Now boys don’t start to ramblin’ round

On this road of sin are you sorrow bound

Take my advice or you’ll curse the day

You started rollin’ down that lost highwayHank Williams.

On the road to personal financial milestones, investors aspire to reach multiple destinations that are important to them – whether it’s saving for a college education or retirement, we all seek to assess travel risks, regularly track progress and hope to avoid hazardous conditions.

We all long to -cheer – “I have arrived!”

However, there is imminent danger on the path to our destinations; like a low fog that hangs heavy, there are forces out there which blind and misdirect investors from the major road onto a lost highway. Unfortunately, obstacles to wealth are created by Wall Street, mainstream financial pundits and the social media they employ as a conduit of misinformation. And investors? You’re not off the hook. Your emotions are going to facilitate a major portfolio accident.

As I prepare framework for a screenplay “Lost Highway,” titled after a song written by Hank Williams, Sr., I gravitate to the Johnny Horton version which is slower, more haunting. Consider the ‘Lost Highway’ one of regret and foreboding, a weigh station between life and death, certainty and the unknown. Singer Johnny Horton, a spiritualist, knew for certain his demise was imminent and and it would be tragic. On November 5, 1960; at 2 am on a bridge in Milano Texas, Mr. Horton’s premonition became an unfortunate reality. More on that story later.

For now, it’s important for readers to navigate their own financial life highway and avoid the diversions which grow larger, deeper, as this bull market rages on.

As investors, let’s attempt to navigate away from these 3 financial potholes, shall we?

1 – As a retail investor, I’d avoid Twitter.

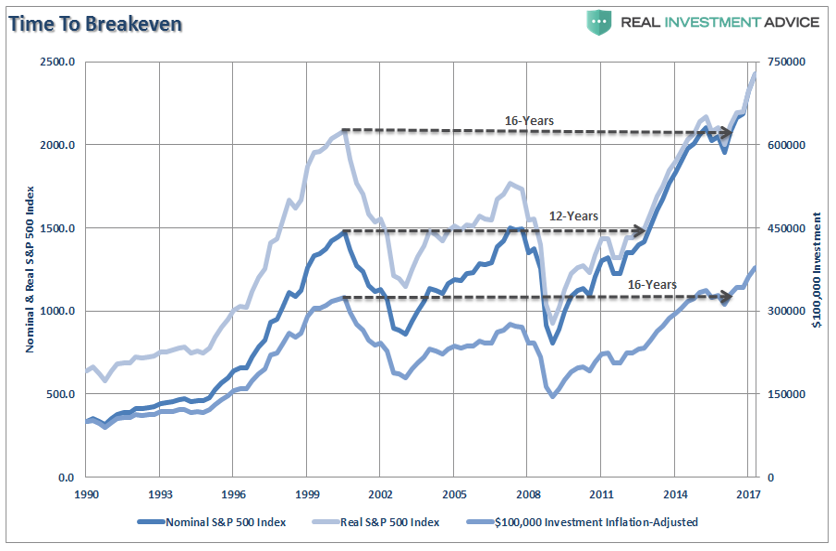

It’s called ‘FinTwit.’ A lost highway where financial experts who appear to know everything pat each other on the backs with joyous volleys of endless-scrolling bon mot. Most of these Twitter folk were running around the house in their Underoos during the last bear market or blew up portfolios during the financial crisis and conveniently chose to forget it because market recovery cures all ills – except for yours of course, because time is more valuable than money.

I mean, why not? The market recovery gave many advisors and big-box financial retailers a free pass. Of course, markets recover, don’t they? Sure they do. If you’re willing to wait a decade or so to break even. In the span of a human life, lots of events occur, lots of hair is lost, lots of wrinkles, lots of wealth stagnates over the years. The stock market is the Dorian Gray of money and the Twitter Twits believe you, as a human, have the lifespan of a vampire.

Let me show you.

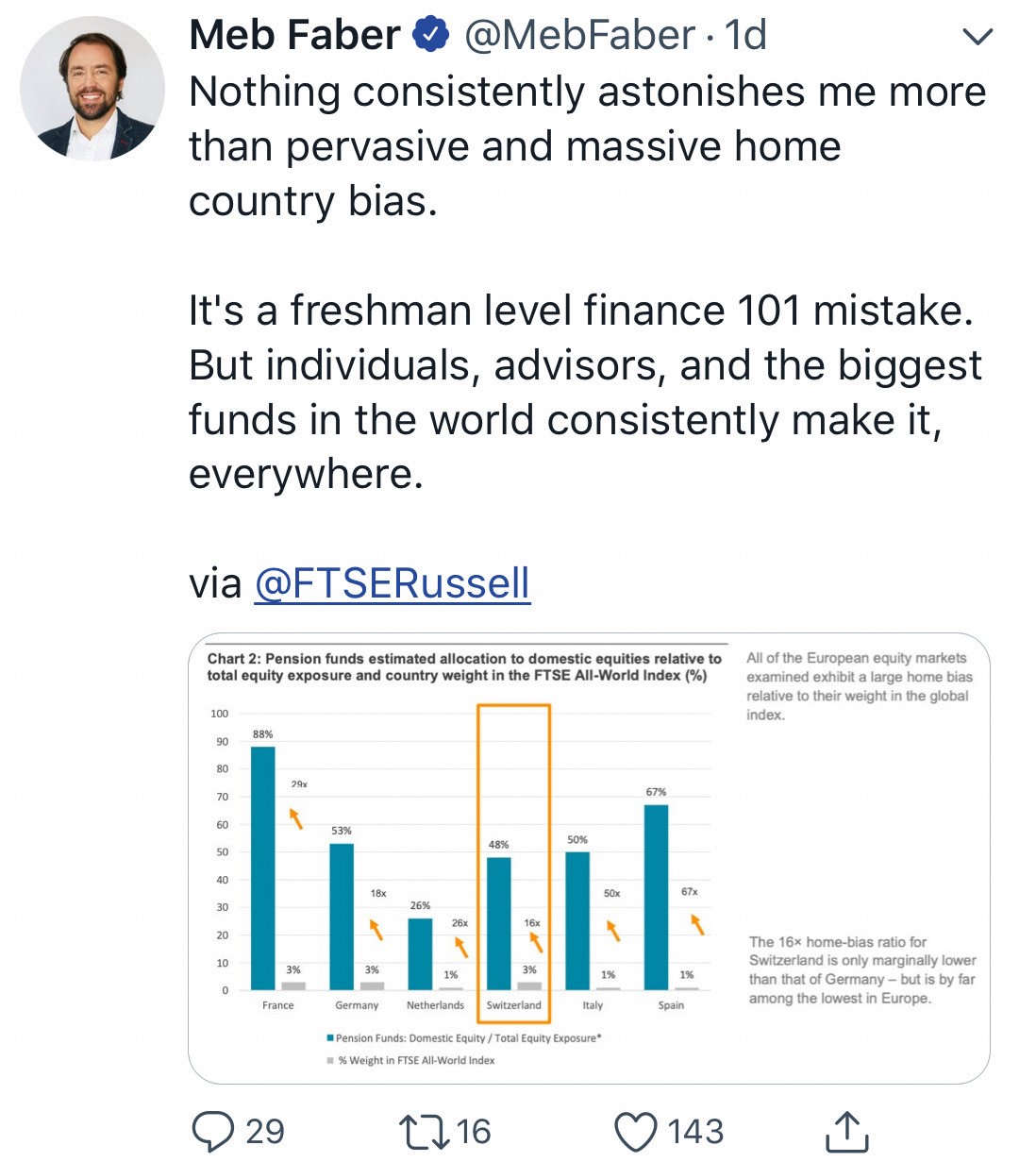

Nothing wrong with Meb; he’s a very academic, smart guy. I like his work. I understand why he shared this tweet. But as my grandfather would say – OOFA! We’re being shamed as advisors for limited exposure to international stocks. I get it. It’s a big world out there. Most investors – professionals and novices – will never seek to invest outside their borders. And that’s a bad idea.

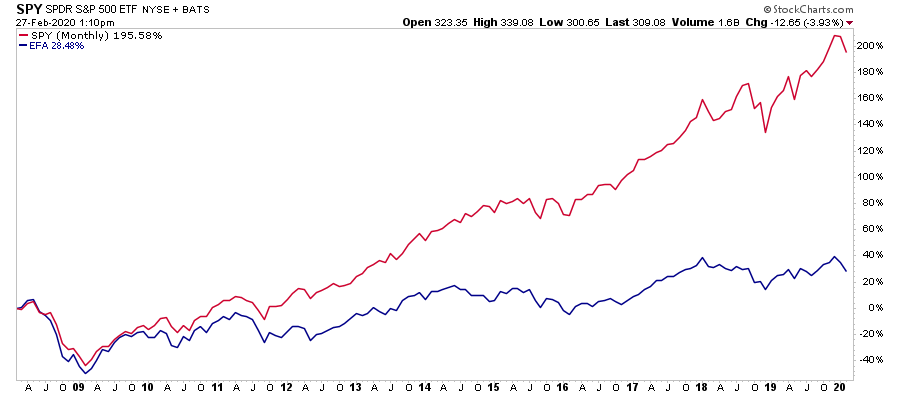

It’s a formidable, worldwide issue deemed Home Country Bias. However, over the last decade it’s been a fruitful endeavor for U.S. advisors and investors to diversify mostly among U.S. stocks. International money managers should have, in hindsight, been overweight in overseas or U.S. stocks. Home-based bias has cost them. The EliteTwits would scoff at me for writing this (not that I care), – I do not see a reason to invest in an asset class that underperforms for extended periods. I don’t find it of value to be diversified at all or at the least, greatly exposed to dormant asset classes just to ‘spread the risk.’

Diversification can indeed minimize specific company risk. If the majority of retail investors owned individual stock portfolios and sought to own ‘oil’ and ‘bleach’ in their portfolios from various countries, diversification from an unsystemic perspective would be effective. After all, if oil stocks falter, it’s most likely food & beverage stocks are thriving or at the least, not faltering as hard as non-cyclical stocks. Anybody you know still own individual stocks? Bueller? Heck, they don’t even split anymore.

Most investors today are encouraged to buy baskets of stocks through index funds or their exchange-traded brethren. So, if I own an investment that represents the S&P 500 and the MSCI EAFE Index i.e; international stocks, and one underperforms for an extended period of time, well then, why do I need to own it? Because mainstream financial media tells me so?

You must understand what diversification is and most crucial, what it isn’t. Certainly, it’s not the panacea it’s communicated to be. There’s no ‘free lunch,’ here, although I continue to hear and read this dangerous adage in the media and on Twitter. The word gets thrown around like a remedy for everything which ails a portfolio. It’s the industry’s ‘catch all’ that can lull investors into complacency, inaction.

So, who buys into this free lunch theory, again? After all, what is free on Wall Street? Investors who let their guard down, buy in to the myth of free lunches on Wall Street, find their money on the menu.

Due to unprecedented central bank intervention, there exists extreme distortion in stock and bond prices. Global risk-averse investors have purchased bonds with a voracious appetite. The odds of negative rates even at least briefly, can manifest here in the states. As I’ve lamented on the radio show in December and January – domestic interest rates will be lower in 2020.

A way to effectively manage risk has morphed into two disparate perceptions. The investor’s definition of diversification and that of the industry has parted, leaving an asset allocation plan increasingly vulnerable.

Today, the practice of diversification is Pablum. Watered down. Reduced to a dangerous buzzword.

What is the staid mainstream definition of diversification?

According to Investopedia – An internet reference guide on money and investments:

- Diversification strives to smooth out unsystematic risk events in a portfolio so the positive performance of some investments neutralizes the negative performance of others. Therefore, the benefits of diversification hold only if the securities in the portfolio are not perfectly correlated.

- Diversification benefits can be gained by investing in foreign securities because they tend to be less closely correlated with domestic investments. For example, an economic downturn in the U.S. economy may not affect Japan’s economy in the same way; therefore, having Japanese investments gives an investor a small cushion of protection against losses due to an American economic downturn.

Now let’s break down the lunch and examine how free it is.

Unsystematic risk – This is the risk the industry seeks to help you manage. It’s the risks related to failure of a specific business or underperformance of an industry.

To wit:

- This is a company- or industry-specific hazard that is inherent in each investment. Unsystematic risk, also known as “nonsystematic risk,” “specific risk,” “diversifiable risk” or “residual risk,” can be reduced through diversification.

- So, by owning stocks in different companies and in different industries, as well as by owning other types of securities such as Treasuries and municipal securities, investors will be less affected by an event or decision that has a strong impact on one company, industry or investment type.

So, think of it this way: A ‘diversified’ portfolio represents a blend of investments – stocks, bonds for example, that are designed to generate returns with less overall business risk. While this information is absolutely valid, the financial industry encourages you to think of diversification as risk management, which it isn’t.

Here’s what you need to remember:

Bleach (consumer staples) and oil (consumer cyclicals) eventually all run down-hill, in the same direction in corrections or bear markets.

Sure, ketchup or bleach may run behind, roll slower, but the direction is the one direction that destroys wealth – SOUTH. Large, small, international stocks. Regardless of the risk within different industries, stocks move together (they connect in down markets).

Consider:

What are the odds of one or two companies in a balanced portfolio to go bust or face an industry-specific hazard at the same time?

What’s the greater risk to you? One company going out of business or underperforming or your entire stock portfolio suffers losses great enough to change your life, alter your financial plan.

You already know the answer.

Diversification is not risk management, it’s risk reduction.

- When your broker preaches diversification as a risk management technique, what does he or she mean?

- It’s not risk management the pros believe in, but risk dilution.

- There’s a difference. The misunderstanding can be painful.

To you, as an investor, diversification is believed to be risk management where portfolio losses are controlled or minimized. Think of risk management as a technique to reduce portfolio losses through down or bear cycles and the establishment of price-sell or rebalancing targets to maintain portfolio allocations. Consider risk dilution as method to spread or combine different investments of various risk to minimize volatility.

Even the best financial professionals only consider half the equation. Beware the lamb (risk management) in wolf’s clothing (risk dilution). The goal of risk dilution is to “cover all bases.” It employs vehicles, usually mutual funds, to cover every asset class so business risk can be managed. The root of the process is to spread your dollars and risk widely across and within asset classes like stocks and bonds to reduce company-specific risk.

There’s a false sense of comfort in covering your bases. Diversification in its present form is not effective reduce the risk you care about as an individual investor – risk of loss.

Today, risk dilution has become a substitute for risk management, but it should be a compliment to it. Risk dilution is a reduction of volatility or how a portfolio moves up or down in relation to the overall market.

Risk dilution works best during rising, or up markets as since most investments move together, especially stocks. Think about betting on every horse in a race.

- In other words, a rising tide, raises all boats.

So, why is risk reduction not risk management, the prevailing sentiment?

Sales Goals: Most financial pros are saddled with aggressive sales goals. Risk dilution is a set and forget strategy. Ongoing risk management is time consuming and takes time away from the selling process. Unfortunately, the financial industry as a whole, has watered it down and broadened it to such a degree it’s become absolutely ineffective as a safeguard against losses. One reason are the sales targets that force financial representatives to spend less time with client portfolios.

Compliance Departments: A targeted diversification strategy places accountability on the advisor and poses risk to the firm. A wider approach makes it easier to vector responsibility to broad market ‘random walks’ so if a global crisis occurs and most assets move down together, an advisor and the compliance department, can “blame” everything outside their control. Here’s a perfect compliance department question: “so why isn’t this investor allocated appropriately to international stocks?” Appropriate for whom?

At RIA, we monitor global trends. We don’t believe investors need to participate in an asset class that’s been out of favor for over ten years. That doesn’t mean we won’t; it means our exposure has been minimal. That stance can change at any time. I mean, isn’t that what your advisor is supposed to do? The average investor holding period is less than two years. So imagine attempting to convince most investors to sit on poor performance for longer than decade. In the trenches, it’s never gonna happen.

I have hundreds of examples of Twitter commentary. that will send you down a Lost Highway. To repeat, my advice to retail investors: Please avoid the medium. It’s generally unhealthy for your psyche. Yes, we’re on Twitter too because we need to be. Avoid our feed too. Follow and read the blog instead.

2 – Avoid an ‘accumulation’ mindset if you’re five years or sooner from retirement, or you may never exit the Lost Highway.

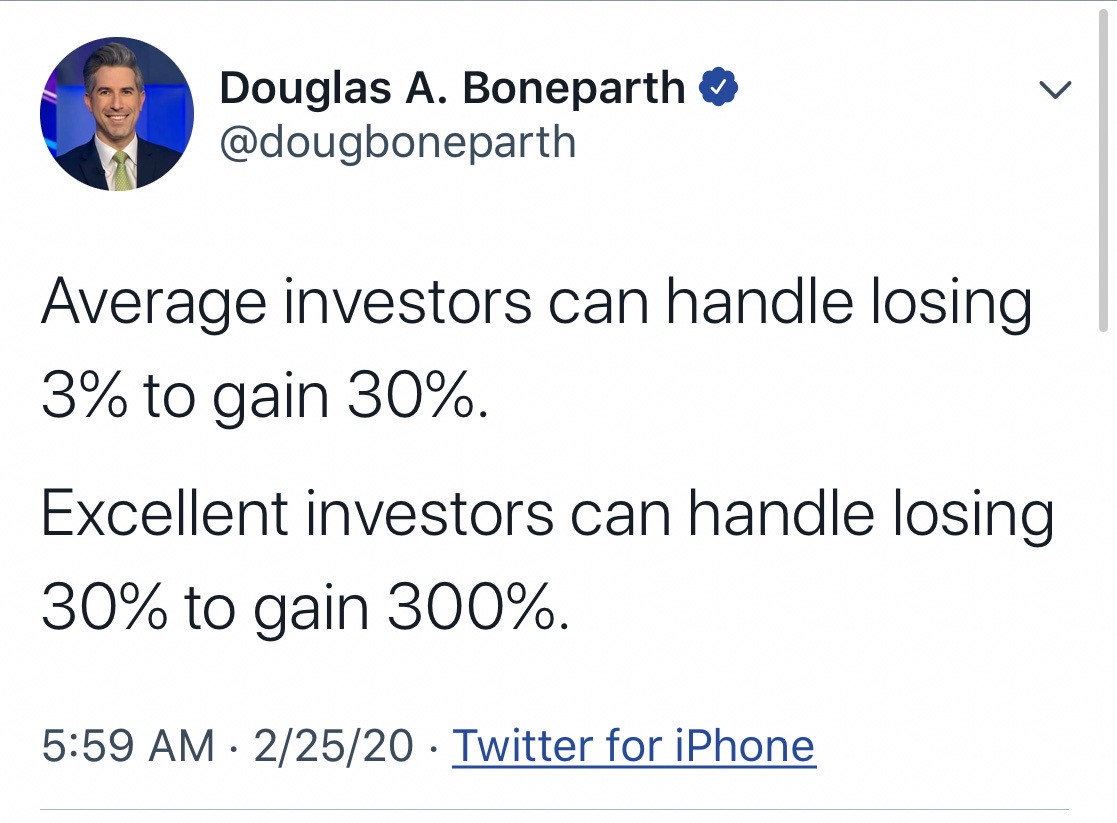

Here’s another unusual tweet. I have yet to meet an investor, average, above-average, HUMAN, over the last 30 years who’s gained 300% after losing 30%. Those who are close to retirement must avoid information like this which fosters overconfidence and complacency.

Investors five years or less until retirement must avoid FOMO or Fear Of Missing Out, when it comes to blowing up their overall asset allocations; tempted to take on more risk than they’re prepared to handle. In January when the S&P 500 was three-standard deviations above its 200-week moving average, retirees or those close to retirement were questioning their tolerance for risk even though their portfolio returns were greater than four times the personalized benchmark rate required to achieve long-term financial goals.

Lance Roberts recently wrote: “There have only been a few points over the last 25-years where such deviations from the long-term mean were prevalent. In every case, the extensions were met by a decline, sometimes mild, sometimes much more extreme.”

And while we were trimming gains, rebalancing and facing challenges to add money to equities for new clients, tenured ones were wondering why we were being so cautious. Now that markets have fallen precipitously, the same retirees now question why they sought greater risk in the first place. Some of the same investors wonder why we’re buying at lower prices or dipping our pinky toe into stock waters. It’s an emotional roller-coaster that ostensibly will destroy portfolio returns.

As we teach around town at our popular Retirement Right Lane Classes, the financial services industry preaches a wholesale accumulation mindset where every downturn is a buying opportunity. However, retirees who are need to re-create a paycheck, withdraw a fixed amount or percentage from variable assets like stocks and bonds, must realize they need to protect capital over time and severe losses must be avoided. Limited losses are inevitable. That’s the price you pay for investing in stocks. If you cannot handle an ebb and flow of risk assets, you shouldn’t be invested in the market. It’s a harsh reality; the recent downturn my serve as a valuable lesson.

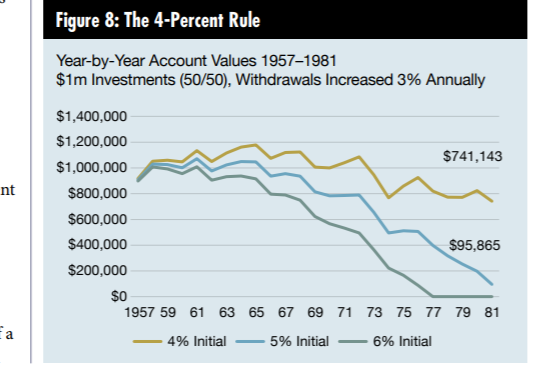

James B. Sandidge, JD in his paper “Adaptive Distribution Theory,” for The Journal of Investment Consulting, describes The Butterfly Effect for retirees. The effect refers to the ability of small changes early on in a process that lead to significant impact later.

Depending on the length of this correction and damage incurred, systematic withdrawal rates may need to stay the same (do not increase cash flow requirements in any year during the first 5 that has a negative return) or reduced altogether. James’ chart from his paper below, outlines how the sacred ‘4 percent withdrawal rule,’ can place a retiree in jeopardy if withdrawals aren’t monitored, revisited through bear market cycles.

3 – Emotions are going to be the demise of your portfolio performance.

I get it. Many investors – novice or seasoned – have forgotten markets correct; newer investors are hard-pressed to believe that bear markets are possible. I personally embrace rough markets. They provide valuable lessons, great wisdom; a dose of humility, a chance to purchase stocks at attractive prices. Each downturn is different and I take notes. It’s through times like this I’m thankful that I’m no longer with my former employer and part of a team who employs a surgical, rules-based sell discipline.

Tenured investors need to be reminded again that portfolios fluctuate! Being all in or all out of stocks is the worst move I’ve ever witnessed. In other words, selling all stocks low, purchasing again higher or ‘when the crisis blows over’ (already too late), tells me that you my friend, should avoid stocks at all costs, through every cycle. It’s a caveman reaction that will lead to very poor returns over time. Stocks are risk assets and over the last decade, we’ve forgotten what the word ‘risk’ means.

Oh, you will bleed through bear markets; it’s crucial not to hemorrhage. Can you surgically sell through down cycles like we do at RIA? If you have solid rules to do so, yes. Should you take a chainsaw to your wealth and sell everything in a panic? No. Personally, I’m using this downturn to place cash I’ve sat on for two years, selectively, slowly, to work in stocks. Our investment team is doing the same at RIA. We maintain a rules-based, three-prong approach to take profits, sell weak players and add to positions we believe are good opportunities.

I pray a prolonged downturn doesn’t turn off yet another generation of young adults from investing in equities. These generations have embraced Twitter, so I fear the messages they’ve taken in as gospel from the FinTwit stars over the years. I believe the FinTwit club members with insensitive tweets which outline how Jeff Bezos lost more wealth (to help followers keep the ‘downturn in perspective,’) are nothing short of idiocy. There’s no way in hell these people deal with clients on a consistent basis.

To keep it in perspective – Bezos, the founder of Amazon, bled close to $12 billion during the market downturn. Don’t feel bad: He’s still worth $116 billion. If you’re not seated at the Bezos table of wealth, big losses can derail future plans. However, an acceptable rate of loss must be accepted and built into a financial plan. Holistic investors are guided by rules; their guidebooks are their personalized financial plans. Investors who fly by the seat of their pants and get absorbed in fear and greed at bottoms and tops are going to find investing a disappointing experience.

Johnny Horton was a singer of folk/country story songs such as The Battle of New Orleans and Johnny Reb. However, my two favorites are North to Alaska and his rendition of Hank Williams’ Lost Highway. Mr. Horton was haunted by a premonition that he’d be killed by a drunk driver. So much so, he cancelled his attendance for the opening of the theatrical film, North to Alaska. He was hesitant to play the famous Skyline Club in Austin.

From Arden Lambert who wrote of the fatal night:

“Soon after the gig was over, he kissed his wife Billie Jean good-bye. Jean was Hank Williams’ widow whom Horton married a year after Williams’ death in 1952. Horton gave his goodbye kiss to Jean in the same place on the same cheek where Hank had kissed her after his last gig at the Skyline.

Horton, together with his bass player Tillman Franks and manager Tommy Tomlinson, headed to Shreveport, Louisiana. From the beginning, Franks noted that Horton was driving too fast (though that wasn’t new about him as he always drove fast). Suddenly, a pick-up truck smashed head-on into Horton’s car. Horton’s companions were severely injured, and he was still alive when the ambulance came. He died, however, on their way to the hospital.”

I imagine Johnny and his bass player still driving that fatal stretch of road in Milano, Texas. Forever trapped on the Lost Highway. Two men who died way too soon.

I implore that you don’t place your portfolio and emotions on a similar road.

Today, it’s easier than ever to do so.

Here’s Johnny’s version of the song. Let me know what you think…

Richard Rosso, MS, CFP, CIMA is the Head of Financial Planning for RIA Advisors. He is also a contributing editor to the “Real Investment Advice” website and published author of “Random Thoughts Of A Money Muse.” Follow Richard on Twitter

Customer Relationship Summary (Form CRS)

Also Read