As a small part of the recent omnibus bill, the SECURE Act 2.0 is now a reality. Investors need to know about H.R. 2954 and additional provisions to enhance retirement readiness. The SECURE Act 2.0 is the combination of three separate bills.

First, the bipartisan measure is a strong incentive for diligent savers and wealthier investors wrapped up in a bountiful bow for Wall Street and financial services firms.

Remember, over half of American households don’t or can’t save enough for retirement. The SECURE Act is like a shiny new car they can’t afford to drive.

As a result, several formidable changes are coming in 2023. Here’s what investors need to know about the SECURE Act 2.0.

Required Minimum Distributions get another overhaul.

RMDs are distributions that investors of a specific age must take from retirement accounts. For 2023, the newest legislation raises the RMD age to 73 and 75 beginning January 1, 2033.

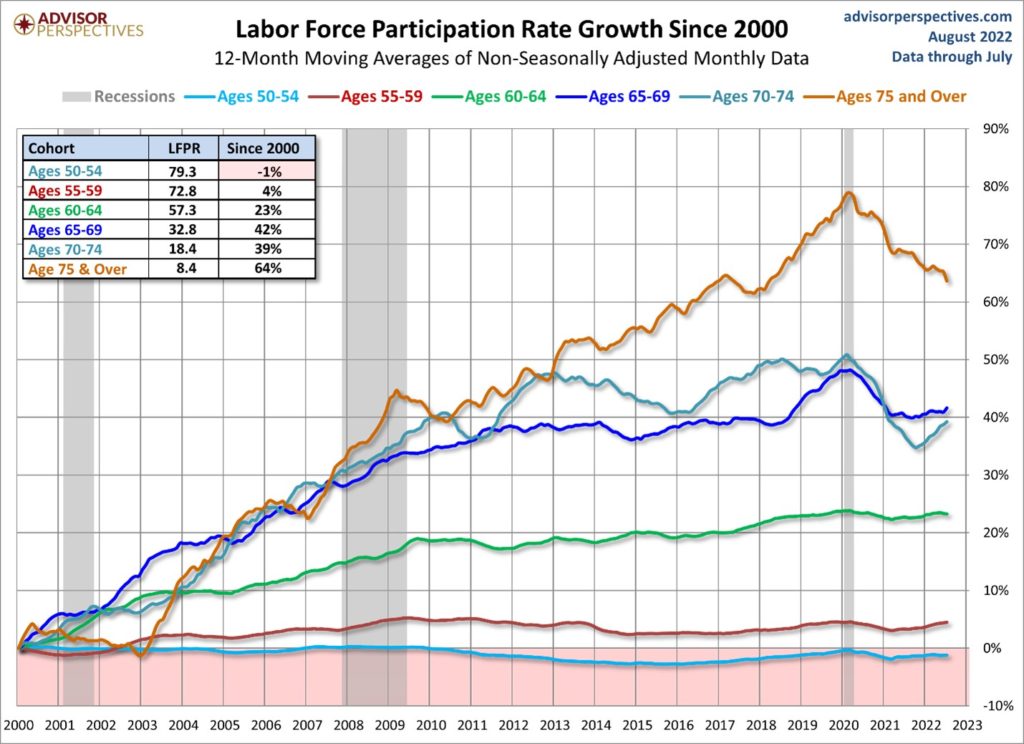

This change makes sense—sort of. Although Labor Force Participation has fallen since 2020, there’s no doubt long term that older workers remain in the workforce longer. I expect 60 and 70-somethings to continue working for several reasons, primarily due to longer life expectancies and inadequate retirement savings: A deadly combination.

So, for some, an RMD is a nuisance and unnecessary as distributions result in forced tax liability. But, according to IRA specialist and CPA Ed Slott, over 80% of people subject to RMDs withdraw more than the minimum because they need the money.

At RIA, our financial planning team advocates unconventional wisdom. In other words, investors should draw down their pre-tax retirement accounts before their RMD deadlines and convert the proceeds to Roth or deposit them in after-tax accounts for greater tax control throughout retirement.

Unfortunately, the bill does not clarify the ten-year rule for distributions from non-spousal IRAs inherited in 2020 and 2021. The IRS is waiving withdrawal penalties on non-spousal inherited IRAs until 2023. Click here to read. I expect the IRS to provide a formal ruling (hopefully) by mid-year.

Penalty relief for late RMDs.

Next, the onerous 50% excise tax for missing required minimum distributions is reduced to 25%, and if corrected promptly, the penalty is reduced to 10%. A correction window is defined as the period of time beginning when the tax is imposed concerning a shortfall from a retirement plan.

So, what is the window?

The earlier the date the IRS demands payment or the last day of the second taxable year that begins after the end of the taxable year in which the tax is imposed. For example, if you miss your RMD in 2023, you’ll have the earliest when notified, or December 31, 2024, to take the distribution.

The excise tax on excess contributions relief.

Also, it’s not uncommon to accidentally overcontribute to retirement accounts. Remember that a 6% excise tax is owed yearly as long as the excess remains in the account.

In the SECURE Act 2.0, a statute of limitations has been created. Taxpayers have three years from when a return would have been required to be filed, excluding extensions.

One-time election for Qualified Charitable Distributions to split-interest entities.

Qualified Charitable Distributions are popular for RMD retirees who look to donate directly to a qualified charity from their retirement accounts. Distributions cannot exceed $100,000 a year. The SECURE Act 2.0 allows a $50,000 one-time deductible contribution to fund a charitable remainder annuity or unitrust.

Retroactive first-year elective deferrals for sole proprietors.

For sole proprietors looking to establish Solo 401ks, they have until their tax filing deadlines (without extensions) to fund a plan. Previously, these retirement accounts required establishment and funding by December 31. Under the new rules, individual business owners have until their tax filing deadline in 2023 to establish and fund their Solo 401k accounts for 2022.

Retirement savings lost and found.

On average, workers change jobs six times during their lifetimes. I expect that multiplier to increase due to post-pandemic work trends. Along the way, they collect retirement accounts like Beanie Babies and forget they exist.

Also, in consultation with the Treasury Department, the Secretary of Labor will establish an online searchable database for forgotten or ‘lost’ retirement plans within two years. Account holders will be able to locate the plan administrators and contact information.

Expanding automatic enrollment in newly-establishment retirement plans.

Newly created 401k or 403b plans will require, during the first year of participation, no less than 3% and not more than 10% unless the participant specifically elects not to have such contributions made or select contributions at a different percentage. Businesses in existence for less than three years are exempt.

Modification of credit for small employer pension plan startup costs.

An employer with 50 employees or fewer is eligible for an enhanced tax credit for start-up plans beginning January 1, 2023. The credit will cover 100% of the startup costs of up to $5,000 for three years. Businesses with more than 50 employees will still receive tax credits subject to limitations based on dollars and a credit phase-in based on the number of employees exceeding 50.

Enhancement of Saver’s Credit.

To encourage retirement savings, the Act outlines a simple 50% refundable saver’s credit rate subject to AGI limitations and phaseouts. In the case of a joint return, the AGI threshold is $48,000, with a phaseout of full credit beginning at $35,000 for couples filing jointly. Single filers would phase out at AGIs over $24,000.

The Saver’s Credit threshold and phaseout amounts adjust for inflation after 2026. The enhancement to the Saver’s Credit applies to taxable years beginning after December 31, 2026.

Indexing IRA catch-up limit as part of the SECURE Act 2.0 – what investors need to know.

The $1,000 IRA catch-up limits for people aged 50 and over, indexed for inflation beginning in 2024. Catch-up contributions to retirement plans increase from $6,500 to $10,000 for eligible participants who would attain the ages 62, 63, 64, but not 65 before the close of 2023. Also, these catch-ups index for inflation.

Treatment of student loan payments as elective deferrals for purposes of matching contributions.

Student loan debt payments are 401(k), 403(b), or SIMPLE IRA employee deferrals and qualify for employer plan matching. As a result, an employee can qualify for matching contributions by making student loan payments and, at the same time, save for retirement, thanks to their employer.

Small immediate financial incentives for contributing to a plan.

Employers can use de minimis financial incentives as employee encouragement to contribute to retirement plans pursuant to a salary reduction agreement. To clarify, employers may use gift cards and cash as dangling fiscal carrots to encourage plan participation.

Improving coverage for part-time workers.

There’s an incentive for part-time workers to participate in company retirement accounts as the SECURE Act 2.0 reduces the service requirements for eligibility from three years to the first consecutive 24-month period.

Qualifying longevity annuity contacts. A crucial element of the SECURE Act 2.0 and what investors need to know.

Our RIA financial planners adhere to rules to help clients manage longevity risk. Most of our clients maximize Social Security retirement benefits for guaranteed income. We believe many retirees will require guaranteed income options to complement Social Security and traditional asset portfolios. Finally, the government is warming up to annuity contracts’ benefits (it’s a slow thaw).

Before the SECURE Act, the maximum premium could not exceed 25% of a retirement account balance or $125,000. Beginning in 2023, the percentage limitation is history, and the maximum premium raised to $200,000.

SIMPLE and SEP Roth IRA options.

Another ‘what the heck too so long?’ moment. Beginning in 2023, SIMPLE IRAs and SEP plan Roth options will be available.

Optional treatment of employer matching contributions as Roth contributions.

Above all, this one is big. Before SECURE Act 2.0, employer matching contributions were always pre-tax. With the SECURE Act 2.0, finally, matching contributions may also be Roth. Keep in mind that such contributions are not excludable from gross income.

Other notable provisions:

Emergency savings enhancements are a big change with the SECURE Act 2.0. and what investors need to know.

Plan participants can withdraw $1,000 yearly without early-withdrawal penalties and must repay in full within three years. Employees must wait another three full years to withdraw again unless paid off sooner. These annual withdrawals are subject to federal and state income taxes. In addition, employers may offer a ‘rainy-day’ account whereby employees contribute $2,500 a year and are allowed four penalty-free withdrawals per year.

Excess 529 contributions to Roth transfer.

Excess 529 contributions can roll over to Roth accounts beginning in 2024. However, there are specific rules and limitations to keep in mind.

Transfer restrictions include:

1. A lifetime transfer cap of $35,000.

2. Rollovers are subject to annual Roth IRA contribution limits ($6,500 in 2023).

3. 529 accounts must be open for 15 years.

4. Transfers may only be made to the beneficiary’s Roth IRA (usually a child).

Hardship withdrawal provisions.

Additional hardship withdrawal provisions are created for victims of domestic abuse, military members, and their spouses. For hardcore tax geeks, read the bill here.

There are several drawbacks to the SECURE Act 2.0. I outline a couple of them.

Greater opportunity for retirement plan leakage. A disappointing element of the SECURE Act 2.0. what investors need to know.

For instance, many workers treat retirement accounts like piggy banks because the government allows withdrawals for several reasons, including first-time home purchases. As a result, retirement plan leakage is a serious, ongoing concern.

Financial pundits must stop the zealous promotion of tax-deferred accounts and help the masses PRIORITIZE and PLAN how to save and invest. At RIA, we’ve established a savings hierarchy.

For example, the crucial first financial step is a financial vulnerability cushion (one year of living expenses in reserve, preferably an online, FDIC-insured online bank). For people who don’t have an emergency reserve, we recommend investing in their company retirement plan only up to the employer match.

RIA recommends increasing pre or post-tax retirement account contributions only after an FVC is funded. As a result, many young people we counsel do not need to tap long-term investment vehicles for emergencies or new homes.

A 2021 Joint Committee on Taxation report outlines how retirement accounts have more holes than Swiss cheese. Leakage occurs when an individual, 20 to 50 years old, takes defined contributions or IRA distributions that exceed contributions the individual makes to those accounts in the same year.

Per the report, leakage is estimated at roughly 22%. The SECURE Act may have its heart in the proper place with emergency saving account options. I approve of the withdrawal provisions for terminally ill patients and the expansion of Roth options. But it seems as if with each new Act, the mark is missed when it comes to leakage. At these times, defined benefits accounts or pensions are sorely missed. Zero leakage. Greater retirement success.

This brings me to my next beef.

America Deserves A Defined Benefit Plan Option For The Masses.

Regardless of its intent, the SECURE Act benefits the wealthiest of savers. And that’s ok – but there will still be millions of workers who lack adequate coverage.

What about a government and private sector alliance to create a national pension vehicle for all workers? In a recent Bloomberg Opinion piece, Teresa Ghilarducci, the Schwartz Professor of Economics at the New School for Social Research, outlines how a bipartisan retirement bill for universal coverage is on the table.

Subsequently, the Retirement Savings for Americans Act of 2022 (RSSA) is a true retirement plan concept that will be introduced in the new Congress. Workers without a plan would automatically enroll in a low-cost defined contribution plan at a 3% contribution rate. Covered workers would receive a match from the federal government. No pre-retirement distribution options would be offered, thus eliminating the danger of leakage.

Read Teresa’s latest opinion here.

In conclusion, the SECURE Act 2.0 is one of the most comprehensive retirement bills in recent history. However, there’s still much more to be done for workers not covered by employer plans.

Regardless, retirees, especially those nearing required distribution age, should work closely with their financial and tax partners to incorporate SECURE Act 2.0 changes into their planning.

Naturally, the five Certified Financial Planners at RIA are here to assist with the SECURE Act 2.0 and what investors need to know.