The yield on the benchmark 10-year Treasury is approaching 2%. The last time 10-year Treasury yields were above 2% was in January 2020. Since the Pandemic, the U.S. Treasury has added close to $7 trillion in debt while non-financial corporations added over $1 trillion. The $8 trillion of new debt is almost 4x the economic growth achieved over the two years. With a rising debt to GDP ratio comes more sensitivity to higher yields. Stock investors are not blind to this fact. If the 10-year U.S. Treasury yield eclipses 2%, we will likely see investors getting a little more anxious. This is the last thing we need with the Fed set to raise rates in March.

What To Watch Today

Economy

- 6:00 a.m. ET: NFIB Small Business Optimism, January (97.5 expected, 98.9 in December)

- 7:00 a.m. ET: MBA Mortgage Applications, week ended Feb. 4 (12% prior week)

- 8:30 a.m. ET: Trade Balance, December (-$83.0 billion expected, -$80.2 billion in November)

Earnings

Pre-market

- 6:00 a.m. ET: Centene Corp. (CNC) to report adjusted earnings of $0.97 on revenue of $32.52 billion

- Pfizer (PFE) to report adjusted earnings of $0.88 on revenue of $24.17 billion

- KKR & Co. (KKR) to report adjusted earnings of $1.20 on revenue of $2.00 billion

- Coty Inc. (COTY) to report adjusted earnings of $1.11 on revenue of $1.61 billion

- Harley-Davidson (HOG) to report an adjusted loss of $0.32 on revenue of $674.54 million

- Warner Music Group (WMG) to report adjusted earnings of $0.28 on revenue of $1.51 billion

- S&P Global Inc. (SPGI) to report adjusted earnings of $3.13 on revenue of $2.05 billion

Post-market

- 4:10 p.m. ET: Chipotle Mexican Grill (CMG) to report adjusted earnings of $5.28 on revenue of $1.96 billion

- Lyft (LYFT) to report adjusted earnings of $0.09 on revenue of $940.42 million

- Corsair Gaming (CRSR) to report adjusted earnings of $0.25 on revenue of $396.00 million

- Peloton (PTON) to report an adjusted loss of $1.17 on revenue of $1.14 billion

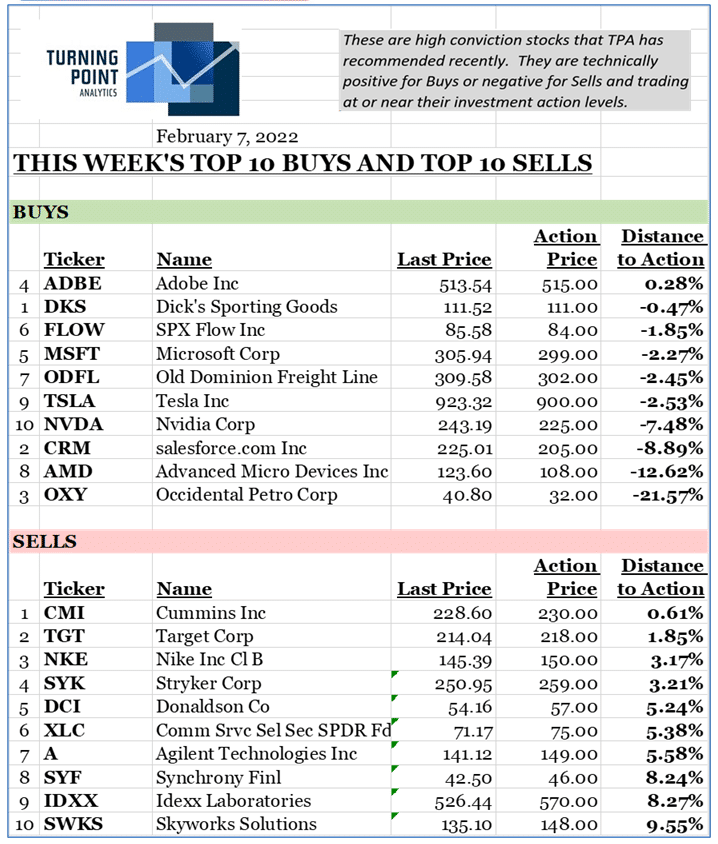

TPA Research Top 10-Buys & Sells

Click on RIAPro+ today to add TPA Research to your subscription for just $20/month.

Liquidity is Lacking

The graph below from the Financial Times/Goldman Sachs shows that stock market liquidity, as measured by the e-mini S&P 500 futures, has been declining for the better part of the last six months. The S&P 500 futures market is now approaching liquidity levels last seen during the Covid market meltdown in mid-March 2020. With the Fed discussing raising rates and reducing its balance sheet, we raise concern that liquidity will dwindle further. The sharp up and down market gyrations of the last few weeks may be with us for a while.

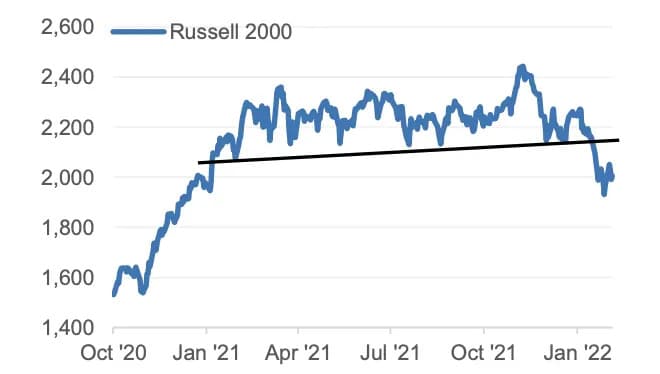

The Russell Sends A Clear Warning

“The Russell 2000 has lagged the S&P 500 by 25 percentage points in the past 12 months, its worst 12-month relative return since 1999.

Decelerating GDP growth has been one headwind to the cyclical small-cap index. During the last 20 years, small-caps have lagged on average in periods when the yield curve was flattening, economic growth was strong but decelerating, or financial conditions were tightening,” David Kostin, Goldman Sachs via Yahoo Finance

Small caps are highly sensitive to changes in inflation, treasury yields, and economic growth as they don’t have the cash flows to offset weaker demand. The Russell 2000 is a good leading indicator of economic weakness.

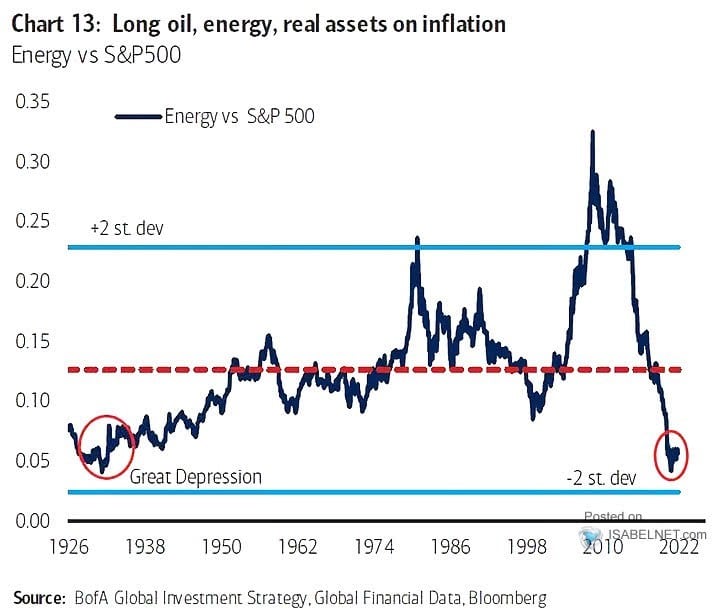

Energy Stocks are on Fire

The graph below shows the excess return by sector versus the S&P 500 normalized to a per-day basis. Over the four periods we show below, the energy sector is grossly outperforming every other sector and the S&P 500. Over the last 35 trading days, it is beating the S&P 500 by nearly 1% per day on average.

While short-term technical analysis points to increasing odds of consolidation or a decline on both a relative and absolute basis, the chart below, courtesy of the Daily Shot, shows the energy sector has plenty of room to run relative to the S&P 500.

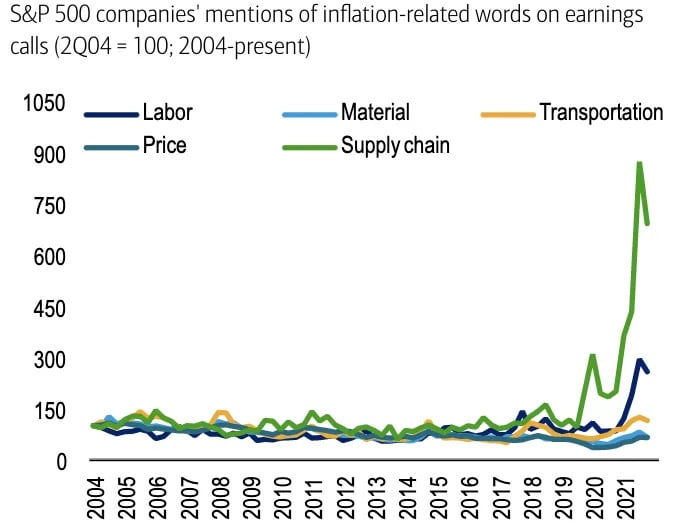

Disinflation In Earnings Announcements

If there is any positive in what has been a decidedly mixed earnings season, it’s that companies are complaining less about supply chain bottlenecks as the chart from Bank of America’s Savita Subramanian shows below. But don’t start jumping for joy that this suggests supply chains are back to any form of normal. ‘Companies have mentioned supply chain and labor less than they did in 4Q, but we believe it is merely because it has been well-telegraphed by now, not because of a change in underlying trend, as many companies expect a bigger inflation headwind in 1Q than 4Q.” – Yahoo Finance

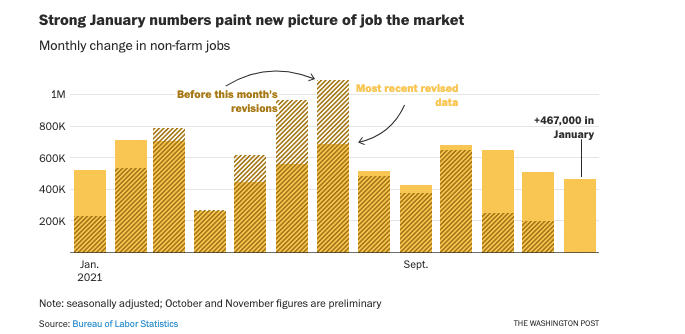

Massive Labor Market Revisions

In Monday’s Commentary, we wrote- “More impressive, December and November data was revised upward by a total of 709k. Such a significant revision is unprecedented.” The graph below from the Washington Post puts the December and November revisions in context. As we show, the downward revisions in May, June, and July were equally significant. The enormous changes leave the annual number close to where it was before revisions. We caution reading too much into the BLS data due to the revisions and odd pandemic-related seasonal adjustments. We suggest using 3-month running averages of the BLS and ADP data to form more accurate opinions about the state of the labor markets.

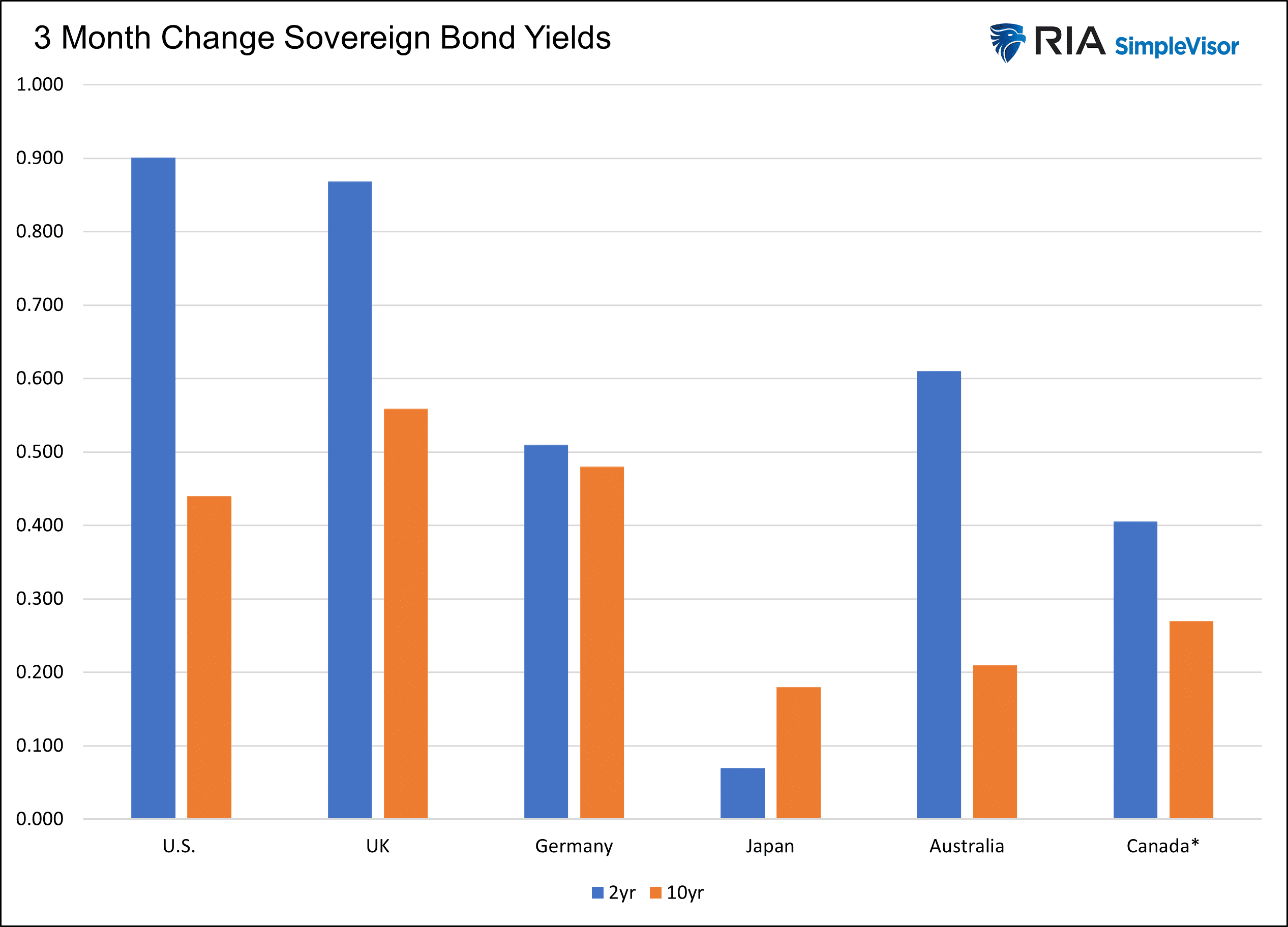

Global Yields Rising

Over the last few months, U.S. bond yields have been on the rise. In just three months, the 2-year Treasury note yield is up nearly 1% and the ten-year up almost .50%. U.S. short-term rates have risen the most compared to other countries shown below as it is believed the Fed will be the most aggressive central bank regarding removing crisis level stimulus. The Fed was the most aggressive with stimulus, so the bond market’s logic makes sense. Germany and Japan still have negative 2-year rates, but their 10-year rates are now above zero percent. Other than Japan, the 2-year note has risen more than the 10-year note, indicating the treasury yield curves for most countries are flattening. *For Canada, we use the 3-year rate as we could not find the 2-year note.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

Also Read