The Markets Are Sending Confounding Messages

On December 11, 1990, at about 9:10 am on a stretch of Interstate 75 between Chattanooga and Knoxville, Tennessee, a fog so thick “you could move it with your hand” settled over Calhoun, Tennessee.

Just north of the Exit 36 Bridge, Deputy Bill Dyer arrived on the scene. Getting out of his cruiser to help a bloody car crash victim, in the distance he immediately heard tires screeching and metal crunching.

In that horrific incident, 12 people died, 42 were injured, and 99 cars and trucks were mangled.

The Calhoun pileup occurred for three reasons.

- Drivers were practically blinded when a thick fog descended.

- Drivers began to reduce their speed at various increments leading to the initial collision and the ones following.

- The fog was dramatically intensified by emissions from a nearby paper processing plant.

The stories and footage of the event are harrowing. While cars and lives are not at risk, a thick man-made fog is descending over markets. This metaphorical fog, induced by central banks, is sending confounding and conflicting messages.

The Fog of Markets

Unknowingly, most investors are managing their wealth amid a dense fog manufactured by central banks.

The confounding signals and lack of visibility emanating from equities, bonds, the dollar, precious metals, and other markets are baffling. In many cases, they are contradictory. Most troubling, they threaten our financial well-being.

To make things tougher, many of these markets sit near critical technical levels. Breakouts through or bounces off of those levels may pose significant implications for the economy and markets.

In this piece, we shine our fog lights on markets to expose these faulty signals and hidden risks.

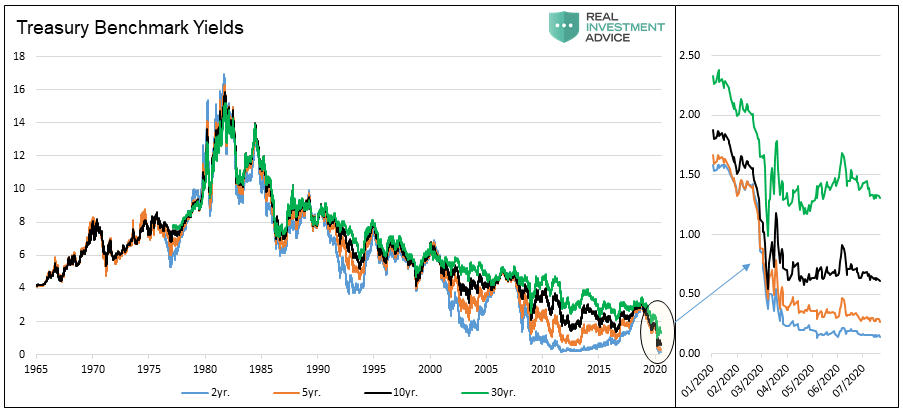

Bond Yields

The graph below charts benchmark U.S. Treasury yields. The four lines have similar patterns. Currently, yields are flat lining, and reside near the lowest levels in U.S history. These records go back to the signing of the Declaration of Independence.

The U.S. Treasury may likely run a $4 trillion deficit this year, more than twice that seen in the 2008 recession. Treasury debt as a percentage of GDP is approximately 125-130%, up from 64% in March 2008. The world is awash in Treasury debt.

The U.S. Treasury may likely run a $4 trillion deficit this year, more than twice that seen in the 2008 recession. Treasury debt as a percentage of GDP is approximately 125-130%, up from 64% in March 2008. The world is awash in Treasury debt.

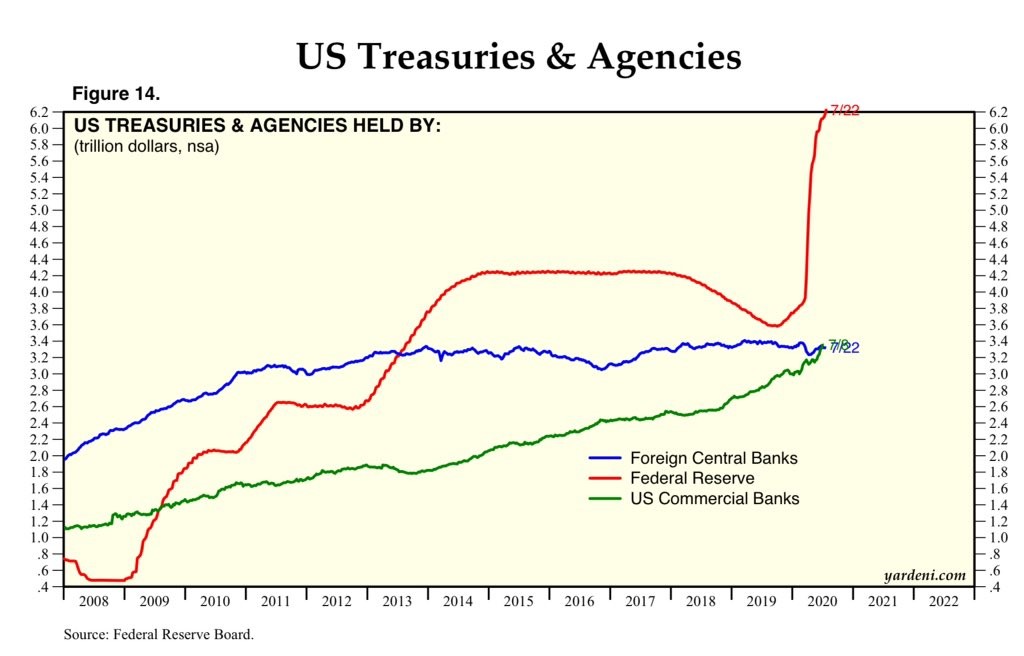

As supply increases rapidly, the second largest holders of Treasury debt, foreign investors, are not materially growing their holdings. Many have even been divesting of bonds backed by Uncle Sam.

As attestable by record low yields, the frightening supply/demand dynamic conjures no fear in the market. Since February, Treasury purchases by the Fed have skyrocketed as shown below. Those purchases more than absorb the new supply stemming from growing fiscal deficits. Fed purchases also obscure investor perspective of the most important price in any global market, the price of money.

Fed purchases also obscure investor perspective of the most important price in any global market, the price of money.

The Broken Barometer

Treasury yields were historically a good barometer for expected inflation/deflation. Falling yields tend to paint a slow growth, disinflationary picture. Higher yields reflect investor desire for compensation to protect against rising inflation concerns.

That ship has sailed.

Since inflation is, by definition, a monetary policy outcome, changes in market-based interest rates used to inform the Fed itself on the appropriateness of their policy stance. Today, however, the Fed thinks they are the wiser arbiter of the price of money. They override all market signals through quantitative easing (QE), among other extraordinary policy schemes.

Recent Fed-speak threatens even more aggressive policy actions, including yield curve control and higher inflation targets. They appear to want to do an even more expanded version of QE. Already warped by Fed influence over interest rates, those actions will further deform inflation indicators and asset prices.

U.S. Dollar

The U.S. dollar index (DXY) has seen a tremendous amount of volatility this year. In March, DXY had a face-ripping rally of 10 points over just two weeks. Since peaking, it has steadily fallen. DXY now rests precariously at the March lows.

As a net importer, a weaker dollar is inflationary and a stronger dollar deflationary. Therefore, a continuance of dollar weakness warns of inflationary pressures ahead.

A weaker dollar may also result from colossal deficits and destructive monetary policy. While some argue other countries’ governments and central banks are doing the same thing, they are not as aggressive. Additionally, unlike the U.S. dollar, currencies of other countries are not the global reserve currency.

Similar to the current state of the Treasury market and interest rates, deciphering the U.S. dollar movement and its meaning are ambiguous. Here too, traditional signals and warnings are compromised by Fed policy.

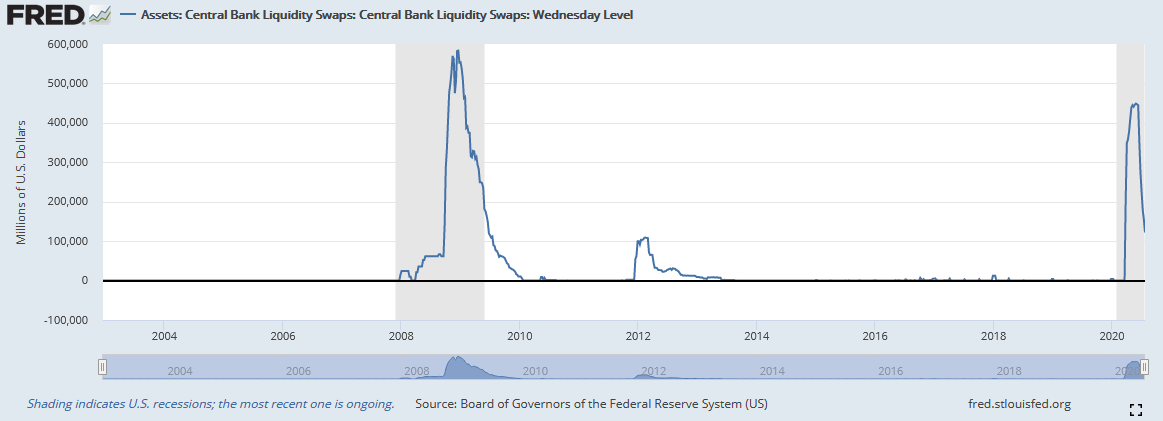

The Fed recently conducted nearly $500 billion in FX dollar swaps with foreign central banks. The publicly stated purpose of the exchanges is to provide foreign nations with dollars. The real purpose is to keep the currency transactions off of the FX markets. Ergo, the intent is to reduce upward pressure on the dollar as foreign countries seek dollars to satisfy dollar debt obligations.

If the dollar keeps falling rapidly, it may raise concerns about inflation. But again, who knows for sure as the barometer is broken.

If the dollar keeps falling rapidly, it may raise concerns about inflation. But again, who knows for sure as the barometer is broken.

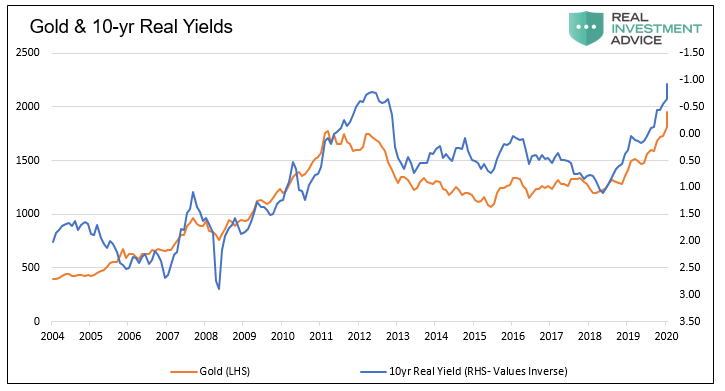

Precious Metals

Gold and silver have been rising rapidly. Historically, such gains would be attributable to dollar weakness, forceful Fed policy, and out of control deficits. This time it appears the most significant driver is interest rates. In particular, 10-year real interest rates or the 10-year Treasury yield less the inflation rate.

The graph below compares the strong correlation of real 10-year Treasury rates to the price of gold. The right axis, real yields, is inverted to better highlight the relationship.

Why are real rates so low? While it is tempting to answer with an economic argument, the truth resides with the Fed. The Fed is not only buying trillions of U.S. Treasury securities and other bonds but also inflation-protected bonds. It is hard to even know what real rates are truly reflective of any more.

Precious metals may be anticipating inflation or deflation, or maybe they are just being influenced by QE. In any case, it seems clear the barbarous relic is signaling trouble ahead.

Gold/Silver Ratio

It’s not just the price of gold and silver that warns of inflation, but the ratio of the two prices. Gold is a precious metal with little industrial value. Silver is also a precious metal but with many industrial applications. In fact, electric vehicles and cell phones, two high growth sectors, use silver.

Silver outperforming gold on a relative basis is typically an inflationary warning. The graph below shows that in March, gold rallied considerably versus silver. Over the last few months, that trend sharply reversed.

If silver continues to outpace gold, we may be drawn to say inflation lies ahead. However, we might also consider speculative excesses resulting from the Fed, which are spilling over into the silver market.

Yield Spreads

Currently, the spread or difference between corporate, municipal, and mortgage debt yields versus Treasury yields are near record lows. Yields, for a large proportion of the fixed income universe, are also at record lows.

Credit spreads tend to widen and yields rise with weaker expected growth and tighten with strong growth. Spreads reflect credit risk and credit risk increases when economic conditions are uncertain or weak.

The current environment may be more uncertain and riskier than any we have seen in our lifetimes. Yet, spreads say the future has never been more certain.

Fed purchases and threats of future purchases warp pricing and logic.

Stock Prices

Similar to the credit markets, risk and valuation assessments of equities are a fleeting memory. While the Fed has not bought equities, they are laying the groundwork by buying junk debt. Investors have no doubt the Fed has their back.

That is not just our opinion, even our politicians know. On July 22, 2020, during an interview with Jim Cramer, Nancy Pelosi stated the following:

“The stock market, there’s a floor there, you know that the Fed are pounding away to minimize the risk at the stock market.”

Whether the Fed is buying the safest Treasury Bills or the riskiest debt, they remove assets from the asset pool. In doing so, they do not just affect one market but all markets.

Equity valuations are off the charts. At the same time economic and earnings outlooks are weak and very uncertain. Most companies are not providing any guidance about revenue and earnings expectations. Stock valuations and prices should not be at or near all-time highs.

Again, the fog from the Fed’s intervention distorts investor visibility.

Summary

Investors know that markets are risky under even normal conditions. Even the best investors sometimes suffer losses. However, like the emissions from the paper plant in Calhoun, Tennessee, the Fed is responsible for making current circumstances unnavigable. The fog of the Fed is rendering most traditional economic signs meaningless. Gauges to help manage risk are obscured and disfigured. Even more confusing, some signals are contradictory to each other.

Just as drivers occasionally get caught in a thick fog, investors must navigate today’s markets differently than when the sun is shining. Investors need to modify their behavior to exercise more caution.

This is not necessarily a bearish note. Opportunities flourish for those aware of risks who safely navigate through treacherous conditions. But, at the same time, failure to do so can end in a tragic financial pileup.

Buckle up and drive with caution so you can reach your financial destination.