“The strong economic recovery will not get interrupted by inflation or a credit crunch, and the market will soon reach 4,500.” – Ed Yardeni via Advisor Perspectives

After discussing BofA’s view of why the market could drop to 3800, I thought it fair to discuss a more optimistic view.

BofA’s view of a market correction was a function of the more exuberant “optimism” in the market. To wit:

“This analysis is interesting, particularly when analysts are rushing to upgrade both economic and earnings estimates.”

“More importantly, investors are incredibly long-biased in portfolios, with equity allocations reaching some of the highest levels in history.”

What Subramanian questioned is whether all the “good news” is already “priced in?”

“Amid increasingly euphoric sentiment, lofty valuations, and peak stimulus, we continue to believe the market has overly priced in the good news. We remain bullish the economy but not the S&P 500. Our technical model, 12-month Price Momentum, has recently turned bearish amid extreme returns over the past year.”

So, with BofA’s context in place, what is Yardeni seeing so differently?

Yardeni’s Outlook

“Not only will the bull market in stocks continue with strong profits, but the bond yield will go to 2% by year-end and 2.5% to 3% next year.”

The basis of Yardeni’s forecast is that of a robust economic recovery that, in his words, was “much better than expected.” The other reasons supporting his optimistic view are:

- Treasury Secretary Yellen and Fed Chair Powell want to step on the accelerator to get broad-based and inclusive maximum employment. The support is $120 billion per month of quantitative easing (QE) and low rates.

- Once the Fed starts to taper its QE, it may be months before it raises rates.

- The risks to the recovery are another round of the virus, which is unlikely given vaccines.

- A credit crunch is problematic but hard to imagine given the liquidity in the economy. That liquidity gets bolstered by the $4 trillion growth in the money supply.

- The stock market is at record highs, and performance expanded beyond a few technology stocks.

- Is the market overvalued? Yes, but valuations are not insanely stretched.

- We will get an increase in inflation, but to a large extent, it remains transient.

The question, is whether BofA is correct that what Yardeni expects has already gotten priced into the markets? Given the massive advance from the 2020 lows, it is likely.

However, to Yardeni’s point, investor’s “bullish bias” is devoid of worry about “risk” as long as the Fed remains active.

Psychology Of QE

A recent commentary from Mish Shedlock on QE is key to understanding the current speculative psychology. I pulled two specific quotes from his article:

“Does anyone think investors care that the total amount of corporate bonds purchased by the Fed during the pandemic amounted to just $14 billion, in a $22 trillion economy, with $11 trillion of nonfinancial corporate debt and $60 trillion of equity securities? No, they do not. Do they care that Fed purchases of unbacked corporate securities were authorized only using CARES funding provided by the Treasury, and that such purchases are otherwise illegal under the Federal Reserve Act? No they do not. Why? Because it isn’t the mechanism of quantitative easing that investors care about. What they care about is Quantitative Easing!” – Ben Hunt

And

“The key to navigating Quantitative Easing! and Fed policy in general is to recognize that their effect on the stock market relies almost entirely on speculative investor psychology. See, as long as investors get inclined to speculate, they treat zero-interest money as an inferior asset, and they will chase any asset with a yield above zero (or a past record of positive returns). Valuation doesn’t matter because investors psychologically rule out the possibility of price declines in the first place.” – John Hussman

In other words, “Quantitative Easing” is a mental formation. The only thing that alters its effectiveness of the Fed’s monetary policy is investor psychology itself.

Such was a point we made in the “Stability/Instability Paradox.”

“With the entirety of the financial ecosystem now more heavily levered than ever, due to the Fed’s profligate measures of suppressing interest rates and flooding the system with excessive levels of liquidity, the ‘instability of stability’ is now the most significant risk.”

Moral Hazard

The ‘stability/instability paradox’ assumes that all players are rational, and such rationality implies avoidance of destruction. In other words, all players will act rationally, and no one will push “’the big red button.’”

Importantly, what Hussman addresses when he says investors psychologically rule out the possibility of price declines is “moral hazard.”

What exactly is the definition of “moral hazard.”

Noun – ECONOMICS

The lack of incentive to guard against risk where one is protected from its consequences, e.g., by insurance.

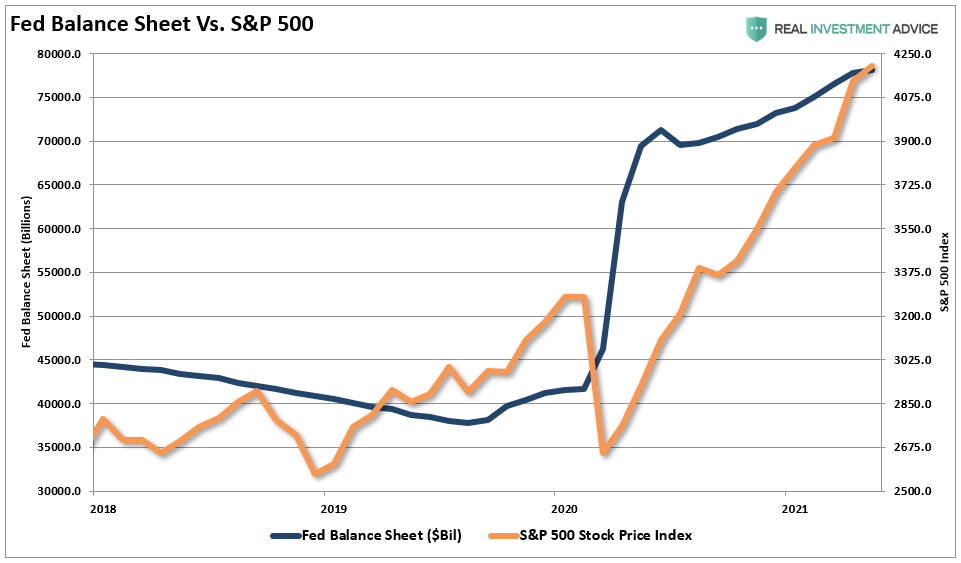

The correlation between the Fed’s monetary interventions and the stock market is evident. The increase in the Fed’s balance sheet remains in near lockstep with the stock market’s climb.

While Fed officials tacitly deny any correlation between their monetary interventions and the stock market, the evidence is quite clear.

However, as stated, the consequences of monetary policy longer-term gets set aside for the short-term benefits of inflated “psychology.”

The Flies In The Ointment

I would be remiss in not briefly addressing some of the concerns in Yardeni’s views.

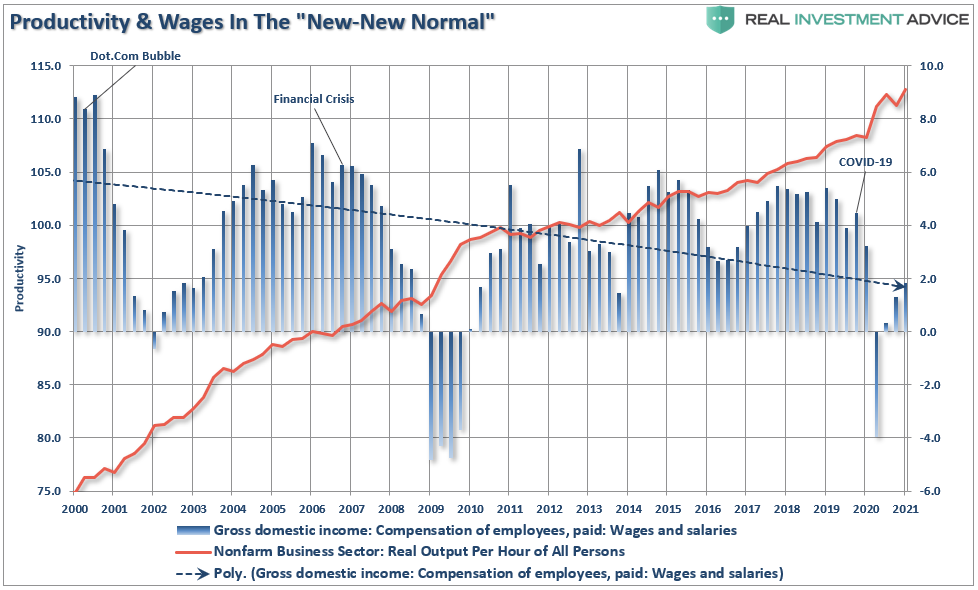

Productivity is deflationary.

As I discussed in “The Roaring ’20s Aren’t Coming:”

“The critical distinction between the technology of the ’20s and today is stark. When technology increases productivity and output while simultaneously increasing demand by increasing ‘reach,’ it is beneficial.

However, when technology improves efficiencies to offset weaker demand and reduce labor and costs, it is not.”

Furthermore, a sustained spike in inflation, which drives rates higher, will negatively impact both the markets and the economy.

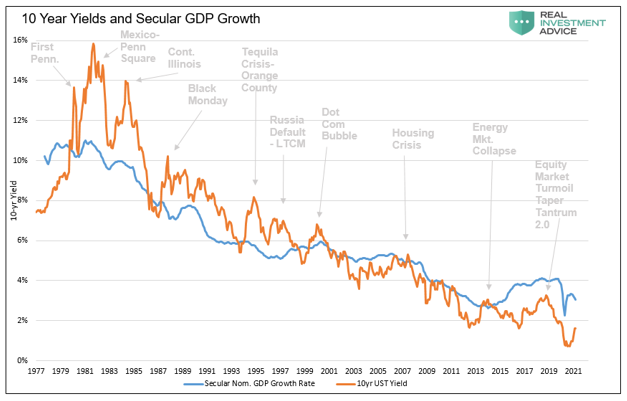

As Michael Lebowitz noted in “What Interest Rate Will Matter,” rate increases have a history of financial events. To wit:

“Looking back over the last 40 years each time interest rates reach the upper end of its downward trend, a financial crisis of sorts occurred. The graph below charts the steady decline in rates and GDP along with the various crisis occurring when rates temporarily rose.”

“Notice, as time goes on it takes less and less of a rate increase to generate a problem. The reason is the growth of debt outpaces the ability to pay for it.”

Yes. Valuations Are Expensive.

While Yardeni suggests valuations are cheap, there is little evidence that such is the case. Most of the assumption is that earnings and the economy will “catch up” with prices. Such would suggest that prices remain stagnant during that process, yet Yardeni assumes prices will surge to 4500 in 2021, eclipsing the benefit of assumed growth.

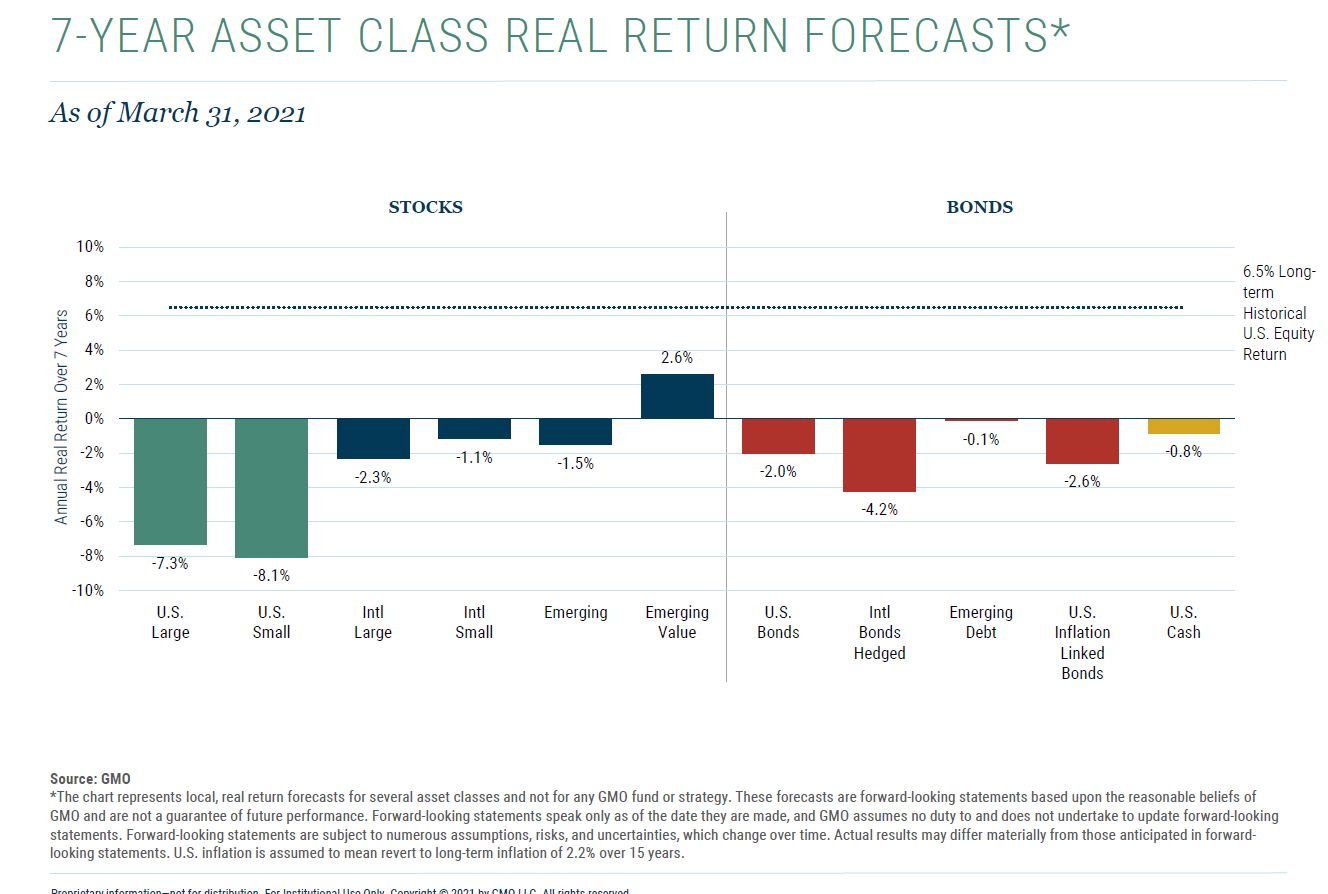

Therefore, valuations are not only high by historical standards but will remain high as prices rise along with economic and earnings growth. The consequence of over-paying for valuations today is substantially lower long-term returns from asset classes in the future. The eponymous GMO noted such in their most recent 7-year forecasts.

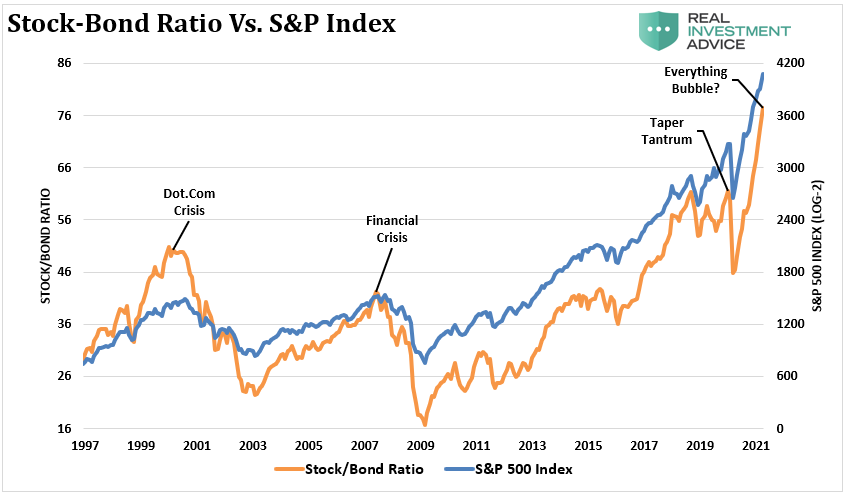

Furthermore, given the extremely high correlation between stocks and bonds, a level of extreme not seen since the “Dot.com” peak, future outcomes seem poor.

The Fed will continue to supply liquidity, which will help the market ignore the reality of the majority of return barometers. However, as we saw in March of 2020, that does not preclude hair-raising volatility and significant declines. But, to Yardeni’s point, in the short-term Fed liquidity does support prices on the margin regardless of the environment.

Not Much Upside

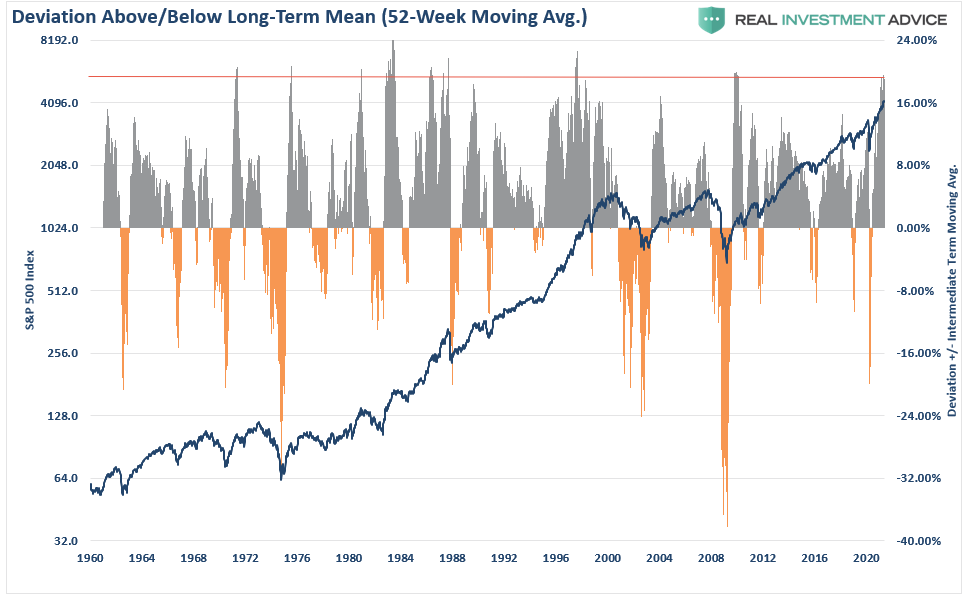

While Yardeni is optimistic on the market short-term, which is probably correct, a target of 4500 by year-end doesn’t offer tremendous upside relative to the risk. As noted previously, the current deviation from long-term means is one of the most significant extremes on record.

Does that mean the market will crash tomorrow? No. However, it does strongly suggest that at some point, a mean-reverting event will occur. Such a decline will wipe out a large chunk of recent gains as markets reprice for slower future economic growth.

If you agree with Dr. Yardeni, the prescription is simple. Buy stocks.

However, as Mark Hulbert recently noted:

“I have no idea whether the stock market is forming a bubble that’s about to break. But I do know that many bulls are fooling themselves when they think a bubble can’t happen when there is such widespread concern. In fact, one of the distinguishing characteristics of a bubble is just that.

So, what should you do if you are close to retirement?

“It’s important for all of us to be aware of this bubble psychology, but especially if you’re a retiree or a near-retiree. That’s because, in that case, your investment horizon is far shorter than for those who are younger. Therefore, you are less able to recover from the deflation of a market bubble.” – Mark Hulbert

You have a choice. But, for now, Yardeni is correct.

Just remember:

“All bull markets last until they are over.” – Jim Dines