Stock Buybacks and the Principal/Agent Problem

“The single greatest edge an investor can have is a long term orientation.” – Seth Klarman

The most recent Nobel Prize in economics was awarded to Oliver Hart and Bengt Holmstrom for their work on how corporate contracts and incentives effect corporations. Among their many findings they discussed how incentive-laden contracts meant to solve one problem tend to create new ones.

Based on a similar premise, we wrote a series of articles discussing stock buybacks and the harm they tend to cause to the long-term financial health of corporations and ultimately the economy. In the series, we are critical of executives motivations and the incentive structures in place that reward them handsomely for share price performance with little regard for the harm they might be doing to the long-term success of the company. The blame, however, is not just on executives and we would be remiss if we did not expand on the complicit role that shareholders play and their motivations to support executives that authorize share buybacks. When considering investors’ hunger for returns in the current extremely low interest rate environment, one better understands why corporate executives are under significant pressure from shareholders to conduct share buybacks.

The Principal-Agent Theory affords a framework from which we might develop a better appreciation for the recent popularity of buybacks. It supports the idea that shareholders are complicit partners with executives in conducting buybacks. The first step in that process requires being clear about how we should define “shareholder.” A more thorough understanding of the fundamental aspects of these dynamics, as offered here, allows for better corporate and macroeconomic analysis as well as ideas about what can be done to true-up false perceptions of value.

While this article, and the series of articles we have written on buybacks, may seem theoretical and academic it is a vital topic for investors to understand. Equity prices and corporate bond yields are based on expected earnings and cash flows. Investors may cheer buybacks today but the true cost of these transactions is steep will be extracted in the future. Failure to properly consider the cost-benefit analysis of buybacks will leave many investors at a loss to understand what went wrong with their forecasts.

Principal-Agent Theory

The Principal-Agent Problem occurs when one group, the agents, can make decisions that adversely affect another group, the principals. In the world of corporate management, the agents are the executives of corporations while the shareholders and to some degree the nation’s populace are the principals.

In the early 1970’s, economists began to argue that the motives of agents (executives) were different from those of the principals (shareholders), thus in their opinion a principal-agent problem existed. To align the interests of executive and shareholders, economists promoted a theory that executives should be given financial incentives derived from corporate stock performance. Over the last 35 years, so-called “principal-agent economists” have successfully influenced boards of directors to bestow upon executives attractive, stock-laden incentives. These rewards, in turn, motivate executives to inflate stock prices at all cost.

The guiding principle behind such incentives is that higher share prices represent increased shareholder value. While true, this is unfortunately very short sighted. Advocates of this view fail to consider that many actions designed to boost share prices in the short term can have negative effects on the company in the long run. When an executive, for example, decides to forgo investment into a capital project and instead repurchases shares, they may push the price of their company’s stock higher, but that same decision reduces the company’s profit potential. Not only are the decisions made by an executive with a one or two-year time horizon very different from decisions made by an executive with a ten or twenty-year time horizon, but they are habit-forming in the worst way. True long-term shareholders and the prosperity of the nation as a whole suffer when the habits of short-termist logic take hold.

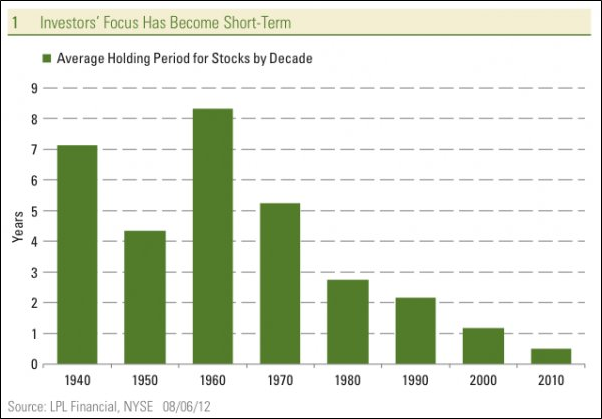

To illustrate the point, consider the graph below courtesy LPL Financial. From the 1940’s through the 1970’s the average holding period for equity investors was six years. Today, the average holding period has dramatically shrunk to about six months. While there are still investors that hold shares for longer time frames, most principles turn over their stock holdings much more frequently. The proper term for these short-term investors is not shareholders but rather speculators or traders who temporarily own the securities of a company. The vast majority of shareholders are not investors at all but renters with little concern for the circumstances of the company beyond their very brief holding period.

Now consider the principal-agent relationship once again. The motives of management are currently aligned with the large majority of shareholders. Both groups want a higher share price so they can profit immediately. Executives profit as their compensation package increases in value and shareholders benefit from increases in their portfolio values. Neither party is incentivized to invest in the future with an eye toward profitability of the company in the long run. While the principal-agent relationship appears to be in sync, the relationship is based on the false premise of what represents shareholder value. This relationship improperly defines “shareholder” and egregiously neglects long-term investors, employees, communities, the economy and the populace at large.

As explained in “The Death of the Virtuous Cycle,” and a video we produced “The Animated Virtuous Cycle,” savings and investment are key to increasing productivity which fuels economic growth and national prosperity. A balanced allocation of investment into corporate capital projects allows for enhancements to the production process, the benefits of which are bestowed not only on corporations but the laborers and the population as a whole. Alternatively, when cash flow derived from profits or debt issuance, are distributed to shareholders through share repurchases, it serves no long-term productive purpose. The intention is to alter the optics of the company’s financial statements, boost the stock price and thereby bolster executive bonuses.

Share buybacks do indeed cause earnings per share to grow by reducing the denominator, but they do not grow top-line revenue or improve the company’s market position in any way. Meanwhile, capital projects are intended to produce organic growth in revenue and earnings, but they also introduce both business risk and execution risk. In the short run, share buybacks appear to be riskless. Hence, for “shareholders” who do not intend to maintain an interest in a company for more than a few months, their preference is for the company to grow earnings per share by engaging the “no-risk” option of buybacks.

A Solution

The concept of “maximizing shareholder value” as the over-arching determinant in corporate decision-making is seriously flawed and responsible in part for the growing misallocation of corporate capital. (Evidence supporting that idea may be found in that over the last ten years S&P 500 corporations have returned more money to shareholders via share buybacks and dividends than they have earned) As previously discussed, the characteristics of shareholders differ markedly today from forty years ago. Mandating the maximization of shareholder value also fails to capture the broader obligations of the agents to those who represent true stakeholders in the organization. Executives should be incentivized to promote the long-term health of their company, the prosperity of the employees who work for it and the communities in which the employees live and do their work. These objectives contrast sharply with current decision-making behavior and demands balanced investment decisions, discipline and quite often a measure of sacrifice in the short-run.

If we eliminate the theory that there is a principal-agent problem, we could radically reduce this perversion of the system imposed by extreme and misplaced financial incentives. The idea seems straight-forward until we realize that corporate executives responsible for strategic decision-making are also the beneficiaries of the maximize shareholder value concept to the tune of billions in compensation. Can corporate boards be convinced that such a change is required and are they willing to enforce such a change? That hinges on the independence of the board itself. Anyone who espouses such ideas likely will not find themselves within a Texas mile of a corporate board seat. Without regard for the logic of the argument, asking corporate executives to behave in such an altruistic manner is naïve. Despite the fact that current decisions to use precious cash for purposes of buybacks are in almost every case negligent, it will not change from the inside out.

Special thanks to Clayton Christensen whose research inspired this article.

Michael Lebowitz, CFA is an Investment Analyst and Portfolio Manager for RIA Advisors. specializing in macroeconomic research, valuations, asset allocation, and risk management. RIA Contributing Editor and Research Director. CFA is an Investment Analyst and Portfolio Manager; Co-founder of 720 Global Research.

Follow Michael on Twitter or go to 720global.com for more research and analysis.

Customer Relationship Summary (Form CRS)

Also Read