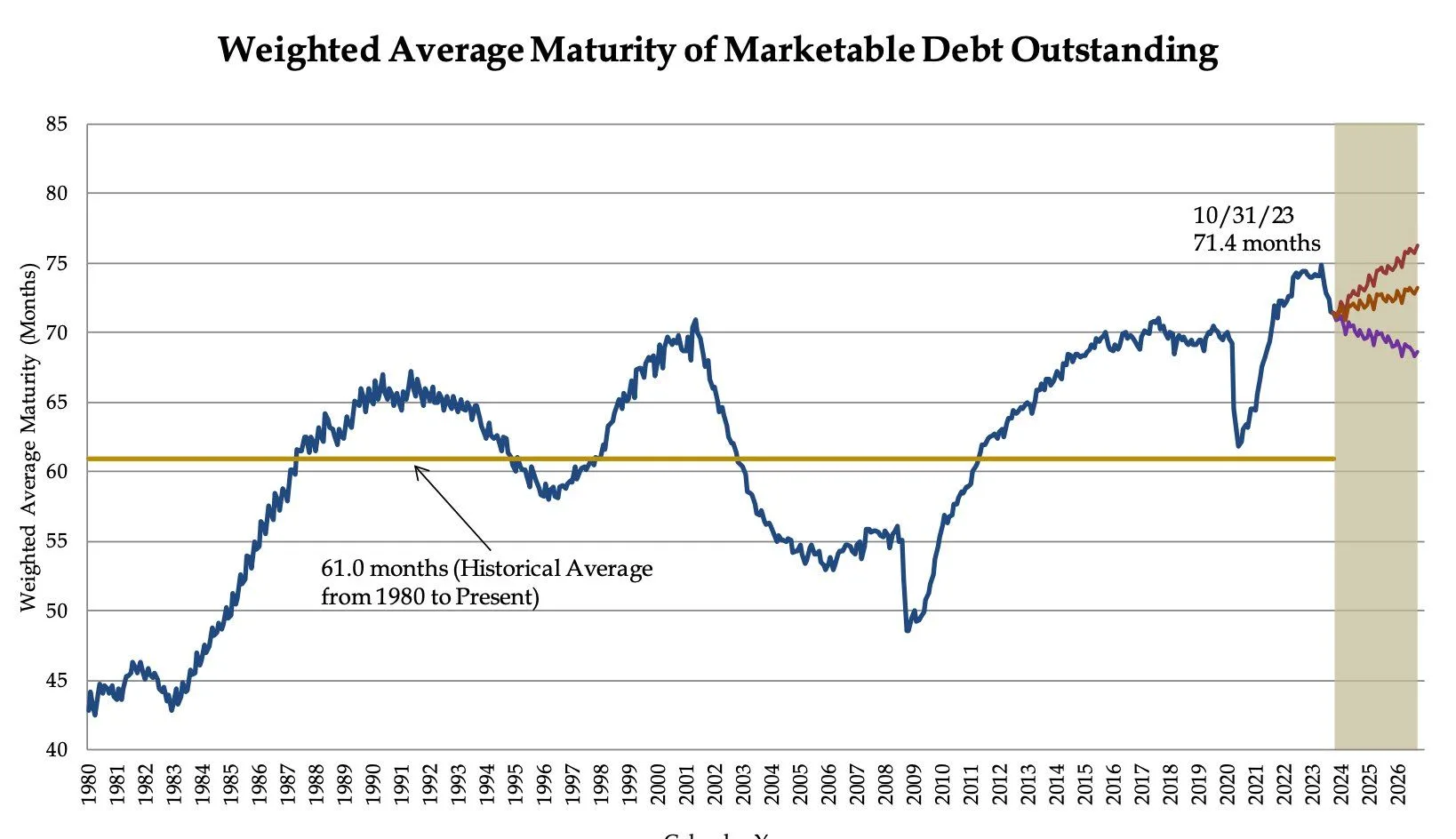

Bond bears have warned that the Treasury will overwhelm the market with debt, pushing yields much higher. For more on why we disagree with the narrative, check out our article, Context and Facts. The Treasury is keenly aware of the narrative and worried that such a mindset could significantly increase their borrowing costs. The Treasury Department’s most recent Quarterly Refunding Announcement (QRA) tried to calm the narrative. The headline from their projections, which provoked a bond rally, stated that debt issuance is expected to be $55 billion less than the market expected.

We think the bond and stock market’s positive reaction to the Treasury plans is misguided. The Treasury can purposely game their forecasts to make their needs look less than they might otherwise be. Given the pressure to relieve the Treasury of high-interest costs, such optimistic forecasting should be expected. However, the mix of bond maturities they issue is more important than how much they issue, and this has bullish ramifications. The graph below shows the weighted average maturity of Treasury debt is at historically high levels. Accordingly, the Treasury can afford to issue more Bills and fewer Notes and Bonds to avoid locking in higher interest rates for long periods. Demand is currently solid for Bills, so such a plan would relieve the long end of the curve of supply concerns and, at the same time, help meet the strong demands of money markets and other short-term bond investors.

What To Watch Today

Earnings

Economy

Market Trading Update

The market traded a little flat yesterday heading into the “Mega” earnings of Google, Microsoft, and AMD last night. Overall, Microsoft blew past lowered earnings estimates on all fronts, while Google missed expectations on ad revenue. As we discussed previously, it is not surprising for either of these companies to trade lower following earnings reports, but given their weight in passive indexes, any decline to support, which could take a few days to work through, can be bought.

Overall, the market remains extremely extended and overbought which continues to limit further upside currently. As I noted yesterday, I expect a correction in February to some degree, which can be used to add equity exposure as needed. Continue to remain patient for now.

On another note, we have been waiting for bonds to trigger their next buy signal, which happened yesterday. We used that turn to bring bond exposures for clients up to target weights as needed. With the FOMC on deck to report this afternoon, a continued dovish stance likely provides a decent trading opportunity for fixed income into next month.

JOLTS

The JOLTs report has some good news and some bad on the labor markets. The number of job openings rebounded from 8.75 million to 9.026 million. The first graph below shows the bumpy nature of this data series. Accordingly, it is rare for a monthly number to rise or fall in consecutive months. As such, we should focus on the declining trend but recognize that 9 million job openings are historically very high.

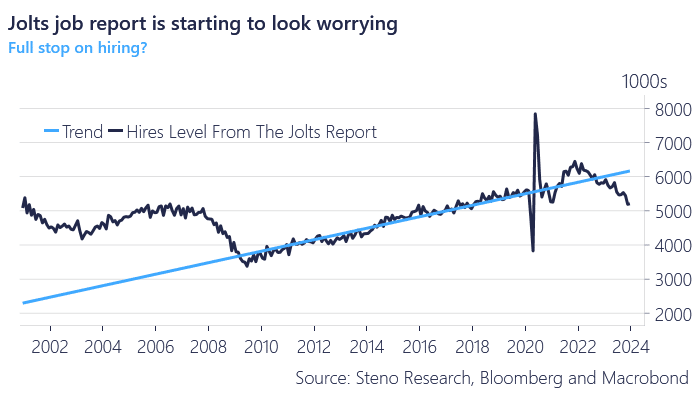

The job quits remained at 2.2%, slightly below its pre-pandemic peak. This figure shows that workers quitting jobs in hopes of getting better, higher-paying jobs have normalized. Such is also a sign that higher wage demands have likely normalized. Of concern is the second graph below from Steno Research. It shows the number of hires keeps trending lower. While layoffs may be low and job openings high, it appears business owners are lax in hiring.

Consumer Confidence: Goldilocks Today – Concern Tomorrow

The Conference Board’s consumer confidence survey was mixed. As shown below, consumers feel great about their present situation. The Present Situation index is now the highest since before COVID-19 hit the economy. Per the quote below, it appears the Goldilocks economic scenario playing out, including low unemployment, falling inflation, and lower interest rates, is prompting a boost in confidence. To wit, the average 12-month inflation expectations fell to 5.2% from 5.6%, the lowest since March 2020 (4.5%).

“January’s increase in consumer confidence likely reflected slower inflation, anticipation of lower interest rates ahead, and generally favorable employment conditions as companies continue to hoard labor,” said Dana Peterson, chief economist at The Conference Board

Despite the positive assessment of their present situation, individuals are much less confident about their future. Might they realize that recent economic robustness is not likely sustainable unless the federal deficit continues at its current pace?

Tweet of the Day

“Want to have better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.