In 1976, a professor of economic history at the University of California, Berkeley published an essay outlining the fundamental laws of a force he perceived as humanity’s greatest existential threat: Stupidity.

Stupid people, Carlo M. Cipolla explained, share several identifying traits:

- they are abundant,

- they are irrational, and;

- they cause problems for others without apparent benefit to themselves

The result is that “stupidity” lowers society’s total well-being and there are no defenses against stupidity. According to Cipolla:

“The only way a society can avoid being crushed by the burden of its idiots is if the non-stupid work even harder to offset the losses of their stupid brethren.”

Let’s take a look at Cipolla’s five basic laws of human stupidity as they apply to investing and the markets today.

Law 1: Always and inevitably everyone underestimates the number of stupid individuals in circulation.

“No matter how many idiots you suspect yourself surrounded by you are invariably low-balling the total.”

In investing, the problem of investor “stupidity” is compounded by a variety of biased assumptions that are made. Individuals assume that when the media publishes something, the superficial factors like the commentator’s job, education level, or other traits suggest they can’t possibly be stupid. We, therefore, attach credibility to their opinion as long as it confirms our own.

This is called “confirmation bias.”

If we believe the stock market is going to rise, then we tend to only seek out news and information that supports our view. This confirmation bias is a primary driver of the psychological investing cycle of individuals as shown below. I discussed this previously in why “Media Headlines Will Lead You To Ruin.”

As individuals, we want “affirmation” our current thought processes are correct. As human beings, we hate being told we are wrong, so we tend to seek out sources that tell us we are “right.”

This is why it is always important to consider both sides of every debate equally and analyze the data accordingly. Being right and making money are not mutually exclusive.

Law 2: The probability that a certain person be stupid is independent of any other characteristic of that person.

Cipolla posits stupidity is a variable that remains constant across all populations. Every category one can imagine—gender, race, nationality, education level, income—possesses a fixed percentage of stupid people.

When it comes to investing, ALL investors, individual and professionals, are subject to making “stupid” decisions. As I discussed recently:

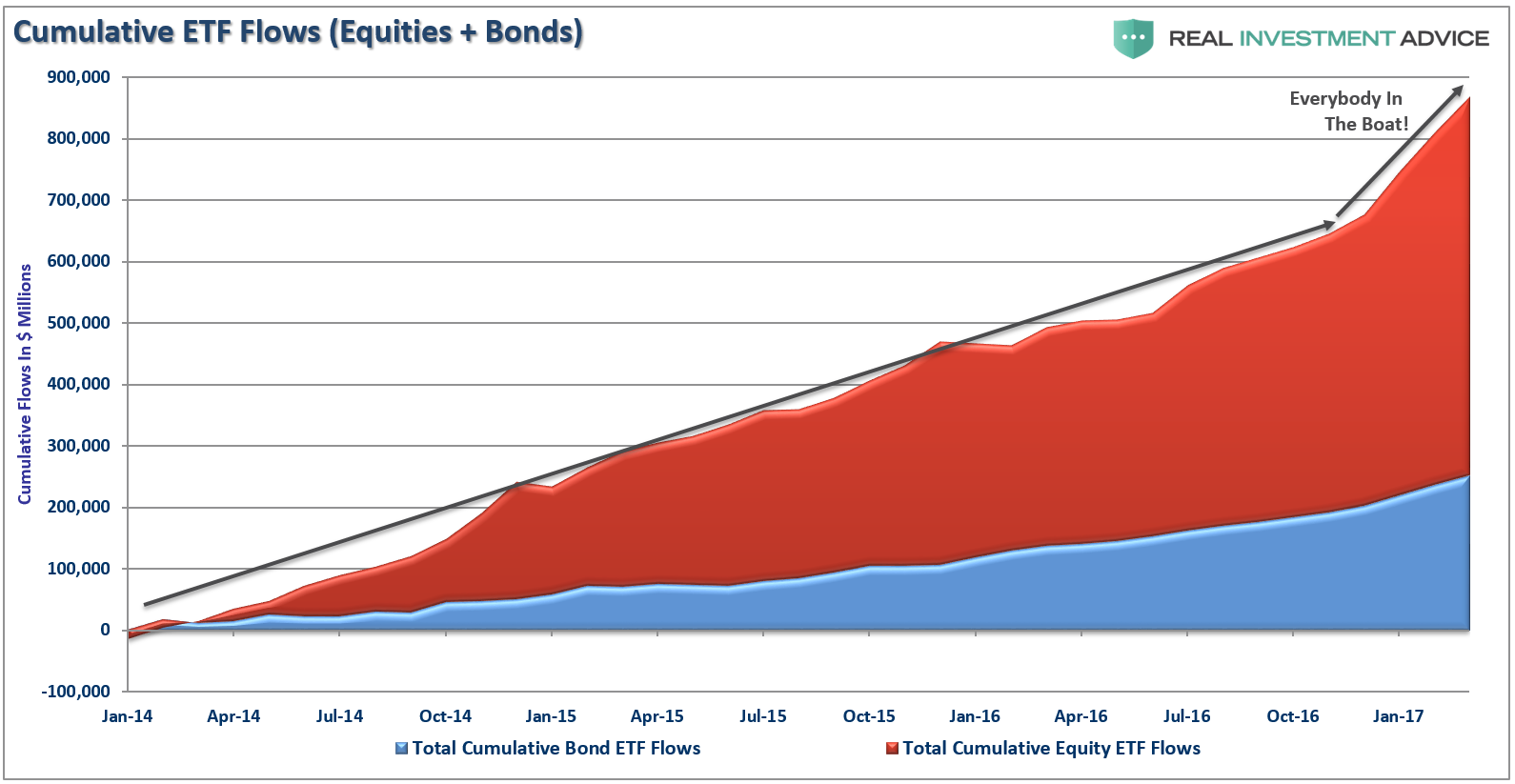

“At each major market peak throughout history, there has always been something that became “the” subject of speculative investment. Rather it was railroads, real estate, emerging markets, technology stocks or tulip bulbs, the end result was always the same as the rush to get into those markets also led to the rush to get out. Today, the rush to buy “ETF’s” has clearly taken that mantle, as I discussed last week, and as shown in the chart below.”

It isn’t the surge into equity ETF’s which should give rise to concern about future outcomes, but the components of “psychology” behind it.

Though we are often unconscious of the action, humans tend to “go with the crowd.” Much of this behavior relates back to “confirmation” of our decisions but also the need for acceptance. The thought process is rooted in the belief that if “everyone else” is doing something, then if I want to be accepted, I need to do it too.

In life, “conforming” to the norm is socially accepted and in many ways expected. However, in the financial markets, the “herding” behavior is what drives market excesses during advances and declines.

As Howard Marks once stated:

“Resisting – and thereby achieving success as a contrarian – isn’t easy. Things combine to make it difficult; including natural herd tendencies and the pain imposed by being out of step, since momentum invariably makes pro-cyclical actions look correct for a while. (That’s why it’s essential to remember that ‘being too far ahead of your time is indistinguishable from being wrong.’

Given the uncertain nature of the future, and thus the difficulty of being confident your position is the right one – especially as price moves against you – it’s challenging to be a lonely contrarian.”

Moving against the “herd” is where the most profits are generated by investors in the long term. The difficulty for most individuals, unfortunately, is knowing when to “bet” against those who are being “stupid.”

Law 3. A stupid person is a person who causes losses to another person or to a group of persons while himself deriving no gain and even possibly incurring losses.

Consistent stupidity is the only consistent thing about the stupid. This is what makes stupid people so dangerous. As Cipolla explains:

“Essentially stupid people are dangerous and damaging because reasonable people find it difficult to imagine and understand unreasonable behavior.“

Throughout history, investors are constantly drawn into investment strategies promoted by a wide variety of “industry professionals” which ultimately leads to losses in the end. This point was clearly made in a recent article by Jason Zweig entitled: “Whatever You Do, Don’t Read This Column.”

“Investors believe the darnedest things.

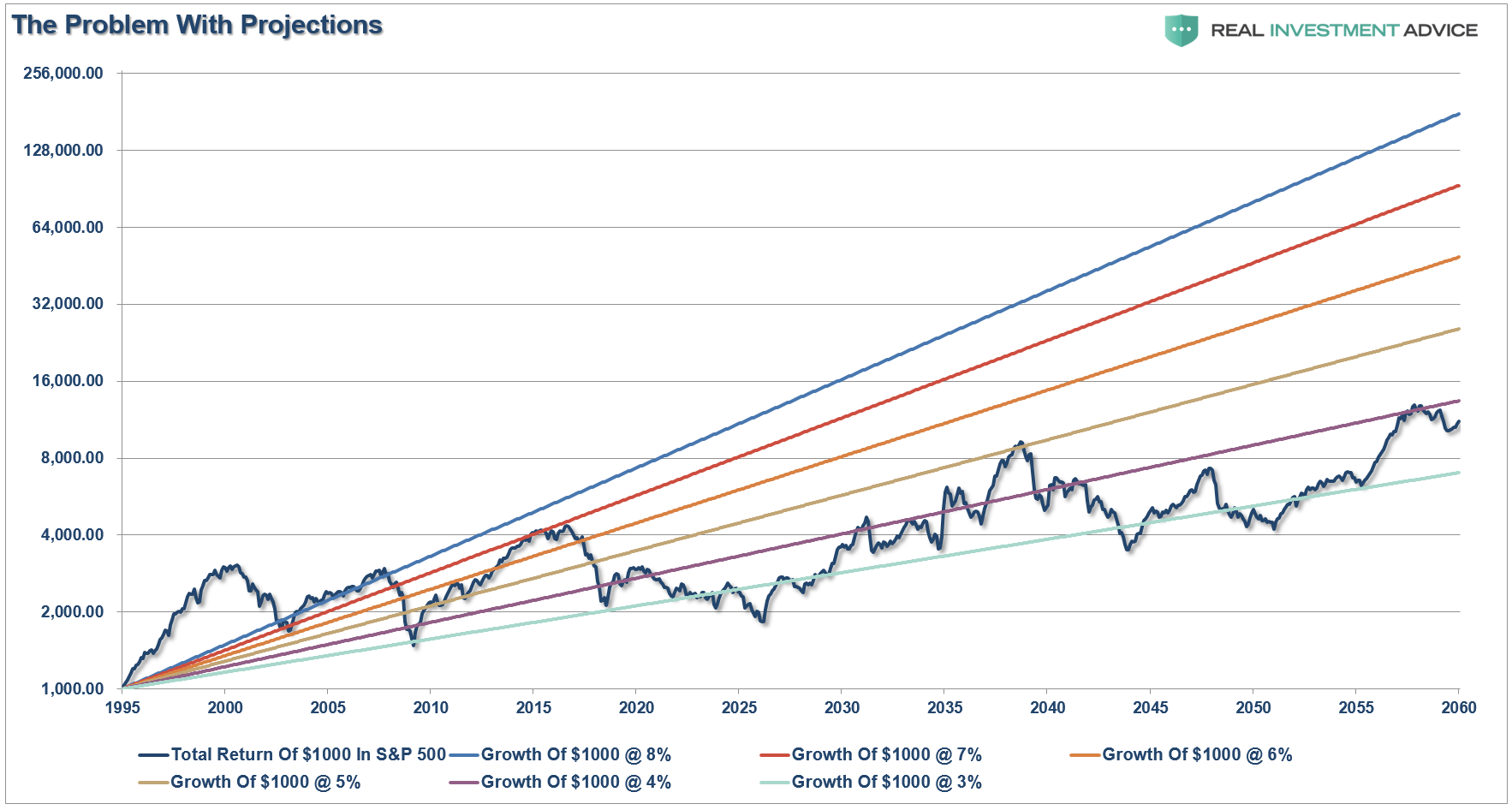

In one recent survey, wealthy individuals said they expect their portfolios to earn a long-run average of 8.5% annually after inflation. With bonds yielding roughly 2.5%, a typical stock-and-bond portfolio would need stocks to grow at 12.5% annually in order to hit that overall 8.5% target. Net of fees and inflation, that would require approximately doubling the 7% annual gain stocks have produced over the long term.

Individuals aren’t the only investors who believe in the improbable. One in six institutional investors, in another survey, projected gains of more than 20% annually on their investments in venture capital — even though such funds, on average, have underperformed the stock market for much of the 2000s.

Although almost nothing is impossible in the financial markets, these expectations are so far-fetched they border on fantasy.”

He is absolutely right, and despite the historical realities of investing, both the individual and the professional will ultimately suffer losses. As shown in the chart below, there is no evidence which shows markets can compound high levels of growth rates from current valuation levels. (For more detail on forward returns read “Valuations Matter”)

There is a massive difference between AVERAGE and ACTUAL returns on invested capital. The impact of losses, in any given year, destroys the annualized “compounding” effect of money.

Individuals who experienced either one, or both, of the last two bear markets, now understand the importance of “time” relating to their investment goals. Individuals that were close to retirement in either 2000, or 2007, and failed to navigate the subsequent market draw downs have had to postpone their retirement plans, potentially indefinitely.

But yet despite the losses incurred by both professionals and individuals, just eight short years after the largest financial crisis since the “Great Depression,” individuals are piling on excessive risk once again under the guise “this time is different.”

Talk about stupid.

Despite the mainstream media’s consistent drivel investors should just “passively index” and forget about actually managing the risk of catastrophic capital loss, the reality is that investors “buy high and sell low” for a reason.

“Greed” and “Fear” are far more powerful in driving our investment decisions versus “Logic” and “Discipline.”

As Jason states:

“The traditional explanations for believing in an investing tooth fairy who will leave money under your pillow are optimism and overconfidence: Hope springs eternal, and each of us thinks we’re better than the other investors out there.

There’s another reason so many investors believe in magic: We can’t handle the truth.”

All of which leads us to:

Law 4: Non-stupid people always underestimate the damaging power of stupid individuals. In particular non-stupid people constantly forget that at all times and places and under any circumstances to deal and/or associate with stupid people always turns out to be a costly mistake.

Lot’s of “non-stupid people” are currently suggesting the next correctionary event will be mild, most likely no more than 20%. The idea is based upon the belief the Federal Reserve, and Central Banks globally, will quickly come to the rescue of a failing market and investors will quickly react by once again jumping back into the market.

However, as we have seen repeatedly throughout history, “stupid” people tend to do exactly the opposite during a crisis than what “non-stupid” people expect.

Then there are the “perennial bulls” who keep telling investors to “hang on, keep putting money in, you’re a long-term investor, right?” These are the ones who never see the bear market destruction until well after the fact and then simply say “well, no one could have seen that coming.”

Non-stupid people are conservative. They analyze the risk of loss and conserve capital during declines. Make sure you are surrounding yourself with those that understand the “math of loss.”

As Howard Marks stated above, sometimes being a contrarian is lonely.

When we underestimate the stupid, we do so at our own peril.

This brings us to the fifth and final law:

Law 5: A stupid person is the most dangerous type of person.

Following the “herd,” has always ended badly for investors. In every full-market cycle, there is an inevitable belief “this time is different” for one reason or another.

It isn’t. It has never been. And this time will not be different either.

However, what has always separated out the great investors from everyone else, is they have acted independently of the “herd.” They have a discipline, a strategy and a driving will to succeed.

They don’t “buy and hold.” They buy cheap and sell expensive. They avoid losses at all costs and they deeply understand the relationship of risk to reward.

They are the “non-stupid.”

These are the ones you want to follow.

Not the ones screaming at you on television telling you to “buy, buy, buy.”

Just remember that for every full-market cycle our job is to not only participate in the first-half of the cycle as prices rise, but to avoid the avoid the devastation during the second-half.

“Non-stupid” investors don’t spend a bulk of their time getting back to even.

That is an investing strategy better left to the “herd.”

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read