Walmart posted earnings per share of $1.30, much weaker than expectations for $1.48. While the bottom line was 23% below the same period last year, Walmart’s revenue grew 2%. Stronger sales and weaker earnings, a common theme in many recent earnings reports, is a consequence of inflation.

“Bottomline results were unexpected and reflect the unusual environment. U.S. inflation levels, particularly in food and fuel”– Walmart CEO Doug McMillon

Walmart’s CEO is not rosy about inflation falling quickly enough to save this year’s earnings. He expects net sales to increase by 4% for the remainder of the year. However, earnings per share are expected to fall by 1%, much lower than original projections in the mid-single digits. As the graph from Statista below highlights, Walmart is the world’s largest retailer. Accordingly, their results are indicative of the challenging climate facing consumers and many retail-oriented businesses. Personal consumption accounts for two-thirds of GDP!

What To Watch Today

Economy

- 7:00 a.m. ET: MBA Mortgage Applications, week ended May 13 (2.0% during prior week)

- 8:30 a.m. ET: Housing starts, April (1.757 million expected, 1.793 million during prior month)

- 8:30 a.m. ET: Building permits, April (1.817 million expected, 1.870 million during prior month)

Earnings

Pre-market

- Lowe’s (LOW) to report adjusted earnings of $3.23 on revenue of $23.81 billion

- Target (TGT) to report adjusted earnings of $3.06 on revenue of $24.34 billion

- Analog Devices (ADI) to report adjusted earnings of $2.11 on revenue of $2.84 billion

- TJ Maxx (TJX) to report adjusted earnings of 60 cents on revenue of $11.6 billion

Post-market

- Cisco (CSCO) to report adjusted earnings of 86 cents on revenue of $13.34 billion

- Bath & Body Works (BBWI) to report adjusted earnings of 53 cents on revenue of $1.44 billion

Market Trading Update – Rally Underway…Finally!

The market finally strung together a few trading days of back-to-back advances which remained a rarity since March. However, while the rally is welcome, it will quickly consume much of the “pent-up” fuel and there are a LOT of “trapped longs” needing an exit. We are still looking to use this rally in stages to reduce some high beta names, raise cash, and rebalance portfolio allocations.

The good news is that the MACD “buy signal” is very close to crossing from an extreme oversold low. So, while an initial rally to the 20-dma (red) may be short-term resistance, there is a reasonable possibility the market could rally to the 50-dma during a short-squeeze retracement.

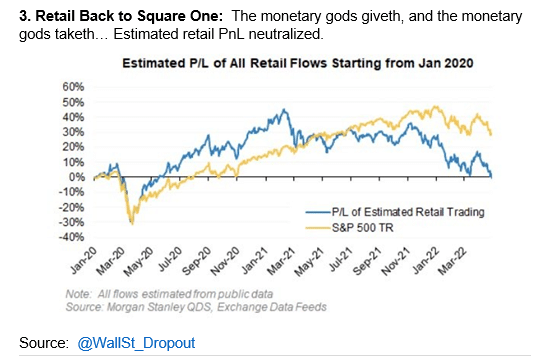

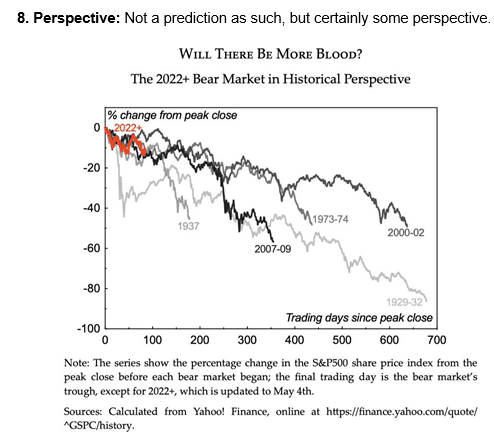

Perspective from Callum Thomas

The following two graphs from Callum Thomas provide unique insight into the recent downturn.

The graph below shows that the recent equity downturn has hurt retail investors more than the broader market indexes. Per the estimate below, retail investors are now flat since the Pandemic started. The S&P 500 is up about 30% over the same period.

The following graph puts the recent downturn into a historical perspective. If this is a bear market, it is quite possible that despite a 20% decline, it may still be in the early innings.

VIX Cycle Point to Reflexive Rally

The graph below from Nautilus Investment Research shows how dependable the 50-day cycle in the VIX volatility index has been over the last 1.5 years. Per the cycle, the VIX peaked in early May and will trough on June 9th. A period of rising or consolidating prices would likely bring the VIX down to 20ish. Further, a 2-4 week period of stability is likely, given the recent bout of volatility. This is just another tool that may help as we further rebalance into what we believe will be a reflexive bounce over the coming weeks.

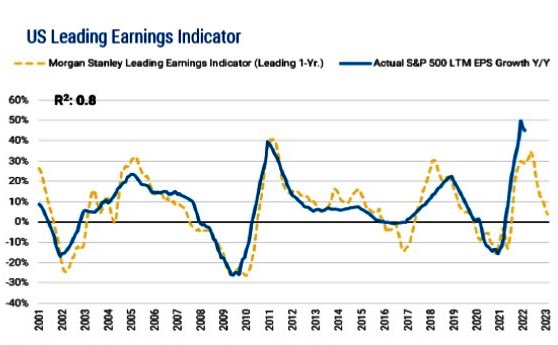

Forward P/E’s Are Cheap, They Say

We have seen numerous pundits screaming that market valuations are cheap. More often than not, they justify said comments with forward P/E valuations. The first graph below shows forward P/Es do appear fair or even cheap relative to the last eight years. The problem with this logic is how they estimate forward earnings.

Currently, S&P Global estimates earnings growth of 15% for the next four quarters. From 2012 through 2019 (pre-pandemic and post-financial crisis) S&P earnings grew by 7%. The current estimate is double the natural run rate. Now consider a distinct possibility of a recession, and inflation is crushing margins and earnings. As we wrote earlier, inflation took a big bite out of Walmart’s earnings. Walmart is the world’s largest retailer. The second graph below from Morgan Stanley shows their reliable proprietary earnings model sees the potential for zero earnings growth. Recalculate forward P/E with zero or even negative earnings growth, and forward-looking valuations are not as cheap as many think.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read