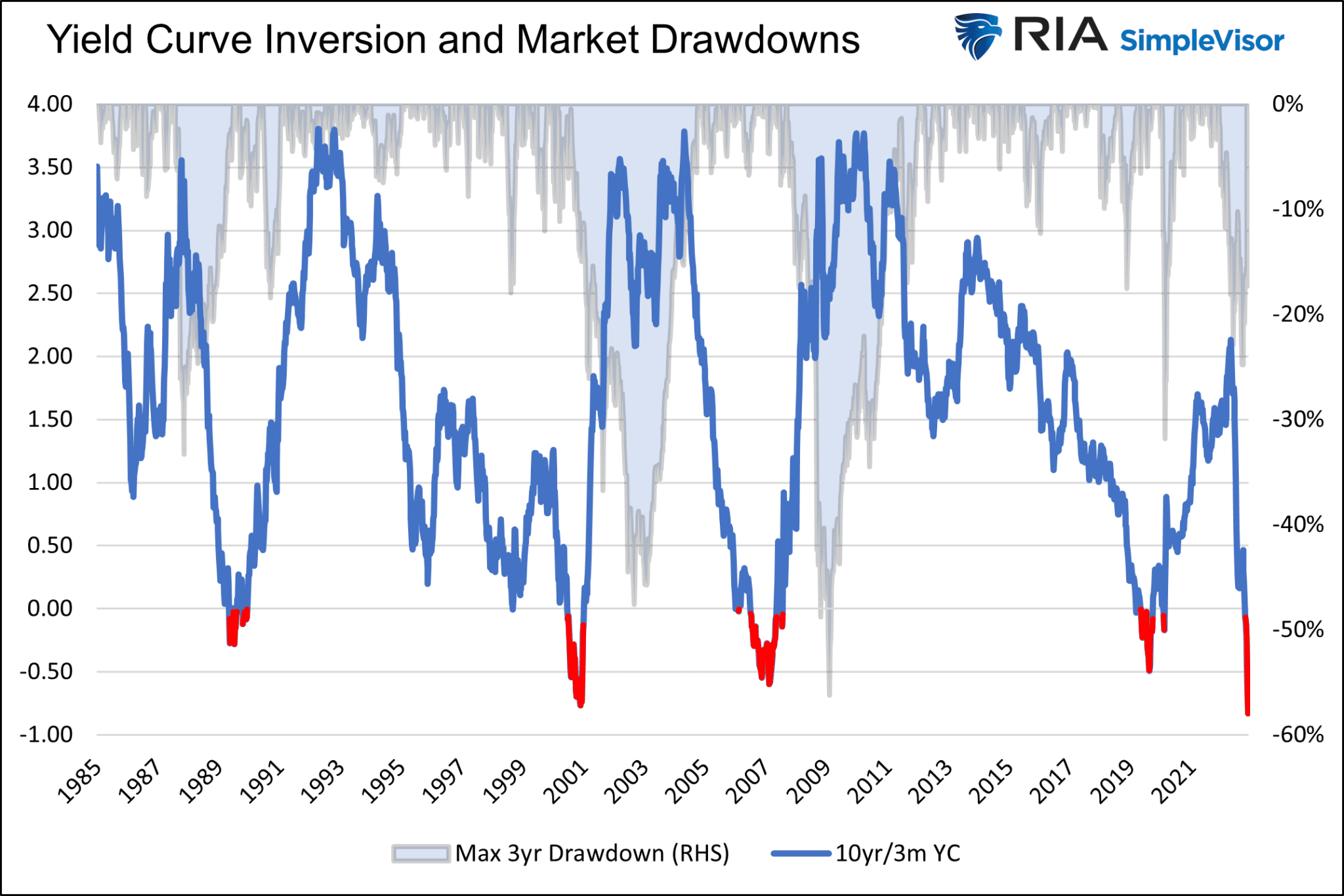

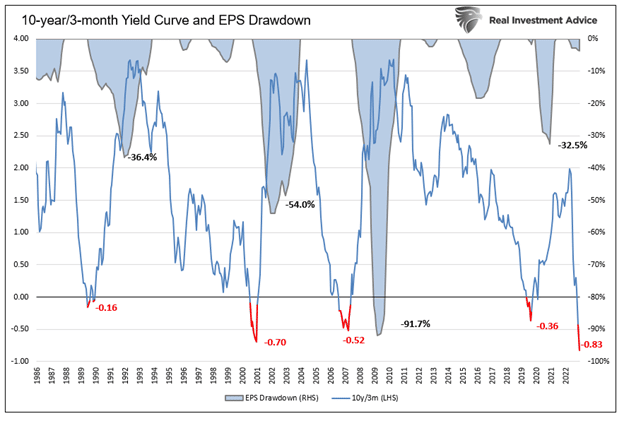

Its the Steepening, Not The Inversion, That Scares Us

On Wednesday, we published The Foghorn is Blowing, But Few Heed Its Warning. The article shares a few graphs, some of which are below, to help consider how the yield curve will steepen from its current inverted level. As shown, inverted yield curves tend to steepen in a sharp “V” shaped pattern. Recessions do not begin, and equity prices do not bottom until the curve is positively sloped. The most likely reason for the curve to steepen is aggressive Fed easing. Maybe the Fed will pull a rabbit out of its hat, and this time will be different. However, history warns that inverted yields always un-invert and often accompany economic and financial damage.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read