China’s National Health Commission announced that approximately 250 million citizens, or 18% of its population, caught the covid virus in December. The surge in covid cases results from China relaxing its strict covid restrictions. The government is essentially allowing the covid virus to spread, which will help improve their long-term economic activity. However, the virus will spread rapidly through China in the short run. Sick manufacturing workers will undoubtedly impair factory production, resulting in weaker output. Demand from China’s consumers will temporarily weaken, pushing inventories higher.

Given China’s dominance in manufacturing and exporting a wide range of essential products, lifting covid restrictions will likely cause supply line issues to resurface and inflationary pressures to pick up worldwide in the first quarter. While the inflationary impact will be temporary, it may keep inflation higher than the Fed’s liking and further bolster their inflation concerns.

Nearly 37 million people in China may have been infected with the Covid-19 virus on a single day this week, according to estimates from the government’s top health authority- Bloomberg

What To Watch Today

Economy

- 8:30 a.m. ET: Wholesale Inventories, MoM, November Preliminary (0.5% prior)

- 8:30 a.m. ET: Advance Goods Trade Balance, November (-$96.8 billion expected, -$99.0 billion prior)

- 8:30 a.m. ET: Retail Inventories, MoM, November (-0.1 expected, -0.2% prior)

- 9:00 a.m. ET: FHFA Housing Pricing Index, MoM, October (-0.6% expected, 0.1% prior);

- 9:00 a.m. ET: S&P CoreLogic Case-Shiller 20-City Composite, MoM, October (-1.40% expected, -1.24% prior)

- 9:00 a.m. ET: S&P CoreLogic Case-Shiller 20-City Composite, YoY, October (8.20% expected, 10.43% prior)

- 9:00 a.m. ET: S&P CoreLogic Case-Shiller U.S. National Home Price Index, YoY, October (10.65% prior)

- 9:00 a.m. ET: Dallas Fed Manufacturing Activity, December (-14.4 prior)

Earnings

- No notable earnings announcements

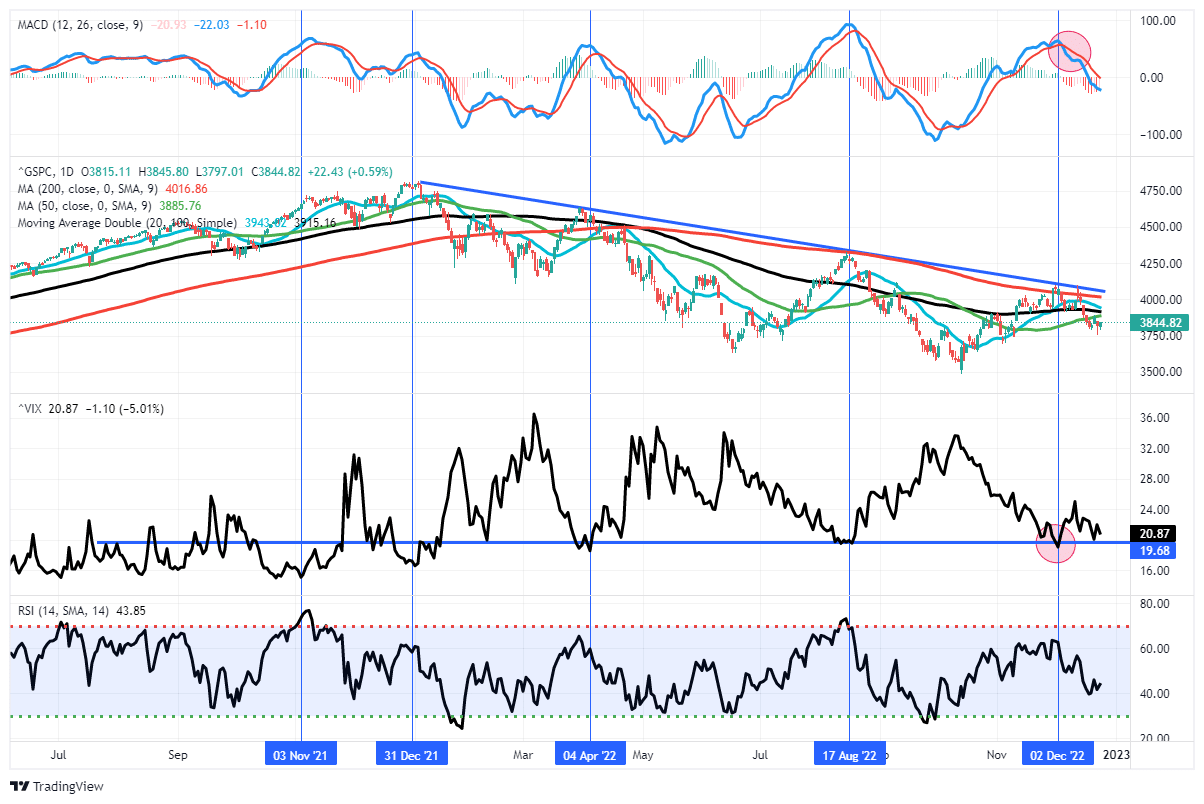

Market Trading Update

With the MACD “sell signal” still intact, that downside break put additional pressure on asset prices this past week. With only one trading week left until year-end, the “Santa Rally” has gotten off to a rather icy start. Since Monday was a market holiday, such leave only four days for “Santa to visit Broad and Wall.” At this point, December will likely have a negative return, which bodes poorly for January. However, markets are pointing higher this morning as traders are looking to close out the year on a positive note.

Importantly, with the market trading below the 50-DMA, there is a cluster of resistance just overhead in the market, with the 20, 100, and 200-DMA sitting just above current levels. Most importantly, the downtrend line from the January highs has continued to cap rallies all year.

While investor sentiment had improved recently, with professional investors getting bullish during the recent rally, that sentiment mostly reversed in recent days as the rally failed. The question is whether traders will begin to buy the market heading into 2023 or if the risk-off positioning we witnessed in December will continue in January.

One thing is for sure. Currently, Wall Street estimates for next year remain mostly bullish, with the median price target at 4000, but with some running as high as 4500, which is nearly 17% above 3850 (as of the time of this writing.)

The Week Ahead

It will be a tranquil week ahead with limited economic data and few Fed speakers. We continue to watch initial jobless claims and continuing claims for signs of weakness in the labor market. We urge caution in reading too much into the data. Labor data can be misleading this time of the year due to seasonal holiday hiring and firing patterns. The Richmond and Dallas Fed Indexes will provide our first glimpse at labor and price conditions in December. The Case-Shiller Home price index is expected to fall 1.5% monthly, but it is still running at a strong +10.5% year-over-year pace.

Many corporations are entering stock buyback blackout periods with Q4 earnings reports due in a few weeks.

Labor Markets Keep Powell Up At Night

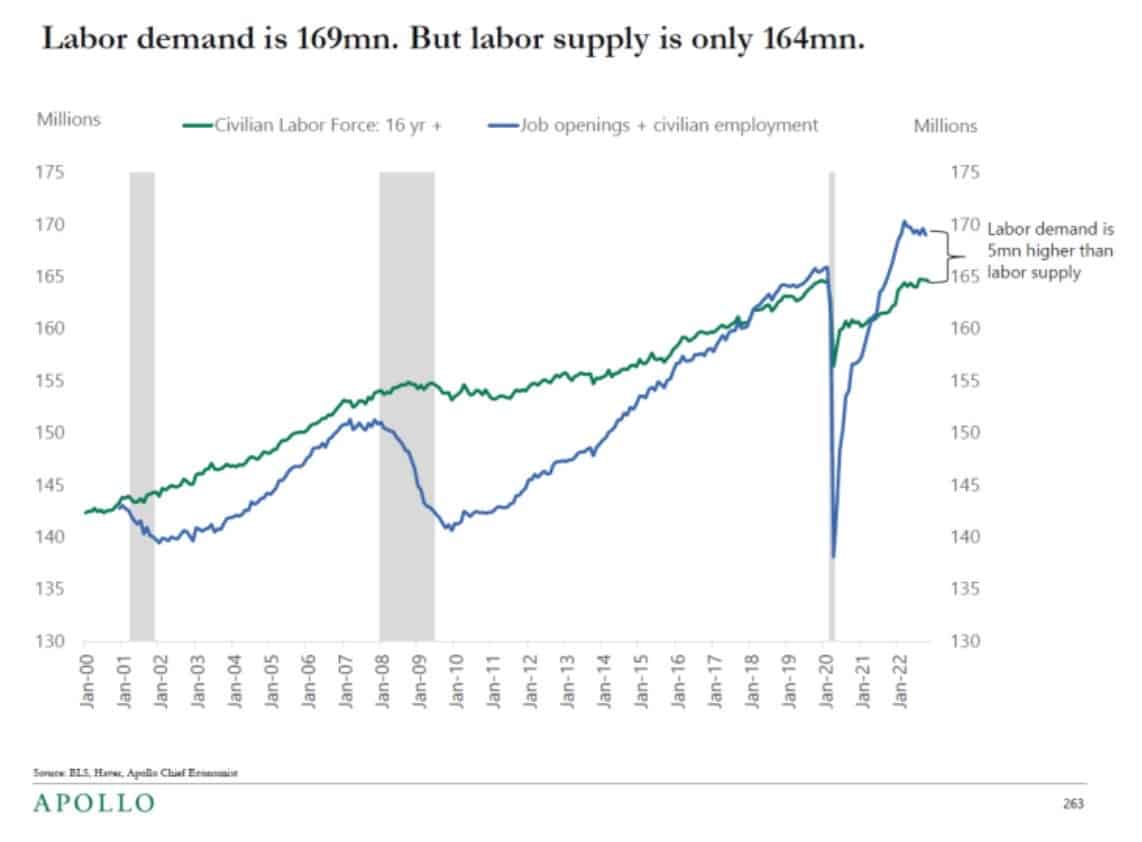

The graph below, courtesy of Apollo, is the Fed’s worst nightmare. It shows that the number of jobs plus job openings is approximately 5 million more than the labor force. Traditionally there are more potential employees than the combination of employment and job openings. Typically, such a condition gives employers leverage in managing wages. Today, employees have the leverage to demand higher wages. This is a big reason wage inflation is strong. Further, it heightens the Fed’s fear that inflation may not fall as quickly as it would prefer. The graph also explains the Fed’s desire to increase the unemployment rate.

Apple or Treasuries?

In Double Dog Dares and Equity Risk Premiums, we explain the equity risk premium and how it can be used as a valuation tool. The article shows that the current S&P 500 equity risk premium is near 20-year lows. Given this expensive valuation, we state the following:

Today, given the potential market turmoil due to a possible recession, higher interest rates, inflation, an aggressively hawkish Fed, and the geopolitical situation in Ukraine, we should be paid more, not less compensation for taking on risk.

The graph below compares the earnings yield on Apple to a five-year Treasury note. The bottom chart shows that the difference, or equity risk premium, is currently approximately +.90%. Such a low premium pales compared to the much more significant premium investors were paid for the last ten years.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.