“Predictions Are Difficult…Especially When They Are About The Future” – Niels Bohr

We can’t predict the future. If we could, fortune tellers would win all of the lotteries. They don’t, we can’t, and we are not going to try to.

However, we can analyze what has happened in the past, weed through the noise of the present, and discern the possible outcomes of the future. The biggest problem with Wall Street, both today and in the past, is the consistent disregard of the unexpected and random events they inevitability occur.

There was once a study done of the accuracy of “predictions.” The study took predictions from a broad range of professions from psychics to weathermen. The study came to two conclusions. The first was that “weathermen” are the MOST accurate predictors of the future. The second conclusion was that the predictive ability was only accurate out to 3-days. Beyond 3-days, and the predictive ability was no better than a coin flip.

When it comes to trying to predict what will happen in the financial markets over the next year, which is an annual event, it is essentially an act of futility. Given the markets are affected by a broad spectrum of inputs from economics, to geopolitics, monetary policy, rates, and financial events, any prediction should be taken with a very high degree of skepticism.

So, with that said, here is how we are preparing for 2020.

Odds Have It

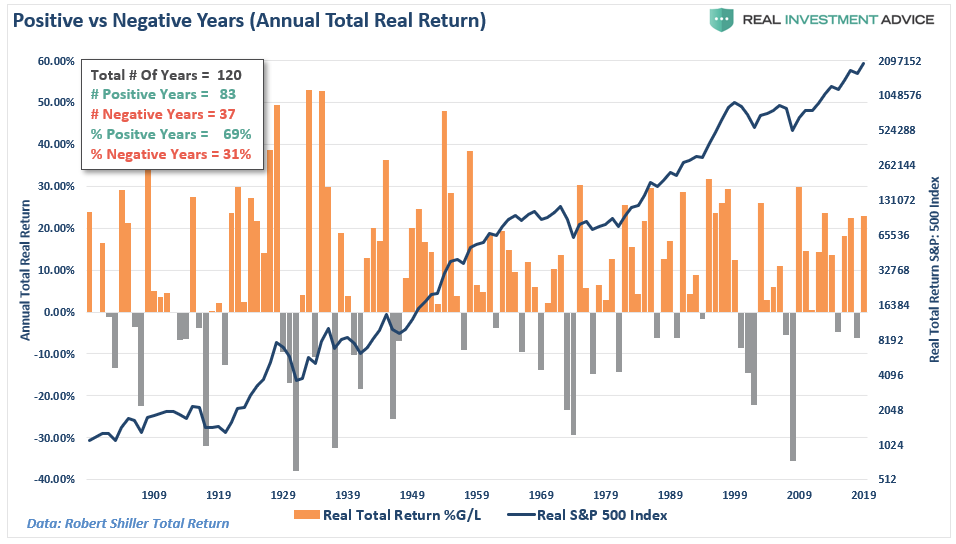

In our portfolio management practice, we begin with the basic assumption there is a 69% chance the market will finish the coming year at a level greater than where it started. That 69% probability comes from the fact that over the last 120-years, the market has (on a total real return basis) finished the year in positive territory 83 times, and negative only 37 times.

Therefore, from an “odds” perspective, markets are more likely to finish positive on any given year, than not. By starting our forecast with this basic assumption, it removes all the “guess work” of what has to go “right,” leaving us with only having to focus on the things which could potentially “go wrong.”

At the core of our portfolio management process is a risk management thesis. That philosophy was well defined by Robert Rubin, former Secretary of the Treasury, when he said;

“As I think back over the years, I have been guided by four principles for decision making. First, the only certainty is that there is no certainty. Second, every decision, as a consequence, is a matter of weighing probabilities. Third, despite uncertainty we must decide and we must act. And lastly, we need to judge decisions not only on the results, but on how they were made.

Most people are in denial about uncertainty. They assume they’re lucky, and that the unpredictable can be reliably forecast. This keeps business brisk for palm readers, psychics, and stockbrokers, but it’s a terrible way to deal with uncertainty. If there are no absolutes, then all decisions become matters of judging the probability of different outcomes, and the costs and benefits of each. Then, on that basis, you can make a good decision.”

It should be obvious that an honest assessment of uncertainty leads to better decisions, but the benefits of Rubin’s approach, and mine, goes beyond that. For starters, although it may seem contradictory, embracing uncertainty reduces risk while denial increases it. Another benefit of acknowledged uncertainty is it keeps you honest.

“A healthy respect for uncertainty and focus on probability drives you never to be satisfied with your conclusions. It keeps you moving forward to seek out more information, to question conventional thinking and to continually refine your judgments and understanding that difference between certainty and likelihood can make all the difference.”

The reality is that we can’t control outcomes. The most we can do is influence the probability of certain outcomes through the management of risks, and investing based on probabilities, rather than possibilities, which is important to capital preservation and investment success over time.

So, as we head into 2020, here is a short-list of the things we are either currently hedging portfolios against, or will potentially need to:

- China fails to comply with the terms of the “Phase One” trade deal which reignites the trade war.

- Earnings growth fails to recover, and valuations finally become a concern for the markets.

- Corporate profits, which have been essentially flat since 2014, deteriorate due to slower economic growth both domestically and globally.

- Excessively high consumer confidence converges with low levels of CEO Confidence as employment begins to weaken.

- Interest rates rise which trips up heavily leveraged consumers and corporations.

- Investors become concerned about excess valuations.

- A credit-related event causes a market liquidity crunch. (Convent-Lite, Leveraged Loans, BBB-rated downgrades all pose a potential threat)

- The Fed’s “repo-crisis” continues to grow and turns out to be something much more significant.

- Similar to 2016, a shocking election result.

While I am not going to address all of these concerns, I do want to touch a few that we feel are significant risks heading into the first half of the decade.

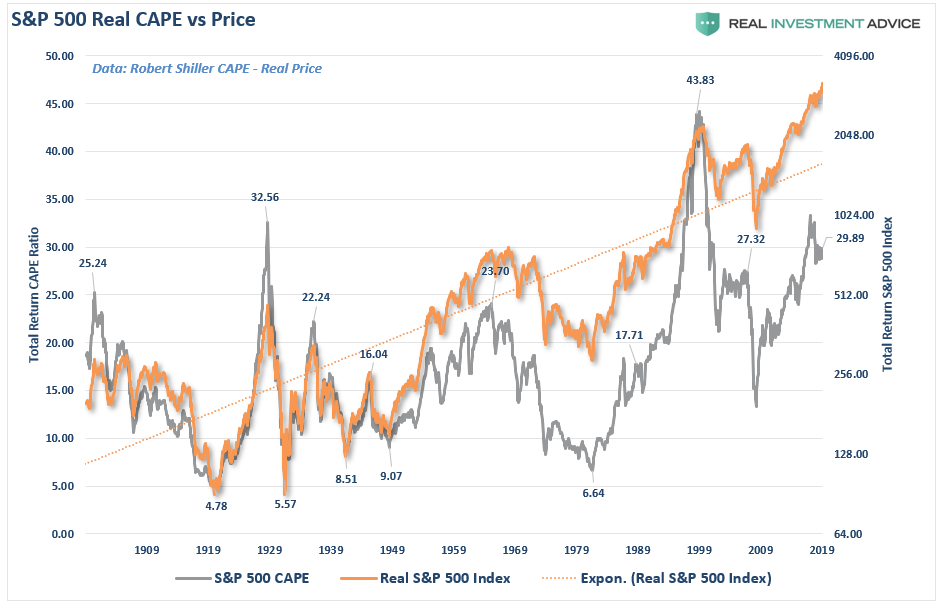

Valuations

While valuations are a terrible market timing device, they do impact long-term returns and investment outcomes. Currently, at 30x earnings, valuations are elevated, which suggests that the next decade of returns will be significantly lower than the last. Statistically, returns in the very low single digits should be expected.

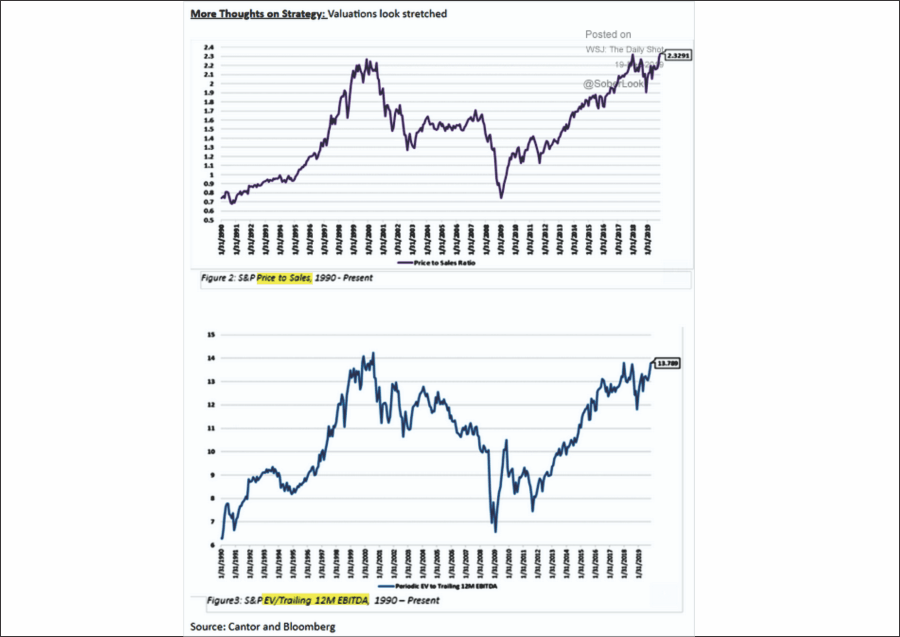

However, it isn’t just PE ratios which are extended, but both Price-to-Sales and Enterprise Value to EBITDA (Earnings Before Interest Taxes Depreciation Amortization) are at or near all time highs.

Record highs in stocks, near-record lows in bond yields, and historically tight credit spreads present significant challenges for investors. Economic data has improved, but many fundamental economic gauges remain soft relative to pre-crisis averages, and are inconsistent with current asset price levels and valuations.

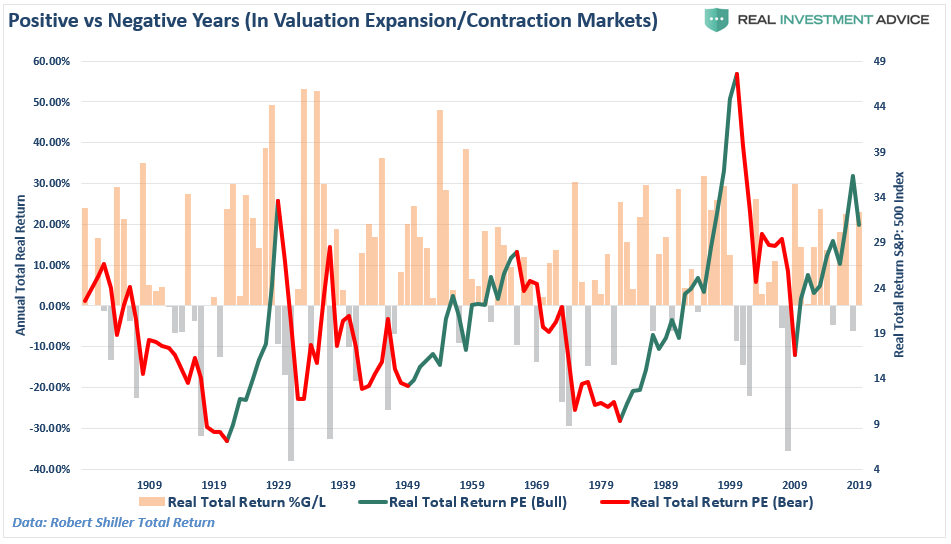

Importantly, it is worth noting that negative returns tend to cluster during periods of declining valuations. These “clusters” of negative returns are what define “secular bear markets.”

Most investors do not seem at all concerned as money continues to move into risky asset classes, a classic sign of a bubble. While a defensive posture seems prudent, the technical picture remains supportive of further gains. One should respect the momentum behind these moves for the foreseeable future, but be mindful that liquidity can evaporate quickly.

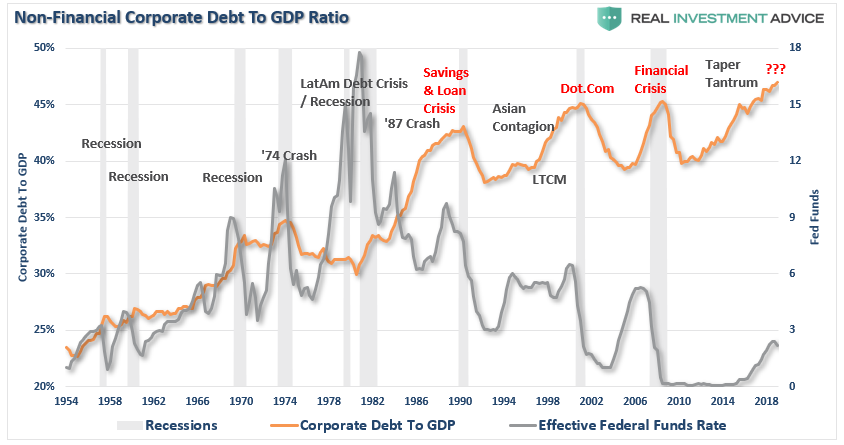

The Debt Risk

One of the common misconceptions in the market currently, is that the “subprime mortgage” issue was vastly larger than what we are talking about currently.

Not by a long shot.

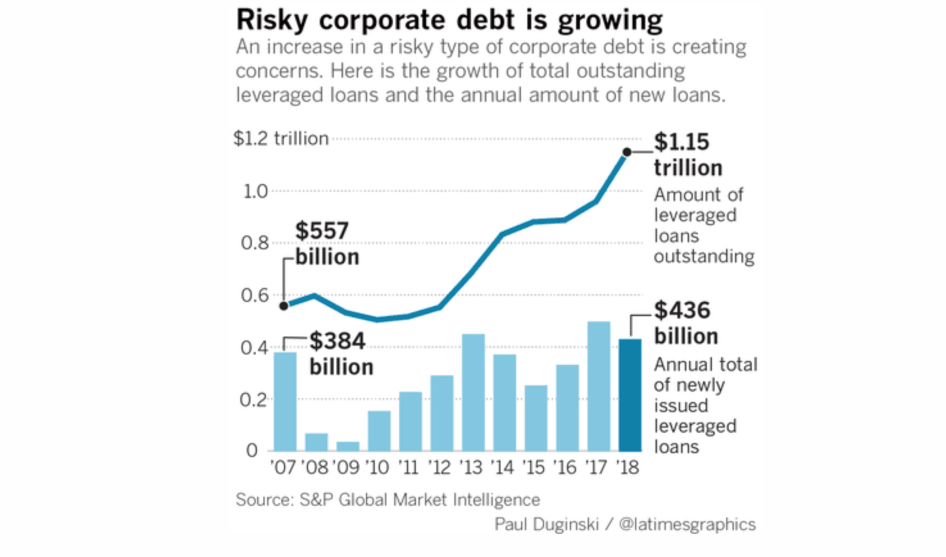

Combined, there is about $1.15 trillion in outstanding U.S. leveraged loans — a record that is double the level five years ago — and, as noted, these loans increasingly are being made with less protection for lenders and investors.

Just to put this into some context, the amount of sub-prime mortgages peaked slightly above $600 billion or about 50% less than the current leveraged loan market.

Of course, that didn’t end so well.

Currently, the same explosion in low-quality debt is happening in another corner of the US debt market as well.

As noted by John Mauldin:

“In just the last 10 years, the triple-B bond market has exploded from $686 billion to $2.5 trillion—an all-time high. To put that in perspective, 50% of the investment-grade bond market now sits on the lowest rung of the quality ladder.

And there’s a reason BBB-rated debt is so plentiful. Ultra-low interest rates have seduced companies to pile into the bond market and corporate debt has surged to heights not seen since the global financial crisis.”

The biggest risk currently is refinancing the debt as over the next 5-years, more than 50% of the debt is maturing. A weaker economy, recession risk, falling asset prices, or rising interest rates could well lock many corporations out of refinancing their share of this $5 trillion debt. Defaults will move significantly higher, and much of this debt will be downgraded to junk.

This is a problem the Fed can not fix with more liquidity.

Technically Troubling

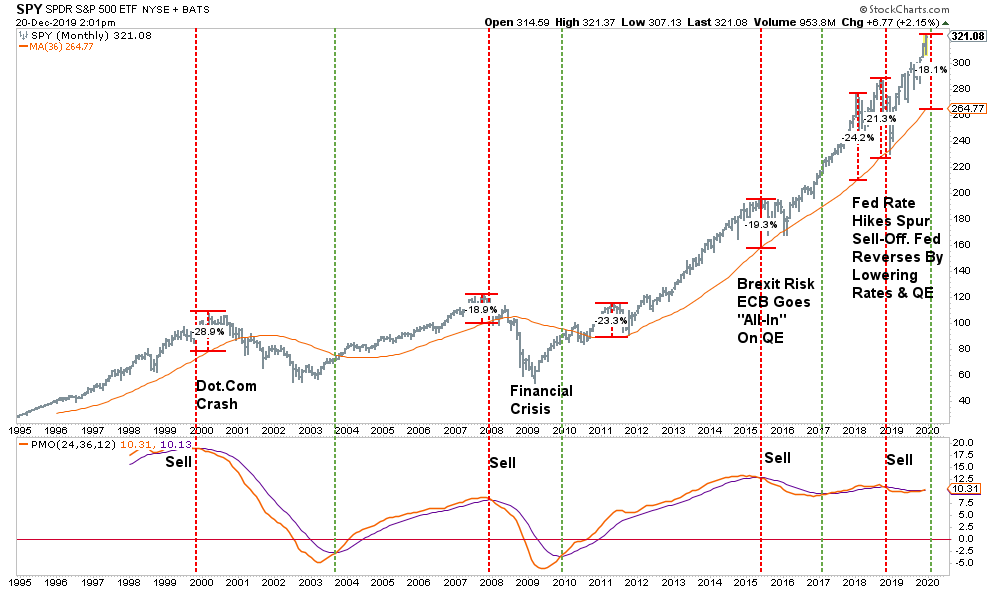

In last week’s Technically Speaking we discussed the more extreme deviations in the market. To wit:

The first chart shows the monthly buy/sell signals stretched back to 1995 (25 Years). As shown, these monthly ‘buy’ and ‘sell’ indications are fairly rare over that stretch. What is interesting is that since 2015 there have been two-major sell signals, both of which were arrested by Central Bank interventions.”

With these “buy signals” in place, and the market pushing higher on conclusions of “trade deals” and the election of the conservative party in the U.K. (which clears the way for Brexit), the markets rallied further toward our target of 3300.

In the short-term it is entirely feasible, particularly with the Federal Reserving pushing billions of dollars into the financial system currently, the bull market could easily eclipse our target of 3300. However, in the longer-term, virtually all of our primarily technical measures are stretched to levels normally seen near market tops rather than at the beginning of a new stretch of gains.

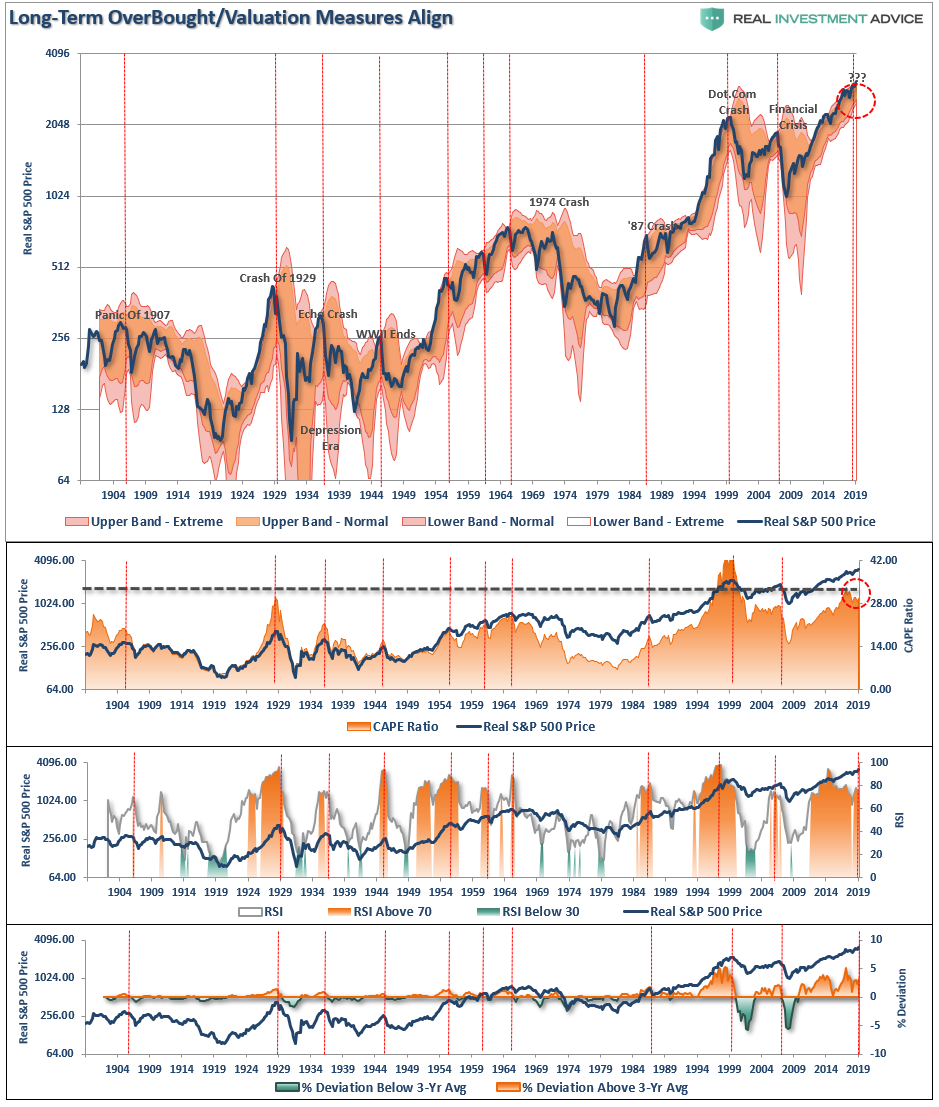

There are several measures used to justify current valuations, but they sound similar to those used in the dot-com Tech bubble. The relationships between valuation and fundamentals, on which cash flows are ultimately based, are grossly dislocated. Markets may well move higher, but to advocate a full allocation to equities under current circumstances ignores warnings of bubbles past.

Stock market cap-to-GDP, price-to-sales, margin balances, cyclically-adjusted price-to-earnings ratios, and others argue convincingly that the stock market is either near historic valuations, or well through them. Owning well-selected, single-name companies because they are fundamentally cheap, not relatively cheap, makes sense. Otherwise, limiting general equity allocation exposures is prudent until reasonable opportunities return. We suggest setting stop losses, and/or options strategies to help limit downside risk and retain any additional upside.

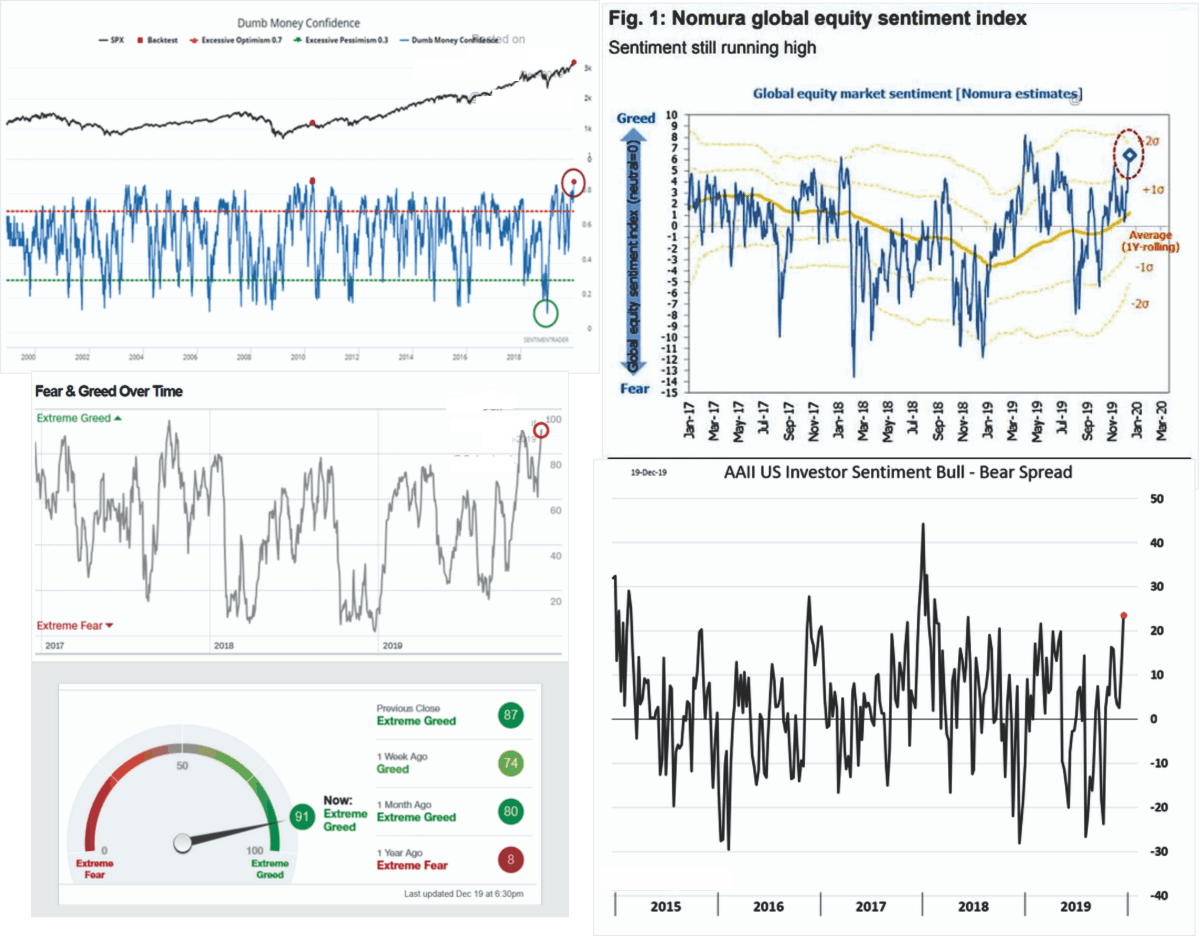

Sentiment Is Excessively Bullish

This past summer everyone was convinced a recession was near, now there is no such concern and investors are literally as “bullish” as they can get.

From a contrarian point of view, this is a fairly obvious warning to reduce risk in the market. However, the “Fear Of Missing Out,” is overriding investor logic at the moment. The recent market surge, which started coincidentally with the Fed’s restart of “QE, Not QE,” is very reminiscent of the surge in asset prices we saw at the end of 1999 as the Fed flooded the system with liquidity in advance of the potential “Y2K” issues.

As noted in our RIAPRO Daily Market Commentary:

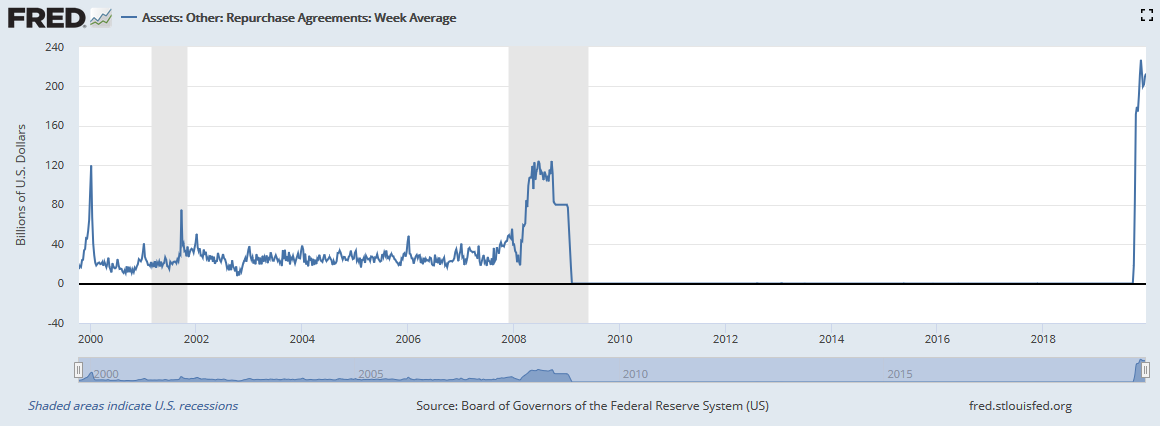

“Today’s ‘Chart of the Day’ shows the surge in the NASDAQ index, which occurred during the last few months of 1999. Most people attribute the massive gain to the feverish pitch in the dot com bubble. We believe the real culprit was the Fed which added substantial amounts of repo liquidity to the banking sector due to concerns of Y2K and the potential for mass computer malfunctioning. Those repo funds gravitated to the financial markets.

For more, please read the following WSJ article from 1999- Federal Reserve Clears Loan Facility Linked To Y2K Computer Problems.”

“The graph below shows the 10x surge in repo during late 1999 and its quick removal shortly after the New Year. Note the recent surge, on the right side of the graph, dwarfs the 1999 experience and that is before an expected $500 billion spike in repo financing over the next week or two.”

“Unlike 1999, we have our doubts as to how quickly the graph normalizes, as the Fed continues to underestimate the scope of the growing overnight funding issues.

To quote Yogi Berra “it’s deja vu, all over again.”

Conclusion

Statistically speaking, the odds suggest that the market could indeed be higher in 2020. However, there are numerous risks which could derail the markets which should not be dismissed.

This is not a “bearish forecast.” It is just an assessment of trends, statistics, and probabilities given the current monetary, financial and economic backdrop.

If we are wrong, and stocks do post gains in the coming year, being more conservative will only mean a small relative under-performance in your portfolio next year.

If we are right, the preservation of capital will be far more beneficial. As we have stated previously, participating in the bull market over the last decade is only one-half of the job. The other half is keeping those gains during the second half of the full market cycle.

One of my favorite quotes is by Howard Marks and is a principle that we live by in our little shop;

“Resisting – and thereby achieving success as a contrarian – isn’t easy. Things combine to make it difficult; including natural herd tendencies and the pain imposed by being out of step, since momentum invariably makes pro-cyclical actions look correct for a while. (That’s why it’s essential to remember that “being too far ahead of your time is indistinguishable from being wrong.”)

Given the uncertain nature of the future, and thus the difficulty of being confident your position is the right one – especially as price moves against you – it’s challenging to be a lonely contrarian.”

As we enter into 2020 it may pay to be a little more cautious after such a large rise in the financial markets.

Let me leave you with Bob Farrell’s 10 Rules:

- Markets tend to return to the mean over time

- Excesses in one direction will lead to an opposite excess in the other direction

- There are no new eras — excesses are never permanent

- Exponential rapidly rising or falling markets usually go further than you think, but they do not correct by going sideways

- The public buys the most at the top and the least at the bottom

- Fear and greed are stronger than long-term resolve

- Markets are strongest when they are broad and weakest when they narrow to a handful of blue-chip names

- Bear markets have three stages — sharp down, reflexive rebound and a drawn-out fundamental downtrend

- When all the experts and forecasts agree — something else is going to happen

- Bull markets are more fun than bear markets

Our job is managing risk to conserve principle and create absolute returns over time. What matters most to us is that we provide a disciplined management process suitable for our clients who seek long-term performance as measured by annualized and risk-adjusted returns, and conservation of investment principle.

We wish you a prosperous 2020.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read