The Problem With Pragmatism… and Inflation

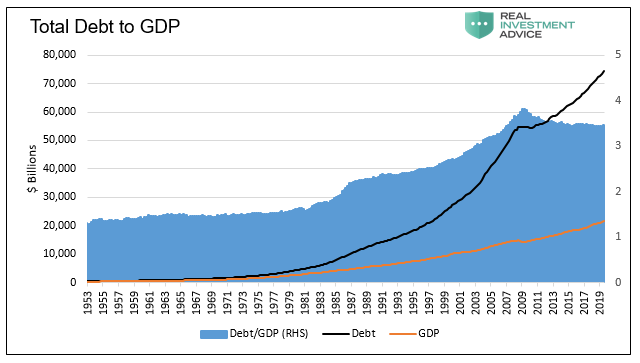

Pragmatism is seeking immediate solutions with little to no consideration for the longer-term benefits and consequences. An excellent example of this is the Social Security system in the United States. In the Depression-era, a government-sponsored savings plan was established to “solve” for lack of retirement savings by requiring contributions to a government-sponsored savings plan. At the time, the idea made sense as the population was greatly skewed towards younger people. No one seriously considered whether there would always be enough workers to support benefits for retired people in the future. Now, long after those policies were enacted and those that pushed the legislation are long gone, the time is fast approaching when Social Security will be unable to pay out what the government has promised.

Pragmatism is the common path of governments, led by politicians seeking re-election and the retention of power. Instead of considering the long-term implications of their policies, they focus on satisfying an immediate desire of their constituents.

In his book Economics in One Lesson, Henry Hazlitt made this point very clear by elaborating on the problems that eventually transpire from imprudent monetary and fiscal policy.

“The art of economics consists in looking not merely at the immediate but at the longer effects of any act or policy; it consists in tracing the consequences of that policy not merely for one group but for all groups.

Nine-tenths of the economic fallacies that are working such dreadful harm in the world today are the result of ignoring this lesson.”

Inflation

Inflation

One of the most pernicious of these issues in our “modern and sophisticated” intellectual age is that of inflation. When asked to define inflation, most people say “rising prices,” with no appreciation for the fact that price movements are an effect, not a cause. They are a symptom of monetary circumstances. Inflation is a disequilibrium between the amounts of currency entering an economic system relative to the productive output of that same system.

In today’s world, there is only fiat (“by decree”) currencies. In other words, the value of currencies are not backed by some physical commodity such as gold, silver, or oil. Currencies are only backed by the perceived productive capacity of the nation and the stability of the issuing government. If a government takes unreasonable measures in managing its fiscal and monetary affairs, then the standard of living in that society will deteriorate, and confidence in it erodes.

Put another way, when the people of a nation or its global counterparts lose confidence in the fiscal and monetary policy-makers, the result is a loss of confidence in the medium of exchange, and a devaluation of the currency ensues. The influence of those in power will ultimately prove to be unsustainable.

Inflation is an indicator of confidence in the currency as a surrogate of confidence in the policies of a government. It is a mirror. This is why James Grant is often quoted as saying, “The gold price is the reciprocal of the world’s faith in central banking.”

Confidence in a currency may be lost in a variety of ways. The one most apparent today is creating too many dollars as a means of subsidizing the spending habits of politicians and the borrowing demands of corporations and citizens.

Precedent

There is plenty of modern-day historical precedent for a loss of confidence from excessive debt creation and the inevitable excessive currency creation. Weimar Germany in the 1920s remains the modern era poster child, but Zimbabwe, Argentina, and Venezuela also offer recent examples.

Following the 2008 financial crisis, many believed that the actions of the Federal Reserve were “heroic.” Despite failing to see the warning signs of a housing bubble in the months and even years leading up to the crisis, the Fed’s perspective was that it exists to provide liquidity. As the chart below illustrates, that is precisely what they did.

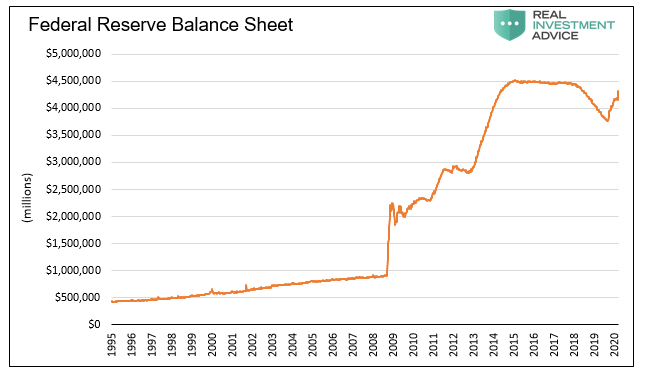

Data Courtesy Bloomberg

That pragmatic response failed to heed Hazlitt’s warning. What are the longer-term effects for the economy, the bailed-out banking system, and all of us? How would these policies affect the economy, markets, society, and the wealth of the nation’s citizens in five, ten, or twenty years?

Keeping interest rates at a low level for many years following the financial crisis while the economy generally appears to have recovered raises other questions. The Fed continues to argue that inflation remains subdued. That argument goes largely undisputed despite credible evidence to the contrary. Further, it provides the Fed a rationalization for keeping rates well below normal.

Politicians who oversee the Fed and want to retain power, consent to low-rate policies believing it will foster economic growth. While that may make sense to some, it is short-sighted and, therefore, pragmatic. The assessment does not account for a variety of other complicating factors, namely, what may transpire in the future as a result? Are seeds of excess being sown as was the case in the dot-com bubble and the housing bubble? If so, can we gauge the magnitude?

Policy Imposition

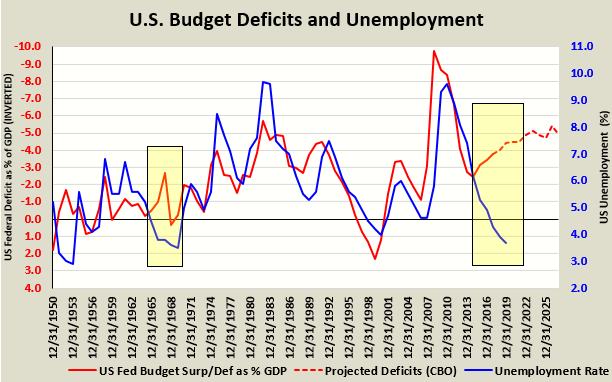

In the mid-1960s, President Lyndon Johnson sought to escalate U.S. involvement in the Vietnam War. In doing so, he knew he would need the help of the Fed to hold interest rates down to run the budget deficits required to fund that war. Although then-Fed Chairman William McChesney Martin was reluctant to ease monetary policy, he endured various forms of abuse from the Oval Office and finally acquiesced.

The bullying these days comes from President Trump. Although his arguments for easier policy contradict what he said on the campaign trail in 2016, Jerome Powell is compliant. Until recently, the economy appeared to be running at full employment and all primary fundamental metrics were well above the prior peaks set in 2007.

Additionally, Congress, at Trump’s behest and as the chart below illustrates, has deployed massive fiscal stimulus that created a yawning gap (highlighted) between fiscal deficits and the unemployment picture. This is a divergence not seen since the Johnson administration in the 1960s (also highlighted) and one of magnitude never seen. As is very quickly becoming clear, those actions both monetary and fiscal, were irresponsible to the point of negligence. Now, when we need it most as the economy shuts down, there is little or no “dry powder”.

Data Courtesy Bloomberg

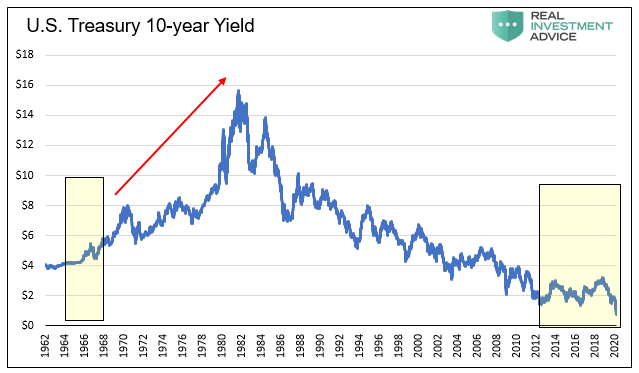

President Johnson got his way and was able to fund the war with abnormally low interest rates. However, what ensued over the next 15 years was a wave of inflation that destroyed the productive capacity of the economy well into the early 1980s. Interest rates eventually rose to 18%, and economic dynamism withered as did the spirits of the average American.

The springboard for that scenario was a pragmatic policy designed to solve an immediate problem with no regard for the future. Monetary policy that suppressed interest rates and fiscal policy that took advantage of artificially low interest rates to accumulate debt at a relatively low cost went against the American public best interests. The public could not conceive that government “of, by and for the people” would act in such a short-sighted and self-serving manner.

Data Courtesy Bloomberg

The Sequel

Before the COVID-19 pandemic, the Congressional Budget Office (CBO) projections for U.S. budget deficits exceeded $1 trillion per year for the next 10-years. According to the CBO, the U.S. Treasury’s $22.5 trillion cumulative debt outstanding was set to reach $34.5 trillion by 2029, and that scenario assumed a very optimistic GDP growth of 3% per year. Further, it laughably assumed no recession will occur in the next decade, even though we are already in the longest economic expansion since the Civil War. In the event of a recession, a $1.8 trillion-dollar annual deficit would align with average historical experience. Given the severity of what is evident from the early stages of the pandemic, that forecast may be very much on the low end of reality.

The 1960s taught us that monetary and fiscal policy is always better erring on the side of conservatism to avoid losing confidence in the currency. Members of the Fed repeatedly tell the public they know this. Yet, if that is the case, why would they be so influenced by a President focused on marketing for re-election purposes? Alternatively, maybe the policy table has been set over the past ten years in a way that prevents them from taking proper measures? Do they assume they would be rejected despite the principled nature of their actions?

Summary

Inflation currently seems to be the very least of our worries. Impeachment, Iran, North Korea and climate change were all crisis head fakes.

The Fed was also distracted by what amounted to financial dumpster fires in the fall of 2019. After a brief respite, the Fed’s balance sheet began surging higher again and they cut the Fed Funds rate well before there was any known threat of a global pandemic. What is unclear is whether imprudent fiscal policies were forcing the Fed into imprudent monetary policy or whether the Fed’s policies, historical and current, are the enabler of fiscal imprudence. Now that the world has changed, as it has a habit of doing sometimes even radically, policymakers and the collective public are in something of a fine mess to understate the situation.

Now we are contending with a real global financial, economic, and humanitarian threat and one that demands principled action as opposed to short-sighted pragmatism.

The COVID-19 pandemic is clearly not a head fake nor is it a random dumpster fire. Neither is it going away any time soon. Unlike heads of state or corporate CEOs, biological threats do not have a political agenda and they do not care about the value of their stock options. There is nothing to negotiate other than the effectiveness of efforts required to protect society.

Given the potential harm caused by the divergence between stimulus and economic fundamentals, it would be short-sighted and irresponsibly pragmatic to count out the prospect of inflation. Given the actions of the central bankers, it could also be the understatement of this new and very unusual decade.