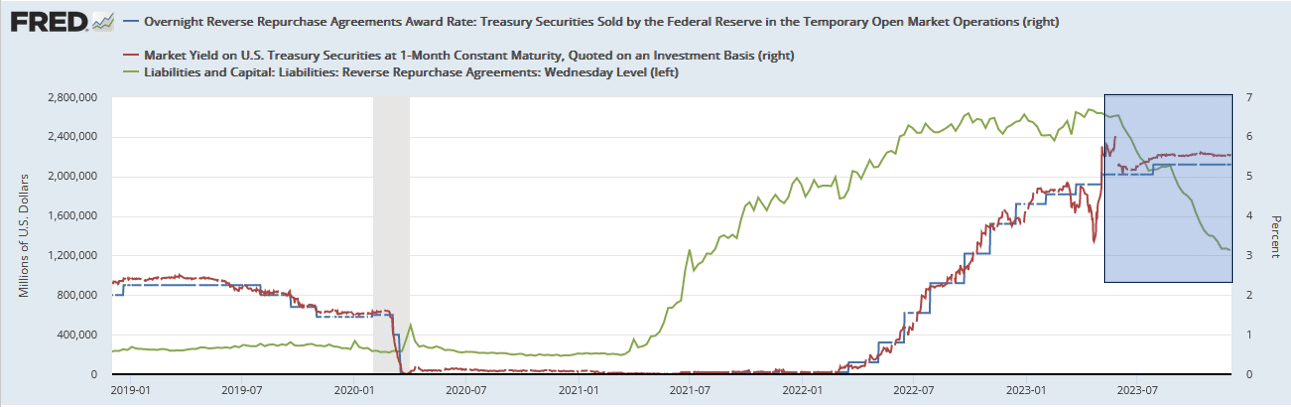

The Fed offers banks and money market funds reverse repurchase agreements (RRP) to drain excess liquidity in the money markets, allowing them to manage the Fed Funds rate. RRP are collateralized overnight loans made by banks and money market funds to the Fed. In March 2021, RRP balances surged due to the excessive liquidity caused by fiscal and monetary stimulus. Had the program not existed, Fed Funds and Treasury Bill demand would have pushed yields well below what the Fed desired. The graph below shows the increase (green) in RRP balances alongside the RRP rate (blue) and one-month Treasury bill yields (red).

The box below highlights that one-month treasury bill yields are now more attractive than RRP. Therefore, RRP balances are declining, signifying that excess liquidity is fading. Money market funds are removing funds from RRP to buy higher-yielding Treasury bills. So far, the decline of RRP is healthy. However, RRP balances may fall to near zero. When that occurs, the Treasury must replace that liquidity from other sources. Coupled with ongoing QT, which also drains liquidity, the removal of excess liquidity from the money markets may increase liquidity stresses for banks and, therefore, the markets.

What To Watch Today

Earnings

Economy

- No notable economic releases

Market Trading Update

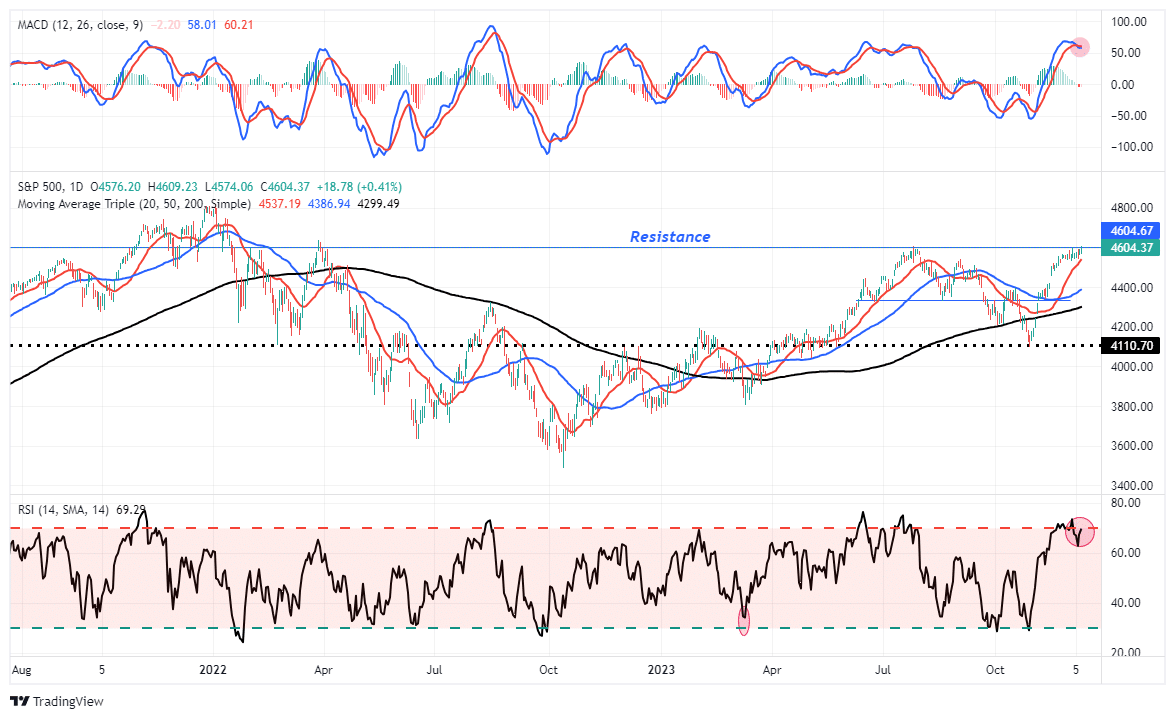

Last week, the market struggled to advance early in the week. On Thursday and Friday, markets climbed to set new closing highs for the year, as shown. However, the combination of overbought conditions and excess bullish sentiment limited gains from weaker-than-expected economic reports that should keep the Federal Reserve at bay next week. It is worth remembering, however, that we are still lower nearly two years later. Most investors have spent the last 15 months making up previous losses, and it is possible that markets may struggle next year as well.

As noted by YahooFinance on Thursday:

“Historically, volatility tends to contract at the end of December, paving the way for predictable year-end gains. But this year, November’s gangbuster returns may have brought forward an early Christmas for investors. Stocks have had three principle catalysts over the last two years — inflation, jobs, and the Federal Reserve — and all three are on the docket over the next week. Whether bullish or bearish, markets could get quite interesting in what is normally a sleepy time of year.”

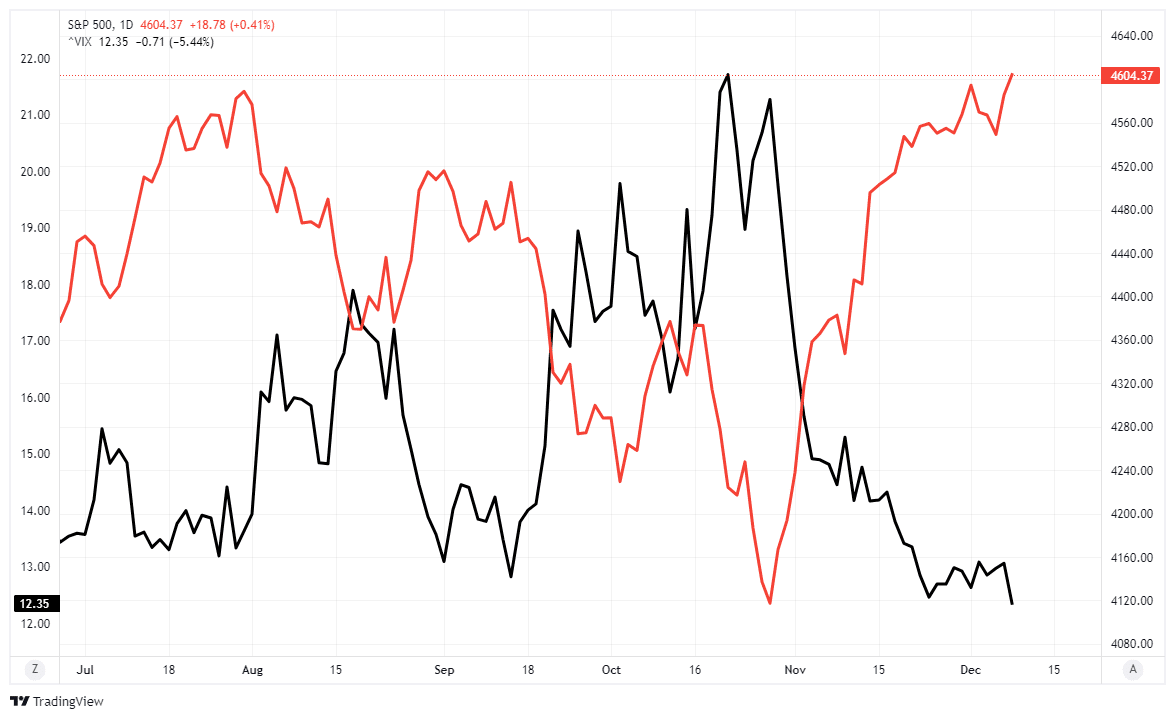

The jobs report yesterday was weak across the board, which will likely keep the Federal Reserve on hold for now, and next week is the inflation report and the last FOMC meeting for the year. With volatility at extremely low levels, as shown, a hot CPI report or a “hawkish message” from the Fed could cause stocks to stumble.

The message remains that risk is prevalent at the moment. However, the question is whether the “Santa Claus” rally was pulled forward.

While bullishness certainly prevails at the moment, along with a strong momentum in the market, this is a great time to set aside the narratives and return our focus to the basic portfolio management rules.

Rules For “Santa Rally”

If you are long equities in the current market, rebalancing risk is easy.

- Tighten up stop-loss levels to current support levels for each position.

- Hedge portfolios against major market declines.

- Take profits in positions that have been big winners

- Sell laggards and losers

- Raise cash and rebalance portfolios to target weightings.

Notice, nothing in there says “sell everything and go to cash.”

Remember, our job as investors is pretty simple – protect our investment capital from short-term destruction so we can play the long-term investment game. Here are our thoughts on this.

- Capital preservation is always the primary objective. If you lose your capital, you are out of the game.

- Seek a rate of return sufficient to keep pace with the inflation rate. Don’t focus on beating the market.

- Keep expectations based on realistic objectives. (The market does not compound at 8%, 6% or 4%)

- Higher rates of return require an exponential increase in the underlying risk profile. This tends to never work out well.

- You can replace lost capital – but you can’t replace lost time. Time is a precious commodity that you cannot afford to waste.

- Portfolios are time-frame specific. If you have a 5-year retirement horizon but build a portfolio with a 20-year time horizon (taking on more risk), the results will likely be disastrous.

As discussed on Tuesday, there is a wide range of potential outcomes, based on valuations, in 2024. No one knows with any certainty what next year will hold. However, by focusing on risk controls and the technical underpinnings, we can safely navigate the waters to safety.

We are certainly anxiously anticipating the arrival of “Santa Claus.” However, we remain keenly aware of the lessons taught to us in 2018 and 2020 that nothing is guaranteed

The Week Ahead

This will be an important week for economic data and the Fed. We suspect the Fed will maintain its hawkish tone in their FOMC minutes and Powell’s press conference on Wednesday. While no one expects the Fed to raise rates, expectations vary as to how the Fed may address the recent easing of financial conditions. If they become more hawkish, stocks and bonds may suffer. That said, recent speeches by Powell and other Fed members lead us to believe they will reiterate what they have said over the last few weeks.

The key data points to follow are CPI on Tuesday, PPI on Wednesday, and Retail Sales on Thursday. CPI is expected to rise 0.1% from 0.0% last month. Core CPI is expected to stay at 4.0% on a year-over-year basis. Retail sales will incorporate some of the post-Thanksgiving holiday sales.

The BLS Employment Report

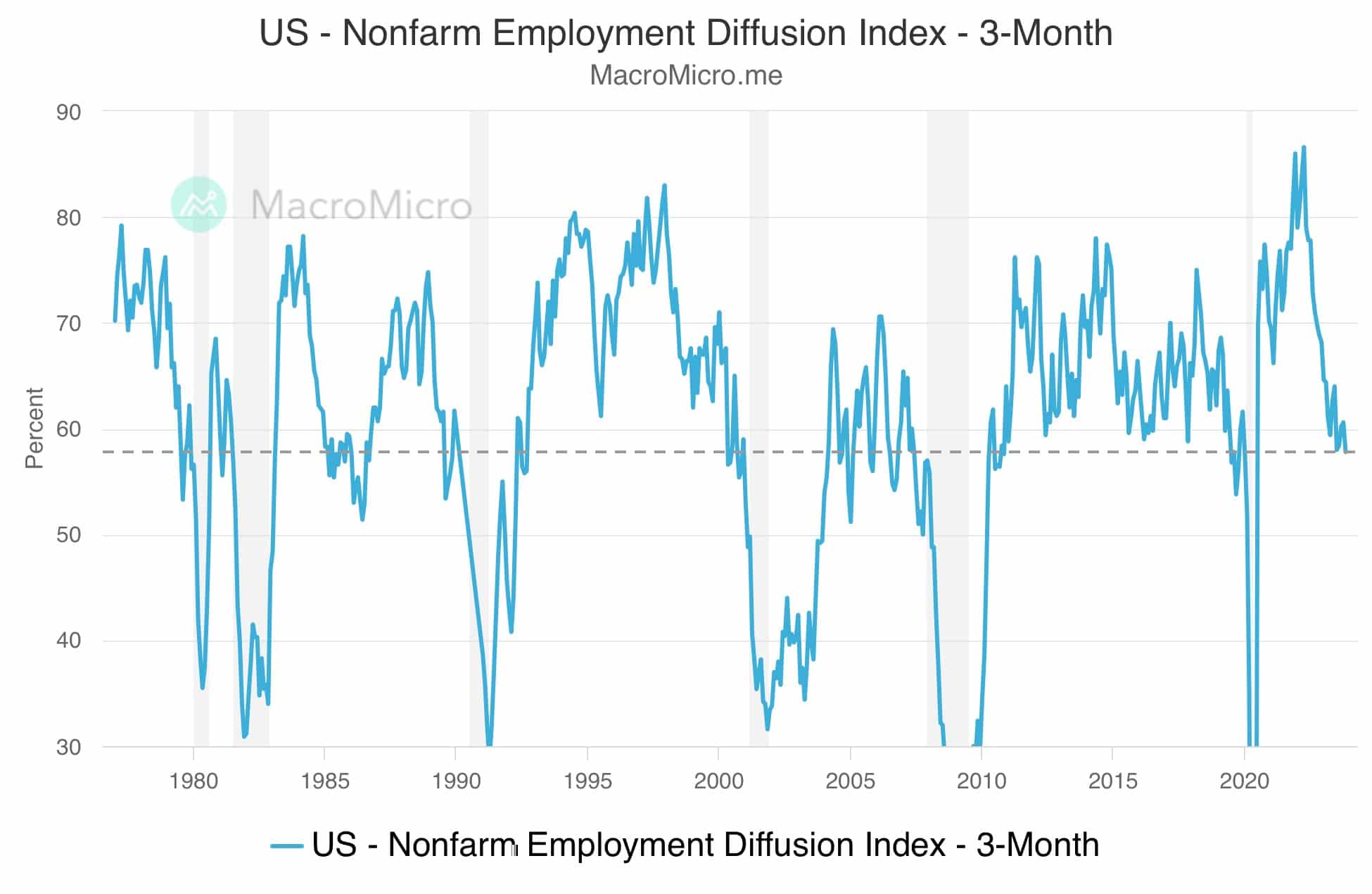

The BLS employment report came in a little better than expected. The economy added 199k jobs in November. Expectations were for a gain of 185k. However, after the ADP and JOLTs reports, many were expecting something worse. The unemployment rate, which had been ticking higher over the previous six months, fell 0.2% to 3.7%. Wages and hours worked also were 0.1% higher than expected. From the Fed’s perspective, this is probably welcome news. It shows the economy remains healthy and may simply be normalizing instead of slipping into a recession. Seasonal adjustments are large in November and December, so we may find out down the road that the report was stronger or weaker than what was reported.

The graph below, courtesy of MacroMicro, shows the employment diffusion index dropped to 57.8% in November. Such is the lowest level in three years. The index measures the percentage of industries reporting job growth. A decline below 50% would raise recession concerns.

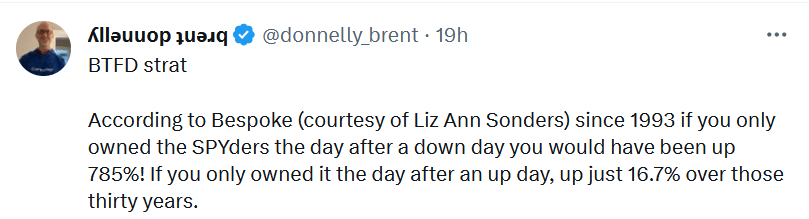

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read