Coal miners used to bring canaries into the mines to protect themselves from harmful gases. The canary will keel over if the gas levels increase, giving the miners time to exit before meeting the same fate. In the same vein, no pun intended, there is a corporate bond credit spread that can serve as an economic canary.

Corporate credit spreads, or the difference between a bond’s yield and Treasury yields, measure the perceived risk of default. Thus, the higher the spread, the greater the premium investors demand to insure against default. From AAA to junk-rated credit, spreads are historically tight. Thus, investors are not overly concerned about economic weakness, which usually precedes defaults. However, a closer inspection of credit spreads by ratings exposes a bit of a warning.

Our canary is the difference between the highest-rated junk bonds, BB, and the junk bonds closest to default, CCC. As shown, CCC bond spreads have been rising. However, BB spreads continue to drift lower. The increased spread between BB and CCC is only minor. In other words, the canary just coughed. Let’s watch the canary to see if its condition worsens.

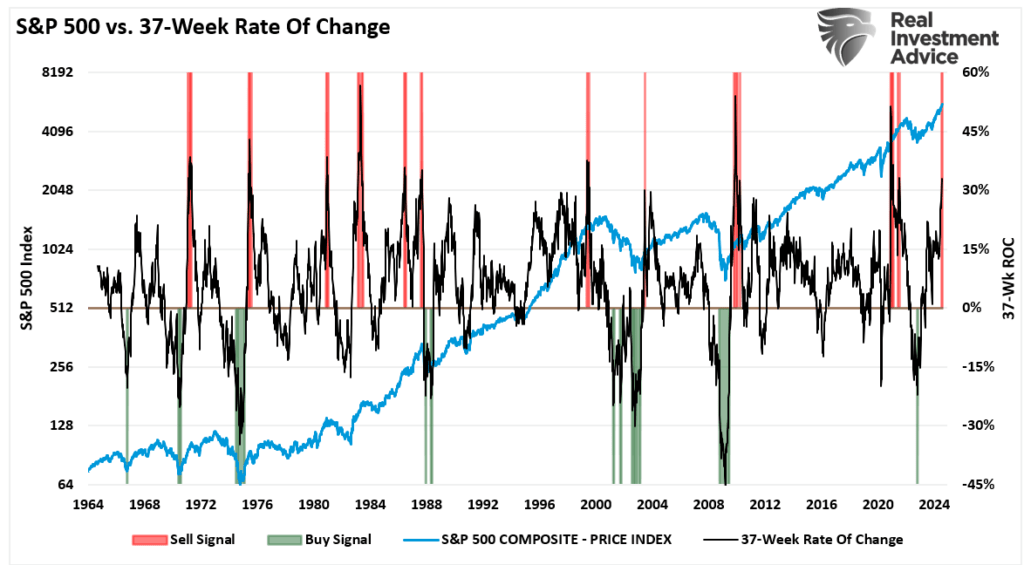

“The rally that began in late October is one of the longest rallies in history. The chart below shows the 37-week rate of change for the S&P 500 index. While there have certainly been periods with larger percentage gains, the current change exceeds 30%, which has historically preceded corrections and consolidations. Conversely, 20% or greater reversions have been decent buying opportunities for investors. The shaded periods show the buying and selling opportunities that have not been that numerous since 1964.”

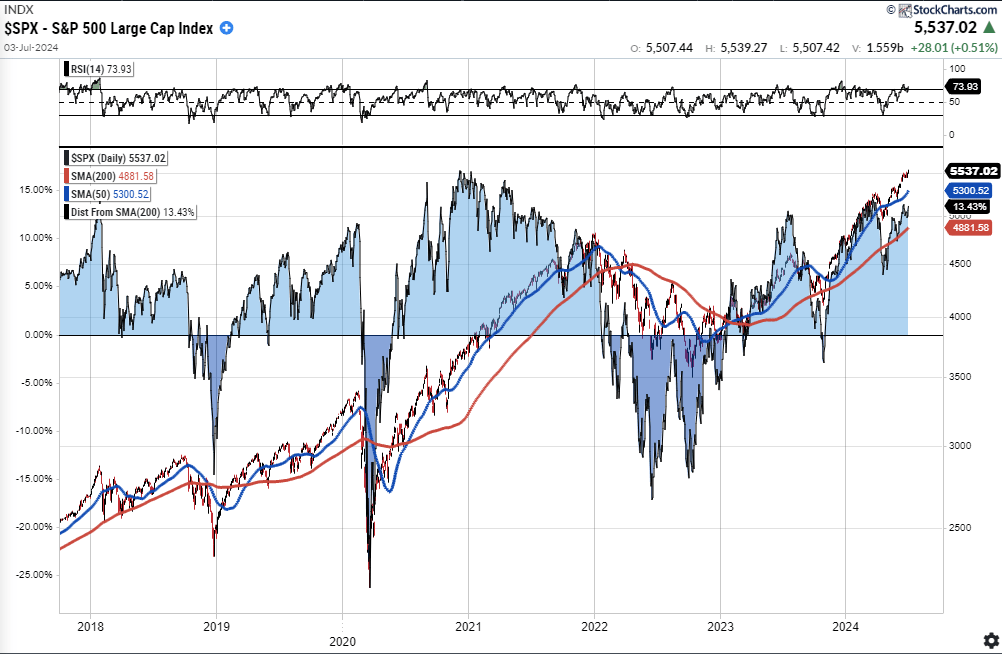

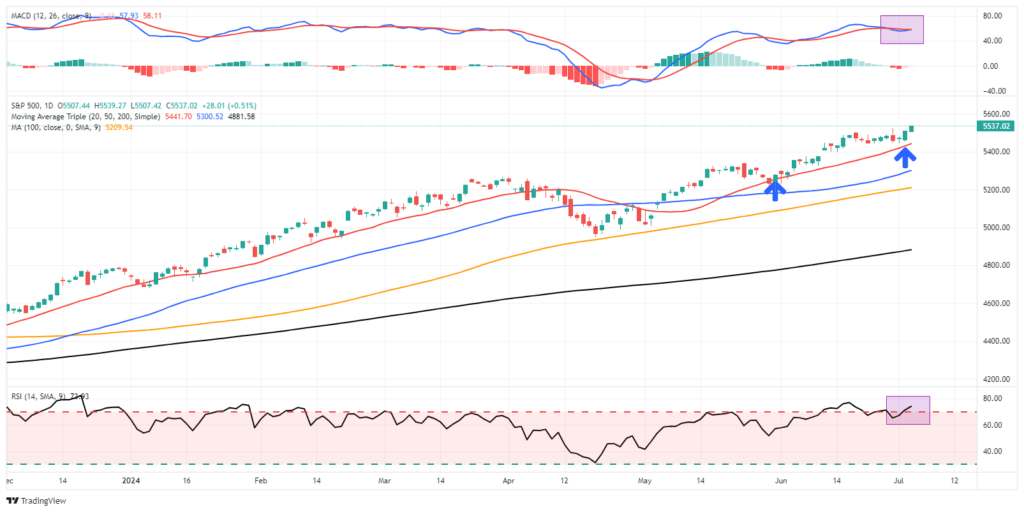

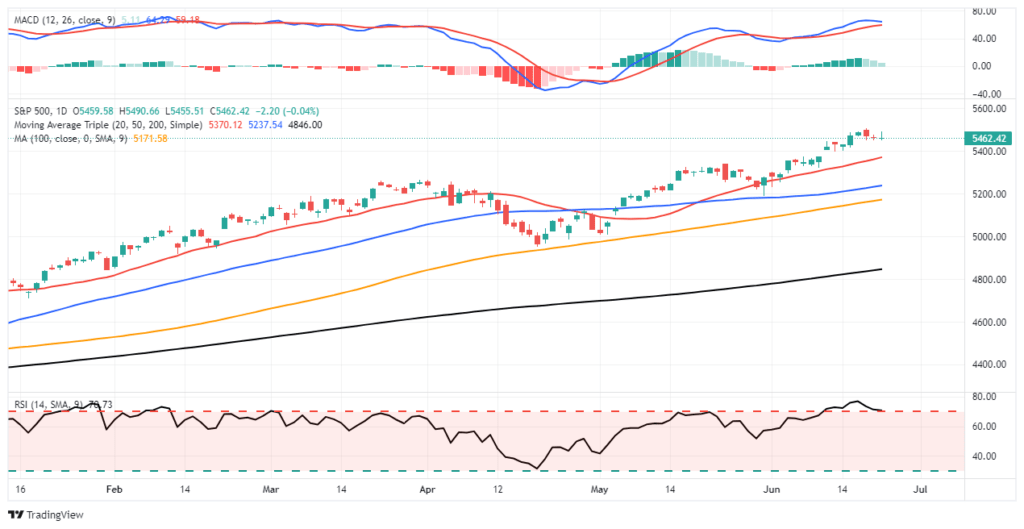

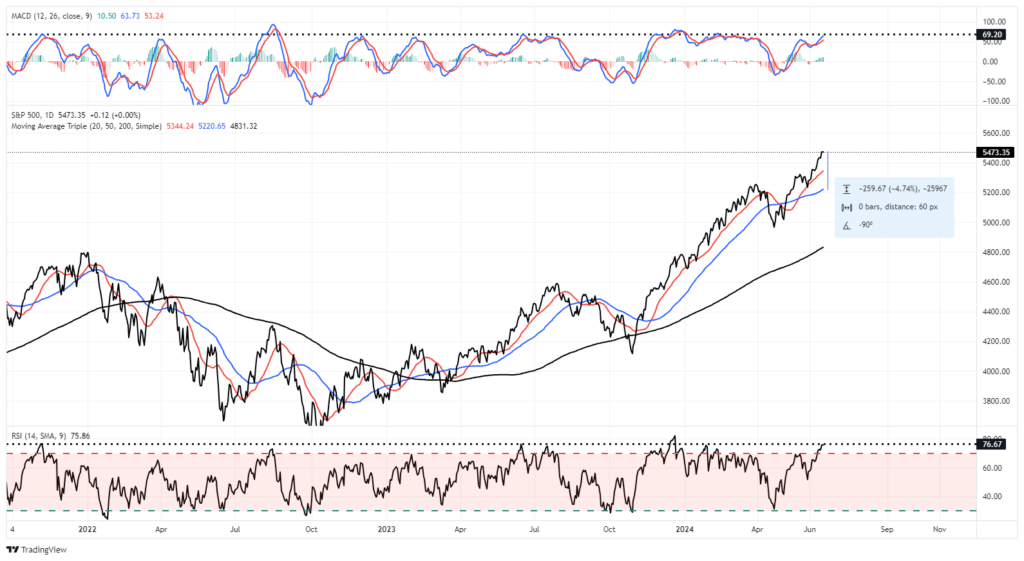

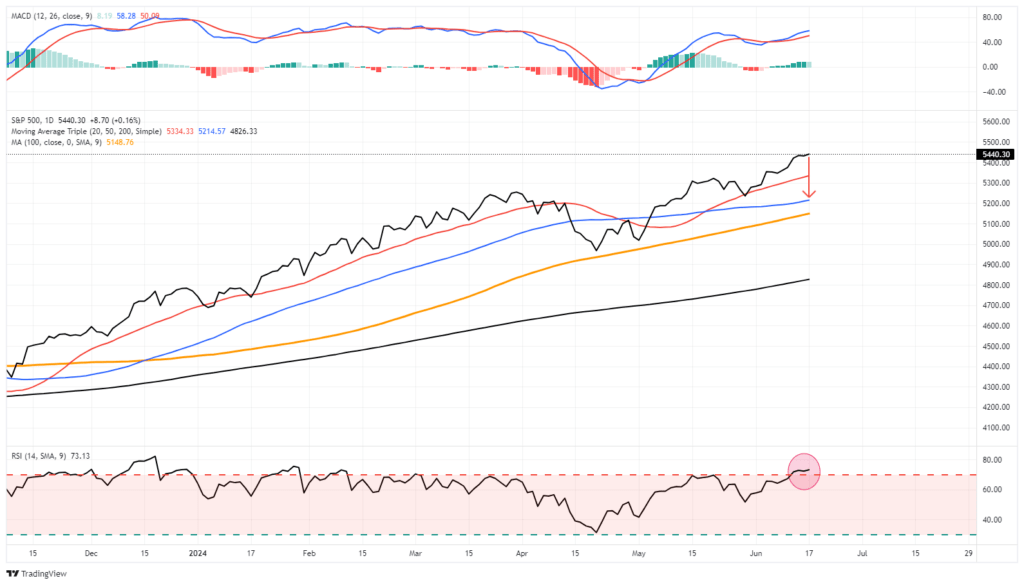

As discussed last week, the market did indeed flip that “sell signal,” pushing higher and topping 5600 for the first time. However, it also pushed the market back into extremely overbought territory, and the deviation from the 50-DMA is quite significant. Such suggests that, as we saw in late May and June, the market will either consolidate or correct back to the 20-DMA. If the bulls can hold that level again, as they have, the market could continue to push higher. Such is possible given the current exuberance surrounding the Fed cutting rates. However, if the 20-DMA fails, as in early April, the 50-DMA becomes the next logical support, with the 100-DMA close behind. Such would encompass another 3-5% correction.

With the market continuing its “non-stop” advance, the bulls have become emboldened to take on more risk and are unconcerned about the risk of a correction. Such often does not end well, but as Warren Buffett once quipped:

“The markets are a lot like sex; it feels best just before the end.”

The Week Ahead

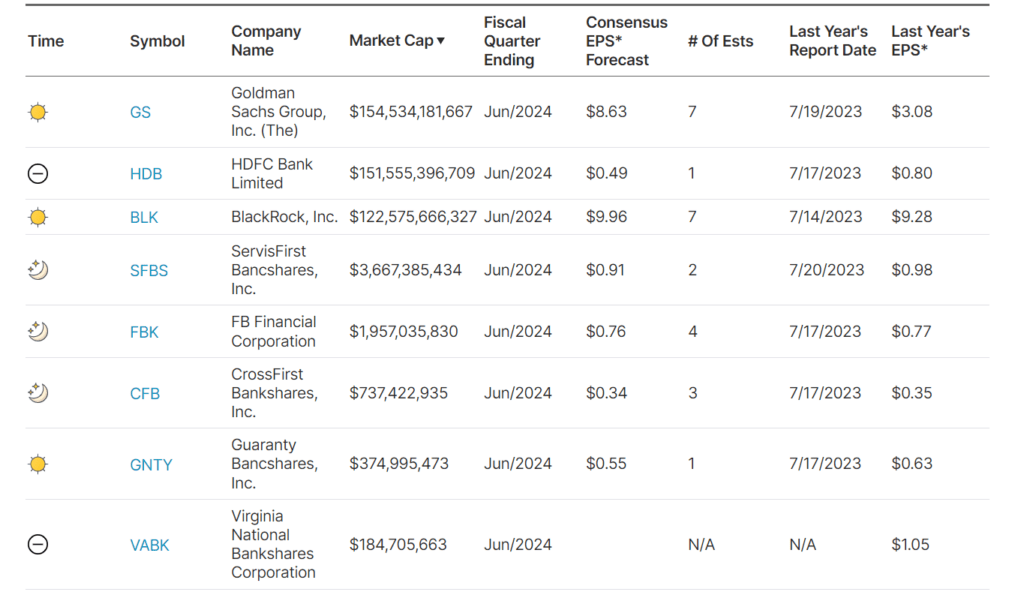

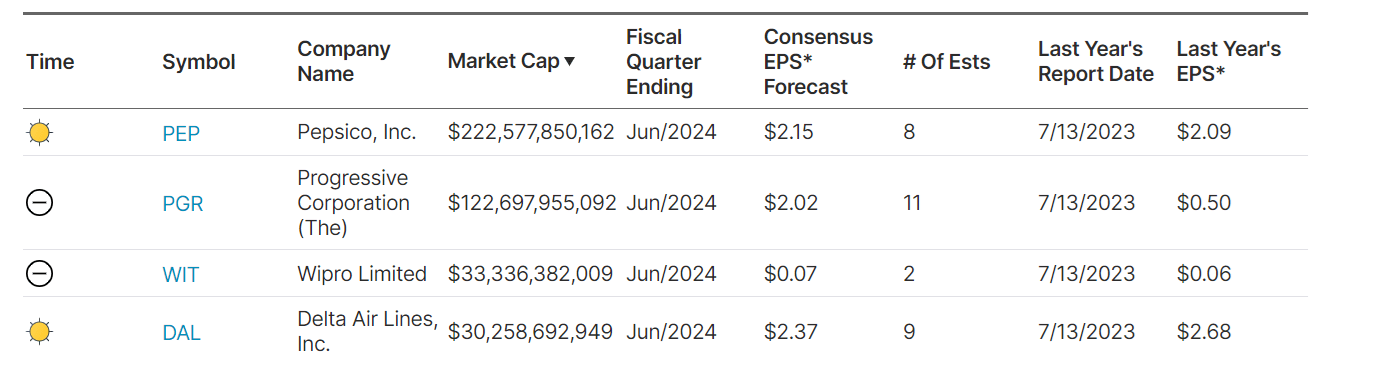

With inflation and the unemployment reports in the rearview mirror, corporate earnings will take center stage. Leading the list are Goldman Sachs, Bank America, United Healthcare, J&J, Netflix, and American Express. We will be watching to see if companies can maintain higher-than-average profit margins despite normalizing inflation. Furthermore, companies like J&J, American Express, and United will provide insight into personal consumption.

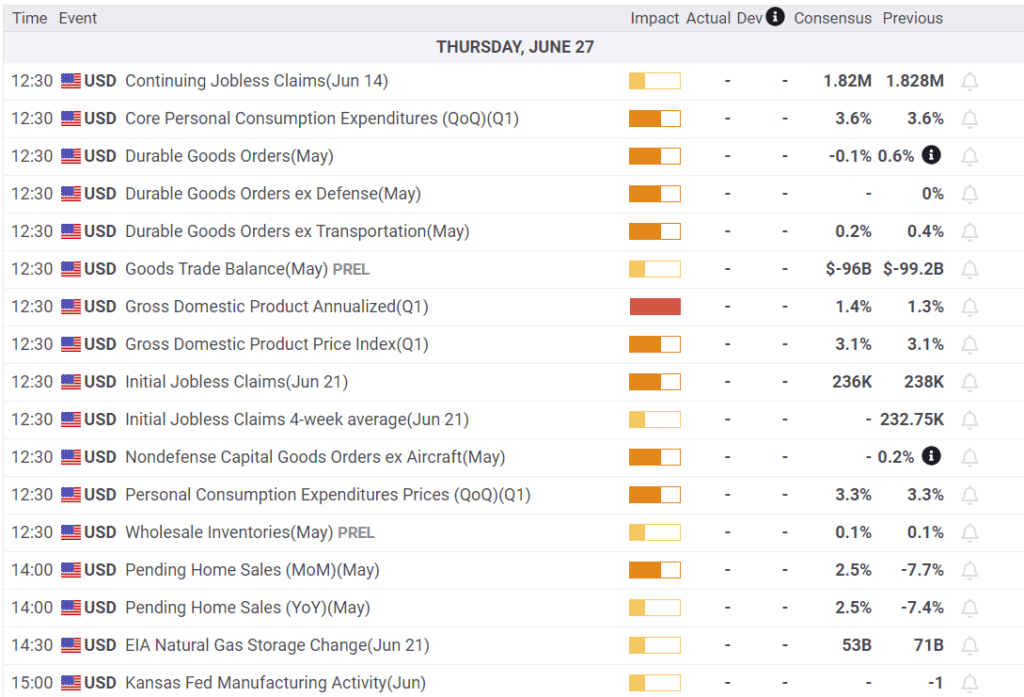

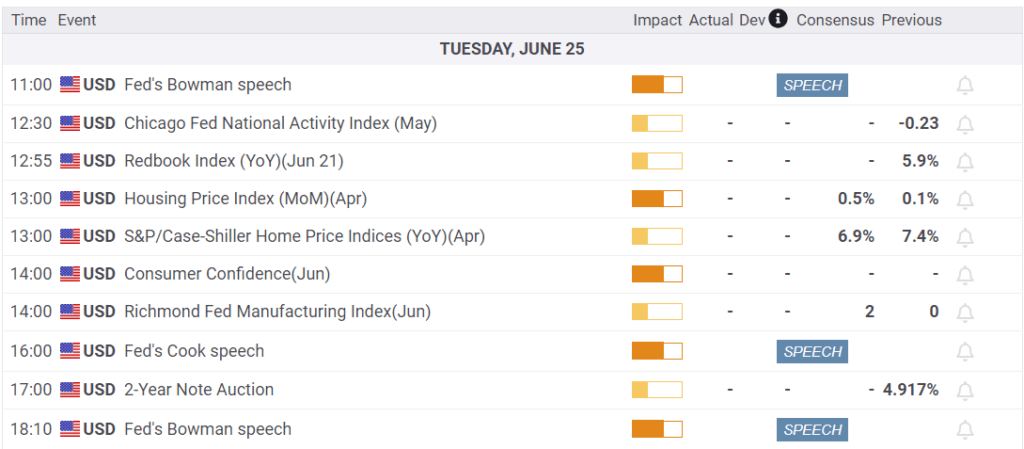

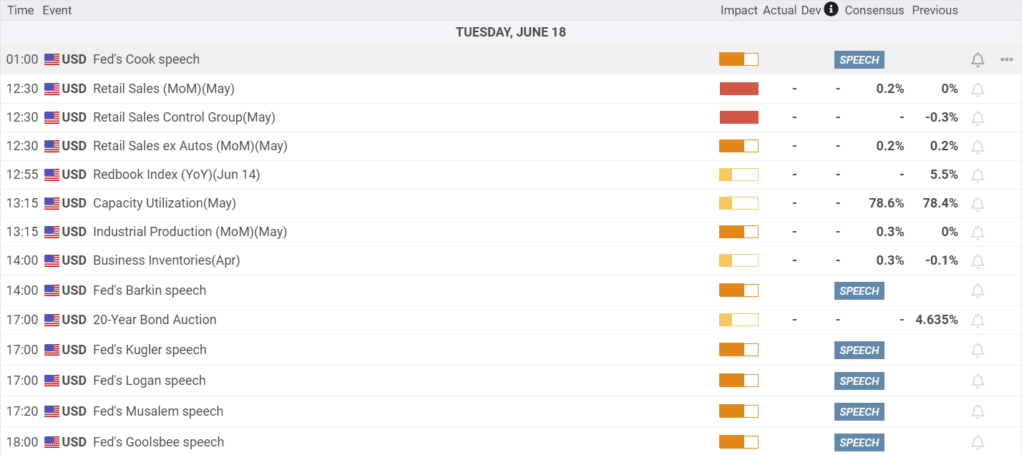

Jerome Powell will speak again today. He may opine on the latest inflation data and how that affects the Fed’s outlook. Also on the calendar is Retail Sales on Tuesday.

Bizarro Stocks

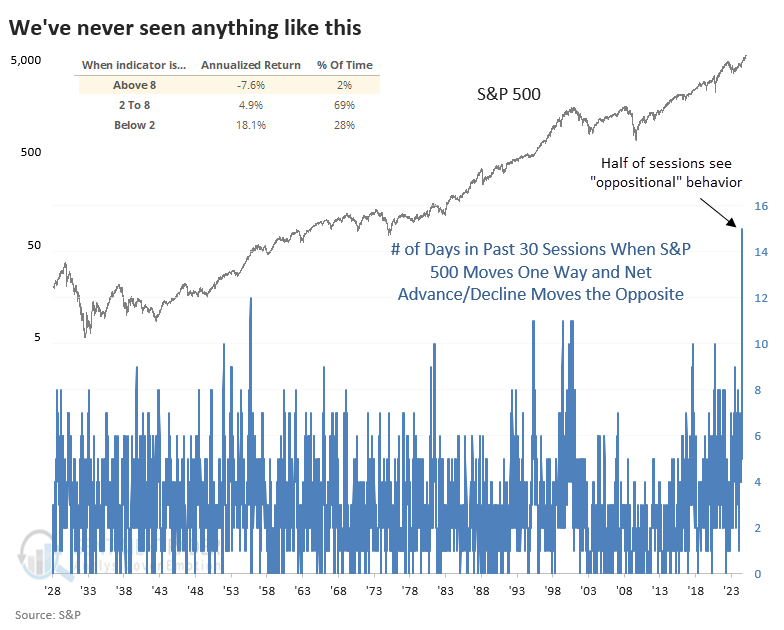

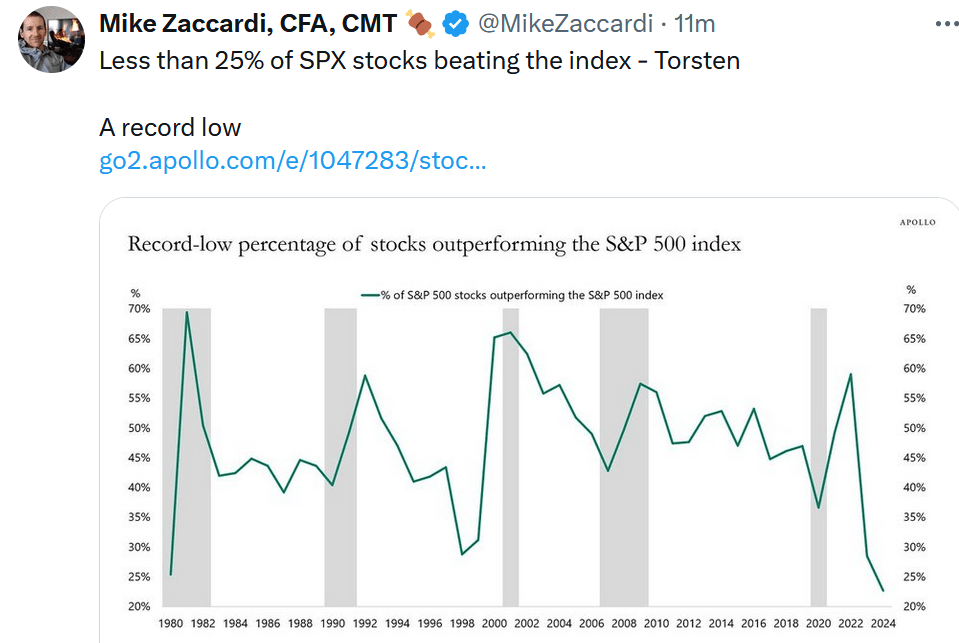

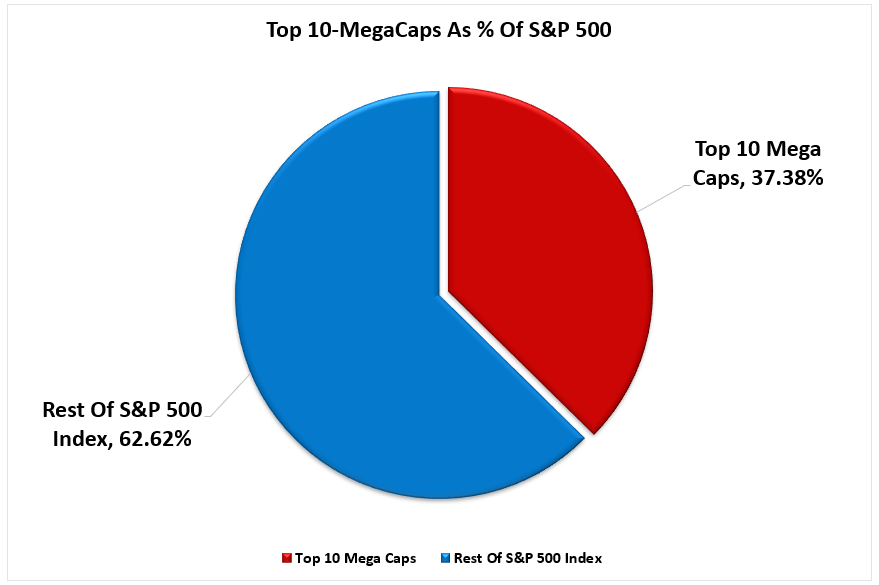

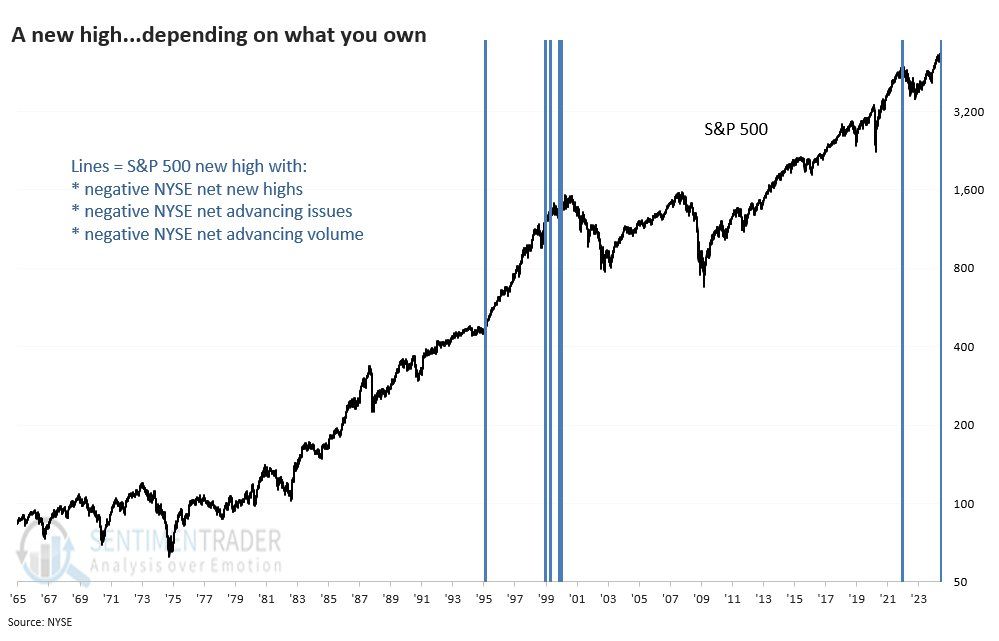

Sentimentrader shared the graph below, showing that fifteen of the last thirty days have seen the S&P 500 index move in the opposite direction as the advance-decline line. The next closest instance, going back to 1928, is 12 days. The table on the top left shows that prior instances when the number of occurrences was above eight were followed by an average annualized return of -7.6%. Furthermore, about 40% of stocks in the S&P 500 are down this year despite the index being up nearly 20%.

Bizzaro stats like these and many others attest to the heavy contribution of large-cap stocks to index returns and how they mask underlying market weakness. The top 30 stocks account for over half of the index. Moreover, Microsoft, Apple, Nvidia, and Amazon account for 25% of the total.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Prices Decline Raising The Odds Of A Rate Cut

The Consumer Price Index (CPI) fell 0.1% last month, following 0.0% the prior month and expectations for a 0.1% increase. Core prices rose 0.1%, a tenth below last month’s reading and the consensus forecast. Year-over-year inflation is down to 3.0%.

The better-than-expected inflation data further affirms the disinflation trend may be back on track. The two graphs below, charting the three-month average of the monthly CPI and the year-over-year CPI, show they are nearing the ten-year average preceding the pandemic and well below the high levels we saw in 2022.

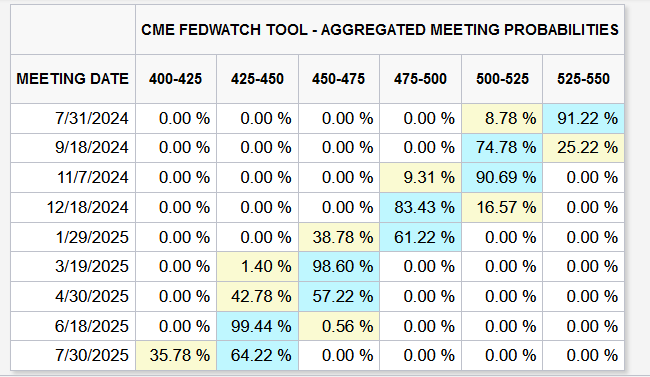

Before cutting interest rates, the Fed may want another month or two of CPI and PCE prices at or below the pre-pandemic average. Such would confirm the year-over-year trend is back on a downward trajectory. However, the Fed is now balanced regarding its reaction to prices and the labor market. If the next CPI is low and the labor market shows further signs of cooling, the September FOMC might be when the Fed makes the first rate cut of this cycle. The odds of a cut at the July 31 meeting rose slightly to 10%. Furthermore, the odds are over 80% that they will reduce rates in September.

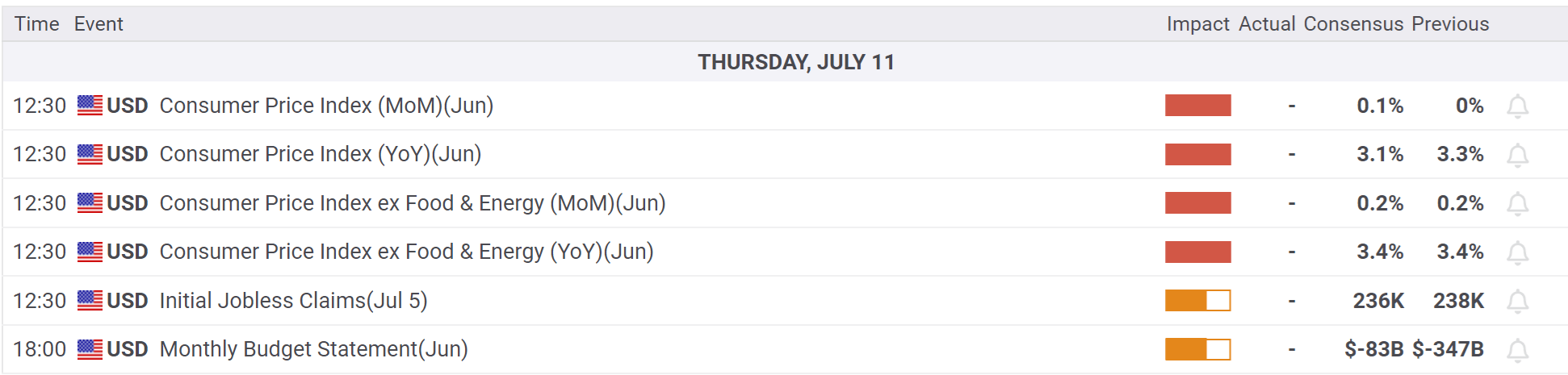

What To Watch Today

Earnings

Economy

Market Trading Update

As discussed yesterday, the market has continued to rise as investors chase a small handful of stocks. The rally that began in late October is one of the longest rallies in history. The chart below shows the 37-week rate of change for the S&P 500 index. While there have certainly been periods with larger percentage gains, the current change exceeds 30%, which has historically preceded corrections and consolidations. Conversely, 20% or greater reversions have been decent buying opportunities for investors. The shaded periods show the buying and selling opportunities that have not been that numerous since 1964.

Of course, as noted, just because the market rally currently exceeds 30% does not mean a reversal is imminent. It is just a warning that investors should pay attention to as they continue to manage risk.

Greg Valliere’s Washington Insight On Biden’s Chances

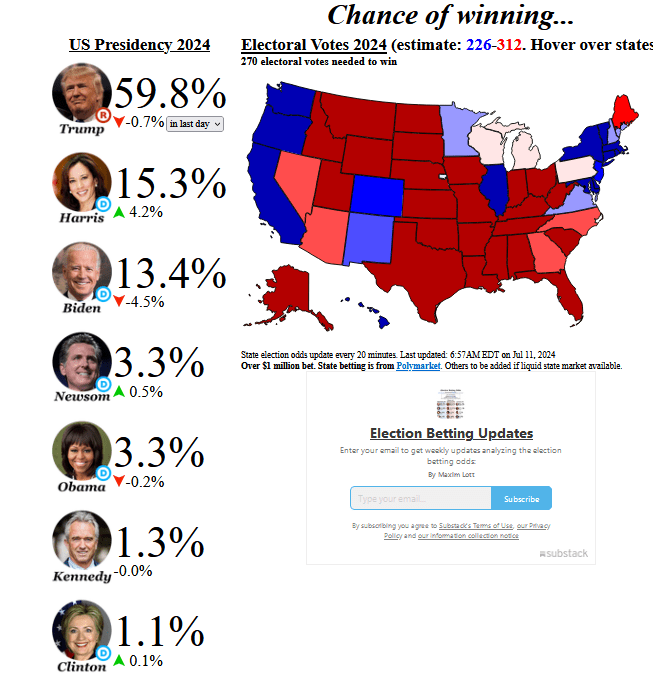

As promised, we occasionally provide Greg Valliere’s latest political insights throughout this election season. His 40+ years of experience analyzing and assessing the political landscape helps us gauge what the coming election may bring so we can focus on what that means for our investments.

Beneath his latest thoughts on the coming election and President Biden’s predicament, we share the current betting odds. The source is Election Betting Odds, which aggregates five betting platforms. As of yesterday, Kamala Harris is slightly favored over Joe Biden, while Donald Trump is the clear favorite.

THE ISSUE IS NOT WHETHER JOE BIDEN WILL STEP DOWN — it’s simply when, our sources are reporting, after the president’s campaign essentially collapsed yesterday. We have no idea when Biden will drop out — it could come as early as his press conference today, but more likely not until late July, ahead of the Democrats’ national convention, which runs from Aug.19 until Aug.22.

MOST POLLS SHOW BIDEN TRAILING by only 2 or 3 points nationwide, a remarkably tight margin, considering his disastrous debate performance two weeks ago. Why?

OUR TAKE is that most voters made up their minds months ago — and they tuned out of the cringe-inducing debate. The public shrugged off the Trump guilty verdicts in NYC, which had virtually no impact on the polls. And the public probably isn’t wondering about Biden’s Parkinson’s doctor.

THE RACE MAY BE SURPRISINGLY CLOSE, but the outlook isn’t good for Biden because he still trails in virtually all of the key battleground states — Georgia, Nevada, Arizona, North Carolina, etc. And in the most important state of all — Pennsylvania — Trump appears to be ahead. Biden has a small lead in Wisconsin and Michigan.

THE ELECTORATE DECIDED MONTHS AGO that Biden was too old to be president, and that concern has grown. The public overwhelmingly believes that Biden isn’t fit to serve for four and a half more years; perhaps the only game changer would be signs that Trump’s cognitive skills are failing — but you underestimate Trump at your own peril.

Is Private Equity For You?

Lance Roberts wrote a thoughtful article this week about private equity. His article, Private Equity – Why Am I so Lucky, helps readers appreciate the rapidly growing $4.4 trillion asset class. Notably, he provides three risks often accompanying private equity investments and why they may be better served for high-net-worth individuals and pension and endowment funds. To wit:

There are significant differences to consider between the vast majority of retail investors and high-net-worth individuals before investing in private equity. The underlying risks of private equity investments can define these differences. There are many risks, but I want to focus on three.

Liquidity Risk

Duration

Loss Absorption

He thoroughly explains those risks and how they differ from traditional investments. Furthermore, he dispels the notion that private equity investments are better than the stocks and bonds most retail investors own. Per the article:

To that point, you should realize that most private equity investments (65%) either fail or return the initial investment at best.

The article does not dissuade individuals from making private equity investments. However, it raises awareness of the risks and complications associated with private equity and how they differ from what most stock and bond investors are used to.

Does this mean that you should never make a private equity investment? Of course not. However, you must understand the risk of investing and the potential ramifications on your financial situation when something goes wrong.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

The “Broken Clock” Fallacy & The Art Of Contrarianism

Some state that “bears are like a ‘broken clock,’ they are right twice a day.” While it may seem true during a rising bull market, the reality is that both “bulls” and “bears” are owned by the “broken clock syndrome.”

The statement exposes the ignorance or bias of those making such a claim. If you invert the logic, such things become more evident.

“If ‘bears’ are right twice a day, then ‘bulls’ must be wrong twice a day.”

In the investing game, the timing of being “wrong” is critical to your long-term goals. As discussed in “The Best Way To Invest,”

“There is a massive difference between AVERAGE and ACTUAL returns on invested capital. Thus, in any given year, the impact of losses destroys the annualized ‘compounding’ effect of money.”

Throughout history, bull market cycles are only one-half of the “full market cycle.” That is because, during every “bull market cycle,” the markets and economy build up excesses that are then “reversed” during the following “bear market.” In other words, as Sir Issac Newton once stated:

“What goes up, must come down.”

Bulls Are Wrong At The Worst Time

During rising bull markets, the bears become an easy target for ridicule. While the bears have logical arguments for why the markets should reverse, markets can often remain “illogical longer than you can remain solvent,” to quote John M. Keynes. Such is an important point because, as Howard Marks once quipped:

“Being early is the same as being wrong.”

The problem for perennially bearish people is that while they may eventually be deemed correct, they were so early to the call that they became the “boy who cried wolf.”

Robert Kiyosaki, who has long called for a market crash, is a good case study.

“But the real tragedy here is that one day he will be right. One day a crash will come and Kiyosaki will take a victory lap for all to see.

Will his prior incorrect calls matter? Not at all. You can try to point out his flawed track record, but it won’t make a difference. Most people aren’t going to see your reply. But what they will see is his tweet. They will feel the pain from the crash after it happens and then they will think, ‘Kiyosaki knew it all along.’”

Oh he got it wrong eight times before? Who cares? He is right now, isn’t he?” – NIck Mugulli

Nick is correct. No one will remember the “bears” wrong calls when the crash eventually comes. However, Nick is also incorrect because the same applies to the “bulls.”

For example, few remember Jim Cramer’s Top 10 Picksin March 2000 or the bullish media analysts who said “buy” through the entire 2008 crisis? But they remember the eventual “buy” recommendations that were eventually right. Unfortunately, few investors had capital left at that point.

We give Nick a pass because he is young and has not lived through an actual bear market. As anyone who has will tell you, it is not an adventure they care to repeat.

The problem with being “bullish all the time” is that when you are eventually wrong, it comes at the worst possible cost: the destruction of investment capital. However, being “bearish all the time” also has a price, such asfailing to grow investment capital to reach financial goals. While some investors left the market to avoid a 50% crash in 2008, they never returned for the subsequent 500% return. What was worse?

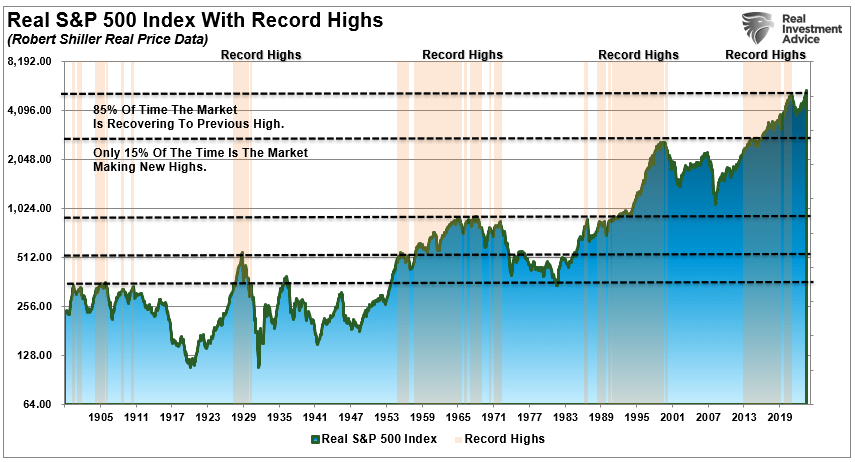

While the “bulls” seem to have their way during rising markets, the always-bullish media overlooks a problem. Over the past 120 years, the market has indeed risen. However, 85% of that time was spent making up previous losses, and only 15% making new highs.

The importance of this point should not be overlooked. Most investors’ “time horizon” only covers one market cycle. Suppose you are starting at or near all-time highs. In that case, there is a relatively significant possibility you may wind up spending a significant chunk of your time horizon “getting back to even.”

The “Art Of Being A Contrarian

The biggest problem for investors, and the “broken clock syndrome,” is the emotional biases by being either “bullish” or “bearish.” Effectively, when individuals pick a side, they become oblivious to the risks. One of the most significant factors is “confirmation bias,” where individuals seek confirmation and ignore non-confirming data.

As investors, we should avoid such a view and be neither bullish nor bearish. We should be open to all the data, weigh incoming data accordingly, and assess the risk inherent in our portfolios. That risk assessment should be an open analysis of our current positioning relative to the market environment. Being underweight equities in a rising bull market can be as harmful as being overweight in a bear market.

As a portfolio manager, I invest money in a way that creates short-term returns but reduces the possibility of catastrophic losses that wipe out years of growth.

We believe you should not be “bullish” or “bearish.” While being “right” during the first half of the cycle is essential, it is far more critical not to be “wrong” during the second half.

Howard Marks once stated that being a “contrarian” is tough, lonely, and generally right. To wit:

“Resisting – and thereby achieving success as a contrarian – isn’t easy. Things combine to make it difficult; including natural herd tendencies and the pain imposed by being out of step, particularly when momentum invariably makes pro-cyclical actions look correct for a while. (That’s why it’s essential to remember that ‘being too far ahead of your time is indistinguishable from being wrong.’)

Given the uncertain nature of the future, and thus the difficulty of being confident your position is the right one – especially as price moves against you – it’s challenging to be a lonely contrarian.”

The problem with being a contrarian is determining where you are during a market cycle. The collective wisdom of market participants is generally “right” during the middle of a market advance but “wrong” at market peaks and troughs.

As an individual, you can avoid the “broken clock“ syndrome.

Avoid the “herd mentality” of paying increasingly higher prices without sound reasoning.

Do your research and avoid “confirmation bias.”

Dev”lop a sound long-term investment strategy that includes “risk management” protocols.

Diversify your portfolio allocation model to include “safer assets.”

Control your “greed” and resist the temptation to “get rich quick” in speculative investments.

Resist getting caught up in “what could have been” or “anchoring” to a past value. Such leads to emotional mistakes.

Realize that price inflation does not last forever. The larger the deviation from the mean, the greater the eventual reversion. Invest accordingly.

Being a contrarian does not mean always going against the grain regardless of market dynamics. However, it does mean that when “everyone agrees,” it is often better to look at what “the crowd” may be overlooking.

QT Today: QE Tomorrow

The Fed’s balance sheet peaked at $9 billion in April 2022. Today, after two years of Quantitative Tightening (QT), it has fallen to $7.2 trillion. When the Fed embarked on QT, its goal was to “normalize” its balance sheet. At the time, the St. Louis Fed claimed the purpose of QT was:

“This policy, termed balance sheet “normalization” or “quantitative tightening” (QT), is designed to drain excess liquidity from the banking system. QT is the opposite of quantitative easing (QE).”

Today, after a healthy dose of QT, the Fed’s balance sheet is still far from normalized. It is over $5 trillion larger than in 2008 when Ben Bernanke promised that the initial round of QE was a temporary measure to stabilize the economy and markets.

Might today’s and many continued rounds of QT normalize the Fed’s balance sheet? We doubt it, and so does the Fed. In our latest article, Fiscal Dominance Is Here, we discuss the bind the Fed is in and how they must enact monetary policy with the massive Federal debt load in mind. Powell will never admit that monetary policy is beholden to the nation’s debt. However, the Fed does. The graphs below from the Fed project its SOMA account, which holds their bonds, will grow by 8-10% a year starting in 2025. The Fed and Treasury have no choice if deficits continue!

What To Watch Today

Earnings

Economy

Market Trading Update

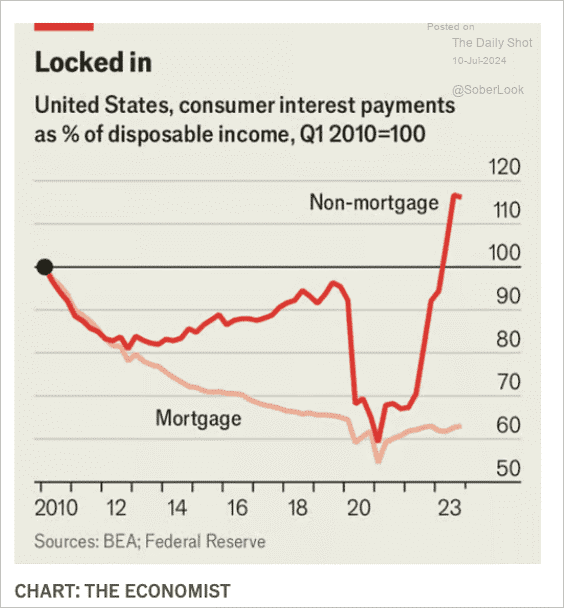

The market is poised to move higher again today if the CPI report confirms what the market is expecting – cooler inflation. With Jerome Powell heading into the FOMC meeting at the end of the month, the recent spat of weaker data has hopes mounting that the Fed could cut rates in July. That hope was recently underpinned by comments from Powell that he doesn’t want to wait too long to cut rates and risk undermining economic growth. That risk is clearly reflected in consumer interest payments (non-mortgage) as a percentage of disposable income, which has risen sharply. The longer high borrowing costs remain, the risk of a recessionary draw down increases.

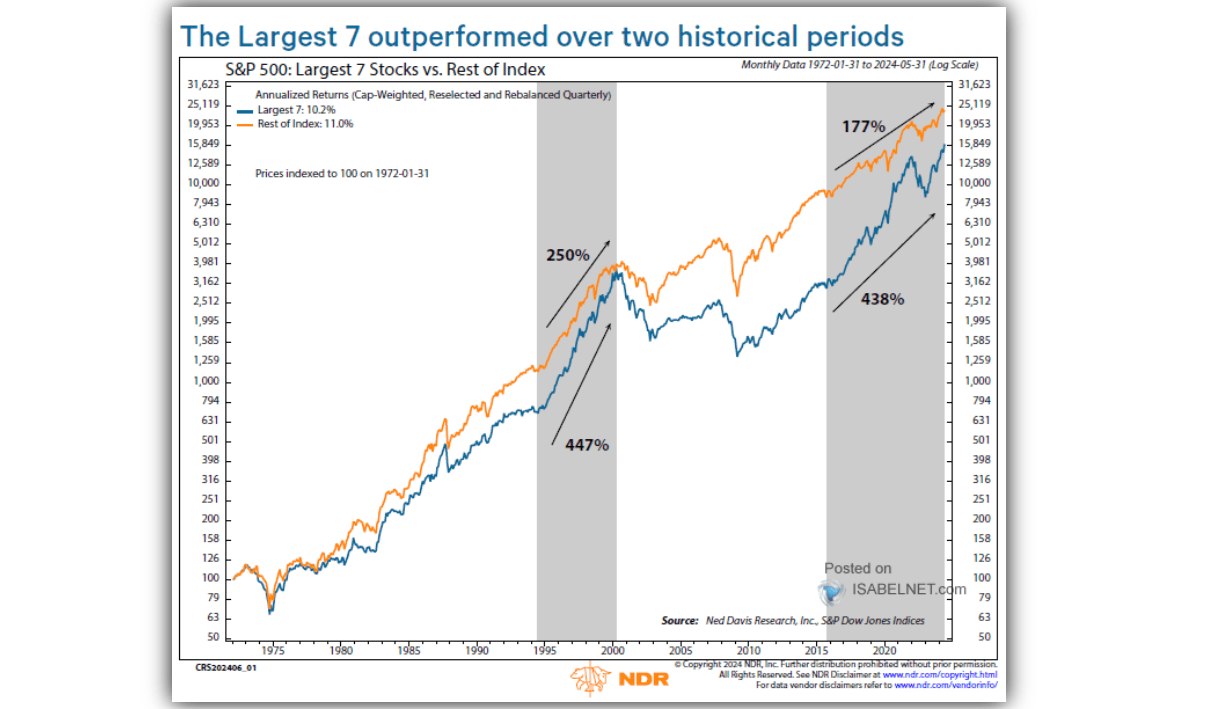

Do not dismiss that risk. When it comes to the financial market, investors are chasing a handful of stocks higher based on expectations of exponential earnings growth in the future. However, a recessionary onset will undermine those expectations as earnings fall and valuations reset. As shown, the last time that the largest 7-stocks outperformed the rest of the market to such a degree was heading into the “Dot.com” bubble. While this time is indeed different, it is unlikely that it is different enough to create infinite earnings growth.

While we remain long equities in our portfolio currently, as we will discuss in this weekend’s newsletter, we are starting to aggressively research multiple hedging strategies to reduce portfolio risk heading into the end of summer. Such a move certainly seems prudent.

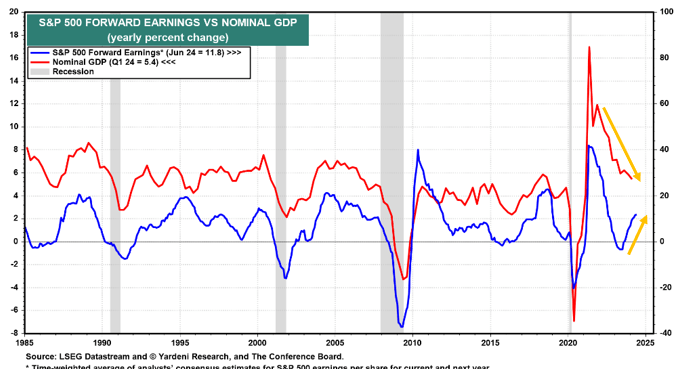

Forward Earnings Projections Appear Optimistic

Corporate earnings tend to be well correlated with economic activity. Also, as the graph below from Yardeni Research shows, forward earnings correlate well with current economic growth. Keep in mind that forward earnings are forecasts, not actual earnings. Recently, as Yardeni highlights with the yellow arrows, forward earnings expectations have been rising while the GDP growth rate has been declining. Therefore we must ask, can earnings expectations continue increasing if the economy slows beyond the natural growth rate? We doubt it, but never rule anything out in this market.

More On Construction Employment

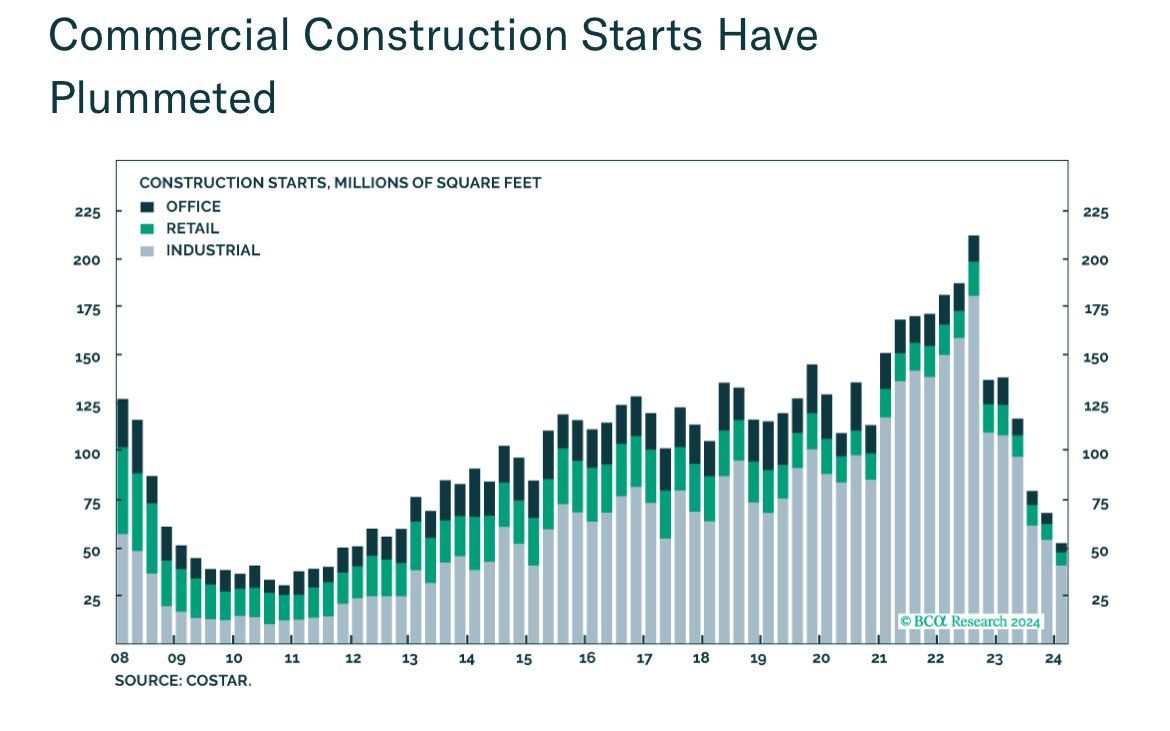

Yesterday’s Commentary touched on the significant jump in construction worker layoffs in the latest Challenger report. We track the sector closely because construction jobs have played a significant role in the robust job market. And as you know, the strong labor market is one reason the Fed is apprehensive about cutting interest rates.

The graph below, courtesy of CoStar, warns that the Challenger warning may not be a one-month anomaly. As measured in square footage, the amount of new commercial projects getting underway has plummeted from over 200 million square feet to just over 50 million. Such is the lowest since the aftermath of the financial crisis.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Chair Powell Testifies To Congress

Fed Chair Jerome Powell testified to Congress yesterday and updated them with the Fed’s latest views on the economy, inflation, and monetary policy. The Fed has kept rates at current levels in part because the labor market was tight. Chair Powell’s concern was that higher wages due to a shortage of workers would feed inflation. In his testimony, Chair Powell claimed that is no longer a concern. To wit:

The most recent labor market data sent a pretty clear signal that the labor market has cooled considerably and appears to be fully back in balance.

Regarding monetary policy, he said, “It’s not likely the next move will be a rate hike.” Further, he continued to stress the risks the Fed faces. Per his speech:

In light of the progress made both in lowering inflation and in cooling the labor market over the past two years, elevated inflation is not the only risk we face. Reducing policy restraint too late or too little could unduly weaken economic activity and employment.

On the inflation front, Chair Powell appears to be getting more optimistic that the recent inflation readings are heading lower again. “More good data would strengthen our confidence that inflation is moving sustainably toward 2%.”

He did not break new ground, but his general tone indicates the Fed wants to cut rates. However, they want more data confirming that the inflationary tailwinds are fading quickly. As shown below, the market favors a rate cut in September. The odds of a cut in July remain low at 5%.

Construction Job Layoffs Rising

The graph below, courtesy of Longview Economics, shows an unusual jump in the number of layoffs in the construction industry. Similarly, the recent data on building permits and housing starts have been slowing rapidly. Accordingly, layoffs in the industry should not be shocking.

There are approximately 8 million construction workers in the labor force. The sector has been one of the leading growth sectors over the last few years. Therefore, we should watch whether the layoffs continue in the Challenger data and if they also appear in the BLS data.

As Longview states:

Unusual to get such a large monthly ‘construction’ layoffs data point Way too soon to extrapolate. BUT a second similar month at this level would be troubling (especially when many other labour market indicators are so soft!)

Tobin’s Q Ratio At A Record High

The graph below, courtesy of ASR Ltd., shows that the Tobin Q ratio is now at its highest level in nearly 125 years. Tobin’s Q ratio uses the market value and replacement value of a company’s assets to determine if they are over or undervalued. When the ratio is greater than one, it means the market values the company more than the value of its assets. Therefore, today’s record readings imply expectations for high growth and, ultimately, profits.

Like Tobin’s, many valuation metrics are at or near historic highs. However, technically, the market remains very strong. Accordingly, investors need to pay close attention to technical warnings that could result in some normalization of valuations.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

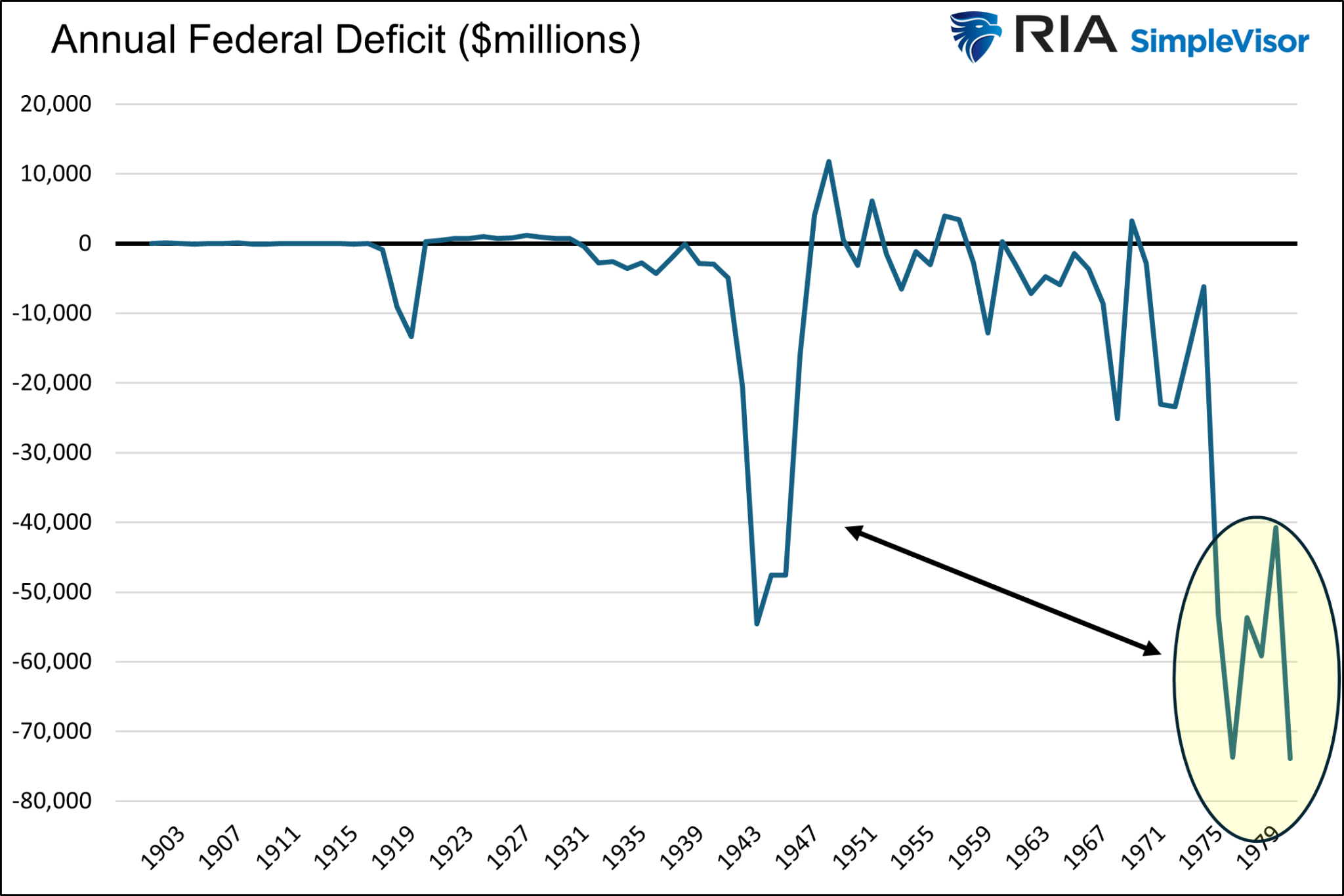

Fiscal Dominance Is Here

As quoted below from an executive summary of a joint report by the Department of Treasury and the Office of Management and Budget (OMB), the current deficit policy is deemed unsustainable. However, they fail to mention how long the Fed, via fiscal dominance, can sustain the unsustainable.

“The debt-to-GDP ratio was approximately 97 percent at the end of FY 2023. Under current policy and based on this report’s assumptions, it is projected to reach 531 percent by 2098. The projected continuous rise of the debt-to-GDP ratio indicates that current policy is unsustainable.” – Financial Report of the United States Government -February 2024.

Fed speakers will deny any notion that its monetary policy aims in part to help the government fund her debts. Regardless of what they say, we are already in an age of fiscal dominance. Monetary policy must consider the nation’s debt situation.

Fiscal Dominance

Fiscal dominance is a condition whereby the amount of debt in an economy reaches a point where monetary policy actions must allow Federal debts and deficits to be serviced and funded cost-effectively. By default, such monetary policy decisions will often come at the expense of traditional employment and price goals. As a result, the Fed must further distort the price of money and ultimately lessen the wealth of the nation’s citizens.

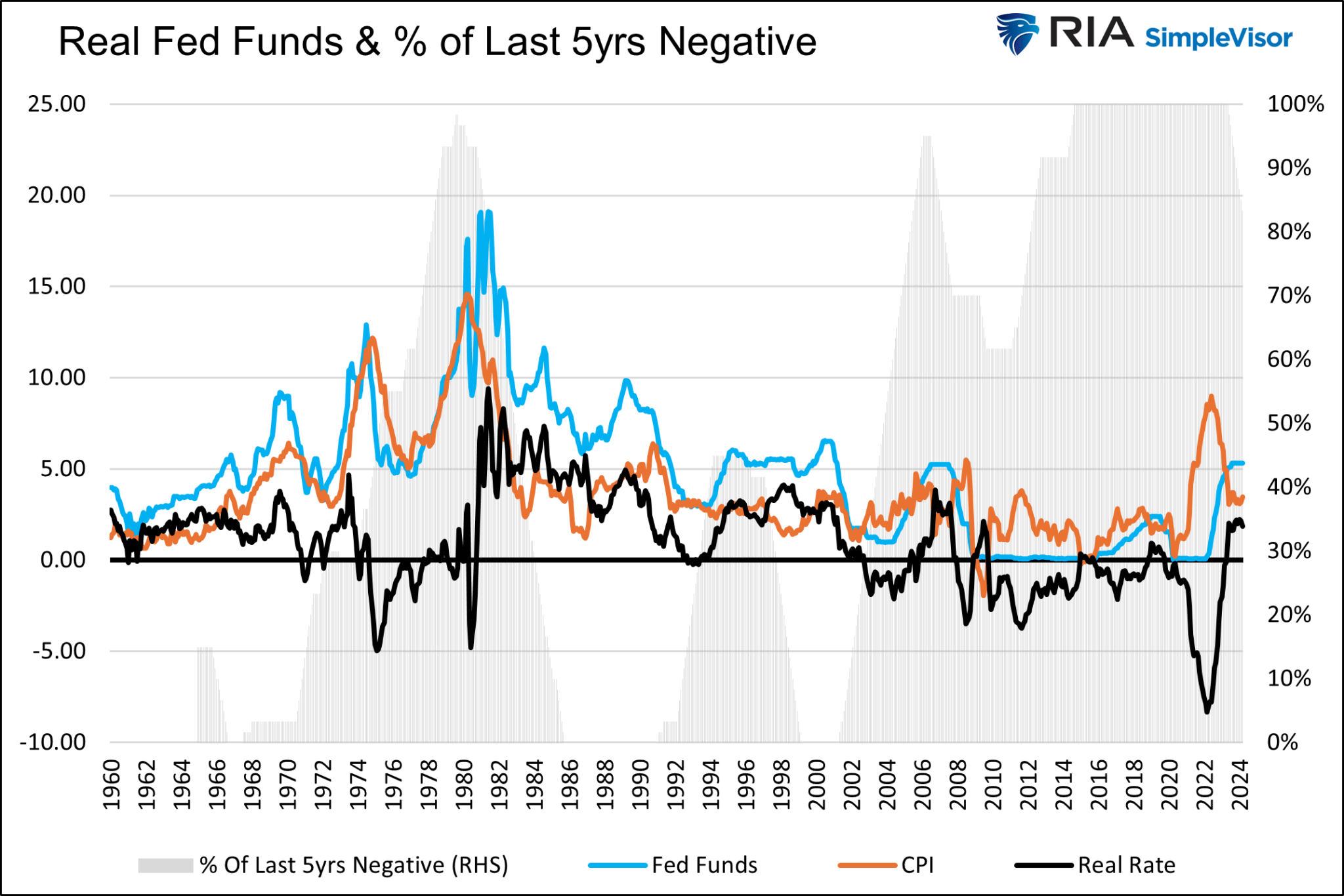

A lender or investor should never accept a yield below the inflation rate. If they do, the loan or investment will reduce their purchasing power.

Regardless of what should happen in an economics classroom, the Fed has forced a negative real rate regime upon lenders and investors for the better part of the last 20+ years. The graph below shows the real Fed Funds rate (black). This is Fed Funds less CPI. The gray area shows the percentage of time over running five-year periods that real Fed Funds were negative. Negative real Fed Funds have become the rule, not the exception.

Soaring Debt Outstanding and Rising Rates

The government has added $2.5 trillion in debt over the last four quarters. Of that, over $1 trillion was to pay its interest expenses on the entire debt stock. Despite recent high interest rates, the average interest rate on the debt is still relatively low at 3.06%.

The two graphs below show why a relatively minimal uptick in the average interest rate on the debt is so troublesome. The federal debt (blue) has grown by 8.5% annually over the last ten years. Despite the amount of debt more than doubling over the period, the interest expense on the debt until very recently has remained very low. The first graph shows that the average interest rate increase is barely visible. However, the second graph shows that the rise in the government’s interest expenses is substantial.

As debt issued years ago with low interest rates matures and new debt with higher interest rates replaces it, the interest expense will keep rising. For context, if we assume the government’s average interest rate is 4.75%, likely close to their weighted average rate on recent debt issuance, the interest expense will rise to $1.65 trillion, not including new debt.

$1.65 trillion is over $300 billion above the government’s next largest expenditure, Social Security. Furthermore, it is double defense spending for 2023. The annual federal deficit has only been above $1.65 trillion twice (2020 and 2021) since its founding in 1776.

While the situation may sound gloomy, lower interest rates solve the problem. If interest rates return to the levels existing before 2022, the interest expense could easily fall below $700 billion, about half of the cost than if rates remain at current levels.

Therefore, interest rates will have to be kept in check by the Fed.

The Fed Understands Their Role

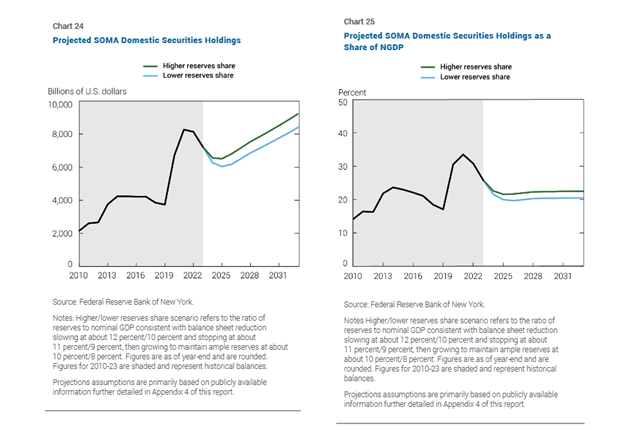

In 2008, Ben Bernanke said QE was a temporary measure that would be reversed once the economy and markets returned to normal. Trillions worth of Treasury purchases later, and the Fed now tells us it’s permanent. Consider the following graph and paragraph by the New York Fed.

“Under the two purely illustrative scenarios, the size of the SOMA portfolio continues to decline to $6.5 trillion and $6.0 trillion, respectively. The portfolio size then remains steady for roughly one year before increasing to keep pace with growth of demand for Federal Reserve liabilities, reaching $9.2 trillion and $8.4 trillion, respectively, by the end of the forecast horizon in 2033.”

The SOMA portfolio is the Fed’s System Open Market Account Holdings. This is the portfolio that holds bonds purchased via QE as well as its other monetary operations.

The graph on the left shows that the Fed expects the SOMA account to rise by about 40% starting in later 2024 through 2032. More importantly, the graph on the right shows that its increase will be commensurate with GDP. In other words, the Fed will continue to help fund the deficit by buying Treasury debt.

Monetary Policy

We know how QE and lower interest rates cut interest expenses, allowing the government to spend recklessly. However, there are other ways the Fed can supplement their efforts if needed. For instance, in our daily Market Commentary from April 24th, we shared the following:

If enacted, the new bank rules would force all banks to “preposition billions more in collateral” at the Fed to support future discount window borrowing. The article estimates that the Fed would require collateral matching up to 40% of a bank’s uninsured deposits, accounting for about 45% of the $17.5 trillion commercial bank deposits. Further, the new rules would require the banks to borrow from the window numerous times a year to help remove the program’s stigma.

In addition to bolstering the banking safety net, it would also force banks to hold significant collateral balances at the Fed. Collateral for Fed loans is quite often U.S. Treasury securities. Accordingly, this new bank rule is another way to help the Treasury fund its massive deficits and stock of outstanding debt from years past.

Rumor has it that the regulators could eliminate leverage requirements for the GSIBs. Doing so would infinitely expand their capacity to own Treasury securities. That may sound like a perfect solution, but there are two problems: the banks must be able to fund the Treasury assets and avoid losing money on them.

The bank bailout BTFP enacted in March 2023 addresses the problems. As we wrote:

In a new scheme, bank regulators could eliminate the need for GSIBs to hold capital against Treasury securities while the Fed reenacts some version of BTFP. Under such a regime, the banks could buy Treasury notes and fund them via the BTFP. If the borrowing rate is less than the bond yield, they make money and, therefore, should be very willing to participate, as there is potentially no downside.

Summary

With the Fed willingly helping the government fund her debts, we believe the odds are small that any significant deficit reduction is possible. While the path is unsustainable, it is likely much longer than most pundits appreciate.

However, fiscal dominance comes with a significant cost. The Fed fuels the widening wealth gap by manipulating interest rates and indirectly influencing the stock market. As we have seen glimpses over the last five years, social unrest will likely become more prevalent. With that comes poor economic confidence from consumers and businesses, which in turn generates a headwind to the economy.

It’s not too late to try and fix our fiscal problems, but time is ticking. As the saying goes, Rule #1 of holes: when you are in one, the first thing to do is stop digging.

The Market Is Very Extended But It Can Stay That Way

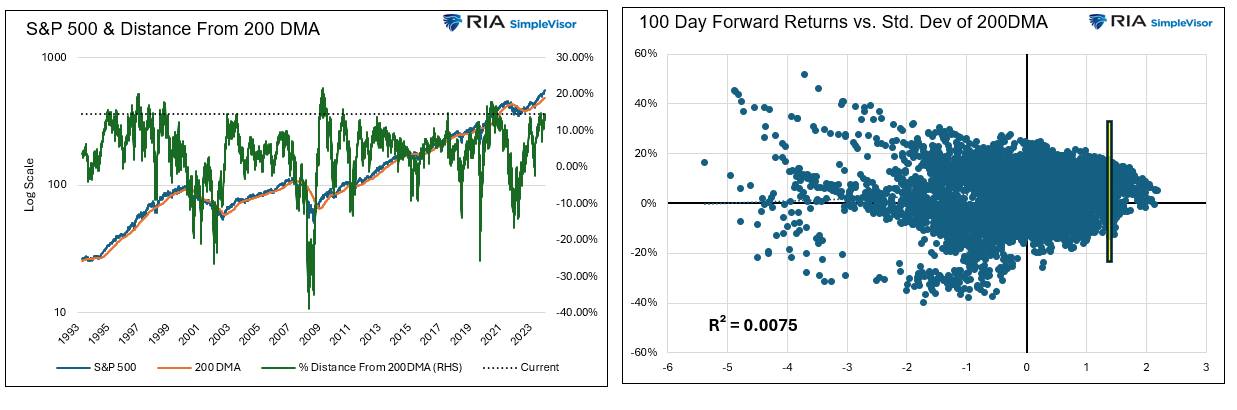

A reader asked us how concerned we are about the market’s extension from crucial moving averages. The short answer is we are. But that doesn’t mean we are moving our equity holdings to cash. We continue to hold our equity positions for two reasons but we remain vigilant.

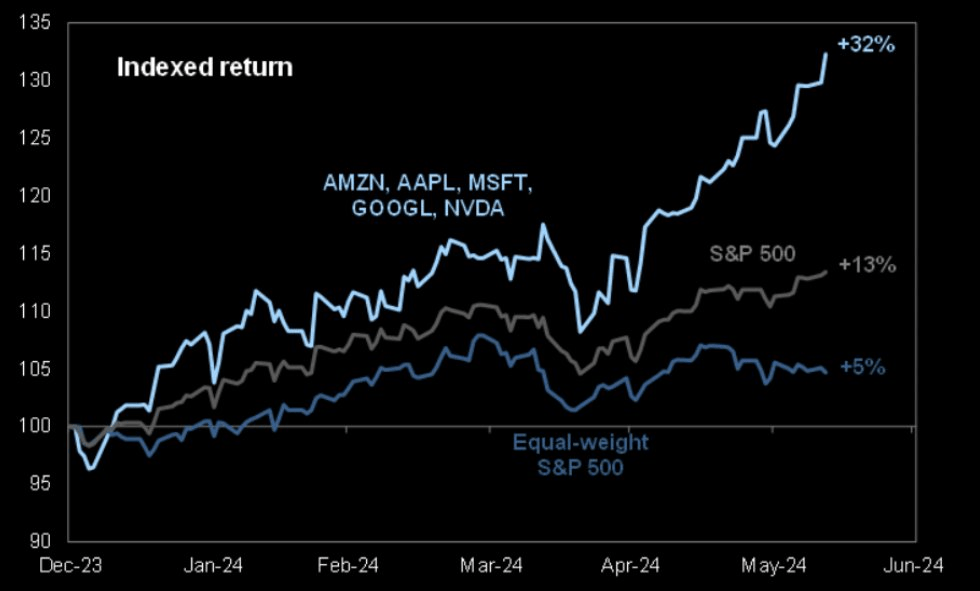

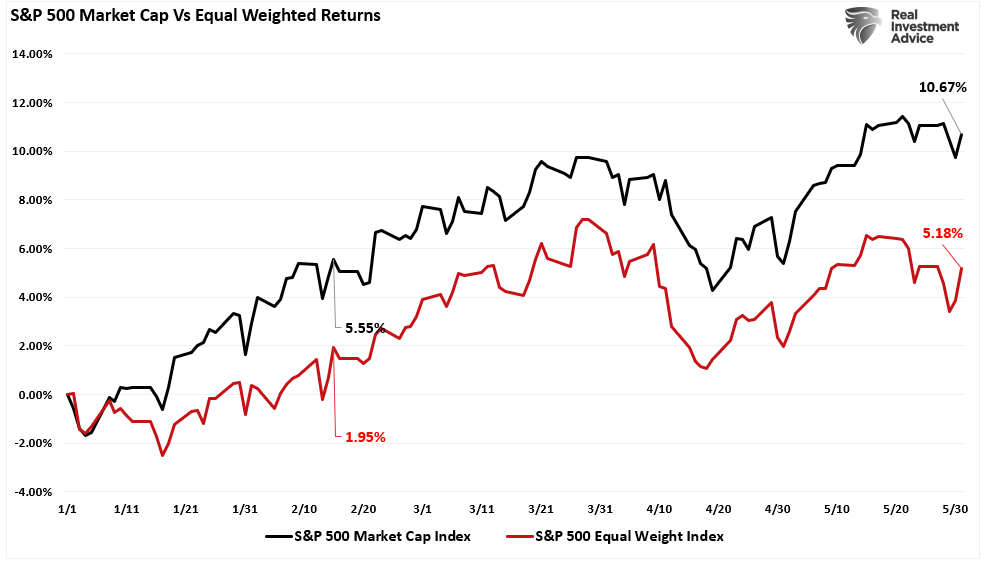

First, the S&P 500 is doing great, but only because of a small handful of the largest-cap stocks. This imbalance is getting extreme. However, the condition doesn’t require a sharp downturn to correct itself. Simply, the other 480 or so stocks that have been underperforming can outperform without the market declining.

Secondly, similar historical deviations from important moving averages offer no conclusive evidence of an imminent downturn. The graph on the left shows the S&P 500 and its 200dma. The green line is the percentage market deviation from the 200dma. As the dotted line shows, the current instance is somewhat extreme but can remain so for a while. The scatter plot on the right compares the standard deviation of the market divergence from the 200 DMA with forward 100-day returns. The yellow bar is where the market currently is. Again, based on prior instances, an impending downturn is not a foregone conclusion. Furthermore, the R2 shows there is no correlation between the two factors.

The bottom line: watch for technical signs the market is breaking down but appreciate this current condition can continue.

What To Watch Today

Earnings

Economy

Market Trading Update

FOMC Minutes

Last Wednesday, after the market closed early for the July 4th holiday, the Fed released its minutes from the mid-June meeting. The minutes were generally dovish. In particular, the Fed seems to be getting more comfortable with continued disinflation. Per the minutes:

“Participants highlighted a variety of factors that were likely to help contribute to continued disinflation in the period ahead. The factors included continued easing of demand–supply pressures in product and labor markets, lagged effects on wages and prices of past monetary policy tightening, the delayed response of measured shelter prices to rental market developments, or the prospect of additional supply-side improvements. The latter prospect included the possibility of a boost to productivity associated with businesses’ deployment of artificial intelligence–related technology.”

Nevertheless, participants suggested that a number of developments in the product and labor markets supported their judgment that price pressures were diminishing. In particular, a few participants emphasized that nominal wage growth, though still above rates consistent with price stability, had declined, notably in labor-intensive sectors. A few participants also noted reports that various retailers had cut prices and offered discounts. Participants further indicated that business contacts reported that their pricing power had declined. Participants suggested that evidence of firms’ reduced pricing power reflected increased customer resistance to price increases, slower growth in economic activity, and a reassessment by businesses of prospective economic conditions.

Their disinflationary views are supported by their opinions on the labor market, which they believe has primarily normalized.

Several participants also suggested that the establishment survey may have overstated actual job gains. Several participants remarked that a variety of indicators, including wage gains for job switchers, suggested that nominal wage growth was slowing, consistent with easing labor market pressures. A number of participants noted that, although the labor market remained strong, the ratio of vacancies to unemployment had returned to pre-pandemic levels and there was some risk that further cooling in labor market conditions could be associated with an increased pace of layoffs. Some participants observed that, with the risks to the Committee’s dual-mandate goals having now come into better balance, labor market conditions would need careful monitoring.

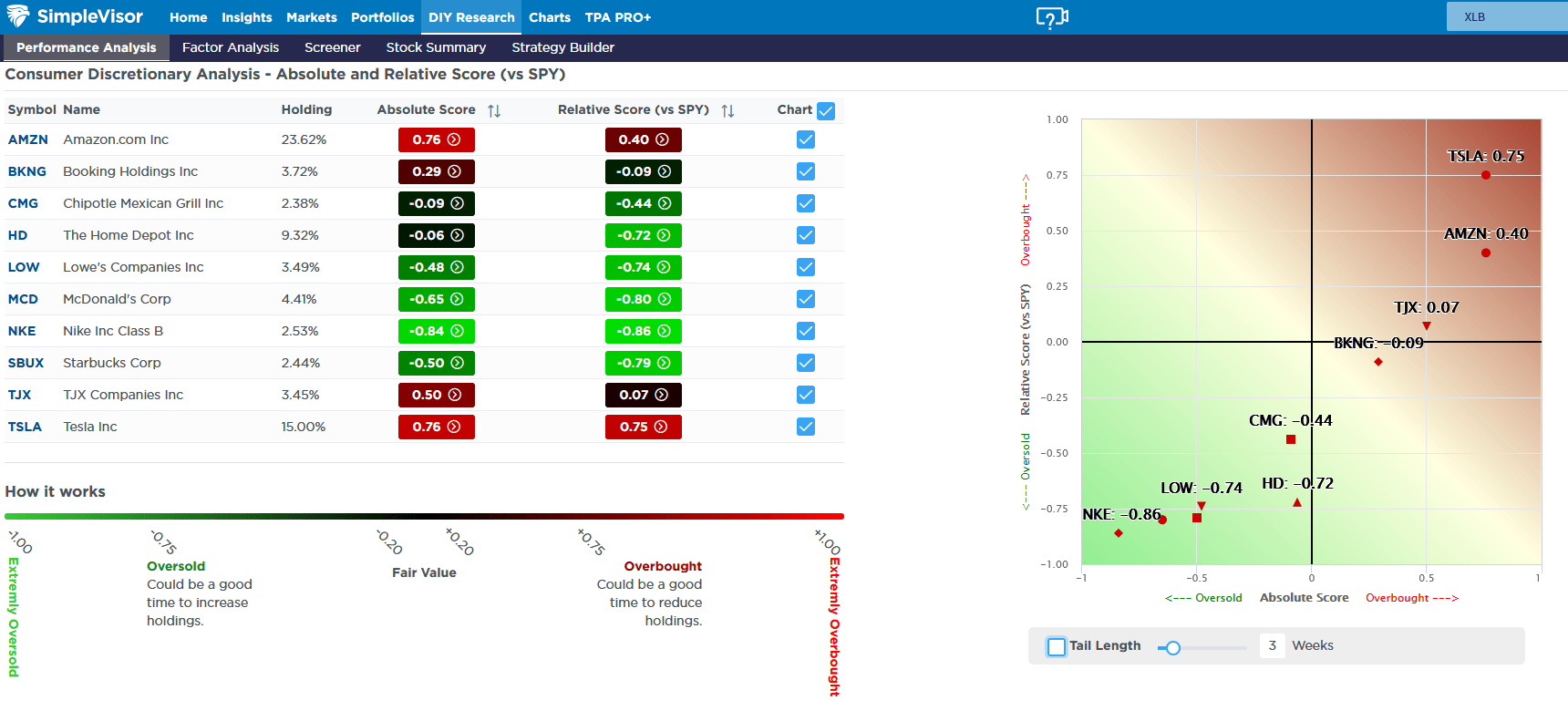

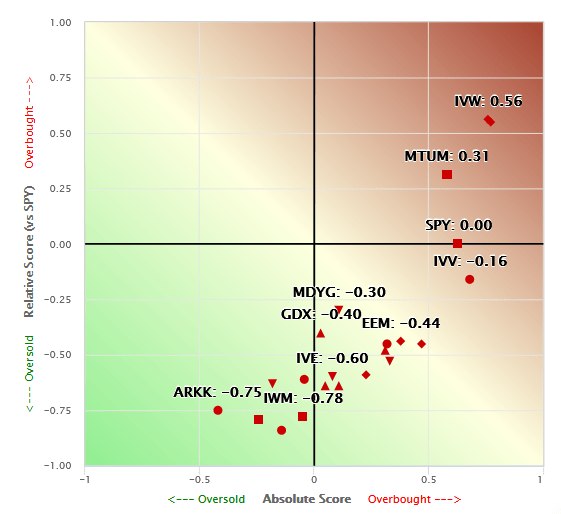

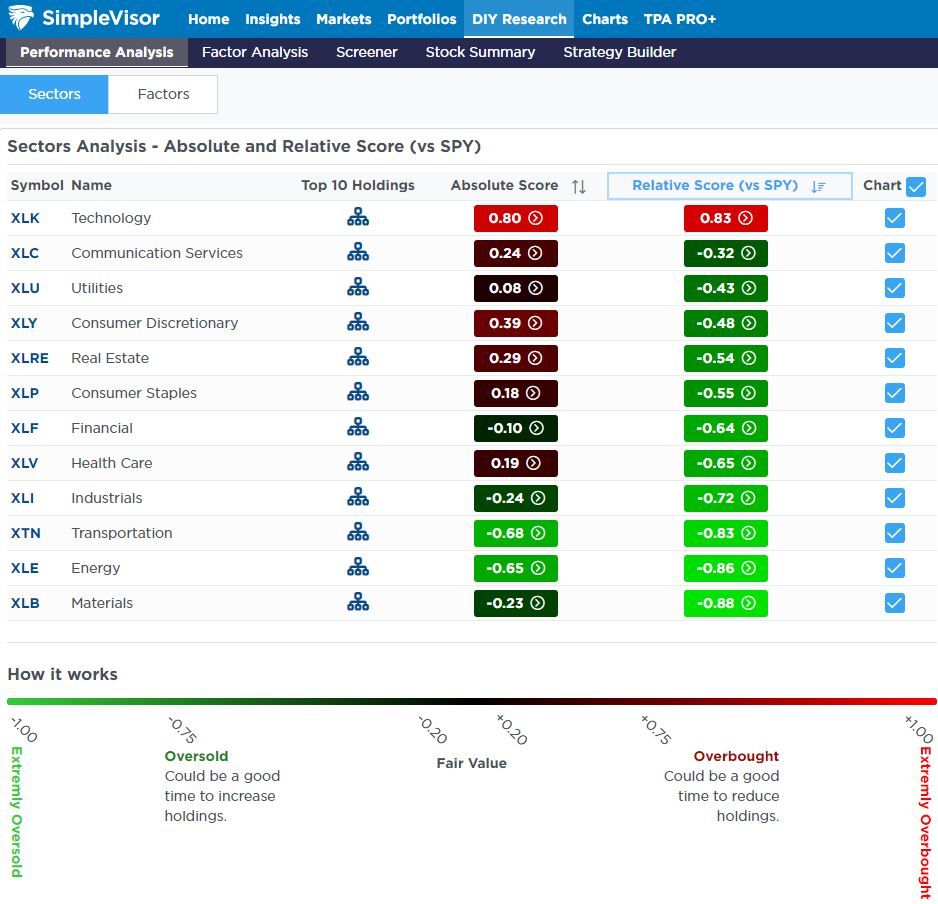

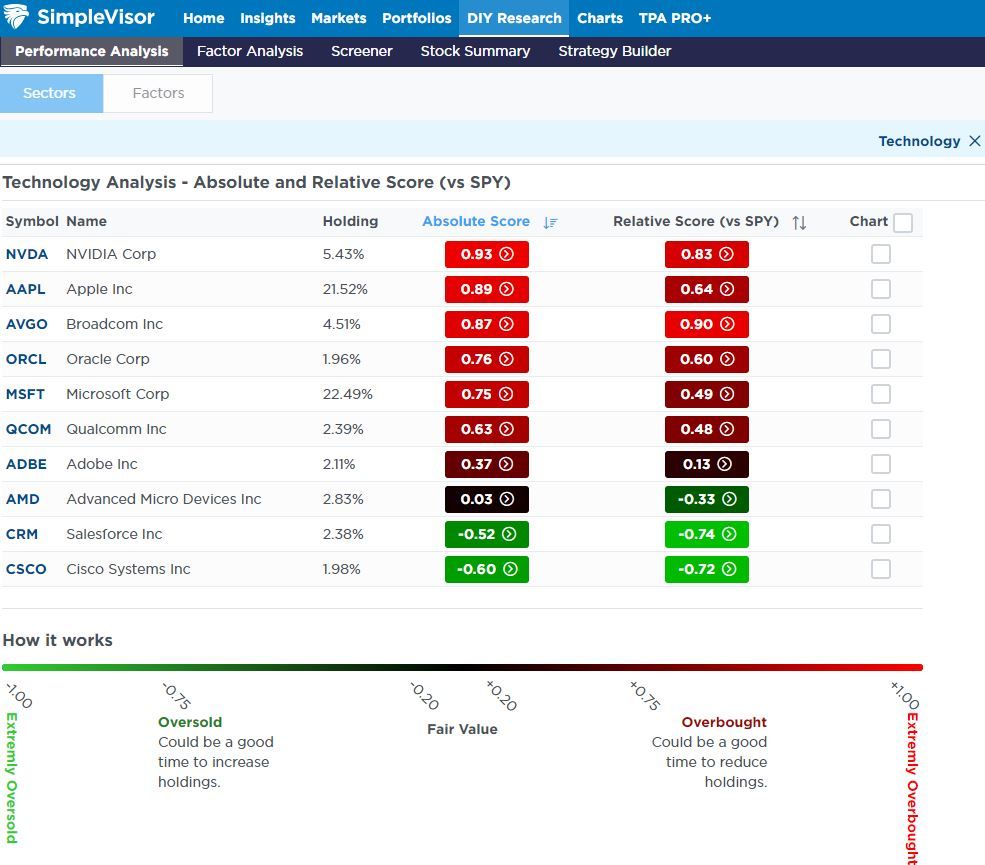

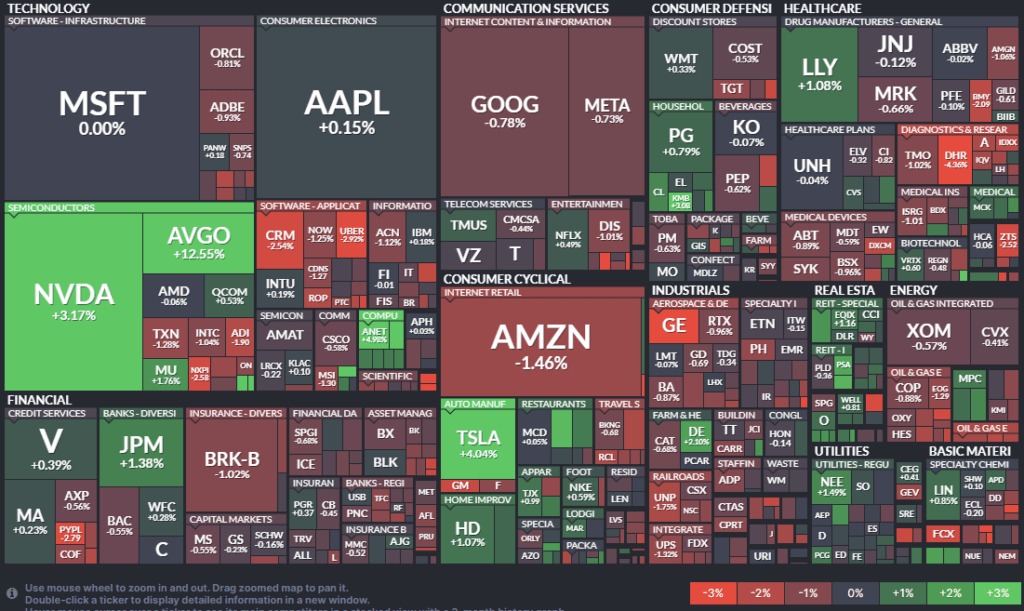

Tesla Powers Consumer Discretionary Stocks

Last week, Tesla was up over 25%, leading the market higher and contributing to the gross outperformance of the consumer discretionary sector (XLY). Tesla accounts for roughly 2% of the S&P 500. Thus, last week’s gain contributed to over a third of the market’s 1.4% increase. Tesla also contributes about 30% to XLY. XLY was up about 3% last week. Tesla added over 6%; therefore, the sector would have been down by approximately 3% without Tesla.

Tesla and Amazon are overbought compared to the market, while most consumer discretionary stocks are grossly oversold (bright green). The first graphic below, courtesy of SimpleVisor, shows that most discretionary stocks are grossly oversold. This is another example of the extreme performance bifurcation we are witnessing. The five-day heat map also shows the massive performance divergence. Note how many of the largest stocks by market cap had great five-day performances. However, the large majority of stocks were lower on the week.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Private Equity – Why Am I So Lucky?

Lately, I have been getting many questions about investing in private equity. Such is common during raging bull markets, as individuals seek higher rates of return than the market generates. Also, during these periods, Wall Street tends to bring new companies to market to fill the demand of the investing public. Private equity is always alluring, as is the tale of someone who bought the company’s shares when it was private and made a massive fortune when it went public.

Who wouldn’t want a piece of that?

The private equity (PE) business is huge. When I say huge, I mean $4.4 Trillion huge.

Those PE companies have been extremely busy over the last several years. While there has been a surge in private equity startups, there has also been the privatizing of public companies. The Atlantic shared some data about the dwindling number of publicly traded stocks along with the corresponding growth in private equity investments:

The publicly traded company is disappearing. In 1996, about 8,000 firms were listed in the U.S. stock market. Since then, the national economy has grown by nearly $20 trillion. The population has increased by 70 million people. And yet, today, the number of American public companies stands at fewer than 4,000. How can that be?

One answer is that the private-equity industry is devouring them.

In 2000, private-equity firms managed about 4 percent of total U.S. corporate equity. By 2021, that number was closer to 20 percent. In other words, private equity has been growing nearly five times faster than the U.S. economy as a whole.

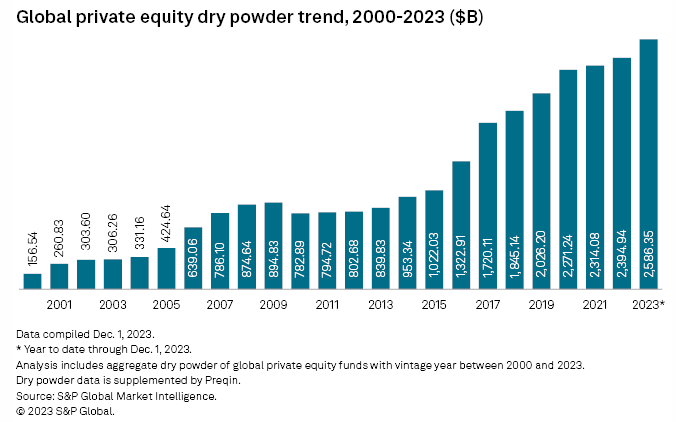

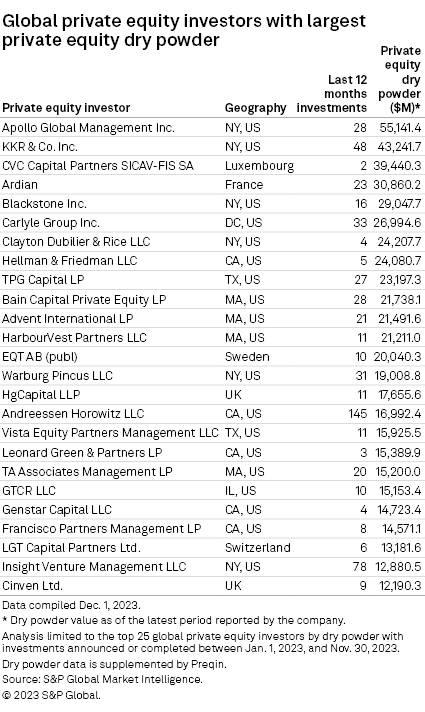

PE firms managed less than $1 billion in the mid-1970s. Today, it’s more than $4 trillion. There is more than $2.5 trillion in dry powder alone globally:

However, that “dry powder” is problematic for PE companies as they must invest it or return it to the investors. Therefore, the demand for deals often means that the deals getting funding may not be the “best” deals.

That is a substantial risk we will discuss in more detail momentarily.

Is Private Equity Right For You?

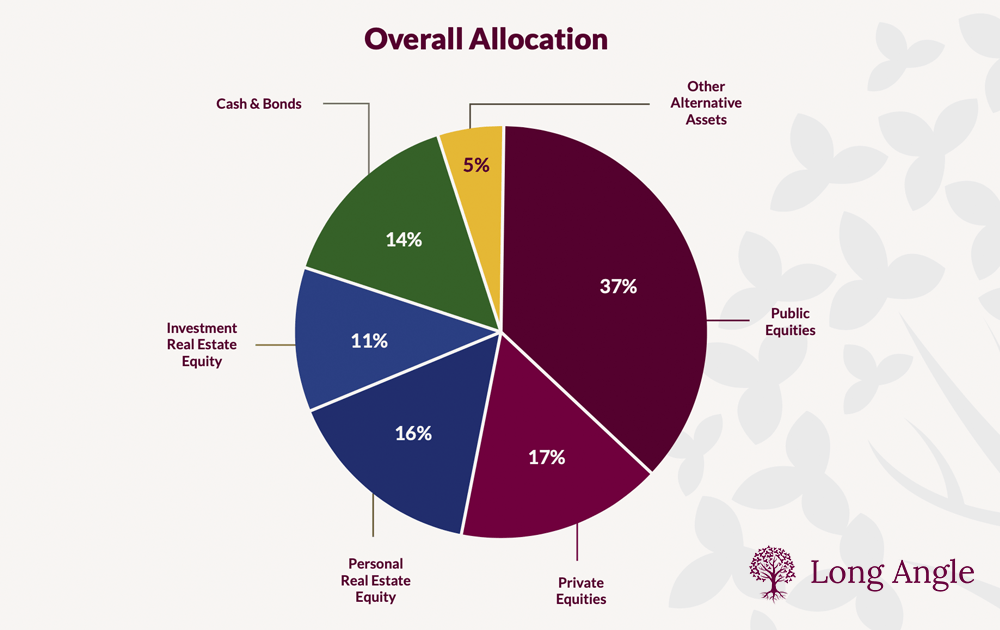

Many individuals hear tales of how high-net-worth individuals (the smart money) own private equity in their allocations. As shown in the chart below from Long Angle, roughly 17% of their allocations are to private equities. These reports don’t generally tell you that their allocation to “private equity” often tends to be their personal businesses. Nonetheless, individual investors frequently see this type of analysis and think they should be replicating that process. But should they?

There are significant differences to consider between the vast majority of retail investors and high-net-worth individuals before investing in private equity. The underlying risks of private equity investments can define these differences. There are many risks, but I want to focus on three.

Liquidity Risk

Duration

Loss Absorption

Liquidity Risk: Many individuals don’t realize when entering into private equity investments that they cannot liquidate them if capital is needed for another reason. While investors often enter into private equity with the anticipation of making outsized returns, they frequently leave themselves vulnerable to the impact of having capital tied up in an illiquid investment. When the eventual crisis happens, the illiquid status of private equity becomes problematic.

Duration Risk: The duration of private equity can often be much longer duration than initially estimated. When a private equity deal is pitched to an individual, it is always accompanied by the most optimistic projections. The projections always include optimistic exit assumptions where the individual will receive an enormous windfall. More often than not, the projections fall very short of reality. A market downturn, economic recession, or a change in underlying industries, interest rates, or inflation can turn an initial 3-year investment into a decade or more. That duration risk multiplies the liquidity risk of keeping capital tied up for much longer than anticipated, sometimes with little or no return. While high-net-worth individuals can absorb both the duration and liquidity issues, most individual investors can not.

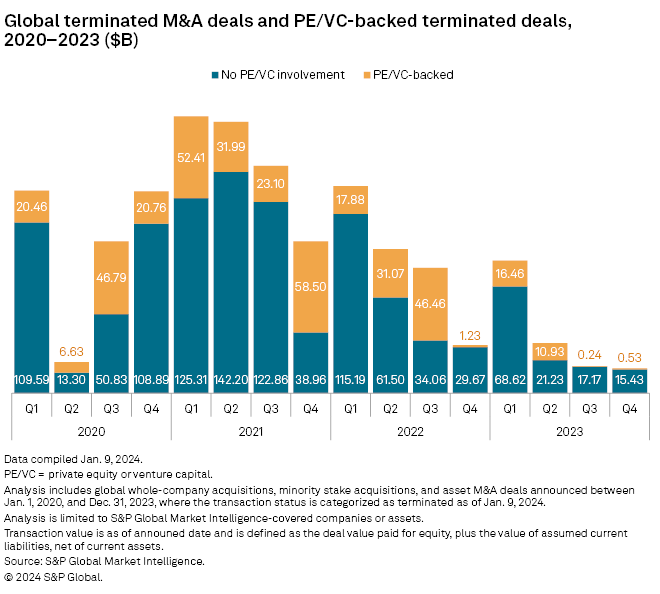

Loss Risk: Lastly, high-net-worth individuals can absorb losses. Many private equity deals inevitably fail, leaving investors with enormous losses on their balance sheets. While high-net-worth investors can invest in numerous deals, the hope is that a successful private equity venture will offset the losses of one or more that failed. Individuals often do not have the capital for that kind of diversification, and a loss on a private equity investment can be very detrimental. The chart below from S&P Global shows the number of private transactions terminated between 2020-2023.

To that point, you should realize that most private equity investments (65%) either fail or return the initial investment at best.

Yes, private equity can be very lucrative. Depending on the deal you invest in, it can also be very harmful. This brings us to the most important question to ask: “Why am I so lucky?”

Why Am I So Lucky?

If you are approached by someone pitching a “private investment,” the first question you should ask is, “Why am I so lucky to be given this opportunity?”

As noted above, the global PE dry powder has soared to an unprecedented $2.59 trillion in 2023 as a slow year in dealmaking closes with limited opportunities for firms to deploy capital raised in previous years. The dry powder total as of Dec. 1st represented close to an 8% increase over December 2022, according to S&P Global Market Intelligence and Preqin data.

That capital is held by some of the largest PE companies in the world. The list below is just a view of the names that you will likely recognize.

Importantly, as noted, these firms must deploy that “dry powder,” or they will eventually lose it. As such, they have armies of employees to scout for the best opportunities, analysts, legal and accounting professionals to analyze those deals, and immediate capital to fund them.

Therefore, as an individual, several questions need to be thoroughly answered.

If this private equity investment is such a good opportunity, then:

Why did the company not approach one of the major P/E firms with capital ready to invest?

If they did and were turned down, why?

How many private equity investors did the company approach before you contacted me?

What is the track record of this salesman’s previous investments in private equity, if any?

Can you analyze the many investment risks associated with illiquid investments?

Yes, some private equity transactions are too small for a major private equity company like Black Rock, which must invest billions at once. However, many mid-tier private equity companies will take those types of deals.

Most importantly, for you to “exit” the investment and realize the windfall, does the person selling you the investment have the network of investment banks, market makers, and institutions to provide that exit? Finding a future buyer or taking a company from private to public can be exceedingly difficult without that network.

These are just some things to consider before committing your hard-earned capital to a risky, highly illiquid investment.

Does this mean that you should never make a private equity investment? Of course not. However, you must understand the risk of investing and the potential ramifications on your financial situation when something goes wrong.

So, “Why am I so lucky?”

July 31 Is Back On The Markets Calendar With Fridays Jobs Report

A year ago, the Fed Funds futures market thought the Fed would have cut rates two to three times before the July 31, 2024 FOMC meeting. Two weeks ago, the odds of a rate cut at the July 31 meeting were near zero. Furthermore, the market was only pricing in one cut for the remainder of the year. With Friday’s jobs report, a fragile ISM report detailed below, and renewed signs that the disinflation trend may be resuming, the prospect of a July 31 rate cut back into focus.

On Friday, the BLS reported the economy gained 206k jobs. The growth was slightly better than expected; however, the unemployment rate rose from 4.0% to 4.1%. Further, the April and May jobs figures were revised lower by 111k in aggregate. Like the prior few employment reports, this report was good from a headline perspective, but a look beneath the hood is troubling.

So, with the unemployment rate ticking up, might the Fed cut rates as soon as July if this week’s inflation data is weak? While the odds remain low, we will watch Jerome Powell’s speeches on Tuesday and Wednesday for clues. This weekend’s Newsletter discusses why the thought of a Fed cut in July is not unthinkable. Per the article, “We don’t think so, but the data is becoming more supportive of action. However, if the Fed cuts rates in July, it is likely a good signal that we will need to become less aggressive on equity allocations.“

What To Watch Today

Earnings

There are no significant reports today.

Economy

There are no significant reports today.

Market Trading Update

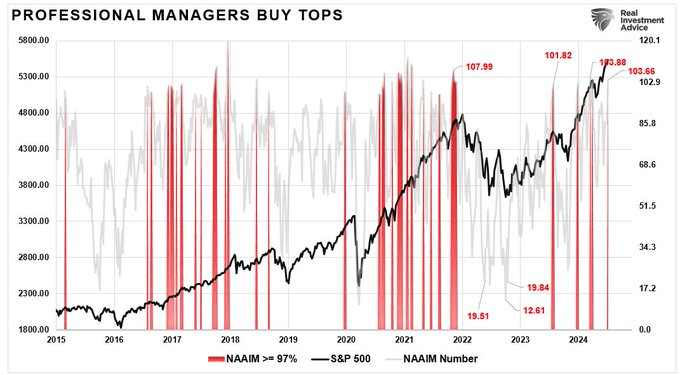

The market continues in a very bullish trend, with investors increasingly confident that they will receive higher returns. That infectious greed has also spilled over onto professionals, with their equity exposure exceeding 100%. While such is a warning sign, it does not necessarily mean the markets will have a deep correction. However, such positioning extremes have previously marked short-term tops and consolidations.

Furthermore, the market’s deviation from the underlying 200-DMA is also starting to reach levels that have previously preceded short-term market corrections or consolidations. As is always the case, for an “average” to exist, the market must trade above and below that average over time. Therefore, the more extreme the deviation from that average, the stronger the pull for a reversion.

These are warning signs that the market needs a short-term correction or consolidation to alleviate those conditions. Such a process would be healthy for a continued bullish advance. However, it doesn’t mean it will happen today or this month. As is always the case, timing is the critical part.

Trade accordingly.

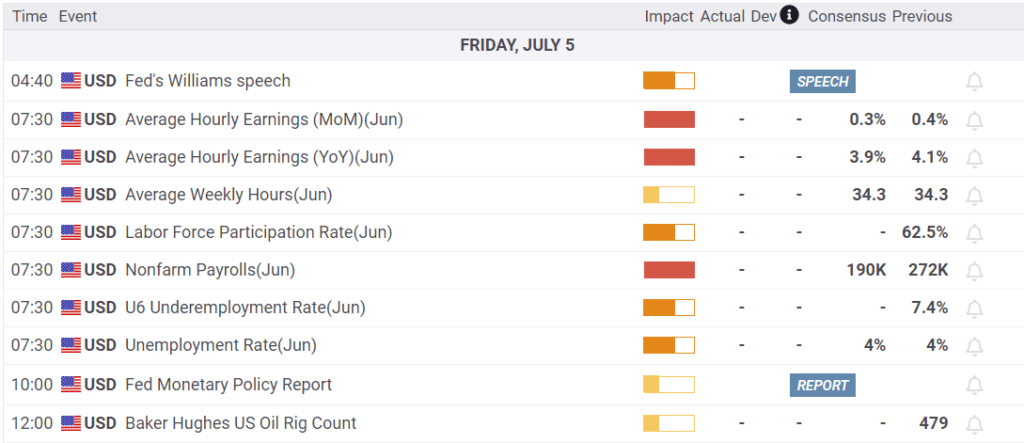

The Week Ahead

This week will be highlighted by CPI on Thursday, PPI on Friday, two Jerome Powell appearances, and the start of earnings reporting season.

If the Fed is going to cut rates on July 31, it will likely require a lower-than-expected CPI number. The market expects CPI to rise by 0.1% and Core CPI by 0.2%. After declining by 0.2% last month, PPI is expected to increase by 0.2%. Jerome Powell speaks on Tuesday and Wednesday. He will likely have the inflation reports before the speeches.

Earnings season kicks off this week, with the large banks reporting earnings on Friday. The following week, a broader array of company earnings reports will be released.

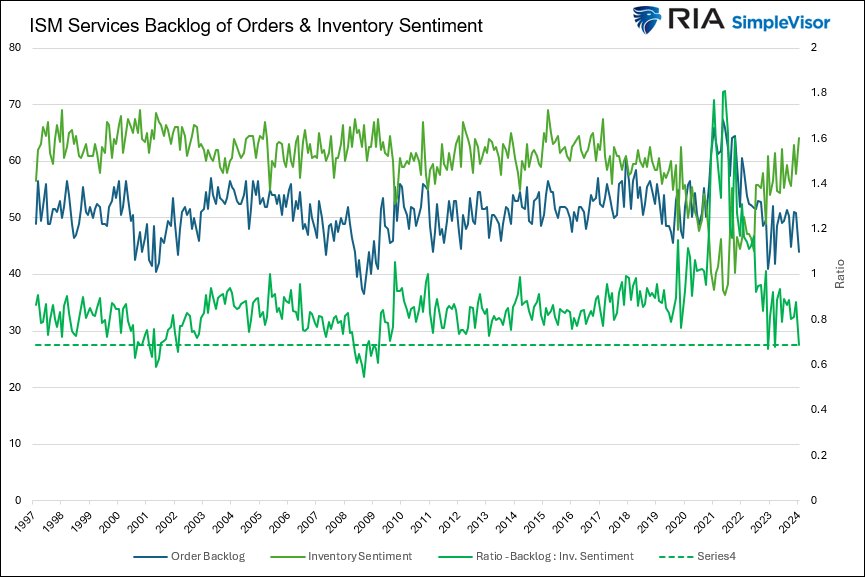

ISM Services Was Much Weaker Than Expected

For the first time since 2009, excluding April and May of 2020, the ISM services index (blue- -lower graph) is in economic contraction territory. Wednesday’s reading of 48.8 was well below estimates of 52.7 and the prior reading of 53.8. Within the index, the prices paid index was weaker than expectations although still above 50, pointing to higher prices. That said, the manufacturing and services ISM are seeing their price indexes resume lower trends. Of the most concern is the employment index. It came in at 46.1, well below the estimate of 49.5. Such further affirms that the BLS headline job growth figures may be overstating the actual state of the labor markets. This is not lost on the Fed as they have acknowledged such.

New orders, a good leading indicator of activity, were also well below expectations at 47.3 versus an expected 53.6. The first graph below shows a robust leading economic indicator for the service sector. The ratio of order backlogs to inventory sentiment is in recessionary territory. Furthermore, within the report is the following quote:

The percentage of ISM Services respondents expecting higher new orders is at its lowest since the GFC and lower than ’01 recession

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

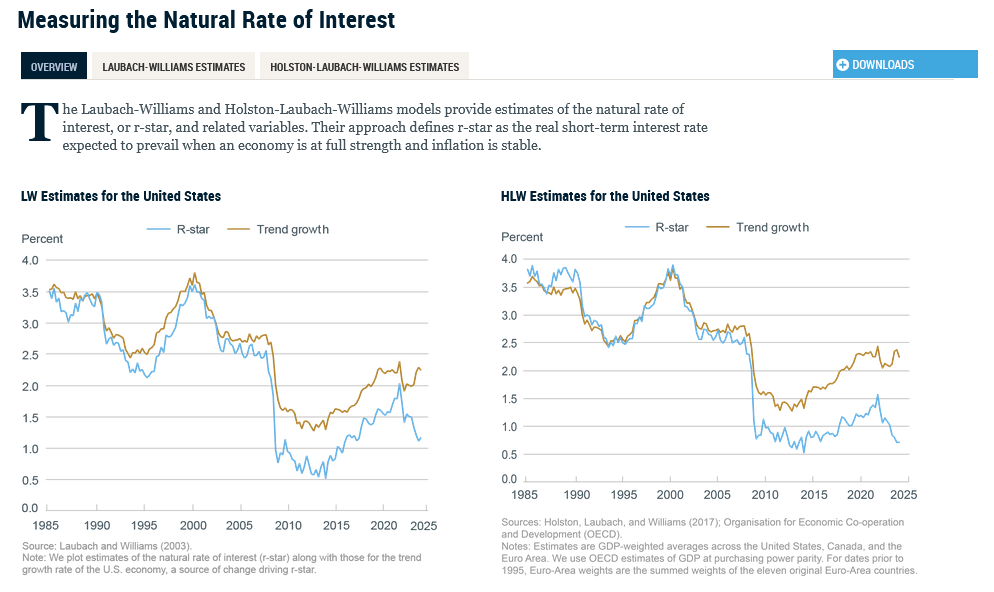

R Star: A Culprit Behind Higher Interest Rates

As we shared on Monday, The Fed Funds Rate Is Too High. The biggest reason is the Fed fears another round of inflation. Therefore, they try to ensure it doesn’t happen via tight money policy. Second, federal deficits have been larger than average, causing a jump in Treasury debt issuance. This is primarily the function of an extra $500 billion a year in interest expenses due to higher interest rates. However, significant deficit spending certainly does not help the cause. Lastly, there is R Star, an explanation many may not have heard of.

R Star is the real neutral rate of interest that balances the economy. Unfortunately, there is no way to calculate an economy’s R Star. Hence, managing interest rates to the figure is a guessing game for the Fed. Some economists and bond investors believe the R Star has increased over the past four years due to the pandemic. Therefore, bond yields should be higher if the natural economic growth rate is higher.

On Wednesday, New York Fed President Williams debunks the idea of a higher R Star. He states:

“Although the value of R Star is always highly uncertain, the case for a sizable increase in R-Star has yet to meet two important tests.”

The first is the “interconnectedness” of R Star across countries. There is no evidence that it is rising in Europe or other developed nations. Actually, it is likely declining in Europe, the UK, and China. “Second, any increase in R Star must overcome the forces that have been pushing R Star down for decades.” Have productivity and demographic trends suddenly changed for the better? Again, there is no evidence this is occurring. The two Fed economic models below show that R Star remains on the same trend for the last 40 years.

What To Watch Today

Earnings

No notable earnings reports

Economy

Market Trading Update

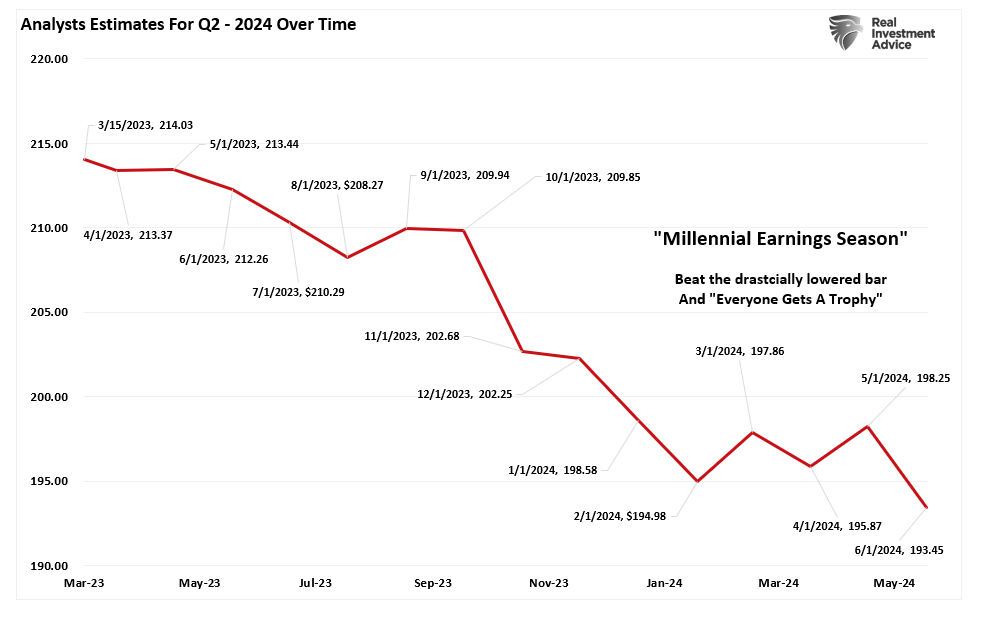

Last week, we noted that we were about to enter Q2 earnings season.

“Speaking of earnings, analysts have been extremely busy over the last 30 days, slashing estimates. In June, Q2 earnings estimates for the S&P 500 index were cut by $5/share to the lowest level yet. Interestingly, while Wall Street continues to boast confidence in rising asset prices, they have cut estimates from $214/share in March last year to just $193/share. Such suggests a dichotomy between expected market performance and the economy, which is where earnings come from.”

As noted, I am using Wednesday’s closing data for the current analysis before I head out for vacation. First, while markets hit an all-time high, I wouldn’t read much into it. Trading volume was light due to the shortening of the week for the Independence Day holiday week. Secondly, while the market did make a new high, it remains a marginal new high tracking along the 20-DMA, which continues to act as bullish support.

The market remains overbought short-term, but the recent rally is close to flipping the short-term MACD “sell signal.” Such would suggest that while the overbought condition could limit the upside, the market will likely try to climb higher over the next two weeks. Continue to manage portfolio risk accordingly, but the bullish trend remains intact.

As noted, investors remain very optimistic about the market currently. Net bullish sentiment remains elevated, volatility is suppressed, and “bad news remains good news” for now.

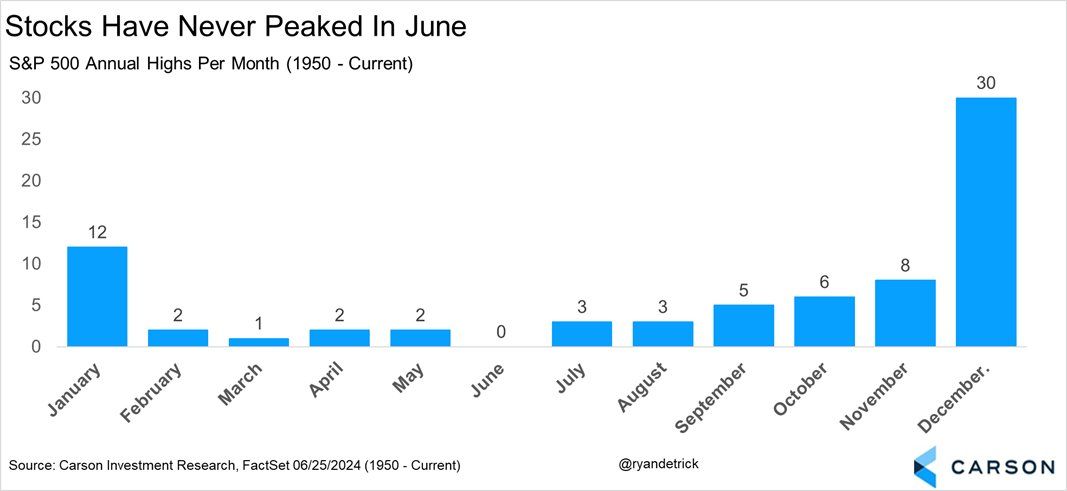

Did Stocks Peak In June?

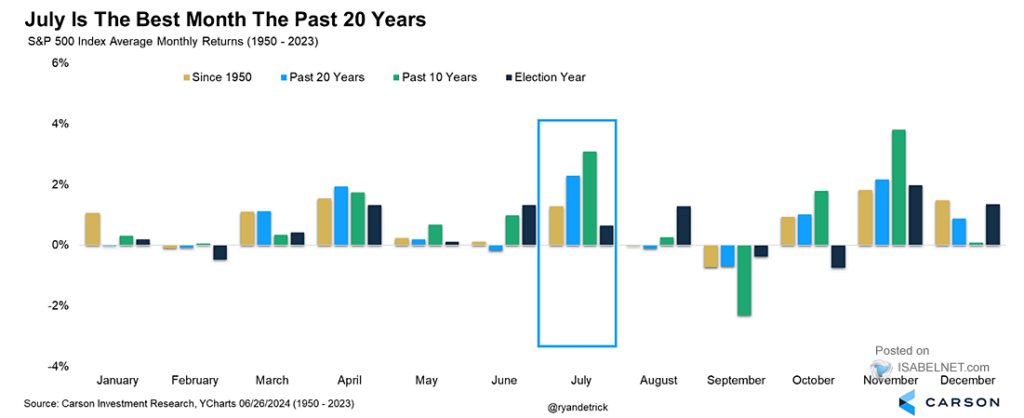

No, at least according to the last 75 years of history. The graph below, courtesy of Ryan Detrick of Carson, shows that the S&P 500 has never peaked for the year in June. However, not surprisingly, the odds of an annual high steadily increase from here.

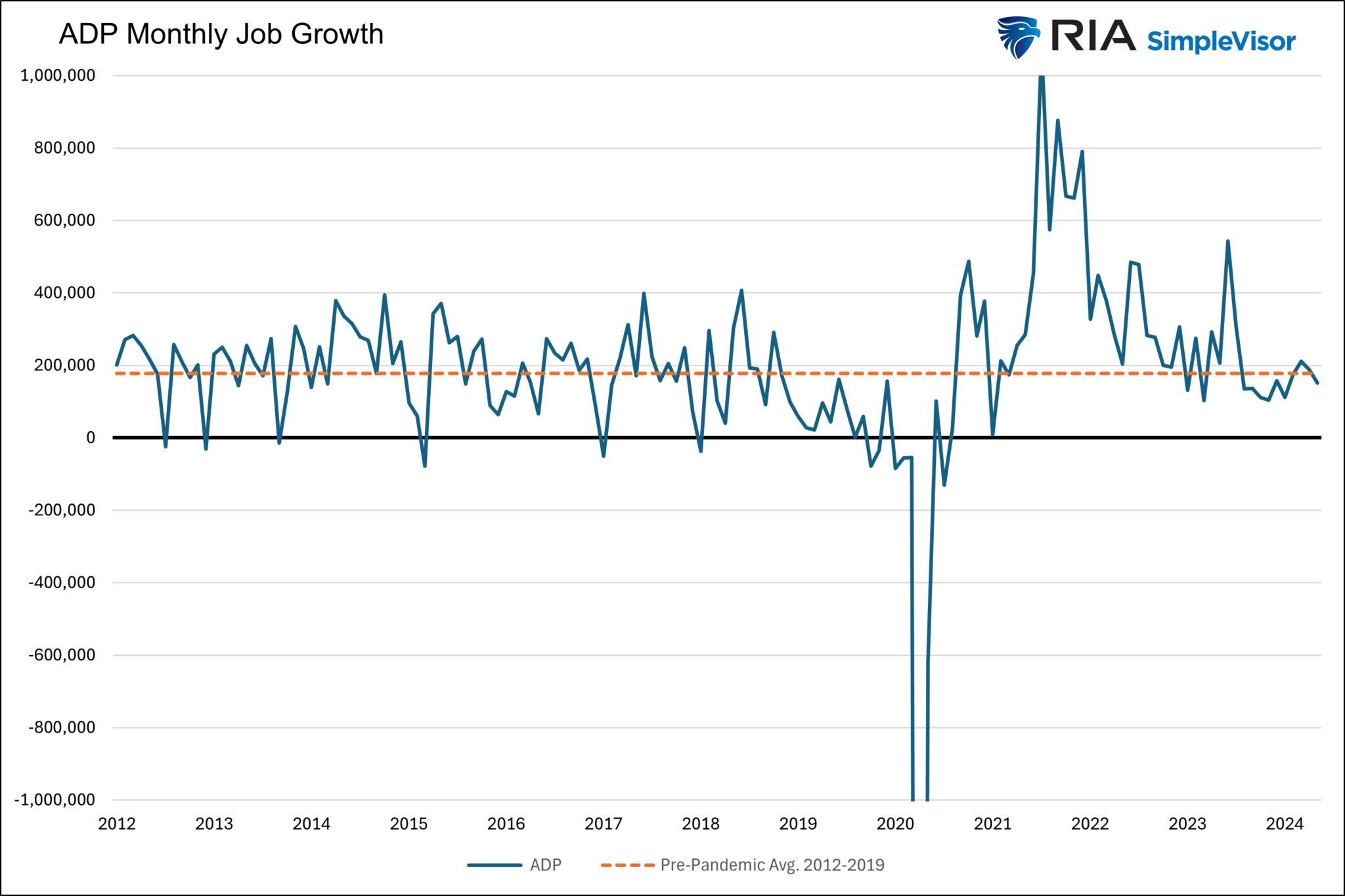

ADP Job Growth

ADP job growth, calculated from actual employment data and not surveys like the BLS, shows that the economy added 150k jobs last month. This is the lowest monthly growth since January. For context, ADP job growth averaged +178k from 2012 through 2019. Over the last twelve months, it has averaged 194k. The current reading (150k) is below both long-term and short-term trends but not overly concerning. That is not to say that the lower trend won’t continue, thus raising concerns in the future.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Petrodollar Panic: Separating Fact From Fiction

Recently, a few media outlets have warned of the imminent demise of the petrodollar agreement, commonly called the petrodollar. With such narratives comes investor anxiety. Consider the following article titles on the topic.

OPEC Will Sever Link With Dollar For Pricing Oil- The New York Times

The Petrodollar Is Dead and that’s a big deal- FX Street

After 50 Years, Death of the Petrodollar Signal End of U.S. Hegemony- The Street Pro

Before jumping to conclusions, let’s discuss what the petrodollar is and isn’t. With that knowledge, we can address concerns about the death of the petrodollar. Furthermore, we can discredit menacing headlines like-Petrodollar Deal Expires; Why This Could Trigger ‘Collapse of Everything.’

Before starting, we need to make a disclaimer. The New York Times article we bullet point above is not recent. We added it to show this is not a new story. The article dated June 1975 starts as follows:

LIBREVILLE, Gabon, June 9 — The oil‐producing nations agreed today to sever the link between oil prices and the dollar and to start quoting prices in Special Drawing Rights, the governor of the Iranian national bank, Mohammed Yeganeh, said.

What Is The Petrodollar?

In 1974, following the economically devastating oil embargo in which the price of crude oil per barrel rose four-fold, sparking a surge in inflation and weakening the economy, the U.S. desperately sought to avoid another embargo at all costs. U.S. politicians theorized that a stronger relationship with Saudi Arabia would go a long way toward achieving its goal.

Fortunately, the Saudis also hoped for a beneficial relationship with the U.S., and they needed a trustworthy investment home for their new oil riches. They also desired better military equipment. At the time, Saudi Arabia was running a huge budget surplus because of its windfall from high oil prices and relatively minor spending needs from within the country.

While there was never a formal petrodollar pact, it is widely believed that the U.S. and Saudi Arabia had a handshake agreement to meet each other’s needs. Saudi Arabia was encouraged to invest its surplus dollars in safe, high-yielding U.S. Treasury securities. In exchange, the U.S. would sell Saudi Arabia military equipment. Both hoped a better relationship would be a productive byproduct. Such is the petrodollar agreement.

The Petrodollar Was Not Really About The Dollar

We think the petrodollar discussions were principally about Saudi Arabia needing a safe home for their surpluses and the U.S. seeking dollars to fund her large fiscal deficits. While the dollar would be the currency for said transactions, it was not likely the focus of the talks.

In dealing with the immense costs of the Vietnam War and ambitious social spending to pacify social unrest, America sought deficit funding. Saudi Arabia needed to invest its surpluses. Given the unprecedented liquidity and safety of the U.S. Treasury market compared to other options, the “agreement” made a lot of sense for both parties. Furthermore, because Saudi oil revenue would be used to buy dollar-based U.S. Treasury bonds, it made sense for Saudi Arabia to require other oil buyers to pay in U.S. dollars.

We share two graphs to better appreciate the deteriorating U.S. fiscal position at the time. The first graph below highlights the deficits during the mid-1970s. Today, many would consider a $50—or $60 billion deficit minimal. But then, the deficits incurred were a sharp departure from the norm.

The second graph provides proper context. The nation was experiencing more significant federal deficits in the mid- to late 1970s than it faced during World War II. Given the immense spending on World War II, that fact was stunning to many people at the time.

Saudi Arabia Doesn’t Have Investible Dollars

Today, the situation is different. America still desperately needs funding, but Saudi Arabia doesn’t have budget surpluses to invest. Per a Bloomberg article entitled The Petrodollar Is Dead, Long Live The Petrodollar:

Fast forward to today, and Saudi Arabia doesn’t have a surplus to recycle at all. Instead, the country is borrowing heavily in the sovereign debt market and selling assets, including chunks of its national oil company, to finance its grand economic plans. True, Riyadh still holds significant hard currency reserves, some of them invested in US Treasuries. But it’s not accumulating them anymore. China and Japan have significant more money tied up on the American debt market than the Saudis do.

The Reserves Monopoly

Many believe the U.S. government bullies foreign countries into using the dollar, thus forcing them to have dollar reserves. Such seems logical as the reserves must be invested and can help fund our deficits.

We do not know what our politicians say to other countries behind closed doors. But we presume some “persuasion” presses other countries to use the dollar. Regardless, there are not many options for the dollar.

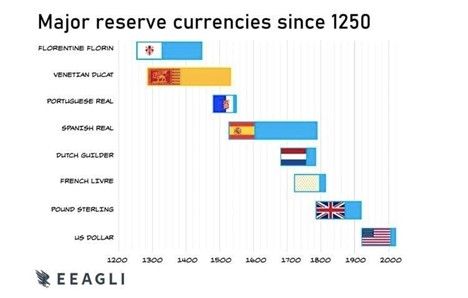

The four reasons, the rule of law, liquid financial markets, and economic and military might, all but guarantee the death of the dollar will not occur anytime soon.

No other country has all four of those traits. China and Russia lack the rule of law and liquid financial markets. Russia also has a small and fragile economy. Europe does not have liquid enough capital markets or military might.

Gold and Bitcoin are often rumored candidates to usurp the dollar. For starters, they do not earn a return on investment. Possibly more problematic, their prices are incredibly volatile. There are many other difficulties precluding them from full-fledged currency status, which we will save for another article.

Summary

Notwithstanding whether there was a formal agreement, the petrodollar is not going anywhere. Even if Saudi Arabia accepts rubles, yuan, pesos, or gold for its oil, it will need to convert those currencies into dollars in almost all instances.

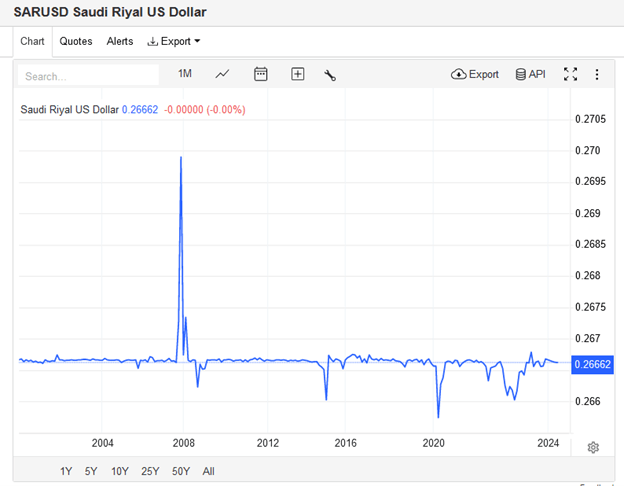

Consider that Saudi Arabia keeps its currency value pegged to the dollar, as shown in the graph below, courtesy of Trading Economics. They also hold approximately $135 billion of U.S. Treasury securities, a three-year high. Does it seem like Saudi Arabia is trying to disassociate from the U.S. dollar and U.S. financial markets?

Stories like those on the petrodollar and others on the “imminent” death of the dollar have been around for decades. Someday they will be right, and the dollar will follow the way of prior global reserve currencies. But for that to happen there needs to be a better alternative, and today, nothing even close exists.

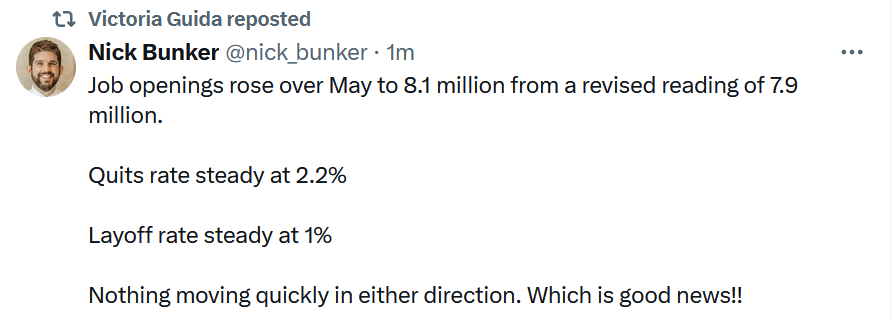

The Economy Is Normalizing – Whats Next?

Tuesday’s JOLTs report is one of many data points showing that the labor market is near or back to the prevailing conditions before the pandemic. It’s not just JOLTs and the labor market normalizing; most other economic indicators show the economy is finally normalizing at pre-pandemic levels.

Yesterday’s Commentary argued that while the unemployment and PCE inflation rates are not far from the Fed’s longer-term projections, the Fed Funds rate is too high, at almost 3% above their extended forecast. Given that divergence, we wrote: “Even if the economy continues to chug along without a recession, it appears that barring higher inflation, significant rate cuts in the coming year will be consistent with the Fed’s economic outlook.”

A reader asked us: “If the economy is normalizing, what comes next?” The oft-used airplane analogy may be the best way to answer. Can the Fed bring the economy back to a typical economic cruising altitude and keep it there? Or might the downward trajectory continue, leading to a soft or hard landing? Given that most other major economies exhibit little economic growth and the Fed is applying tight monetary policy, a new period of higher-than-average growth is the least likely scenario. However, that could change if significant fiscal stimulus follows the election. We are looking for signs that the economy might continue to weaken, thus prompting recession calls. However, the Wall Street consensus is for smooth sailing ahead. Stay tuned!

What To Watch Today

Earnings

Economy

Market Trading Update

In yesterday’s commentary, we discussed the drastic drop in bond ETFs, which sparked many questions. As usual, most things don’t mean anything. Intra-day and daily price movements in anything are usually unrelated to any macro theme and are a function of short-term overbought or oversold conditions.

Such is the case with the market as we begin the year’s second half. Historically, performance tends to be stronger in the first half of the month and weaker in the last half. August and September also tend to be weaker, particularly in election years.

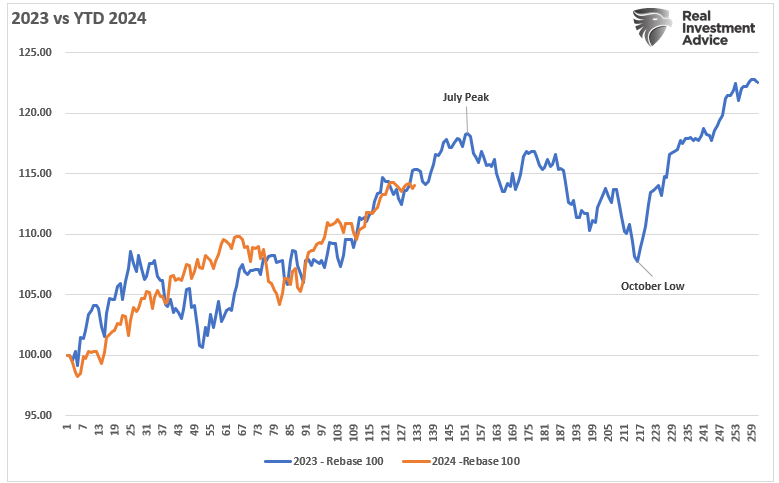

Interestingly, we are now repeating much of what we said this time last year. In 2023, the markets were racing higher, hoping for Fed rate cuts and the “artificial intelligence” craze. At that time, markets were overbought and deviated from their means, but momentum was very strong as volatility remained suppressed. Then, like today, we were warning of the potential for a 5-10% correction to reverse some of those conditions.

As shown, the beginning of this year has been almost a mirror image of last year, with market performance very close. Will the correlation continue, and we see a correction this summer, or will this time be different? I don’t know for certain, but the similarity is eerie, and the risk of correction is elevated in the near term. Trade accordingly.

More On Bad Breadth

The graph below from Ned Davis Research is very telling for two reasons. First, thus far in 2024, the percentage of stocks outperforming the S&P 500 is at a record low, going back about fifty years. This follows a near-record low in 2023. Looking back, there is only one other instance of two consecutive years with such poor market breadth: 1998 and 1999.

While comparing the internet era in the late 1990s to the AI era today may seem appropriate, it’s important to remember the old adage: “Markets can remain irrational longer than you can remain solvent.” The point is that while the market will correct at some point, and yes, AI and other stocks with massive price surges can fall by 30, 40, or even 50% or more, that may not occur for a while.

Accordingly, appreciate the risks and realize a correction is highly likely. However, to better anticipate such an event, close attention must be paid to the market technicals. As they always have, they will alert us when to take a more conservative posture.

Jerome Powell’s Latest Thoughts

Fed Chair Powell spoke on Tuesday morning in Portugal at an ECB forum and shared his latest thoughts on the economy, inflation, and rate cuts. He was generally dovish but didn’t seem overly anxious to cut interest rates. Below, we share a few poignant comments.

Inflation now shows signs of resuming its disinflationary trend.” “We are getting back on a disinflationary path.” “We’ve made a lot of progress.

I’m not going to be landing on any specific dates here today…so we’re aware that we have two-sided risks now, more so than we did a year ago. That’s a big change. I’d say risks are coming much more into balance now

The risk of inflation is that we act too fast

We are well aware of the risk going too soon and too fast

Inflation may get back to 2% late next year or the following year

As shown below, Fed Funds futures now imply an 83% chance the Fed will cut rates twice by year-end. The number of rate cuts has fluctuated between one and two over the previous two months.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

The Fed Funds Rate Is Too High

Let’s step back and ignore the last four years in which the economy cratered with the onset of the pandemic and then boomed on massive monetary and fiscal stimulus. Let’s also try to ignore the peak 6% core PCE inflation rate in 2022 and the historically low 3.4% unemployment rate in 2023. What if, in the years preceding the pandemic, we told you that in 2024, the Fed Funds rate would be 5.25-5.50%? You probably would have assumed inflation was at least 5% and the unemployment rate was exceptionally low.

The current unemployment rate is 4%, and the core PCE inflation rate is 2.6%. In December 2019, the unemployment rate was 3.6%, and the core PCE was 1.6%. At the time, Fed Funds were 1.5%. Here we sit today, with the unemployment rate .4% higher and core PCE 1% higher than in 2019. Yet, the Fed Funds rate is 4% more than in 2019. Does it seem a bit high? To help answer the question, consider the Fed’s long-term forecasts.

As we circle below, the Fed thinks the natural long-term unemployment rate is 4.2% and PCE 2.0%. Under such an outlook, the Fed believes Fed Funds should be 2.8%. While it’s hard to make a case for the Fed to cut rates today, a simple look at their two objectives, full employment and stable prices, and its long-term economic projections make one appreciate that the current Fed Funds rate is exceptionally high. Even if the economy continues to chug along without a recession, it appears that barring higher inflation, significant rate cuts in the coming year will be consistent with the Fed’s economic outlook.

What To Watch Today

Earnings

No notable earnings releases today

Economy

Market Trading Update

As discussed yesterday, this is the beginning of a new quarter, the end of the first half, and the beginning of the Q2 earnings season. We noted that with this holiday-shortened week, volatility could certainly pick up. Unsurprisingly, I received several emails about the sharp sell-off in long-date Treasury bond ETFs. As shown, bond ETFs had a sharp reversal due to end-of-quarter rebalancing and dividend distributions yesterday, temporarily suppressing the price. However, bonds had enjoyed a very nice rally and were overbought going into quarter-end, so the sell-off is unsurprising

The economic data continues to show economic deterioration, which is bond-supportive, so the recent selloff in bond ETFs is likely presenting a good buying opportunity for traders. The last time bonds approached this level of oversold conditions was in April and May before a decent rally occurred.

Economic Surprise Index

We have read articles warning of an imminent recession due to the low economic surprise index. While we rule nothing out, it’s best to appreciate what the index tells us. Surprise indexes measure specific economic data forecasts versus the actual data. When the surprise index declines, it simply means that economic forecasters are generally overly optimistic. Hence, economic data is weaker than expected. Initially, that typically means the economy is slowing. However, economists are quick to adjust their forecasts for trend changes. Once this occurs, data may still deteriorate, but economists’ forecasts tend to be closer to reality or often overly pessimistic. Frequently, the surprise index will rebound. However, that doesnt mean the economy is improving, it only means forecasts are more realistic.

As shown below, the surprise index tends to oscillate. Low readings can precede a recession, but they occur with enough frequency they often prove to be a false alarm.

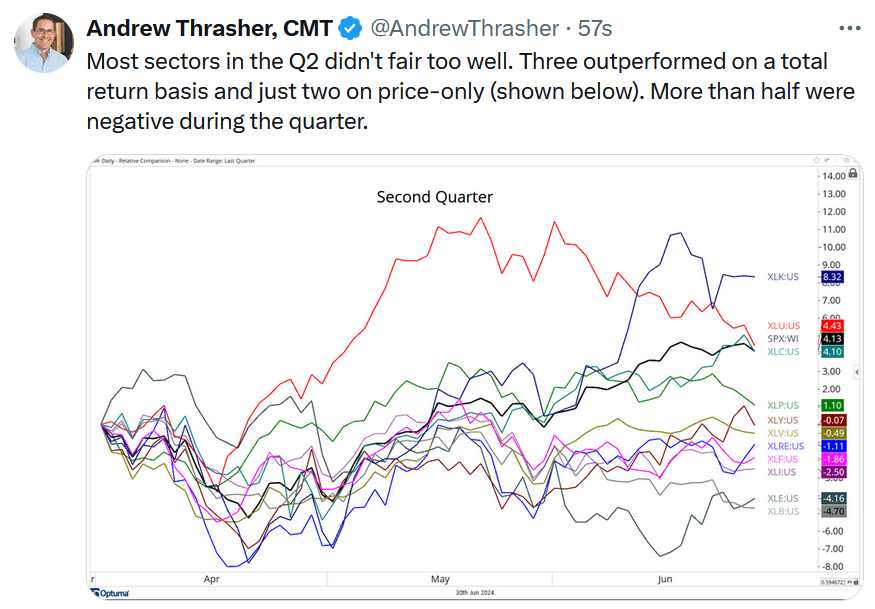

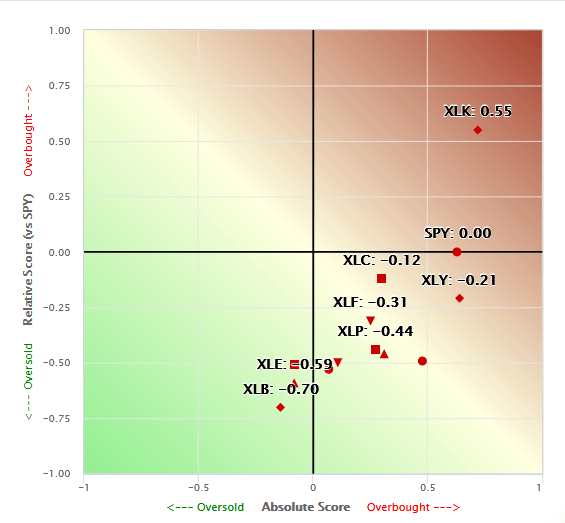

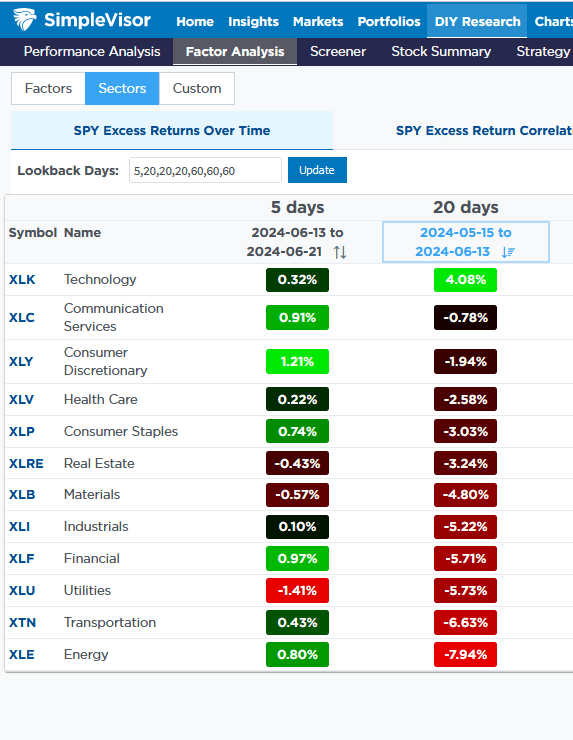

Sector Review- Materials Continue to Struggle

Over the last four weeks, the materials sector (XLB) has slipped by nearly 5% versus the S&P 500. Other than utilities, which are 6.5% worse than the S&P 500, it is the worst-performing sector over that period. Energy, which had the lowest relative SimpleVisor score for a few weeks running, was the market’s best-performing sector last week.

The second table, courtesy of SimpleVisor, shows the performance of each sector over consecutive periods ranging from the last five days to 20 and 60-day increments.

The third graph shows the price ratio of XLB to SPY. Other than XLB’s outperformance in the first quarter of 2024, XLB has been weak on a relative basis.

Some may say that the weakness in materials stocks is a telling signal about the state of the economy. We would counter, claiming that the service sector accounts for three-quarters of economic activity. The manufacturing sector has been in a recession for about two years, yet economic growth has been above average.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

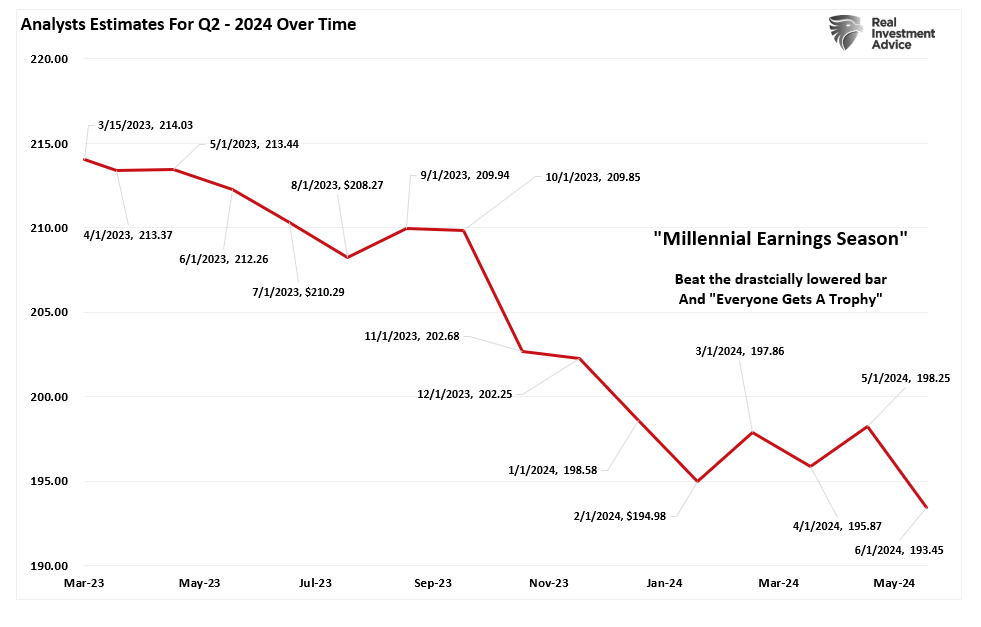

Earnings Bar Lowered As Q2 Reports Begin

Wall Street analysts continue significantly lowering the earnings bar as we enter the Q2 reporting period. Even as analysts lower that earnings bar, stocks have rallied sharply over the last few months.

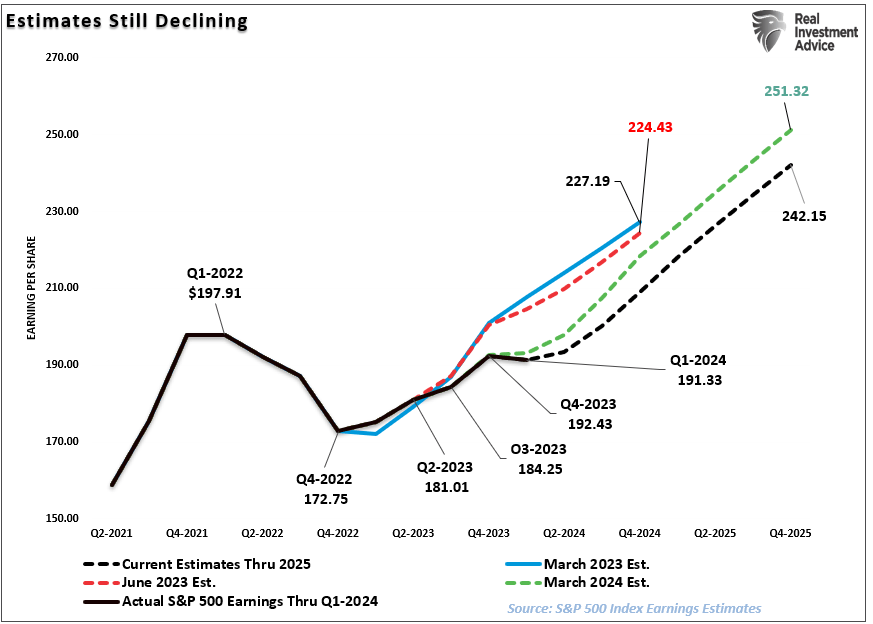

As we have discussed previously, it will be unsurprising that we will see a high percentage of companies “beat” Wall Street estimates. Of course, the high beat rate is always the case due to the sharp downward revisions in analysts’ estimates as the reporting period begins. The chart below shows the changes for the Q2 earnings period from when analysts provided their first estimates in March 2023. Analysts have slashed estimates over the last 30 days, dropping estimates by roughly $5/share.

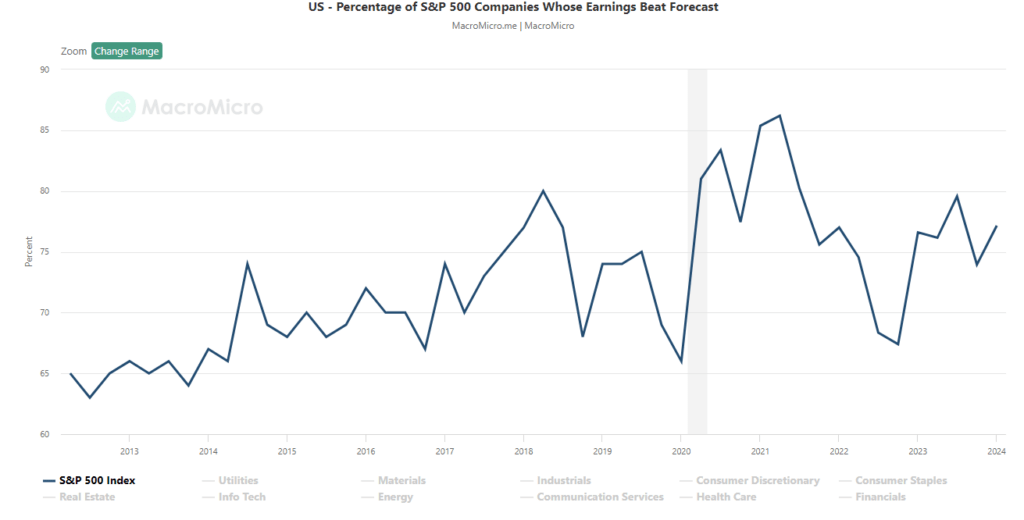

That is why we call it “Millennial Earnings Season.” Wall Street continuously lowers estimates as the reporting period approaches so “everyone gets a trophy.” An easy way to see this is the number of companies beating estimates each quarter, regardless of economic and financial conditions. Since 2000, roughly 70% of companies regularly beat estimates by 5%, but since 2017, that average has risen to approximately 75%. Again, that “beat rate” would be substantially lower if investors held analysts to their original estimates.

Analysts remain optimistic about earnings even with economic growth weakening, inflation remaining elevated, and liquidity declining. However, despite the decline in Q2 earnings estimates, analysts still believe that the first quarter of 2023 marked the bottom for the earnings decline. Again, this is despite the Fed rate hikes and tighter bank lending standards that will act to slow economic growth.

However, between March and June of this year, analysts cut forward expectations for 2025 by roughly $9/share.

However, even with the earnings bar lowered going forward, earnings estimates remain detached from the long-term growth trend.

As discussed previously, economic growth, from which companies derive revenue and earnings, must also strongly grow for earnings to grow at such an expected pace.

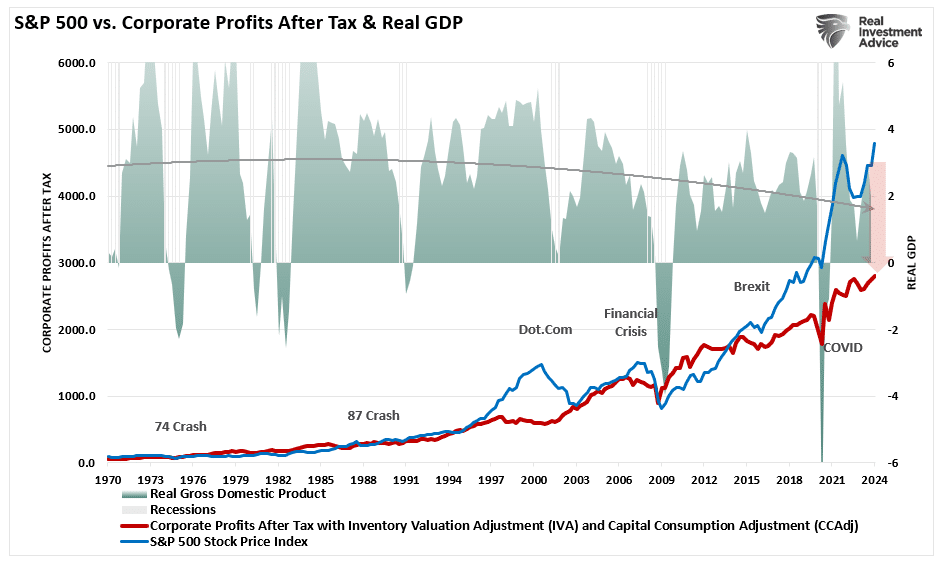

Since 1947, earnings per share have grown at 7.72%, while the economy has expanded by 6.35% annually. That close relationship in growth rates is logical, given the significant role that consumer spending has in the GDP equation. However, while nominal stock prices have averaged 9.35% (including dividends), reversions to underlying economic growth will eventually occur. Such is because corporate earnings are a function of consumptive spending, corporate investments, imports, and exports. The same goes for corporate profits, where stock prices have significantly deviated.

Such is essential to investors due to the coming impact on “valuations.”

Given current economic assessments from Wall Street to the Federal Reserve, strong growth rates are unlikely. The data also suggest a reversion to the mean is entirely possible.

The Reversion To The Mean

Following the pandemic-driven surge in monetary policy and a shuttering of the economy, the economy is slowly returning to normal. Of course, normal may seem very different compared to the economic activity we have witnessed over the last several years. Numerous factors at play support the idea of weaker economic growth rates and, subsequently, weaker earnings over the next few years.

The economy is returning to a slow growth environment with a risk of recession.

Inflation is falling, meaning less pricing power for corporations.

No artificial stimulus to support demand.

Over the last three years, the pull forward of consumption will now drag on future demand.

“We have previously noted an inherent problem with ongoing monetary interventions. Notably, the fiscal policies implemented post the pandemic-driven economic shutdown created a surge in demand and unprecedented corporate earnings.”

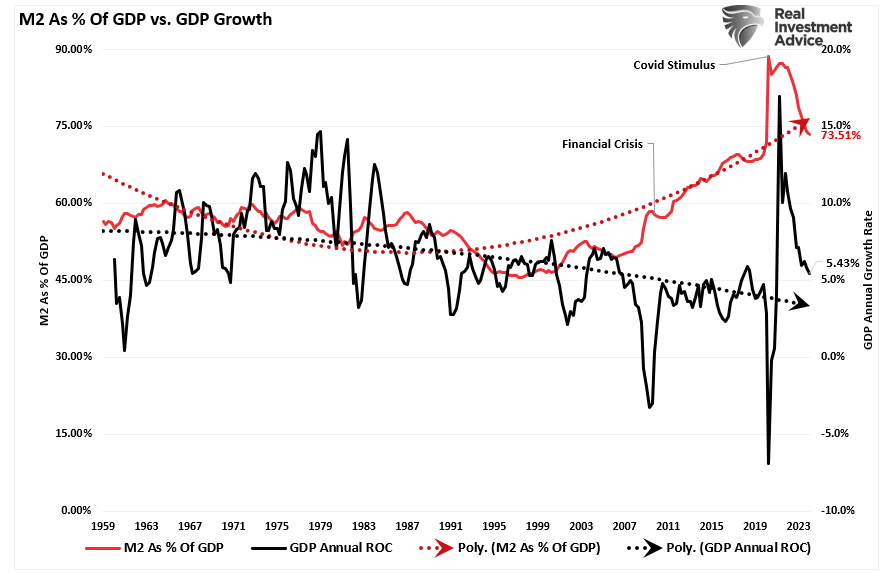

As shown below, the surge in the M2 money supply is over. Without further stimulus, economic growth will revert to more sustainable and lower levels.

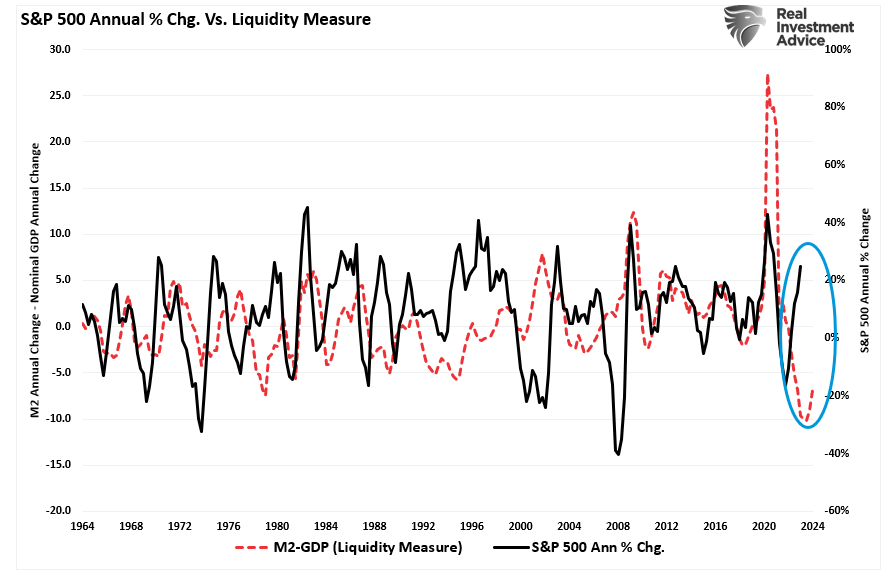

While the media often states that “stocks are not the economy,” as noted, economic activity creates corporate revenues and earnings. As such, stocks can not grow faster than the economy over long periods. A decent correlation exists between the expansion and contraction of M2 less GDP growth (a measure of liquidity excess) and the annual rate of change in the S&P 500 index. Currently, the deviation seems unsustainable. More notably, the current percentage annual change in the S&P 500 is approaching levels that have preceded a reversal of that growth rate.

So, either the annualized rate of return from the S&P 500 will decline due to repricing the market for lower-than-expected earnings growth rates, or the liquidity measure is about to turn sharply higher.

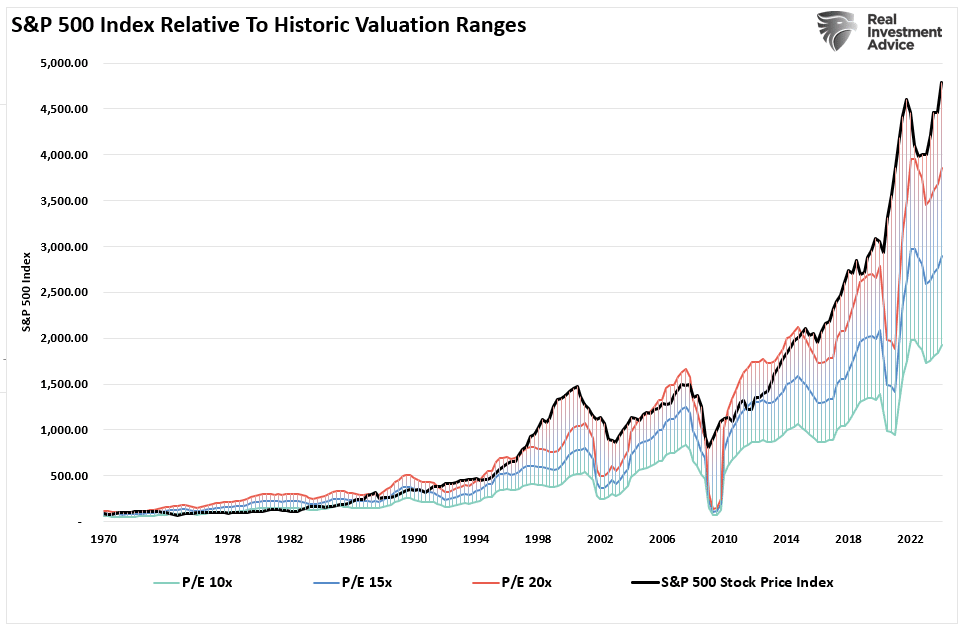

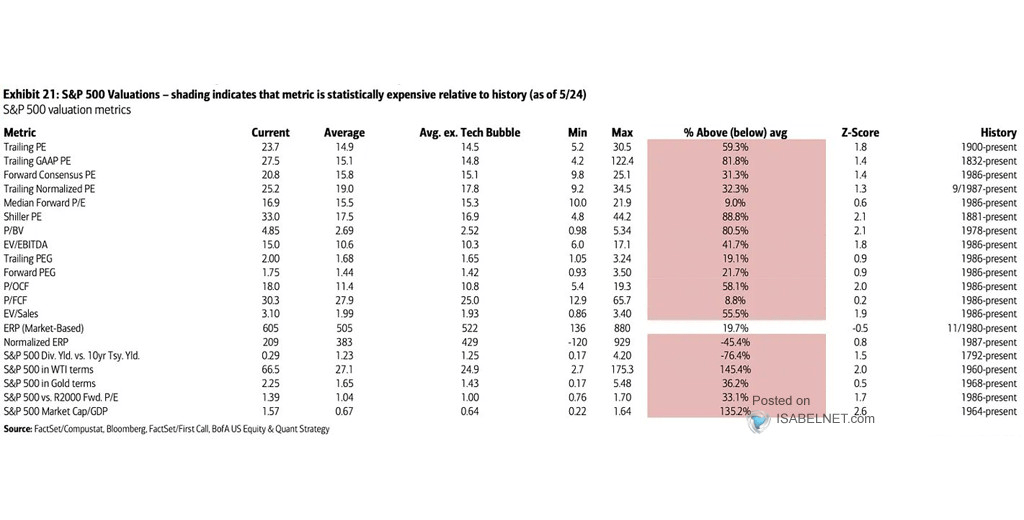

Valuations Remain A Risk

The problem with Wall Street consistently lowering the earnings bar by reducing forward estimates should be obvious. Given that Wall Street touts forward earnings estimates, investors overpay for investments. As should be obvious, overpaying for an investment today leads to lower future returns.

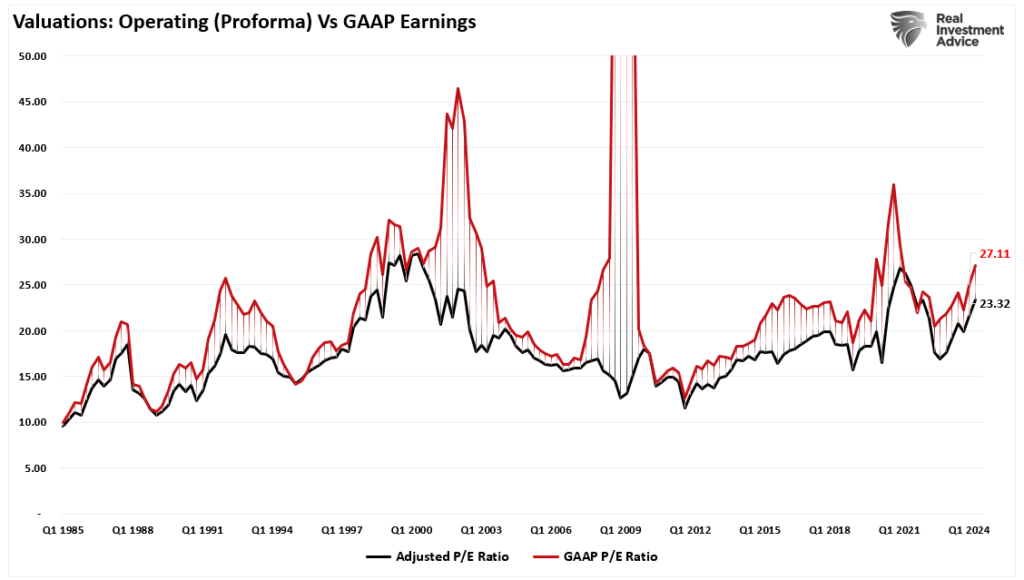

Even with the decline in earnings from the peak, valuations remain historically expensive on both a trailing and forward basis. (Notice the significant divergences in valuations during recessionary periods as adjusted earnings do NOT reflect what is occurring with actual earnings.)

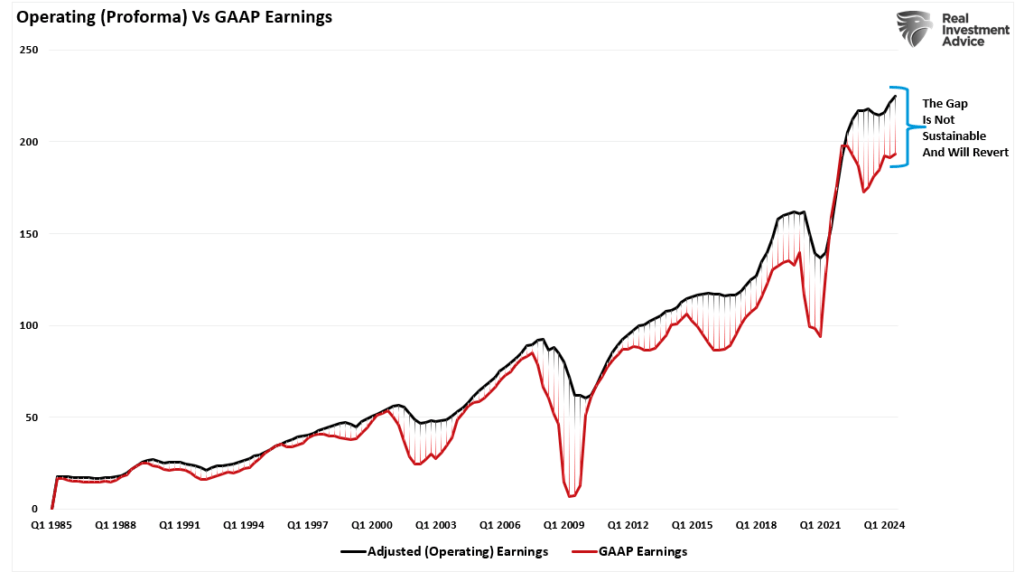

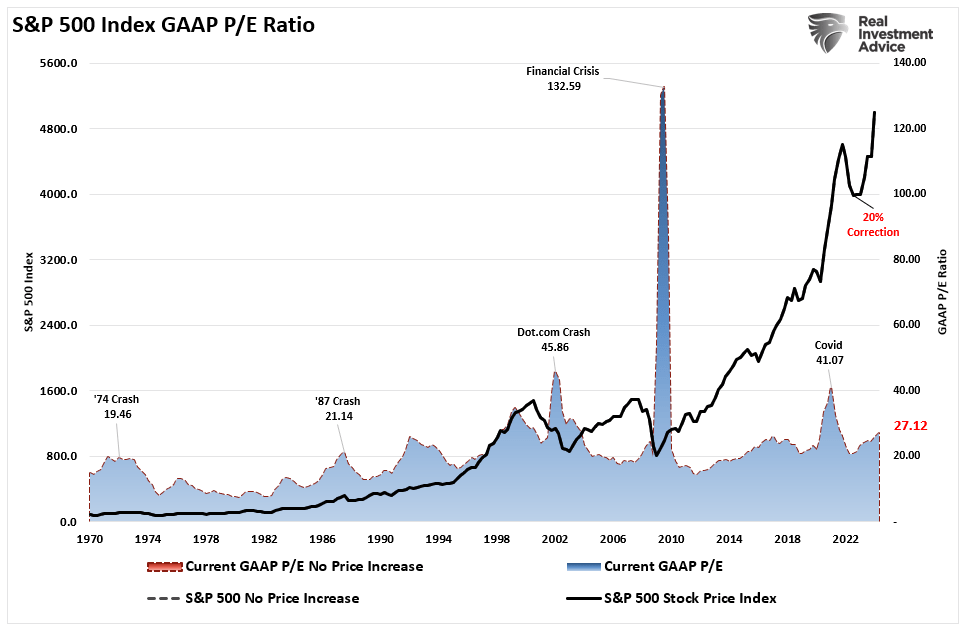

Most companies report “operating” earnings, which obfuscate profitability by excluding all the “bad stuff.” A significant divergence exists between operating (or adjusted) and GAAP earnings. When such a wide gap exists, you must question the “quality” of those earnings.

The chart below uses GAAP earnings. If we assume current earnings are correct, then such leaves the market trading above 27x earnings. (That valuation level remains near previous bull market peak valuations.)

Since markets are already trading well above historical valuation ranges, this suggests that outcomes will likely not be as “bullish” as many currently expect. Such is particularly the case if more monetary accommodations from the Federal Reserve and the Government are absent.

Trojan Horses

As always, the hope is that Q2 earnings and the entire coming year’s reports will rise to justify the market’s overvaluation. However, when earnings are rising, so are the markets.

Most importantly, analysts have a long and sordid history of being overly bullish on growth expectations, which fall short. Such is particularly the case today. Much of the economic and earnings growth was not organic. Instead, it was from the flood of stimulus into the economy, which is now evaporating.

Overpaying for assets has never worked out well for investors.

With the Federal Reserve intent on slowing economic growth to quell inflation, it is only logical that earnings will decline. If this is the case, prices must accommodate lower earnings by reducing current valuation multiples.

When it comes to analysts’ estimates, always remain wary of “Greeks bearing gifts.”

Supercore PCE Is The Weakest Since August