So, you want double-digit returns in 2022? Hold cash. Sounds crazy, I know.

Especially today with the mainstream financial media headlines and big shots like Ray Dalio, who laments how ravaged cash is due to inflation. While that is indeed true for a long-term investment portfolio to a degree, maintaining a decent cash emergency reserve and going a step further with a financial vulnerability cushion can get you to double-digit returns.

Want to see how? I’ll show you.

First, let me share a broad perspective concerning the state of household cash coffers. According to a 2021 survey from Bankrate, only 39% of Americans say they could cover an unexpected expense of $1,000. Moreover, the Personal Saving Rate, which skyrocketed to 13.1% in 2020, has retreated to 6.9% as of September 2021. Moreover, real wages, which account for inflation, have declined by 1%. Consequently, the overall state of most Americans is cash poor.

Keep in mind, the decision to hold cash is a conscious tradeoff. The reasons to have cash are as diverse as people are. For some, it’s an emotional Snuggie to smooth out portfolio volatility or ‘dry powder’ for future purchases. Perhaps, you’re an investor dependent on portfolio cash to recreate a retirement paycheck.

Regardless of your motivations, maintaining a cash position is the ultimate protection against unforeseen events, and we seem to have quite a few of them over the last decade or so. Wall Street seeks to grab every dollar we possess, so they employ entire marketing departments to pick your pockets.

Even better, they’re persuasive enough for us to pick our own pockets because they disseminate scary stories about cash vs. the inflation monster. And while cash indeed can succumb to the inflation beast, it depends entirely upon the arena in which cash fights your financial battles. In many cases, cash rises victorious.

Cash is fungible – it channels through every financial category and keeps your household functioning – Sort of like oil in an engine. Therefore, breaking down the mental accounting barriers around cash Wall Street built in your head is crucial. In many cases, cash can provide attractive returns just because it’s available, ready for the taking because you need it!

How valuable are liquidity and preservation to robust financial health? Crucial.

One: Cash provides an attractive alternative in case of emergencies.

The Personal Savings Rate has dropped precipitously since March 2020. Household cash accumulated during the pandemic is dwindling. As a result, credit card usage to service daily needs is increasing. In the case of a financial emergency, would I want cash eroded by inflation or maintain a credit card balance?

Per Bankrate.com, the current three-month trend for credit card interest rates is 16.3%, and with the Federal Funds Rate forecasted to increase at least three times this year, interest rates on credit cards will inevitably go higher as well. So isn’t it worth maintaining six months of living expenses in cash instead of turning to high-interest alternatives?

It seems like a rudimentary question, but it’s common for our brains to categorize financial decisions and make them in a vacuum. For example, some consumers maintain a credit card balance yet have cash in reserves to pay it off. Unfortunately, mental walls prevent the flow of cash to its highest and best use in some instances! One small move and double-digit returns come from holding cash and parting with it at an opportune time.

Two: Cash is an asset class and a respected addition to your portfolio.

In a portfolio strategy for retirees in the distribution stage, it makes sense to hold cash, perhaps a year’s worth. After all, periodic distribution of cash, cash flow in general, is the life’s blood of retirement.

However, what about younger investors with over a decade left to retirement? Cash is still worth a place in an accumulation portfolio. Here’s why:.’

Brokers lament – “Cash isn’t working for you! Cash will lose to inflation!” Well, there are times when cash will do just that. However, it’s the responsibility of your money manager to make portfolio adjustments. The ebb and flow of portfolios to adjust for risk is a responsibility most brokers will not undertake; therefore, they must trash cash regardless of valuations and the market’s overall health.

REMEMBER – It’s not cash forever; it’s cash for now. Can you imagine telling your broker that double-digit returns can come from holding cash?

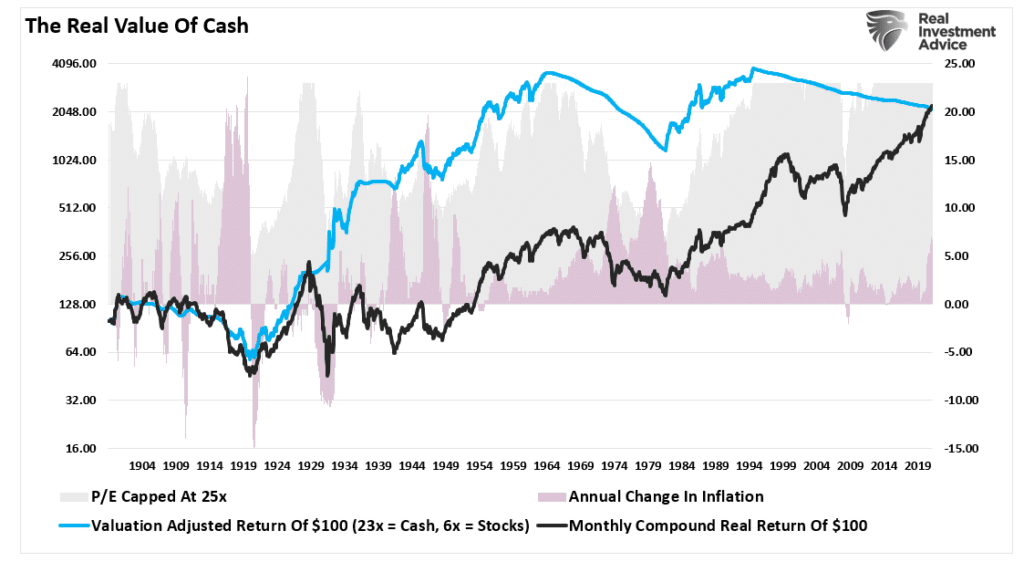

Here, RIA’s Chief Investment Strategist Lance Roberts outlines the inflation-adjusted return of $100 invested in the S&P 500 (capital appreciation only using data provided by Dr. Robert Shiller). The chart also shows Dr. Shiller’s CAPE ratio. Lance caps the CAPE ratio at 23x earnings which has historically been the peak of secular bull markets. He then conducts a simple cash/stock switching model which buys stocks at a CAPE ratio of 6x or less and moves back to cash at a ratio of 23x.

During the significant inflation of the 1970s in the United States, the value of cash experienced downward pressure. In other words, although the CAPE ratio in 1970 was roughly 23x, a switch to cash didn’t work so well, which validates the erosion of returns on cash. However, the sentiment of this chart validates the fact that holding an allocation to cash during a period of nose-bleed valuation levels is a formidable risk management tactic. As of this writing, the Shiller P/E is 39X.

An idea for a do-it-yourself investor is to maintain a minimum of 5% cash to add to opportunities slowly; I expect significant volatility in 2022 as the Fed clumsily severs its love affair with risk assets by pulling liquidity and increasing short term rates.

As Lance so eloquently states –

“While no individual could effectively manage money this way, the importance of “cash” as an asset class is revealed. While cash did lose relative purchasing power, due to inflation, the benefits of having capital to invest at lower valuations produced substantial outperformance over waiting for previously destroyed investment capital to recover.

Time frames are crucial in the discussion of cash as an asset class. If an individual is “literally” burying cash in their backyard, then the discussion of the loss of purchasing power is appropriate.

However, if cash is a “tactical” holding to avoid short-term destruction of capital, then the protection afforded outweighs the loss of purchasing power in the distant future.”

Much of the mainstream media will quickly disagree with the concept of holding cash and tout long-term returns as the reason to remain invested in both good times and bad. The problem is it is YOUR money at risk. Furthermore, most individuals lack the “time” necessary to capture 30 to 60-year return averages truly.

So, if you want double-digit returns, hold cash because it allows you to pounce on opportunities. Again, cash is an emotional salve since it smooths the overall portfolio ride. Thus cash may prevent a novice investor from bailing out of markets entirely at the absolute worst time.

Three: Cash can magnify your purchasing power.

Mark Cuban recently shared with Vanity Fair magazine that having cash can save money. In the article, he mentions how “negotiating with cash is a far better way to get a return on your investment.” A valid point. Ironically, cash provides leverage. Yet, leverage or debt places a borrower below a creditor in the financial pecking order of things.

For example, I worked with clients through the financial crisis who possessed tremendous leverage and deployed cash for real estate property offered at distressed prices because of overindebted owners. One client specifically headed to Florida and purchased four Naples and Fort Myers properties for 60 cents on the dollar because he held cash and waited for an opportunity. Today, those houses, townhomes provide robust rental income and have appreciated tremendously since early 2010.

Cash is boring; cash is not a riveting topic for cocktail party fodder.

But double-digit returns can come from holding cash.

Are you smart and patient enough to know when to release it?

Richard Rosso, MS, CFP, CIMA is the Head of Financial Planning for RIA Advisors. He is also a contributing editor to the “Real Investment Advice” website and published author of “Random Thoughts Of A Money Muse.” Follow Richard on Twitter

Customer Relationship Summary (Form CRS)