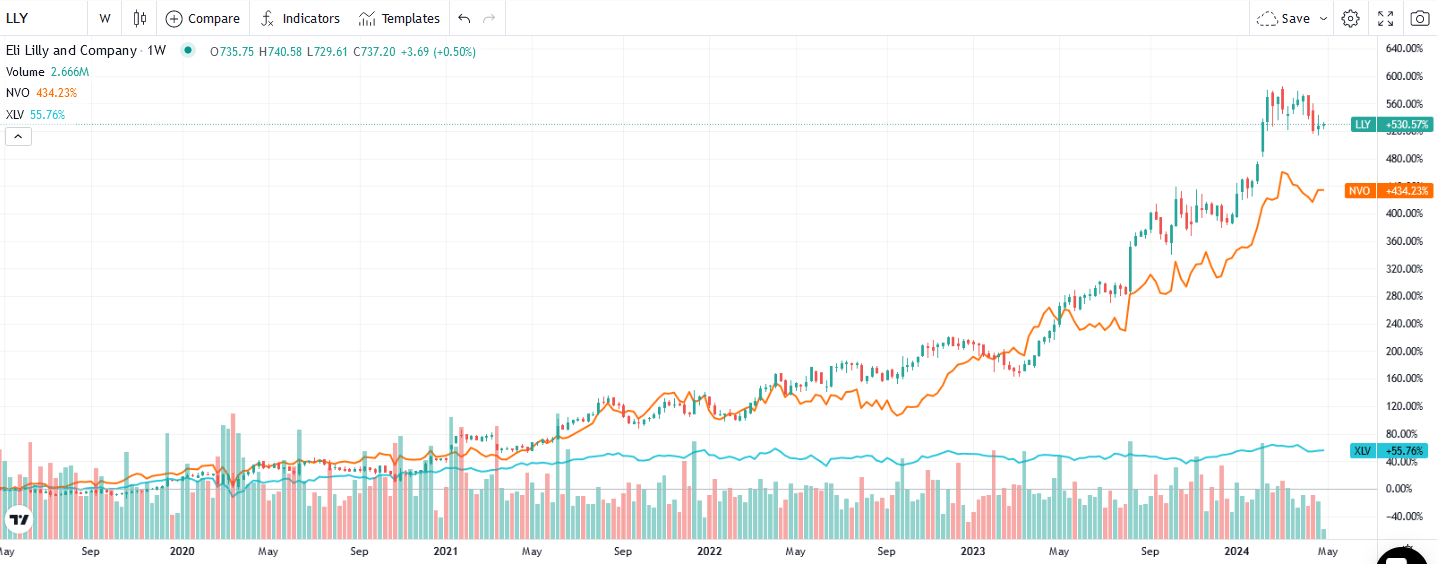

Eli Lilly (LLY) shares have risen significantly as the company is proving to be a leader in a new class of drugs that help with weight loss and diabetes. For the quarter, its total revenue was $8.77 billion, which is 26% higher than the first quarter of 2023. Revenues for their four drugs that help with weight loss and diabetes are as follows: Trulicity ($1.46bn), Mounjaro ($1.81bn), Zepbound ($515mm), and Humalog ($538mm). These drugs single-handedly account for almost half of Lilly’s revenue.

Bloomberg estimates that by the year 2030, annual sales of weight-loss medications will reach $80bn, making them among the largest class of drugs in history, as measured by sales. Further, they expect Eli Lilly and Novo Nordisk to garner more than 90% of the market. The revenue from these weight loss and diabetes drugs is snowballing, and plenty of potential remains. First, consider that 83% of Mounjaro’s sales are domestic, and Novo Nordisk reports that 90% of Ozempic sales are domestic. Rapid revenue growth can continue as sales in the U.S. and worldwide increase. Further driving growth, Medicare’s decision to subsidize Wegovy for heart disease patients and similar actions by the insurance companies provide another impetus for growth.

The graph below shows the tremendous growth in Eli Lilly (LLY) and Novo Nordisk (NVO) shares as compared to the broader healthcare sector (XLV).

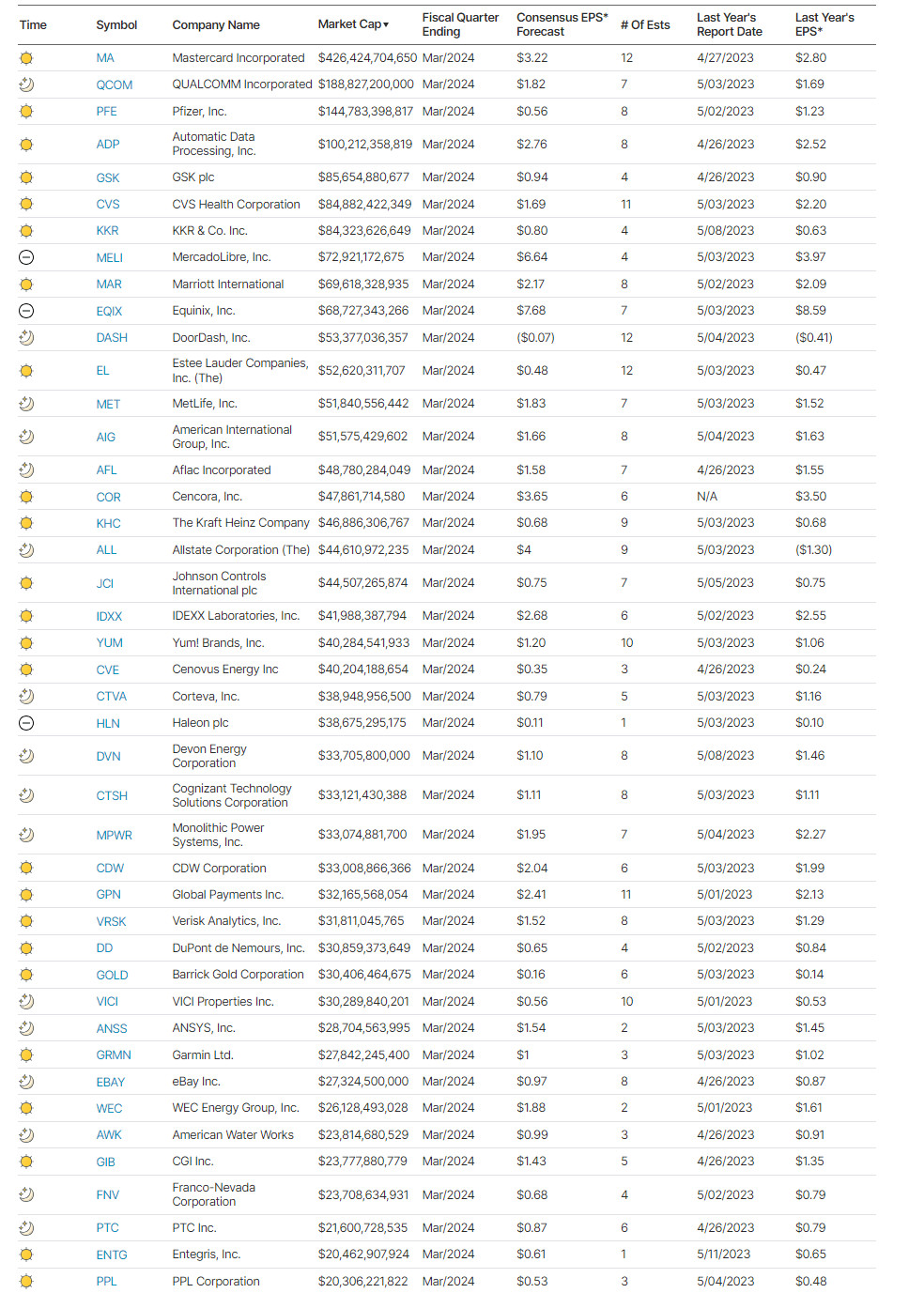

What To Watch Today

Earnings

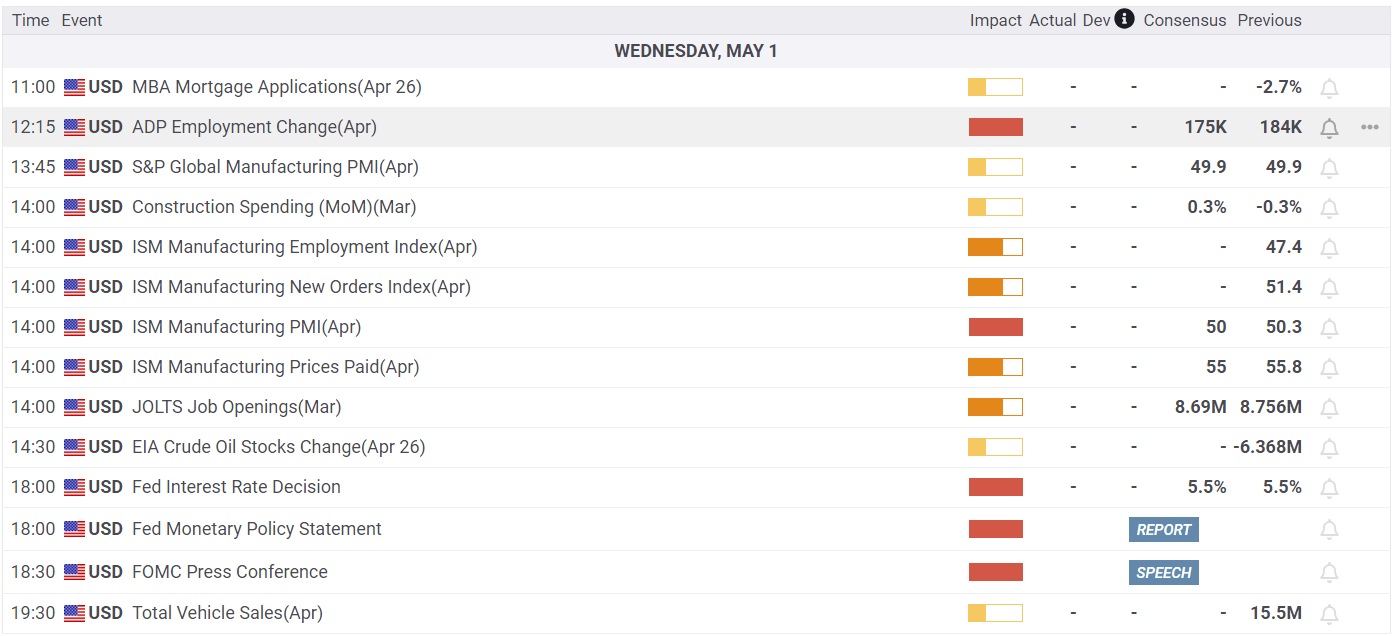

Economy

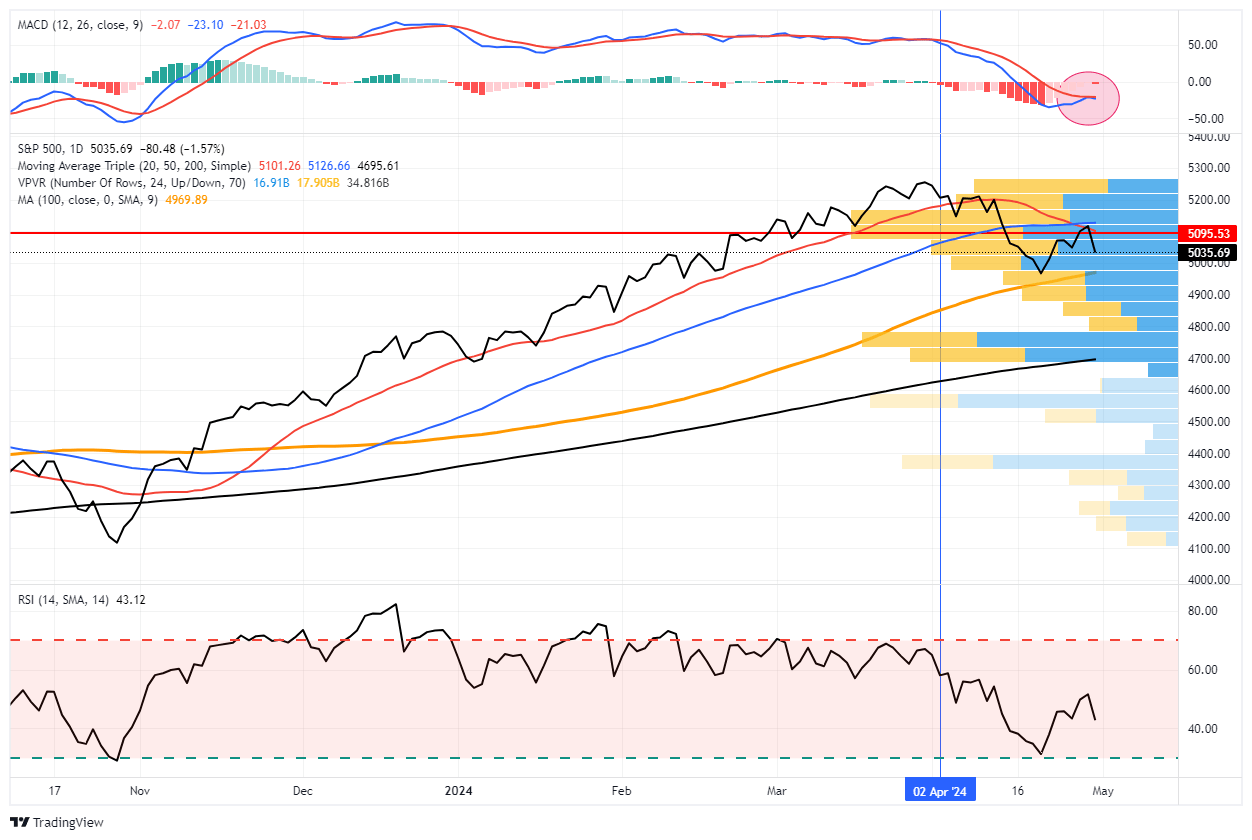

Market Trading Update

As discussed yesterday, the market failed at the test initial resistance at the 50-DMA. While that failure is unsurprising, given the recent rally from the lows, it is now paramount the market holds crucial support at the 100-DMA. This correction continues to be a low volatility event, which suggests it is unlikely to devolve into a deeper decline. However, it is always important to never discount a possibility entirely. The outcome of the FOMC meeting today is expected to be a non-event, with Fed Chair Powell continuing to hold the line on economic data and rate cuts later this year. Of course, going into the meeting, it is unsurprising traders took some of the recent gains just in case the Fed comes out more “hawkish” than expected.

Earnings continue to be okay, with Apple (AAPL) reporting tomorrow and the employment report on Friday. However, there is plenty of room for additional volatility until next week.

Higher Wages Spook Markets

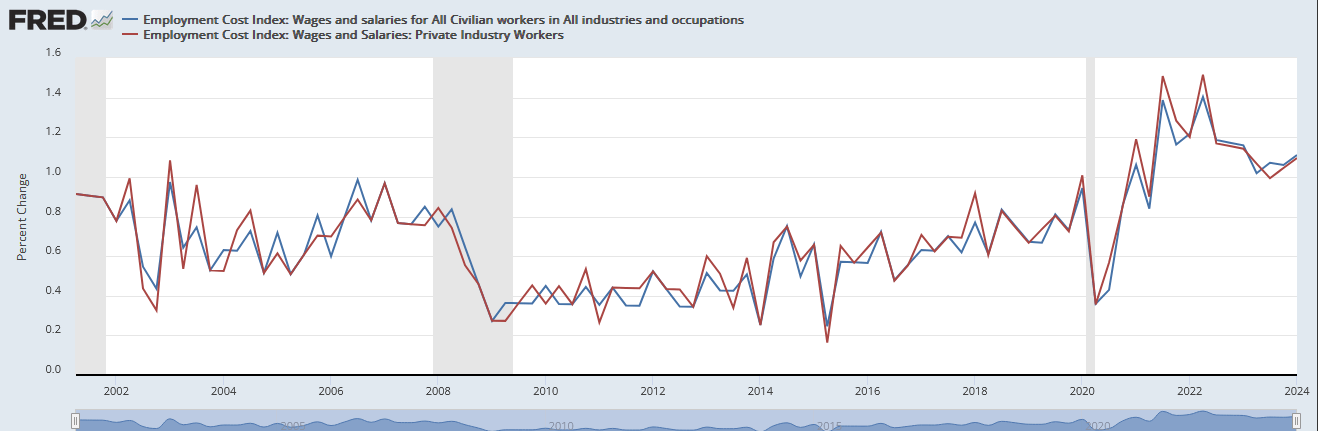

The employment cost index (ECI) rose more than expected, prompting concern that the Fed may further delay rate cuts. The ECI for the quarter was up 1.1%, above estimates of 0.9% and last quarter’s 0.9% reading. The graph below shows that the private and civilian sectors are closely aligned.

For the last few years, the Fed has been worried that higher wages will feed more inflation. Such a feedback loop is known as a price-wage spiral. Per Nick Timiraos of the Wall Street Journal, “The ECI is seen inside the Fed as the highest-quality measure of compensation growth.” While ECI adds to concerns that inflation could stay sticky, Nick caveats the increase, saying that the higher-than-expected increase in wages may be a function of cost-of-living increases and minimum wage adjustments given at the start of the year. Again, this is a quarterly number, so the data encompasses January, February, and March.

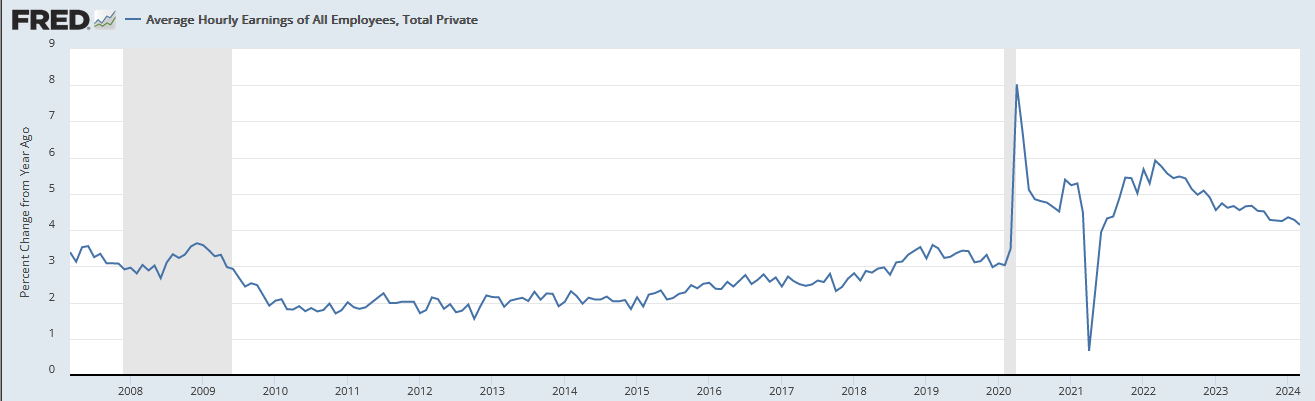

Thus far, the monthly BLS labor report has not confirmed the latest ECI data. The second graph shows average hourly earnings continue to decline. The monthly changes in hourly earnings also do not show a recent upward bias, as we see in ECI. This Friday’s BLS will provide an update on wages.

Chicago PMI And Consumer Confidence

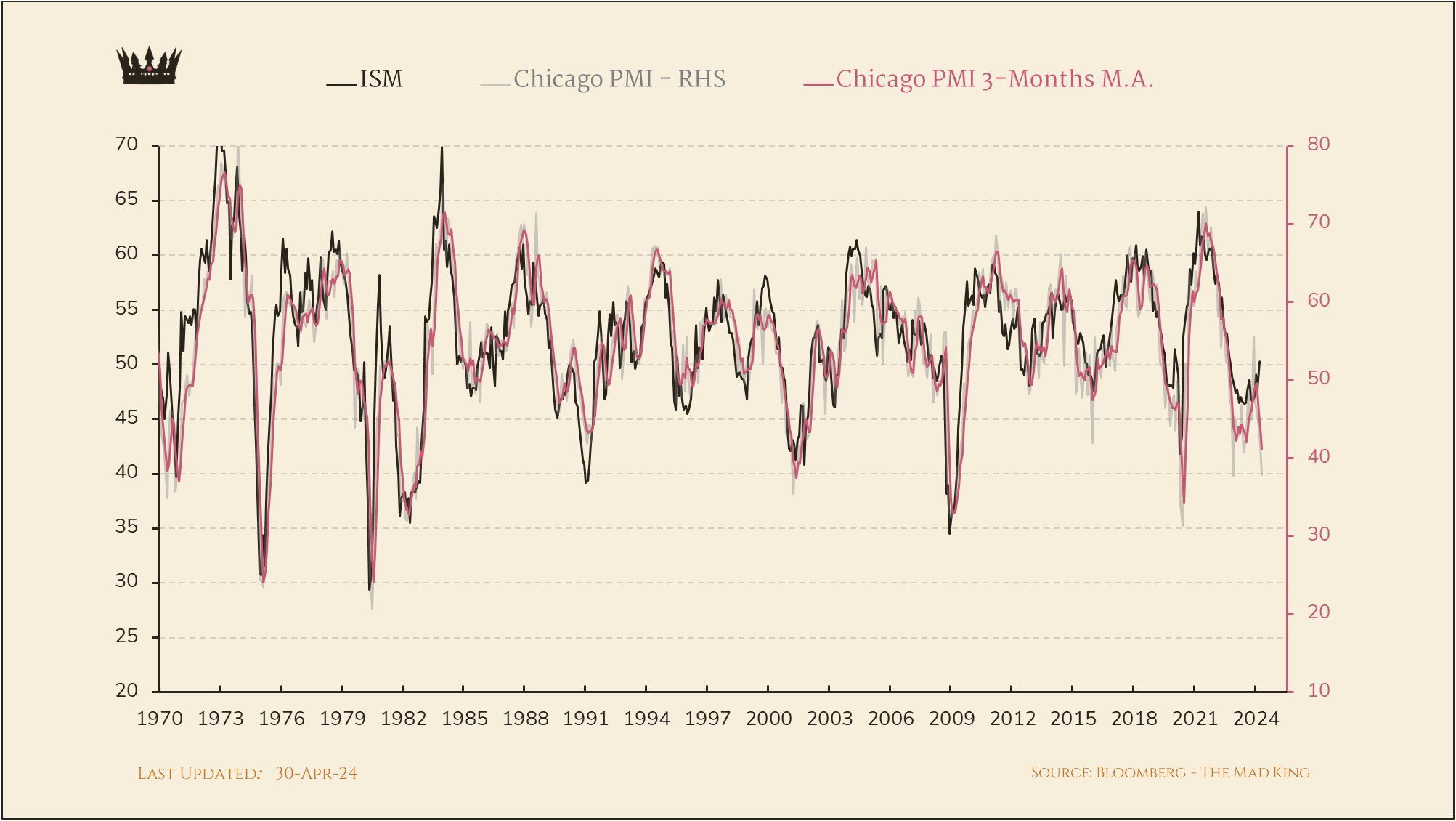

Manufacturing in the midwest, as evidenced by the well-followed Chicago PMI index, may not be recovering. While only one month of data, if the national ISM survey follows the Chicago PMI, the recent optimism that the manufacturing sector may exit an 18-month recession may fade quickly. Other than 2020, when Chicago PMI plunged for just two months during Covid and spiked back, the Chicago PMI hasn’t been this low since 2009.

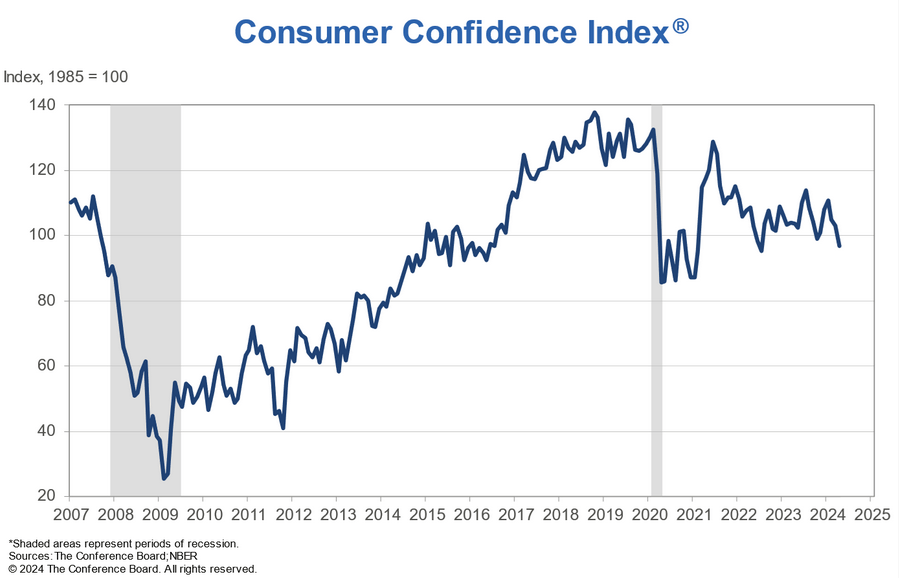

Moods are not only dour in the manufacturing sector. As the second graph shows, Tuesday’s consumer confidence survey is heading lower. Like the Chicago PMI report, consumer confidence was worse than expected. The index fell to 97.0 from a downwardly revised 103.1. The estimate was 104. Both the present situation and expectations indexes were lower. Changes in consumer sentiment often precede changes in consumer spending. Again, one month does not make a trend, but given that consumers account for two-thirds of the economy, this reading, like the Chicago PMI, cautions that the economy may slow in the coming months.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read