Various politicians and a Fed member have recently claimed that the recent bout of high inflation was due to pandemic-related production and transportation shortages. They are correct in that the reduced supply of goods and services is undoubtedly a cause of inflation. However, this convenient excuse seems to take the blame away from themselves. Excessive fiscal and monetary policy used to boost economic growth during the pandemic drove demand well above any pre-pandemic norm. The fact is that reduced supply AND strong demand led to inflation.

Massive fiscal spending, including direct checks to citizens, generous unemployment benefits, student loan relief, mortgage forbearance, and other financial benefits, provided citizens and companies with money to spend. Those holding on to their jobs were better off financially than if the pandemic had never occurred. The graph below from the San Francisco Federal Reserve proves our point. It quantifies how supply and demand-driven factors contribute to CPI. As shown, the demand-driven inflation (blue) and supply-driven inflation (green) bars in 2021 and 2022 were larger than before the pandemic. They have started to normalize over the last year.

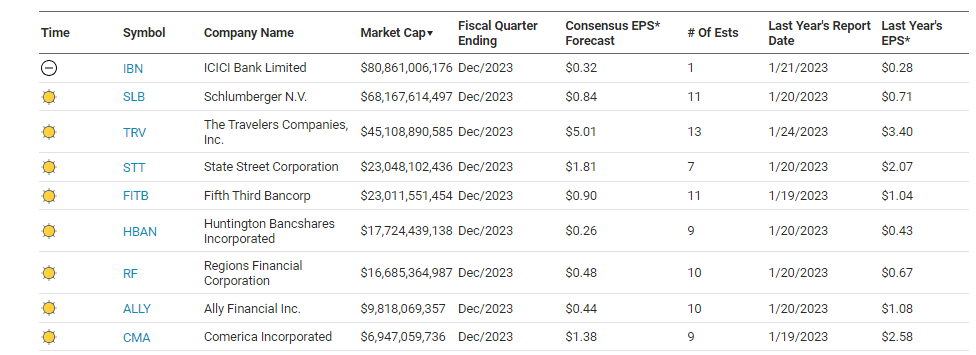

What To Watch Today

Earnings

Economy

Investing Summit: Early Bird Registration Available Now

January 27th, we are hosting a live event featuring Greg Valliere to discuss investing in the 2024 presidential election. What will a new president mean for the markets, the risks, and where to invest through it all? Greg will be joined by Lance Roberts, Michael Lebowitz, and Adam Taggart for morning presentations covering everything you need to know for the New Year.

Register now, as there are only 150 seats. The session is a LIVE EVENT, and no recordings will be provided.

Market Trading Update

Yesterday, the market opened higher after Wednesday’s decline but fell to almost unchanged in the afternoon. However, the market then surged back to life with little newsflow other than the Senate passing a stopgap funding measure, which offset the earlier concerns from Raphael Bostic, who suggested the Fed wouldn’t cut rates until the 3rd quarter.

In such an unpredictable environment, it would be unwise to lock in an emphatic approach to monetary policy. That is why I believe we should allow events to continue to unfold before beginning the process of normalizing policy. My outlook right now is for our first cut to be sometime in the third quarter this year, and we’ll just have to see how the data progress.”

With the relief of the stopgap funding measure, stocks soared into the close. However, they remain within the ongoing consolidation range that has existed since mid-December. That rally put the market back above the 20-DMA, which remains bullish while the overbought conditions continue to reverse.

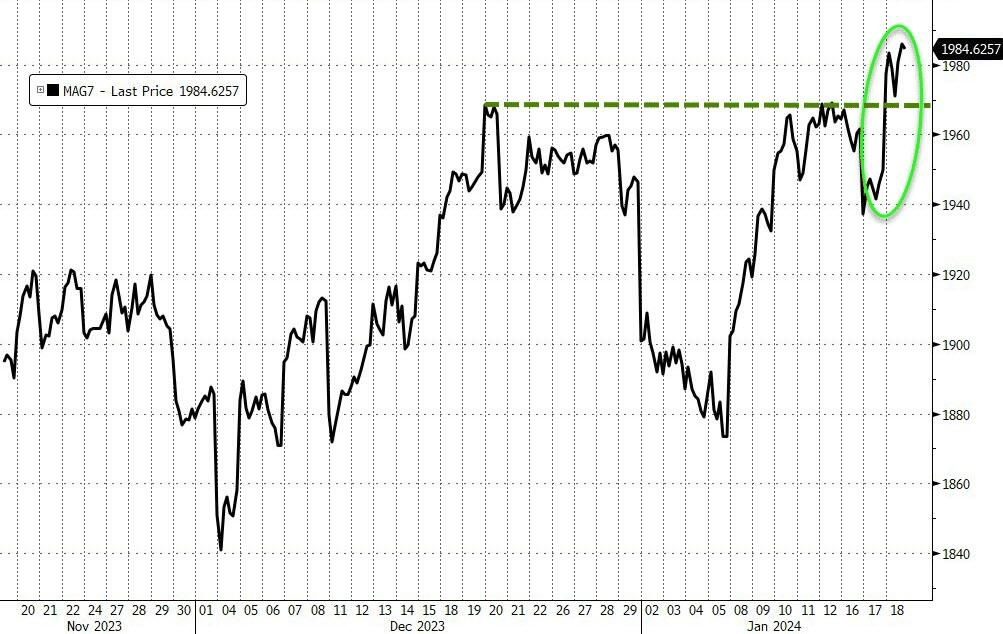

However, we have been looking for a rotation from the “Magnificent 7″ to more undervalued, unloved stocks. Such is not the case as of late as money continues to chase the mega-cap names.

The market is likely getting close to the end of this ongoing consolidation, and a breakout above the recent highs will confirm the market’s next move is higher. Continue to manage risk and wait for the breakout to add exposure.

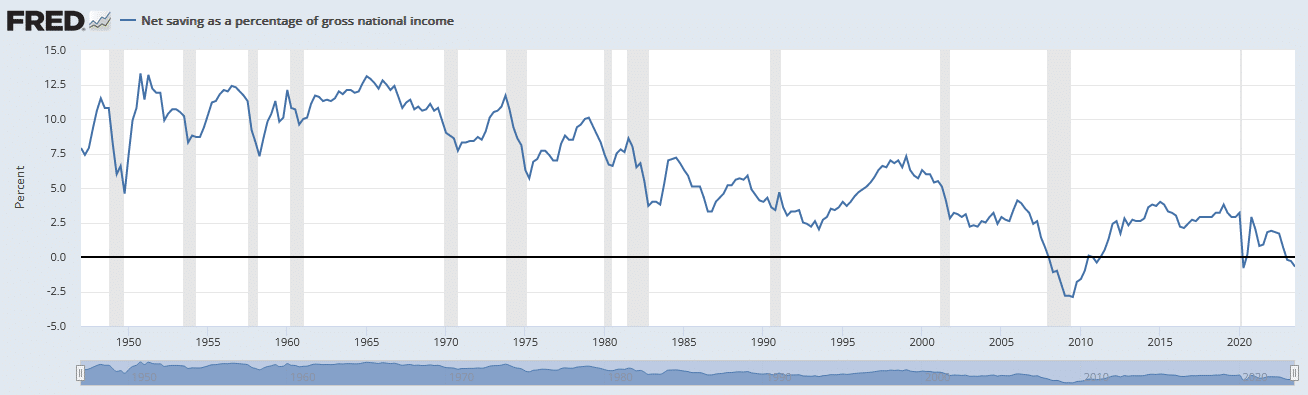

Net Savings Are Negative

Recently, we have discussed how the increased usage of Buy-Now-Pay-Later Loans and credit cards was employed to help fund holiday buying. We are also concerned that high debt balances incurred during the holiday season may result in weaker consumption as consumers must now pay off the debt.

The graph below, charting the nation’s aggregate net savings as a percentage of income, sheds more light on the topic. In total, consumers spent more than they earned in recent months. Such has only happened twice in the last 75 years. Assuming net savings return to positive territory in the coming months, there may not be much to worry about. However, if net savings continue below zero and the labor market weakens, the odds of a recession become much more worrisome. Simply, negative net savings are not sustainable. Either debt is defaulted on, or savings must increase, resulting in less consumption.

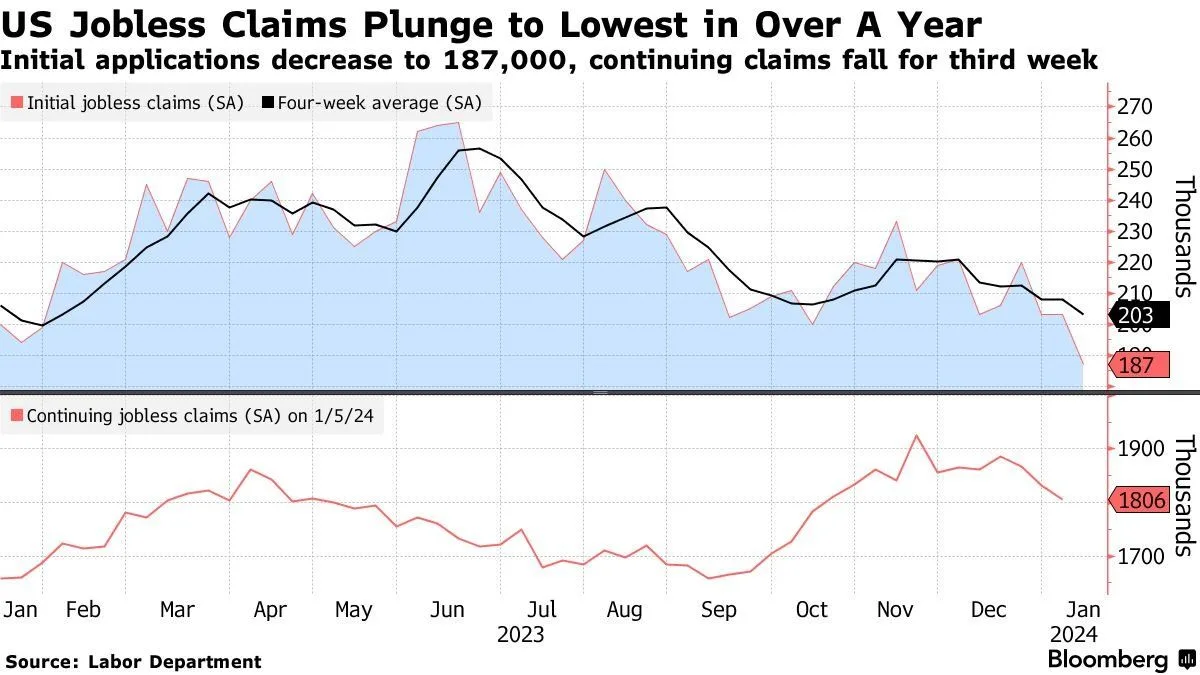

Initial Jobless Claims Signal A Strong Job Market

Despite a few concerning stats in December’s BLS employment report, initial jobless claims tell us all is well. Per Zacks:

Intitial Jobless Claims for last week dropped below 200K for the first time since February of last year: 187K, the smallest amount of new jobless claims since January of last year. It’s also -16K below the already low (though slightly upwardly revised) 203K the previous week. This is as clear a sign as any — and as granular an economic print as we’re likely to see anywhere — that domestic employment continues to roll along strongly, as robust an indication that a recession remains off the foreseeable horizon.

Continuing Claims, which a couple months ago looked like it was heading to 2 million in short order (1.925 million in mid-November), fell back meaningfully again to 1.806 million — the lowest print since October of last year, prior to the ramp-up in longer-term jobless claims. Gone are the half-century lows of 1.6 million we were seeing during the Great Reopening, but this morning’s tally is beneath the already-low 1.832 million revision for the previous week. Again: a robust job market. This is currently the case for the short-term and long-term.

Despite the market’s obsession with the monthly BLS report, jobless claims are more meaningful data. Unlike the BLS reports, it is not survey-based. Instead, it relies on actual jobless claim submissions from each state.

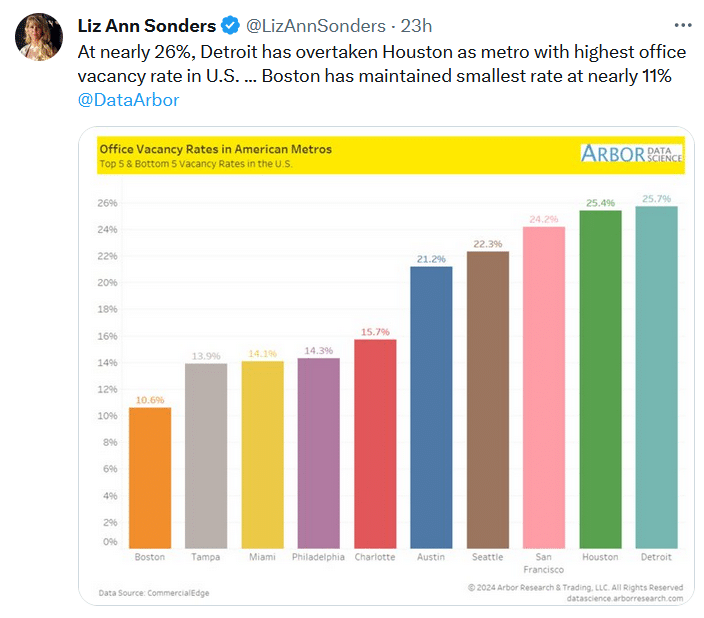

Tweet of the Day

“Want to have better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.