“The market seems to have gotten way out in front over this one CPI report. Everybody should just take a deep breath and calm down. We’ve got a ways to go ” -Federal Reserve Governor Christopher Waller.

After the market’s powerful reaction to CPI, investors woke to words of warning from Christoper Waller. In addition to the quote above, he added the Fed has a “long, long way to go to get inflation down.” Waller believes rate hikes will continue until inflation falls consistently over many months and nears the Fed’s 2% target. The important takeaway from Waller’s comments and Chair Powell’s FOMC press conference is the Fed has significant concerns about taking its foot off the monetary brakes too early. Waller said the worst possibility is that Fed stops raising rates and inflation reignites. Powell and Waller are looking to the 1970s and 1980s inflation outbreaks for guidance. Such a mindset leads us to believe the market may be getting ahead of itself in thinking the Fed is anywhere close to a policy pivot.

The graph circles the first two outbursts of inflation in 1968-1970 and 1973-1975. In both cases, the Fed hiked aggressively but eased equally aggressively once inflation peaked. The box covering the third instance of high inflation highlights the Fed kept Fed Funds above 10% for three years after inflation topped. Since then, Paul Volcker has preached the Fed’s extremely tight policy for an extended period, ultimately slayed the inflation problem.

What To Watch Today

Economy

- 8:30 a.m. ET: Empire Manufacturing, November (-6.0 expected, -9.1 prior)

- 8:30 a.m. ET: PPI Final Demand, month-over-month, October (0.4% expected, 0.4% prior)

- 8:30 a.m. ET: PPI Excluding Food and Energy, MoM, October (0.3% expected, 0.3% prior)

- 8:30 a.m. ET: PPI Excluding Food, Energy, and Trade, MoM, October (0.3% expected, 0.4% prior)

- 8:30 a.m. ET: PPI Final Demand, year-over-year, October (8.4% expected, 8.5% prior)

- 8:30 a.m. ET: PPI Excluding Food and Energy, year-over-year, October (7.2% expected, 7.2% prior)

- 8:30 a.m. ET: PPI Excluding Food, Energy, and Trade, YoY, October (5.6% expected, 5.6% prior)

- 9:00 a.m. ET: Bloomberg Nov. United States Economic Survey

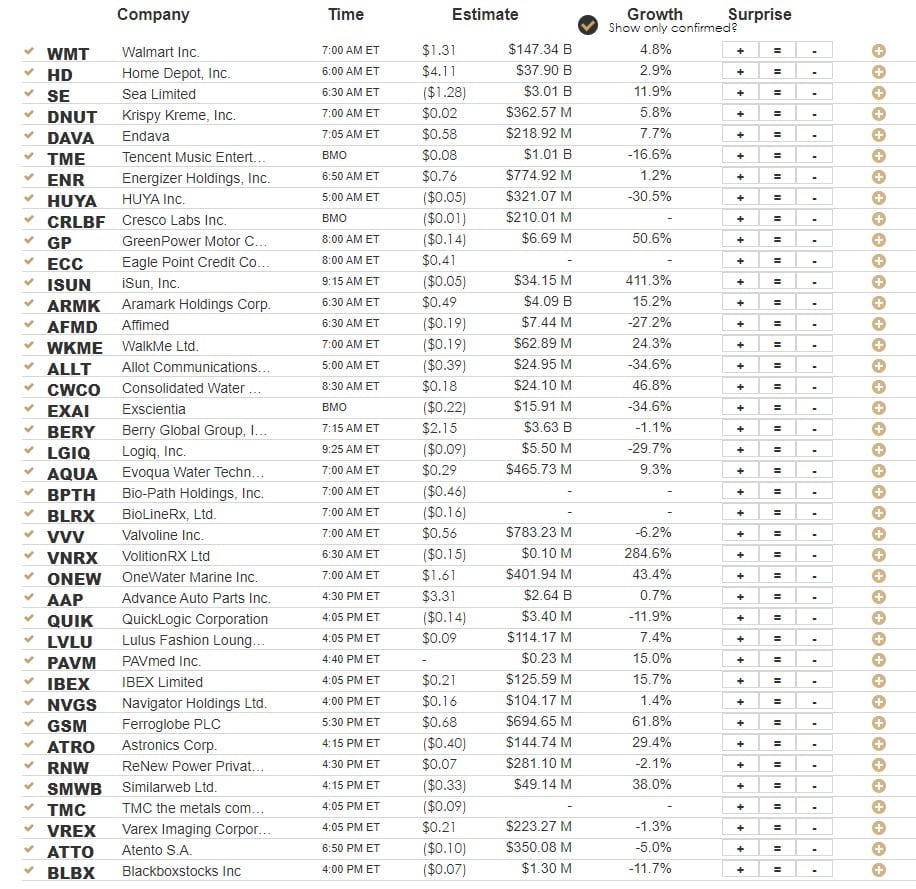

Earnings

Market Trading Update

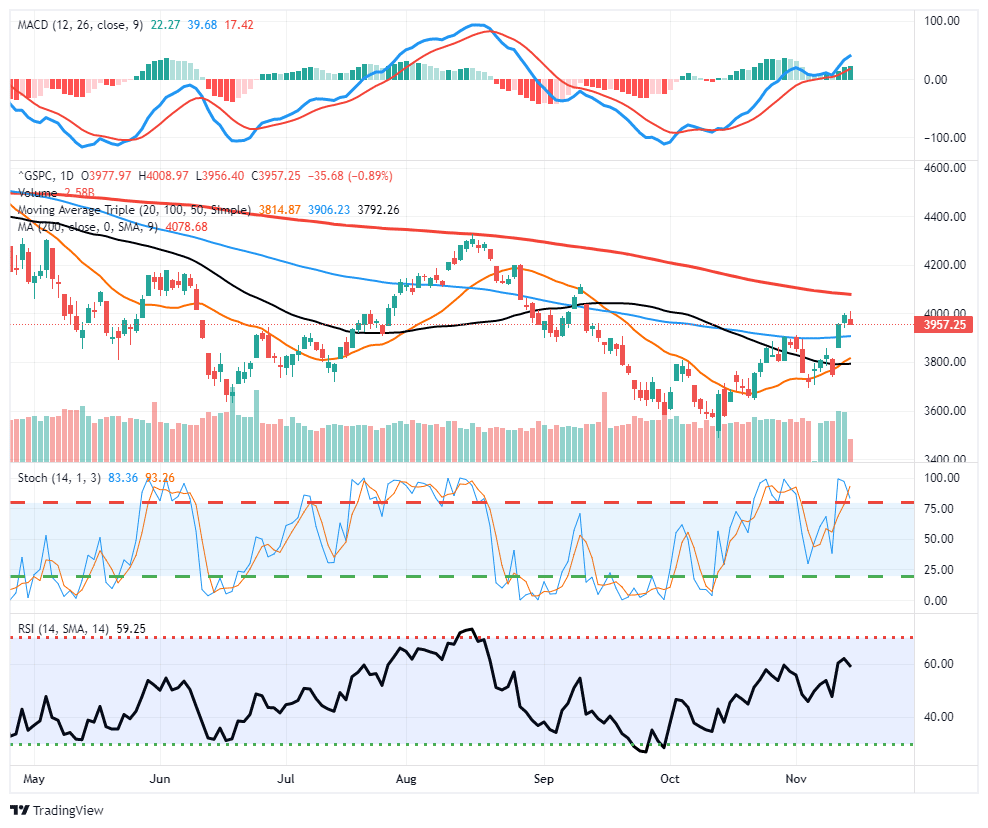

Unsurprisingly, the market traded off yesterday after a strong advance last week. The 100-dma is now important support for the market to hold. The 200-dma is important resistance. Such suggests that while there is some upside currently, it is limited, and we could see more volatile trading into the end of November.

We have recommended using the rally for the last several weeks to raise cash and reduce equity risk. We did that again yesterday by reducing equity exposure to 38% of the portfolio (our target allocation is 35%, and increasing cash to 17.5%. The rest of the portfolio is most short-duration fixed income for now. While we still expect some short-term upside to the market, we suspect next year will be challenging, at least initially, as tighter Fed policy takes effect.

Quantifying The Lag Effect

Over the years, economic activity has become increasingly reliant on debt. As evidence, the Fed’s primary monetary policy to increase or slow economic growth and inflation is the cost of borrowing money- interest rates. However, as we have been consistently warned, Fed policy changes take a long time to fully affect the economy.

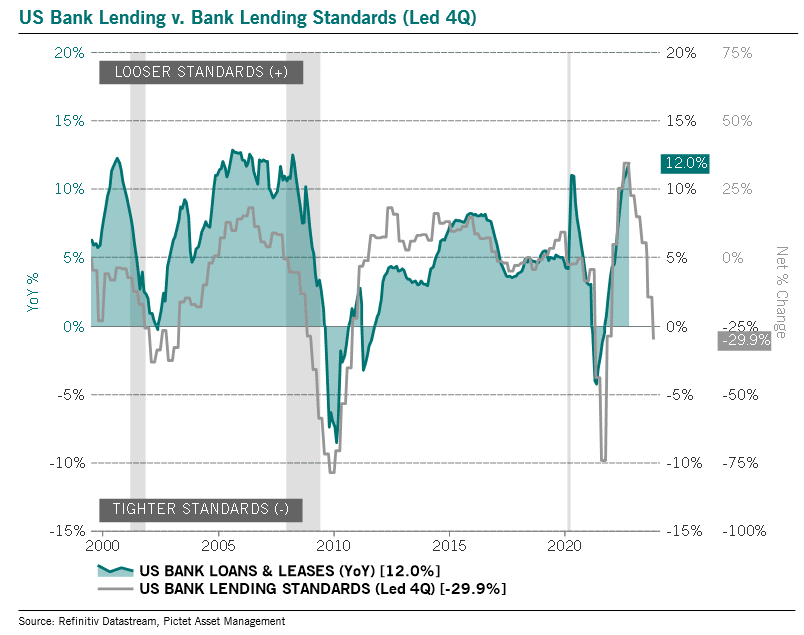

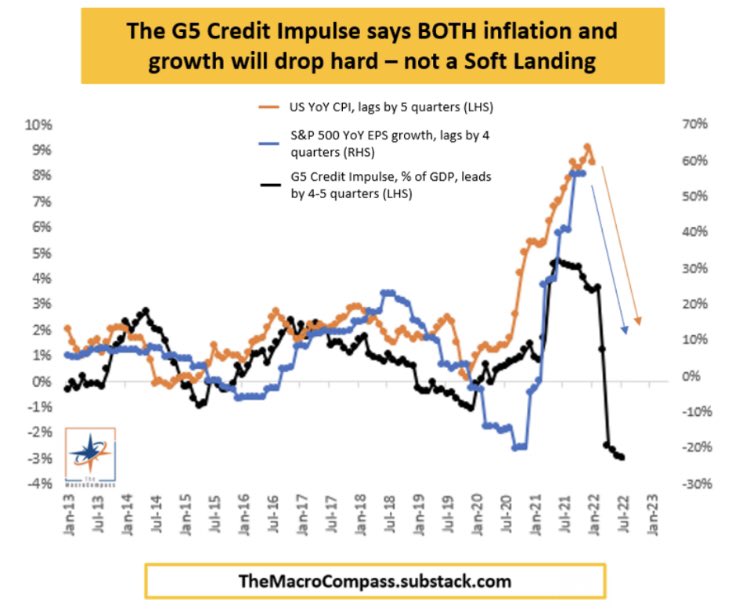

The graph below from Pictet Asset Management provides strong evidence that the lag time between interest rate changes and economic activity may be as long as four quarters. It shows it can take a year before actual bank lending reacts to tighter or looser bank lending standards. The second graph below from MacroCompass similarly shows it takes four to five quarters for a decline in credit conditions to weigh on inflation and earnings growth.

The Fed started aggressively raising rates about a year ago, when bank lending standards tightened. As such, we should expect lending, the gasoline fueling economic growth, will slow significantly in the coming months.

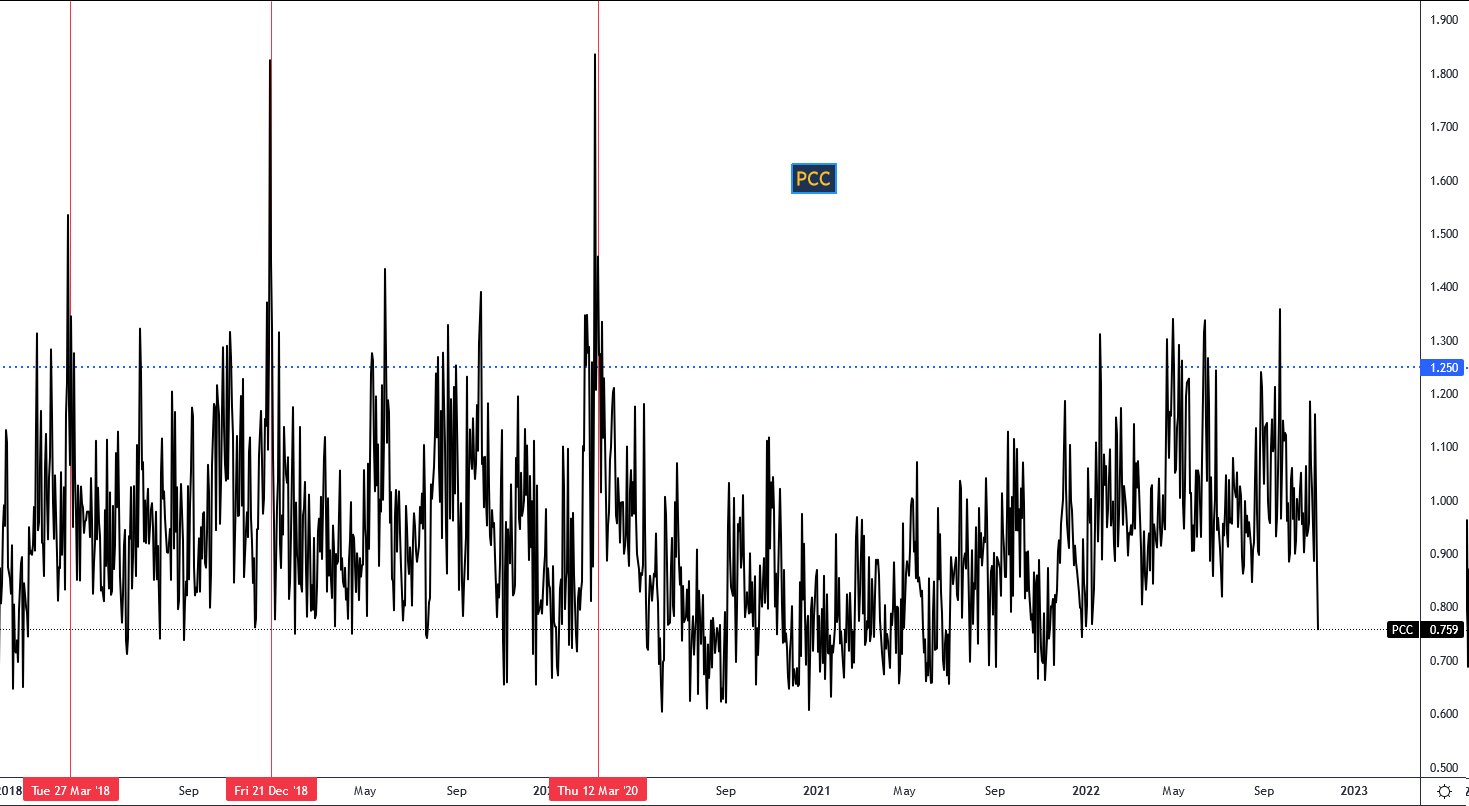

Put Call Ratio Hits 2022 Lows

The put-call ratio (number of puts as a ratio to the number of calls) is trading at a 2022 low. Viewing this through a bullish lens may provide relief that positive sentiment is finally returning to markets. The bearish camp would counter it signals investors are too complacent and ignoring the plethora of macroeconomic and liquidity risks. Unlike in 2021, when the ratio was very low, today, the volatility index (VIX) remains well above levels seen throughout most of 2021. Are we in a regime change, or are investors getting ahead of themselves?

Crypto and Liquidity

The recent FTX news should raise deep concern for crypto investors. Your assets are only as good as the custodian of said assets. The FTX event calls into question the infrastructure backing how many investors hold crypto assets.

For non-crypto investors, there is also an important takeaway. Changes in liquidity are often most appreciable in the riskiest asset classes. As we saw with Bernie Madoff and Jon Corzine, removing liquidity often uncovers fraud and unsustainable market schemes. While we are not overly concerned the FTX crisis will infect more traditional asset markets, we harbor concerns that the instance highlights that QT and higher rates are slowly taking liquidity from the markets. In time, the lack of liquidity, if it continues, will likely creep into the stock market.

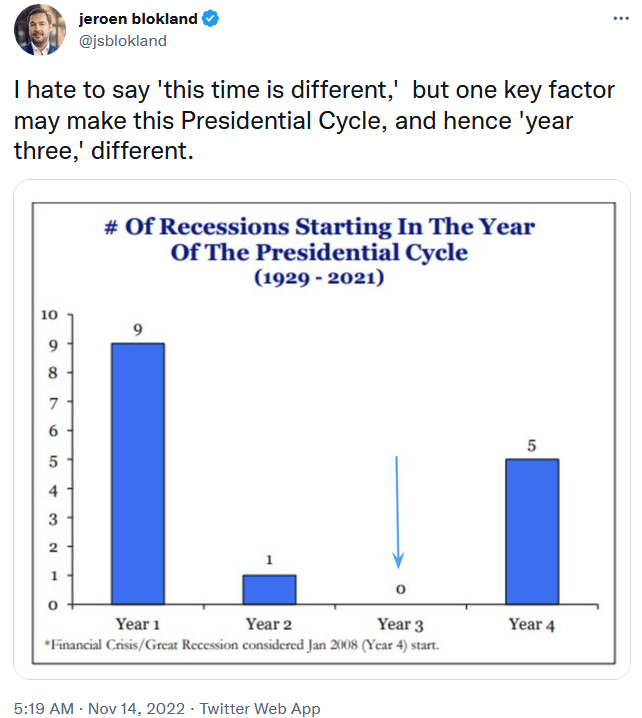

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read