The Technical Value Scorecard Report uses 6-technical readings to score and gauge which sectors, factors, indexes, and bond classes are overbought or oversold. We present the data on a relative basis (versus the assets benchmark) and on an absolute stand-alone basis. You will find more detail on the model and the specific tickers below the charts.

Commentary 8-06-21

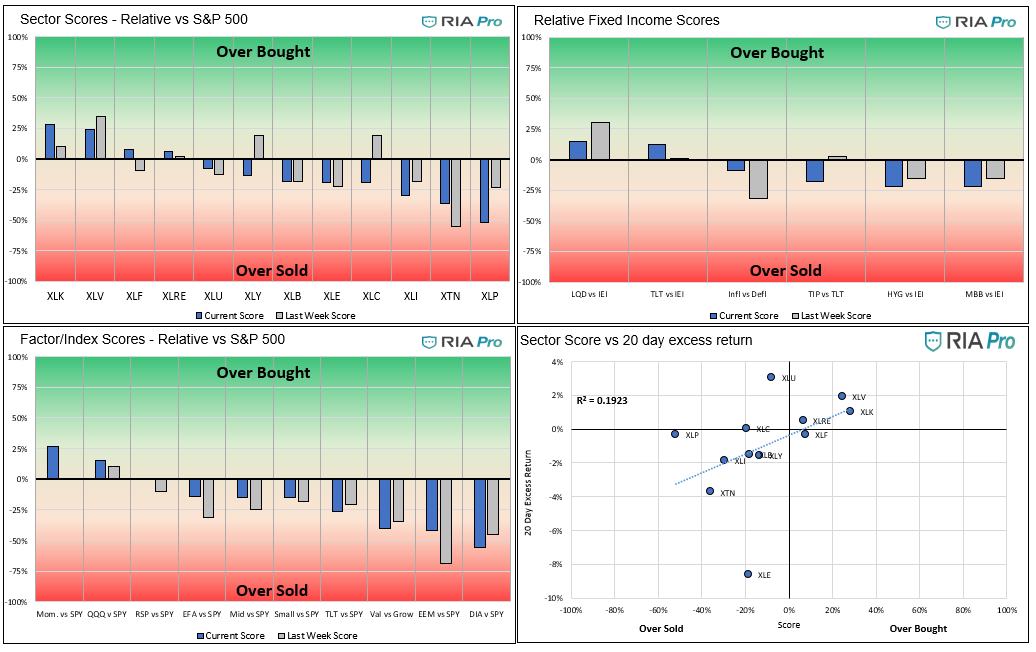

- The S&P remained rangebound this week. Utilities were the best performing sector on the week, beating the S&P 500 by over 1.5%. Materials and staples were the worst, down 2% and 1.5% respectively. The divergence between staples and utilities is interesting. Both sectors are considered defensive and often travel together. In Wednesday’s market commentary, we had this to say: “93% of the utility stocks in the ETF are above their respective 200 dma and that percentage has been steadily climbing for the last 2 months. Only 66% of staples stocks are above their respective 200 dma and the percentage has been steadily falling since May. The weakening breadth of XLP may result in relative weakness versus XLU, especially if inflation and inflation expectations remain high.”

- On a relative basis, versus the S&P 500, most sectors continue to be in the fair value range (+/-50%). In general, the growth, deflationary beneficiaries remain slightly overbought, while the inflationary beneficiaries are slightly oversold. The graph continues to point to indecision in the markets. This condition may persist through August as the market waits on the Fed’s Jackson Hole meeting in late August.

- The factor/index relative graphs show relative weakness in the Dow Jones and emerging markets. Momentum and the NASDAQ are slightly overbought. The strongest sign of indecision is in the scatter plot. With an r-squared of .1923, the plot denotes almost no correlation between returns and scores. As we noted last week, this is occurring because we are range-bound with relatively small weekly changes in prices.

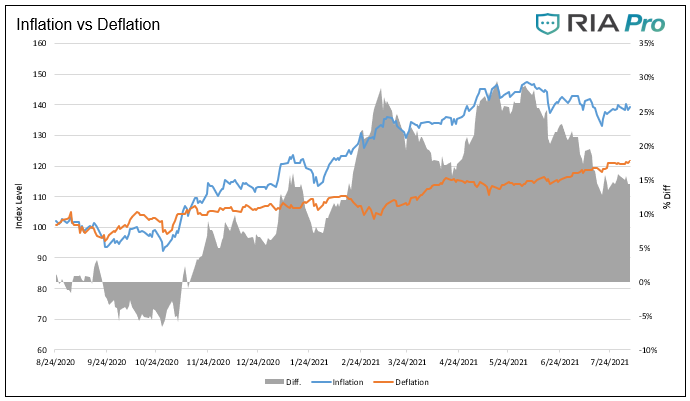

- The third graph below shows the returns between the inflation/deflation sectors and factors has leveled off over the last couple of weeks. This is likely another sign of indecision in regards to inflation expectations and a result of some signs that prices and economic growth are slowing from their torrid pace. As you can see, the return differential typically trends in one direction or the other.

- On an absolute basis, most sectors and markets remain overbought. The graph on the bottom right (second set of graphs) shows the S&P 500 is near the upper bound of recent scores. In mid-June and mid-July, similar levels were attained, and a brief decline ensued. Our proprietary money flow indicator is also signaling the potential for a decline. The trend however, is upward so any decline, as we have seen, may be minimal. Equity markets are in the seasonally weakest part of the year, so any upside may be limited as well. The chop may continue.

- Emerging markets remain the only oversold factor/index, albeit marginally. Momentum and the NASDAQ are reaching overbought levels that warrants caution. We caution you on the Momentum ETF (MTUM) as it is constantly changing its constituency and, by definition, chasing stocks that overbought and selling those that oversold. Over the last few months, it has been “late to the party” on a few occasions.

- The utility sector has an absolute score over 50%, plus it is over 2 standard deviations from its 50 dma and very close to its 20 and 200 dma. This overbought condition may continue a little longer as it was beated down for so long.

Graphs (Click on the graphs to expand)

Users Guide

The score is a percentage of the maximum score based on a series of weighted technical indicators for the last 200 trading days. Assets with scores over or under +/-70% are likely to either consolidate or change trend. When the scatter plot in the sector graphs has an R-squared greater than .60 the signals are more reliable.

The first set of four graphs below are relative value-based, meaning the technical analysis is based on the ratio of the asset to its benchmark. The second set of graphs is computed solely on the price of the asset. At times we present “Sector spaghetti graphs” which compare momentum and our score over time to provide further current and historical indications of strength or weakness. The square at the end of each squiggle is the current reading. The top right corner is the most bullish, while the bottom left corner the most bearish.

The technical value scorecard report is one of many tools we use to manage our portfolios. This report may send a strong buy or sell signal, but we may not take any action if other research and models do not affirm it.

The ETFs used in the model are as follows:

- Staples XLP

- Utilities XLU

- Health Care XLV

- Real Estate XLRE

- Materials XLB

- Industrials XLI

- Communications XLC

- Banking XLF

- Transportation XTN

- Energy XLE

- Discretionary XLY

- S&P 500 SPY

- Value IVE

- Growth IVW

- Small Cap SLY

- Mid Cap MDY

- Momentum MTUM

- Equal Weighted S&P 500 RSP

- NASDAQ QQQ

- Dow Jones DIA

- Emerg. Markets EEM

- Foreign Markets EFA

- IG Corp Bonds LQD

- High Yield Bonds HYG

- Long Tsy Bonds TLT

- Med Term Tsy IEI

- Mortgages MBB

- Inflation TIP

- Inflation Index- XLB, XLE, XLF, and Value (IVE)

- Deflation Index- XLP, XLU, XLK, and Growth (IWE)

Michael Lebowitz, CFA is an Investment Analyst and Portfolio Manager for RIA Advisors. specializing in macroeconomic research, valuations, asset allocation, and risk management. RIA Contributing Editor and Research Director. CFA is an Investment Analyst and Portfolio Manager; Co-founder of 720 Global Research.

Follow Michael on Twitter or go to 720global.com for more research and analysis.

Customer Relationship Summary (Form CRS)

Also Read