Yesterday morning an ominous Wall Street Journal article warned investors that the Fed will speed up the pace of tapering QE. We have more on the article and the Fed pivot in the commentary below. Usually, such hawkish news would be bad for risk assets. For instance, media commentary last week attributes volatility to the Fed. Yesterday, markets surged on a reminder the Fed is turning hawkish. That rally is set to continue this morning.

Narratives to explain trading activity can often be misleading. In our opinion, the stock surge of Monday and last week’s violent price movements point to mutual fund rebalancing. That said, the funds are likely not done, and we may see some more wild swings before the markets settle down for the holidays.

What To Watch Today

Economy

- 8:30 a.m. ET: Non-farm productivity, 3Q final (-4.9% expected, -5.0% in 2Q)

- 8:30 a.m. ET: Unit labor costs, 3Q final (8.3% expected, 8.3% in 2Q)

- 8:30 a.m. ET: Trade balance, October (-$66.8 billion expected , -$80.9 billion in September)

- 3:00 p.m. ET: Consumer credit, October ($25.000 billion expected, $29.913 billion in September)

Earnings

Pre-market

- 6:55 a.m. ET: AutoZone (AZO) to report adjusted earnings of $20.82 on revenue of $3.38 billion

Post-market

- 4:05 p.m. ET: ChargePoint Holdings (CHPT) to report adjusted losses of 14 cents on revenue of $63.46 million

- 4:05 p.m. ET: StitchFix (SFIX) to report adjusted losses of 13 cents on revenue of $570.73 million

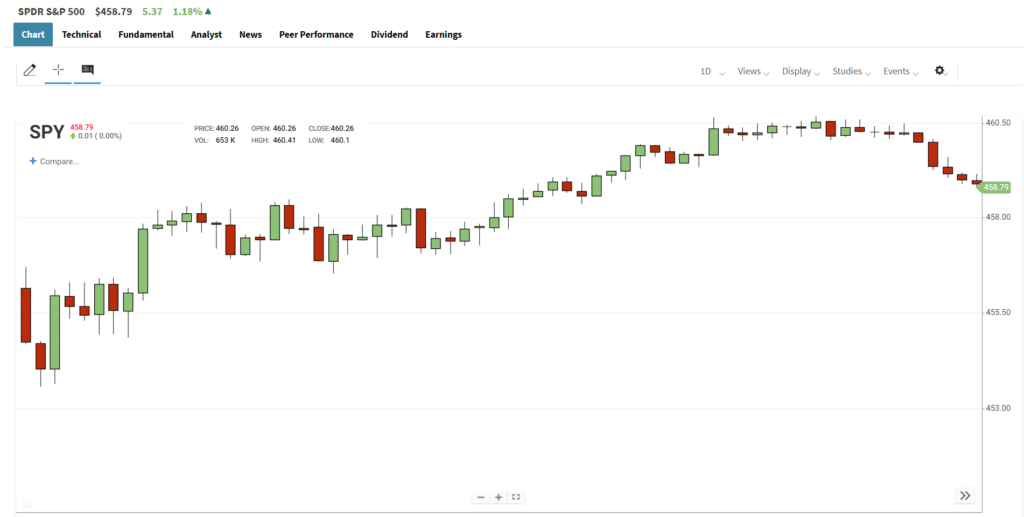

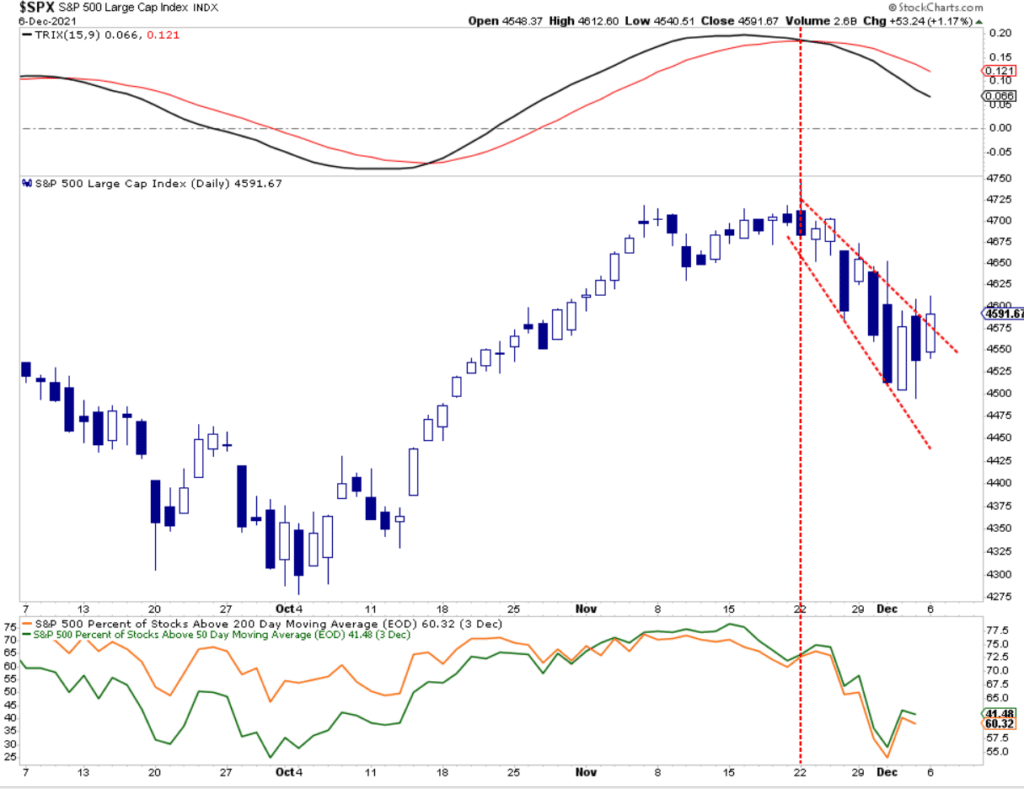

Market Rallies On Money But Breadth Remains Weak

As noted in this past weekend’s newsletter, we added to our SPY holdings late Friday in anticipation of a market rally this week. That rally came on Monday, with markets very oversold. However, we will expect some additional weakness over the next week as mutual fund distributions continue. Furthermore, breadth remains incredibly weak so monitor your risk exposures closely.

As noted, despite the Fed Pivot, the attempt to break out of the downtrend channel is a positive development. If the market can hold above the downtrend line, a rally back to the November lows becomes more likely.

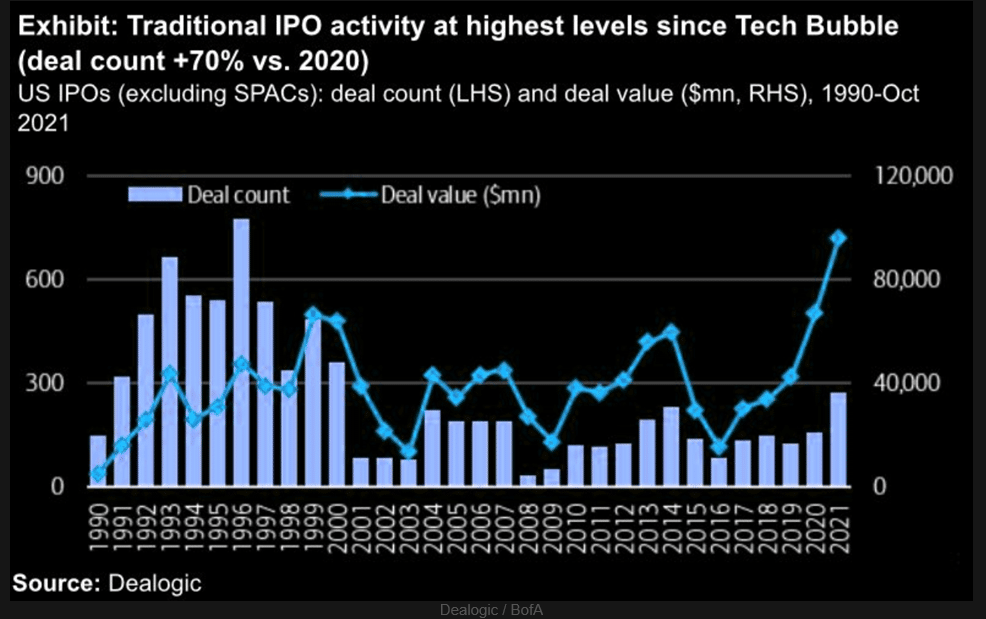

WallStreet Rushes To Market – What Do They Know?

If you haven’t figured this out by now, WallStreet is a business and a very big business at that. Their job is to meet the demand for products by creating them. In other words, the Wall Street business is selling you products and it doesn’t matter if that product is good, bad, or entirely defective. With that in mind, now process this.

IPO deals YTD is highest since Tech Bubble in 2000, but as % of mkt cap, deal value is half of ’99, BofA has calculated. There’s also half number of public comps today (3,300) vs ’99 (6,000). Another difference is concentration by industry is less, w/no sector >50% of IPOs in ’21.” – @TheMarketEar

The Fed Pivots

As is quite common, the Fed likes to signal changes in policy via the media. Today, the Wall Street Journal published an article entitled, High Inflation, Falling Unemployment Prompted Powell’s Fed Pivot. The article confirms Chairman Powell’s testimony to Congress from last week. The bottom line per the article: “Officials are making plans to accelerate the process at their policy meeting next week, ending it by March instead.”

The article clearly articulates that inflation, not employment, is now the Fed’s primary concern. While the Fed thinks high inflation rates will come down next year, they “can’t act as though we’re sure of that.” The Fed often gets economic data before their release. Is it possible this Friday’s CPI report is concerning?

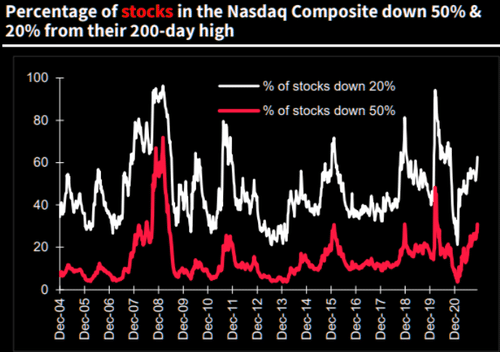

So Much Pain (For Some/Many) At All-Time Highs

Two amazing stats:

1. Almost a third of the stocks in the Nasdaq Comp are down 50% from highs (see SocGen chart)

2. Over the last 6 months, 4 stocks (MSFT, AAPL, NVDA, GOOGL) have generated almost 70% of the S&P 500’s return.

Time For Value?

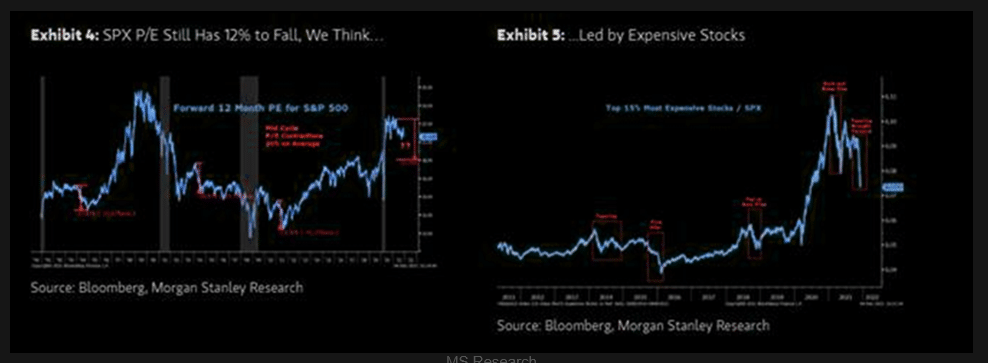

12% More Downside?

“We reiterate our view that tapering is tightening for the markets and it will lead to lower valuations like it always does at this stage of any recovery. How much lower? We forecast S&P 500 forward P/Es to fall to 18x, or approximately 12% below current levels. Obviously, for the more expensive parts of the market, that decline will be larger.” – Morgan Stanley

High valuations, combined with the Fed tightening monetary policy, have not had good outcomes for investors, particularly speculative ones.

While we currently expect a short-term oversold rally, there is a real risk that 2022 could be a vastly different market for investors as compared to 2021.

The Communications Sector (XLC) is Struggling

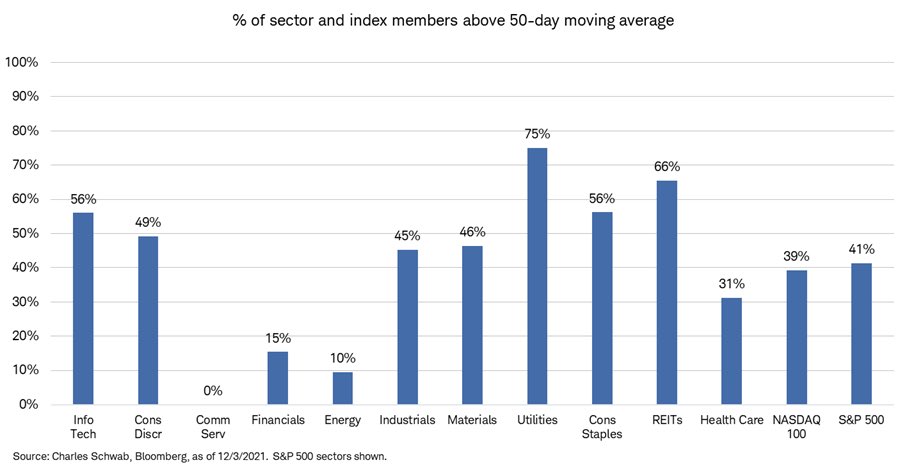

In last Friday’s Relative Value Scorecard report for RIAPro subscribers, we noted the communications sector is performing incredibly poorly on a relative basis versus the S&P 500. To wit: “The standout on the relative charts is the incredibly oversold condition of the communications sector. Its score is -12.41 out of a possible -13.5.” While a bounce versus the market is likely, we caution the sector is very top-heavy. As such, over half of its weighting is in three stocks- FB, GOOG, and NFLX. The fortunes of those companies, especially FB and GOOG are likely to drive the sector. The graph below, courtesy of Charles Schwab, further highlights how poorly the communications sector is trading. Every member of the sector is below its respective 50dma, and 81% are below their 200dma.

The Week Ahead

There are not many relevant economic data releases this week, but what data is coming out is essential to assess better what the Fed may do at their FOMC meeting next week. Wednesday’s JOLTs report is expected to show the number of job openings continues at or near record-high levels, meaning the labor market is robust. Job Quits, another indicator of the jobs market will also be high, signaling employee confidence in their ability to quit and find a better or higher-paying job. On Friday, the BLS will report on CPI. After last month’s shocking 6.2% print, economists expect another bump higher to 6.8%. Such a number will further pressure Powell and the Fed to speed up the taper process. It may also push Fed members to discuss the timing of interest rate hikes.

The Treasury will auction 10 and 30-year bonds on Wednesday and Thursday, respectively. Typically the auctions can weigh on bond prices in the days prior. The Fed will enter its self-imposed media blackout window this week with the FOMC meeting next Wednesday.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

Also Read