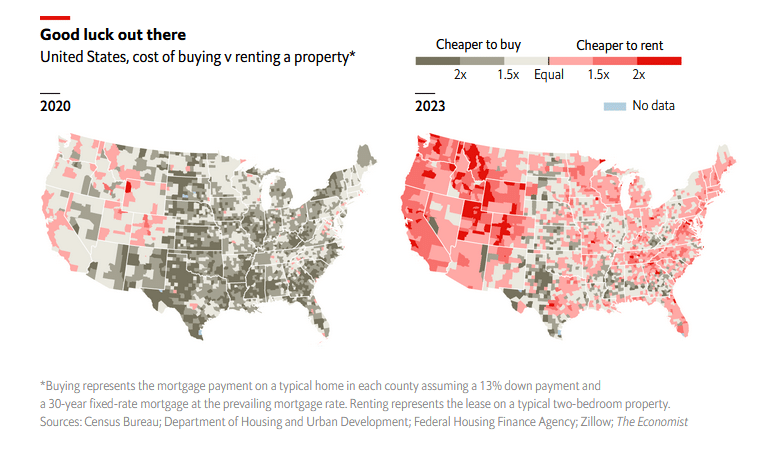

The Economist published an article entitled Is It Cheaper To Rent Or Buy Property? It shows how the financial decision of buying versus renting has drastically changed due to the fiscal and monetary response to the pandemic. With massive stimulus came inflation and higher mortgage rates. Typically, higher mortgage rates result in lower home prices. However, like most things in the last few years, house prices defied normal behaviors. However, they have recently stabilized. Existing home sales are now at the same levels as in the spring of 2020, when many buyers and sellers were scared to leave their houses, let alone make important financial decisions, such as buying or selling a house. The result is a drastic change in the financials of renting versus buying a home.

In a rarity, renting is now cheaper than buying a home. Since January 2020, the Case-Shiller National Home Price Index is up 44%. Over the same period, the Zillow Observed Rent Index is up 31%. It is not just the increase in home prices making homeownership more expensive than renting. Higher mortgage rates are also a problem. Based on average home prices and the 4+% spike in mortgage rates, the mortgage payment on many homes has doubled. Not surprisingly, renting is now cheaper in many parts of the country. Per the Economist: “By our reckoning, house prices would have to tumble by one-third, average mortgage rates would have to fall to 3.2%, or rental costs would have to rise by at least 50%.“

What To Watch Today

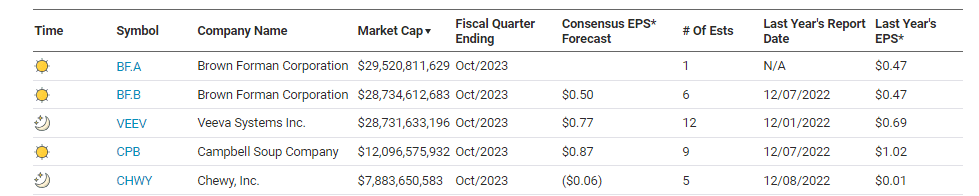

Earnings

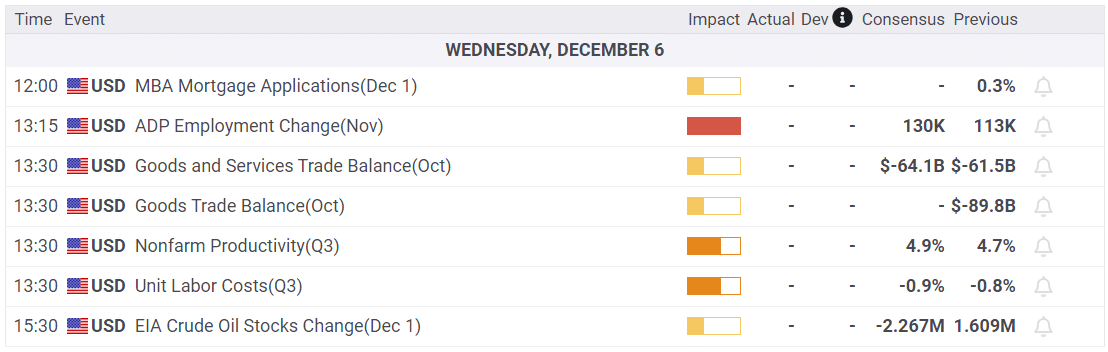

Economy

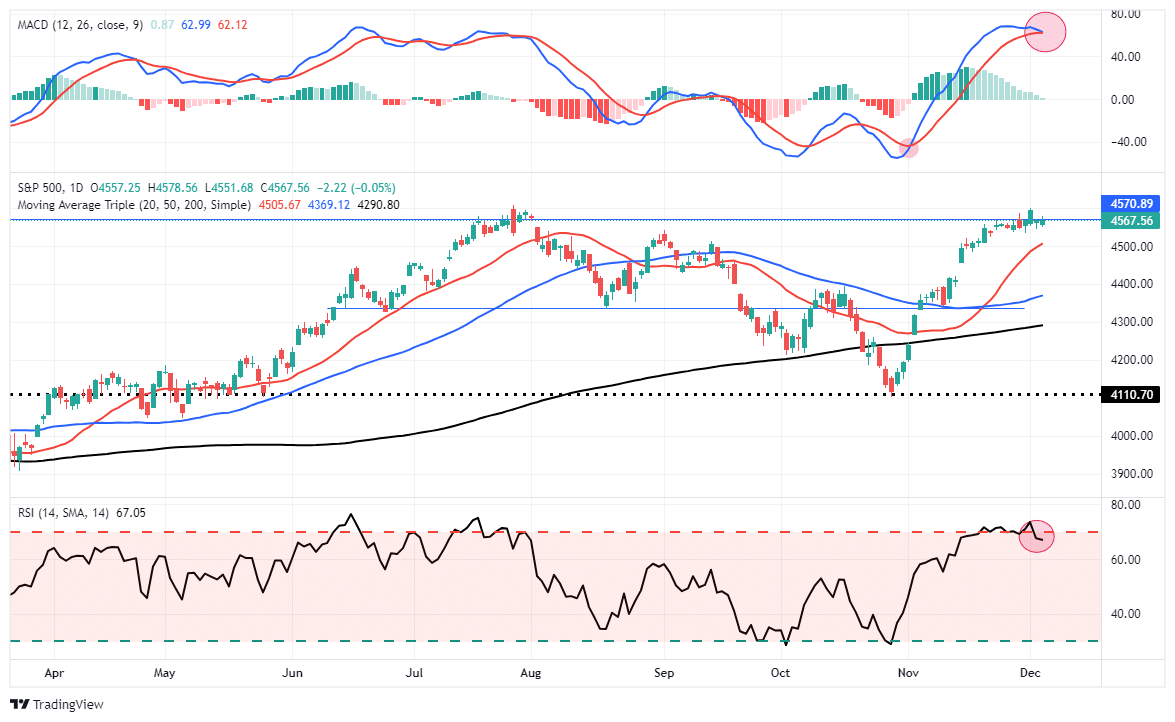

Market Trading Update

There is no real change from yesterday, as the market continues to trade flat over the last few days. Despite the one-day pop to the previous year’s highs, the market has gone nowhere since the last week of November. The good news is that buyers continue to remain present, keeping sellers at bay for now. The market remains overbought, and we are very close to triggering a MACD sell signal, which should signal weaker prices over the next week or so. Remain cautious for now and continue rebalancing risks accordingly.

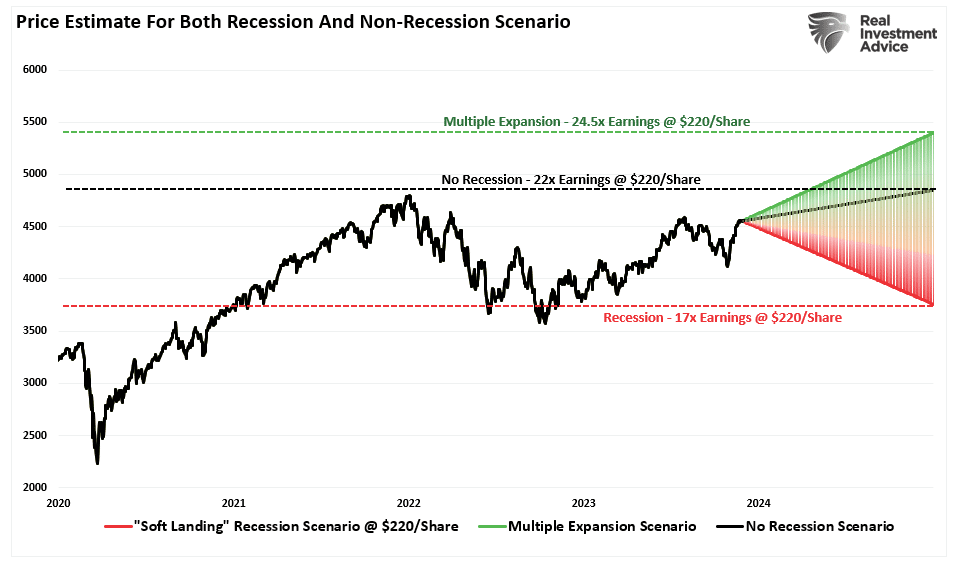

2024 S&P 500 Estimates

Our latest article, Wall Street Analysts Are Optimistic For 2024, looks ahead to what we can expect in 2024. Based on a MarketWatch survey of nine of the largest Wall Street banks and brokers, the average estimate for a 2024 end-of-year S&P 500 target is 4836. Such entails a 6% gain. The article notes that the problem with the optimistic forecasts is that they are predicated on 20% earnings growth. To sustain such a higher-than-average earnings growth rate, the following factors must exist:

The problem with current forward estimates is that several factors must exist to sustain historically high earnings growth. Per the article:

The problem with current forward estimates is that several factors must exist to sustain historically high earnings growth.

- Economic growth must remain more robust than the average 20-year growth rate.

- Wage and labor growth must reverse to sustain historically elevated profit margins, and,

- Both interest rates and inflation must reverse to very low levels.

While such is possible, the probabilities are low, as strong economic growth can not exist in a low inflation and interest-rate environment. More notably, if the Fed cuts rates, as most economists and analysts expect next year, such will be in response to a near-recessionary or recessionary environment. Such would not support current strong earnings estimates of $220.24 per share next year.

The article forecasts a 6.5% return in a “NO-recession scenario.” But it cautions: “However, should the economy slip into a mild recession, valuations would be expected to revert toward the longer-term median of 17x earnings. Such would imply a level of 3744 or roughly a 17% decline next year.” If the bulls are correct and earnings grow at 20%, the economy avoids a recession, and valuations are static, an 18.5% gain is possible. The range of outcomes is graphed below.

Food for thought: the average return under the three scenarios is about 6-7%. High-quality corporate bonds yield 5% or more, and risk-free Treasury bonds yield about 4.25%. The decision to buy equities versus bonds is much harder today than a few years ago when rates were near zero.

Preview of the BLS Employment Report

October JOLTS job openings fell sharply to 8.7mm versus estimates of 9.3mm. The prior month was revised lower from 9.53mm to 9.35mm. The quits rate stayed constant at 2.3%, which is where it stood on the eve of the pandemic. The hiring rate continues to decline. It is now at +0.2%, a level consistent with an unemployment rate of around 4.5%. While the data shows weakening, layoffs remain at 1%, below the 1.4% pre-pandemic average (2000-2019).

The mixed data certainly points to the continued normalization of the labor market. However, there is not enough in the JOLTS data to conclude anything more troubling.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read