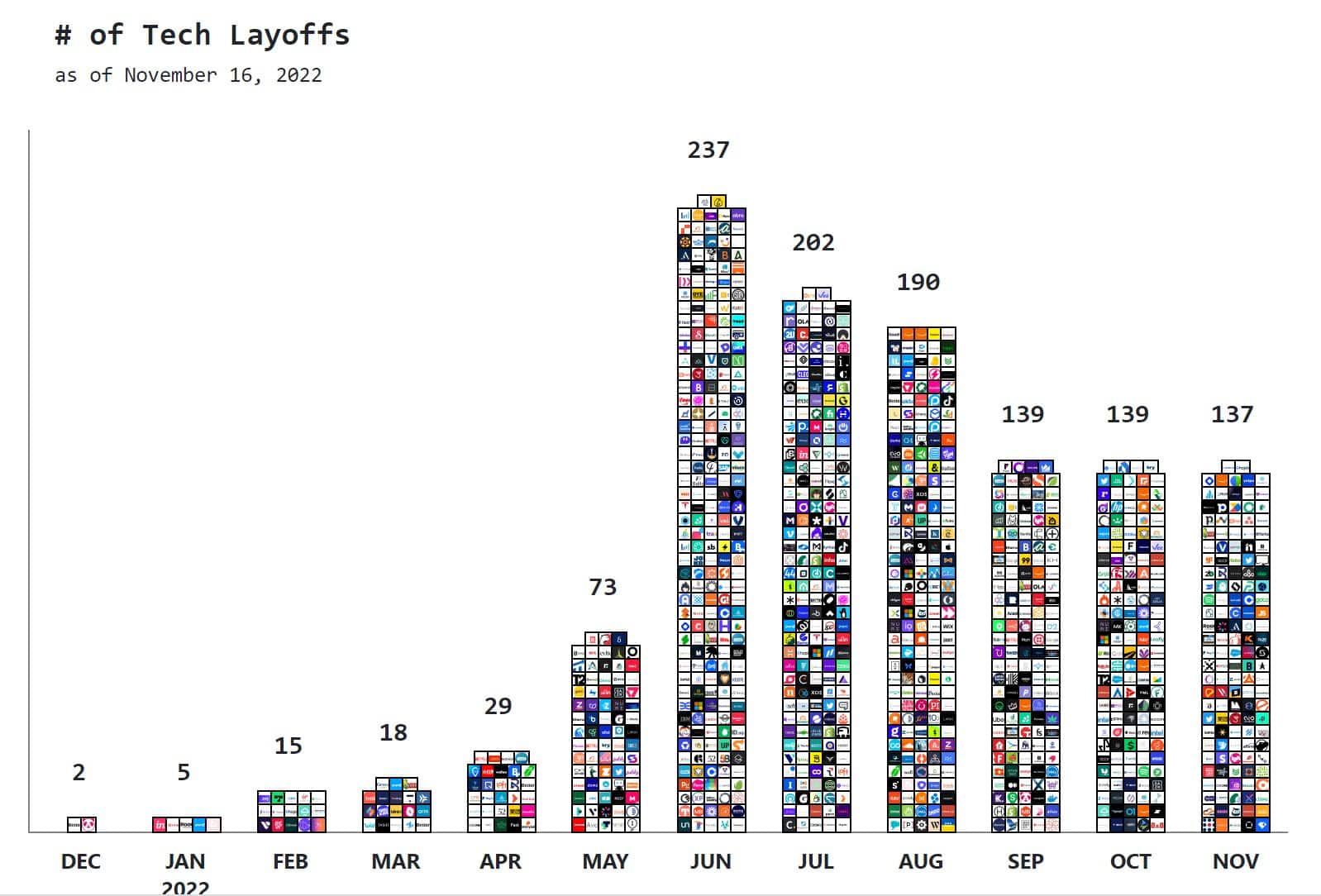

Meta cut 11,000 jobs. Twitter let 3,700 employees go. Stripe, Coinbase, and Microsoft all fired about 1,000 employees. The list of tech layoffs continues, and the media is hyping it. While the number of announcements of tech-related layoffs seems problematic, should we care about it from a broader macroeconomic viewpoint?

Per the BLS, information technology jobs constitute 1.8% of the workforce. Even in a depression where half of those jobs could be lost, the unemployment rate would only rise by 0.9%. During the 2008 recession, the unemployment rate increased by 4.5%. So while tech layoffs make for great headlines and likely attract many readers, they do not represent a big enough part of the economy to overly worry about. Further, many tech companies overstaffed over the last two years. Some of these layoffs are not necessarily economic warnings but a normalization of staffing to better match normalizing demand for tech products.

What To Watch Today

Economy

- 10:00 a.m. ET: Existing Home Sales, October (4.40 million expected, 4.71 million prior)

- 10:00 a.m. ET: Existing Home Sales, month-over-month, October (-6.6% expected, -1.5% prior)

- 10:00 a.m. ET: Leading Index, October (-0.4% expected, -0.4% prior)

Earnings

Market Trading Update

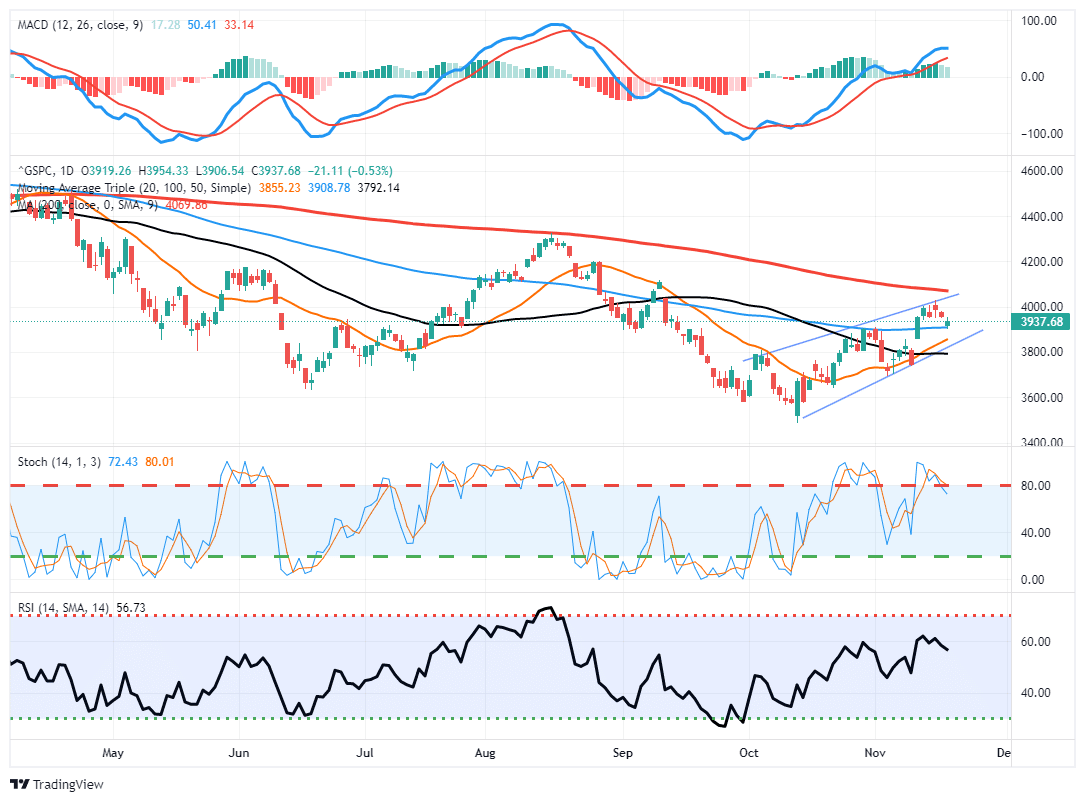

Tough talk from Fed officials (Daly and Bullard) put investors in a sour mood yesterday as the “pivot” was pushed out. While the market ended lower yesterday, the was buying in the early afternoon, with the market almost returning to breakeven before selling off into the close. This kind of action is bullish from a short-term standpoint and suggests that buyers continue to bid for stocks even on down days.

After running into the top of the rising trend channel, the market is seemingly in a healthy correction process. The market held support at the 50-dma, and the 20-dma is just below, which also defines the current uptrend. If these supports hold, another rally attempt into month-end will not be surprising. However, we suggest using any such rally to reduce risk and rebalance portfolio exposures. We suspect we could see some heavier selling in the first two weeks of December, which could retest recent lows.

December 15th- Dot Plot Warning

The Fed has numerous ways to convey its policy expectations to the market. The FOMC meetings, associated press conferences, and speeches and articles garner significant attention and alert investors to what the Fed is thinking. Not followed as closely are the quarterly Fed “dot plots.” The dot plots are each Fed member’s expectations for the Fed Funds rate, GDP, unemployment, and inflation. The September Fed Funds dot plot below is the latest release. The median estimate for year-end 2022 was 4.4%. The rate increases to a peak of 4.6% in 2023. Note that six members, at the time, thought Fed Funds would peak at 4.875% in 2023. As we share below, we believe the December 15th dot plots have the potential to stun the markets.

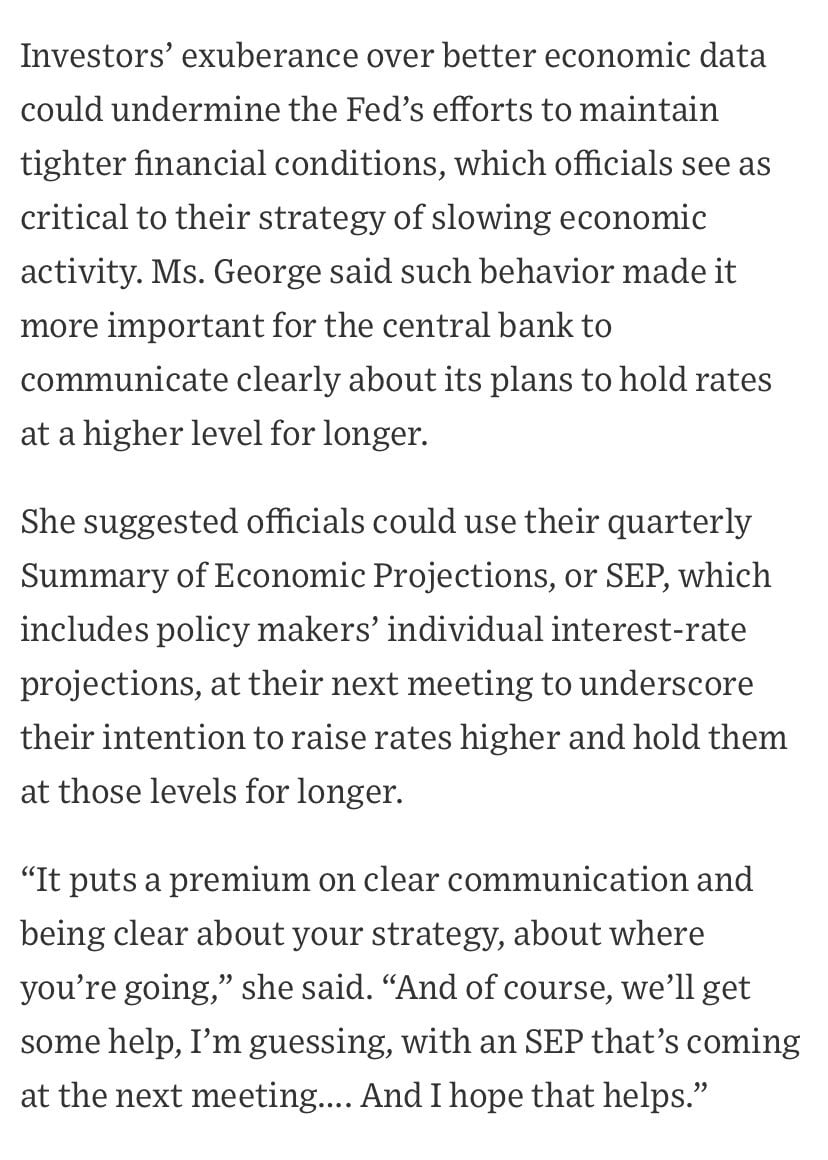

The Fed Funds futures market is in line with the September dot plots. The implied Fed Funds curve peaks in April at 4.91 and falls to 3.60 in two years. Recent comments by Fed President Esther George, shown below, make us think the Fed might use the dot plots in December to shock the markets. Pay close attention to the second paragraph. If the Fed takes this route, they might raise the terminal rate well above 4.91% and or increase 2024’s expectation to convey the Fed will not be pivoting anytime soon.

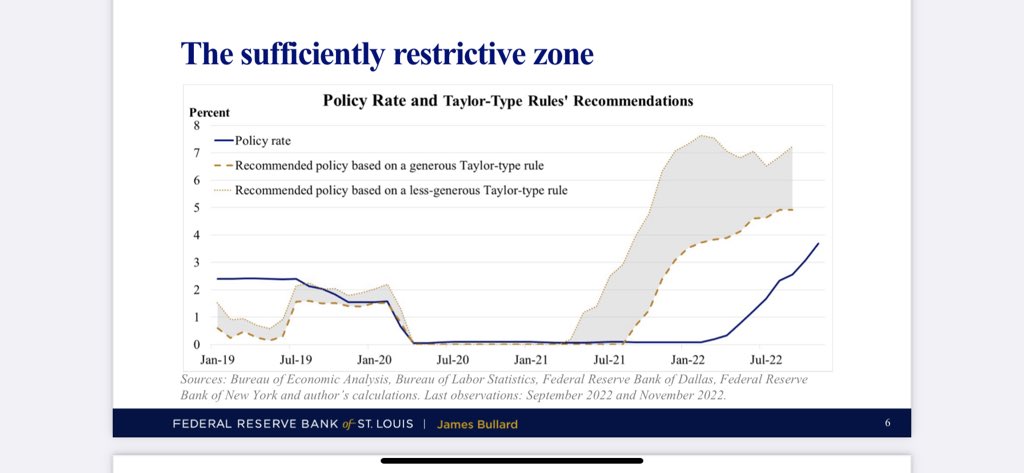

Bullard Piles on to the Hawkish Rhetoric

St. Louis Fed President Jim Bullard sent shivers through the markets on Thursday. In his presentation, he states:

“The policy rate is not yet in a zone that may be considered sufficiently restrictive.”

The graph below, from his discussion, claims a rules-based approach to monetary policy suggests the Fed Funds terminal rate should be above 5%. That rate may be as high as 7%. Stocks immediately fell upon learning that Fed Funds may increase more than anyone expects.

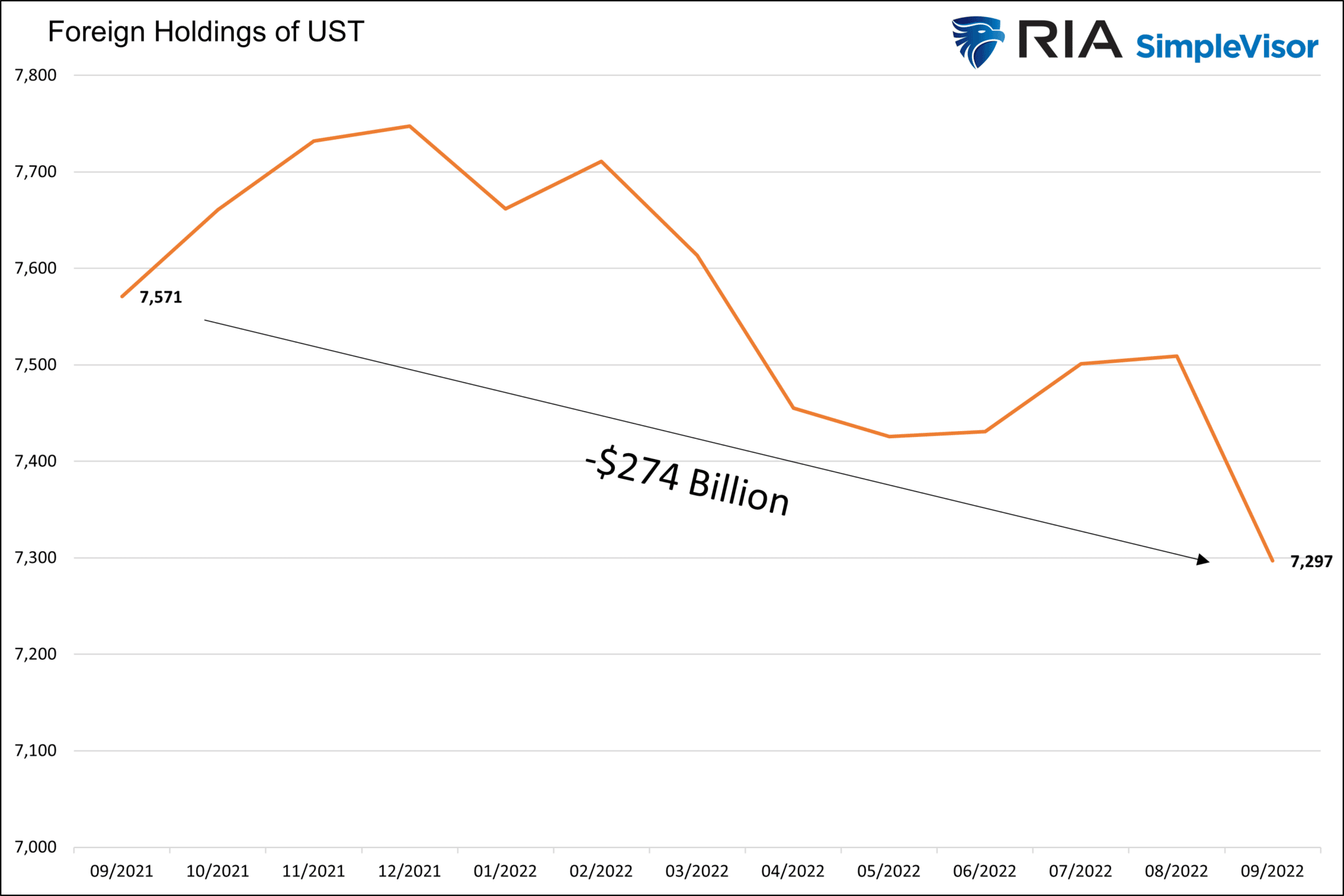

Foreigners Selling Treasury Bonds

We have noted in the past the likelihood that foreign nations are selling their holdings of U.S. Treasury bonds to help support their currencies versus the dollar. The latest round of data shows that this is indeed occurring. Foreign holdings of U.S. Treasuries fell to $7.297 trillion in September from $7.571 trillion a year ago. The largest holder, Japan, shed $179 billion of Treasury bonds. China, the second largest holder, sold $113 billion.

The problem is not just their selling. They are selling while the supply of bonds is increasing rapidly. Total debt outstanding rose by $2 trillion over the last year. Further, the Fed has added another $200 billion in its actions to reduce its balance sheet. We are bullish bonds because we think the Fed ultimately breaks something and causes economic deterioration and much lower inflation. However, we are mindful that the supply outlook is a factor working against us.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read