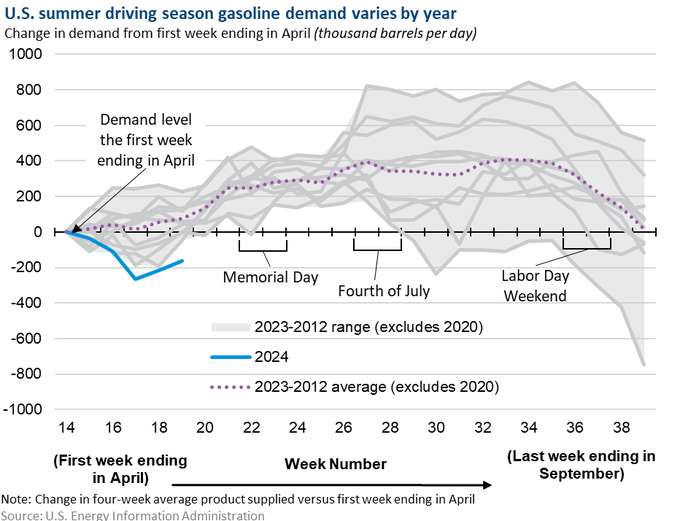

Summer driving season, lasting from Memorial Day to Labor Day is fast approaching. Typically, during driving season, U.S. motor gasoline consumption is 400,000 barrels/day above the average for spring and fall. As shown below, gasoline consumption has run at its lowest since 2012.

Typically, above-average consumption rates start ramping up in April. Yet, this year, they have declined in April and early May. Whether this is related to the timing of Easter, which fell in March, or the weather has yet to be seen. However, if they continue to be below normal, especially after Memorial Day, this will serve as another indicator that consumers are cutting back on spending.

What To Watch Today

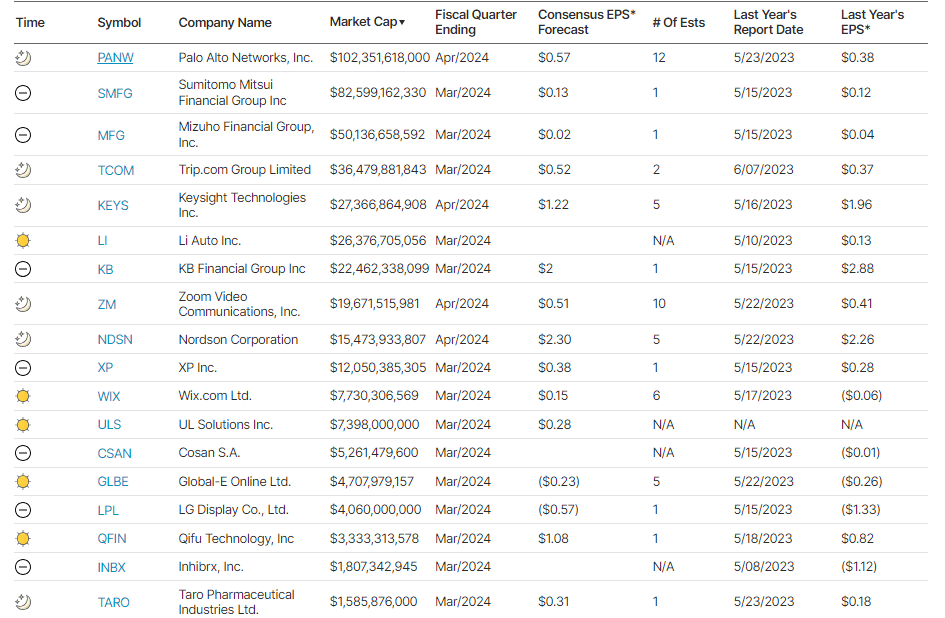

Earnings

Economy

Market Trading Update

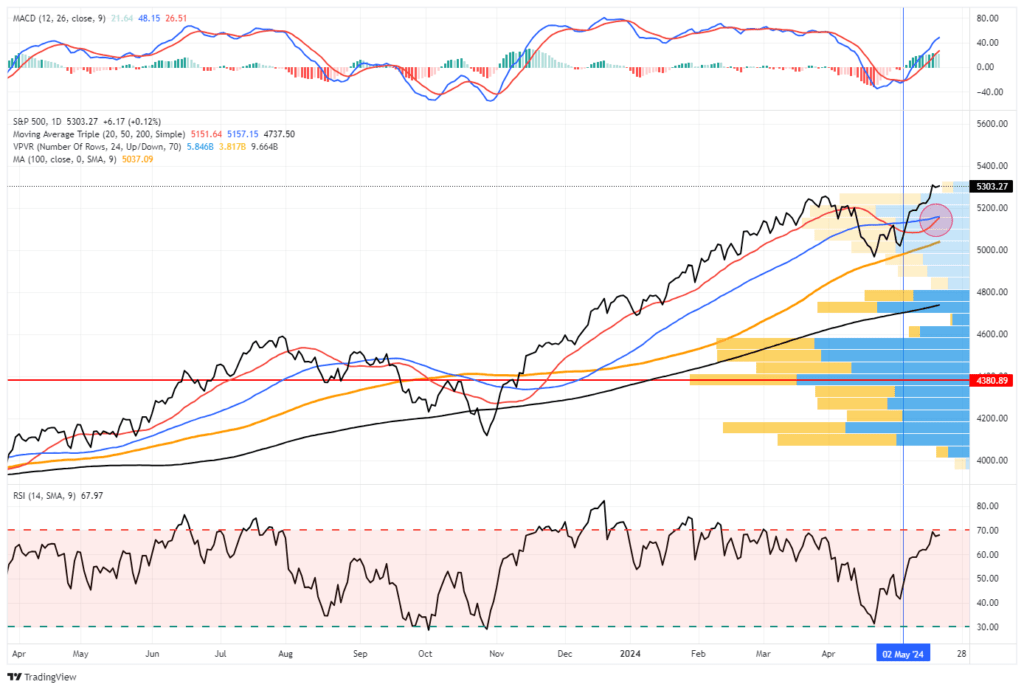

Last week, we discussed that the April correction was likely over.

“Notably, the breakout above key resistance and the reversal of the volatility index suggest that the recent correction is over. However, while the April correction may be over, as noted above, there is still a decent probability of another correction before the Presidential election in November. As shown below, such tends to be a statistical normality during Presidential election years.”

This past week, markets surged to all-time highs as a plethora of bad economic data and a weaker-than-expected inflation print lifted hopes of Fed rate cuts in the coming months.

From a technical perspective, the markets remain on a current MACD “buy signal” and have cleared all previous resistance levels. Furthermore, the 20-DMA is set to cross above the 50-DMA next week, providing additional support to any short-term market correction. We should expect a pullback or consolidation with the market overbought on multiple levels. Such consolidations will provide a better entry point for investors who need to increase equity exposures.

The Week Ahead

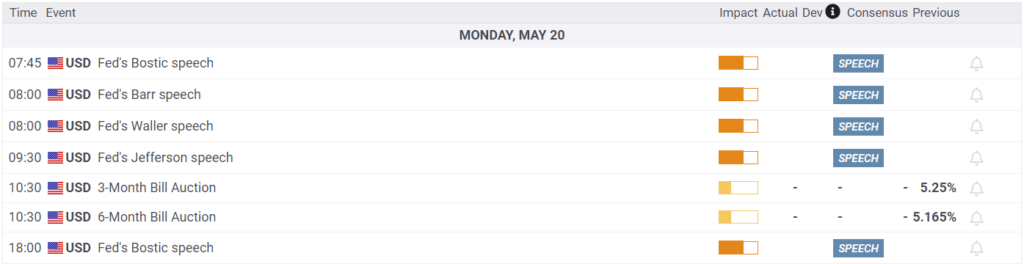

This week will be light on the economic data front. Today and tomorrow will feature a flurry of Fed speakers, including Bostic, Barr, Waller, and Jefferson. Wednesday will bring S&P flash PMIs, April New and Existing Home Sales data, and FOMC Minutes. We suspect the Fed speakers will stick to their recent narratives this week, keeping the door open for rate cuts toward the end of this year.

The Flash PMIs will provide a preliminary look at manufacturing and services trends for May. New Home Sales are expected to decline to 0.68 million from 0.693 million in March. Meanwhile, Existing Home Sales are forecast to decrease to 4.18 million from 4.19 million in March. High interest rates continue weighing on existing home sales, with many would-be sellers locked into low-rate mortgages.

We cap off this week with Durable Goods Orders data for April and May consumer sentiment figures. Growth in durable goods orders is forecast to decline to 0.5% MoM, following 2.6% growth in March. Finally, the consensus estimate is for consumer sentiment to decline to 67.4 in May from 77.2 in April.

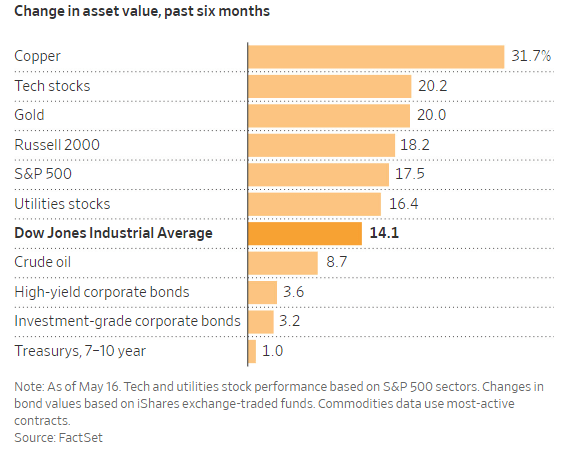

The Everything Rally Continues

The DOW hit the 4,000 mark for the first time in history last week following a solid earnings season. As shown below, many major asset classes have risen in concert over the past six months. A combination of robust earnings, low unemployment, and optimism surrounding AI advancements have driven gains in equities. Attractive yields have pulled money into the bond market. Meanwhile, precious and industrial metals have surged on the trifecta of a bullish economic backdrop, investor interest, and tightening supply in physical markets. Meme stocks are even back in vogue, with sharp rallies in yesteryear’s favorites over the past week. The question remains whether weakening economic data will eventually catch up with markets. For now, however, the Everything Rally continues.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.