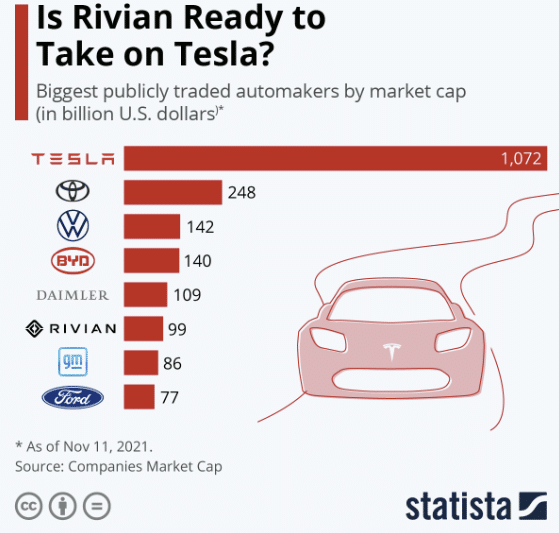

Shares of Rivian (RIVN), the newest entrant into the electric vehicle market, are soaring. Rivian closed Thursday with a market cap of $100 billion. Not bad, considering GM is at $89 billion and Ford is $78 billion. Despite lagging in market cap, Ford benefits as it owns 12% of Rivian. Amazon has a 20% stake in the company and expects to own at least 10,000 Rivian trucks for deliveries next year.

What To Watch Today

Economy

- 10:00 a.m. ET: JOLTS Job Openings, September (10.300 million expected, 10.439 million in August)

- 10:00 a.m. ET: University of Michigan Sentiment, November preliminary (72.5 expected, 71.7 in October)

Earnings

- Before market open: Warby Parker (WRBY) to report adjusted losses of 57 cents on revenue of $537.43 million

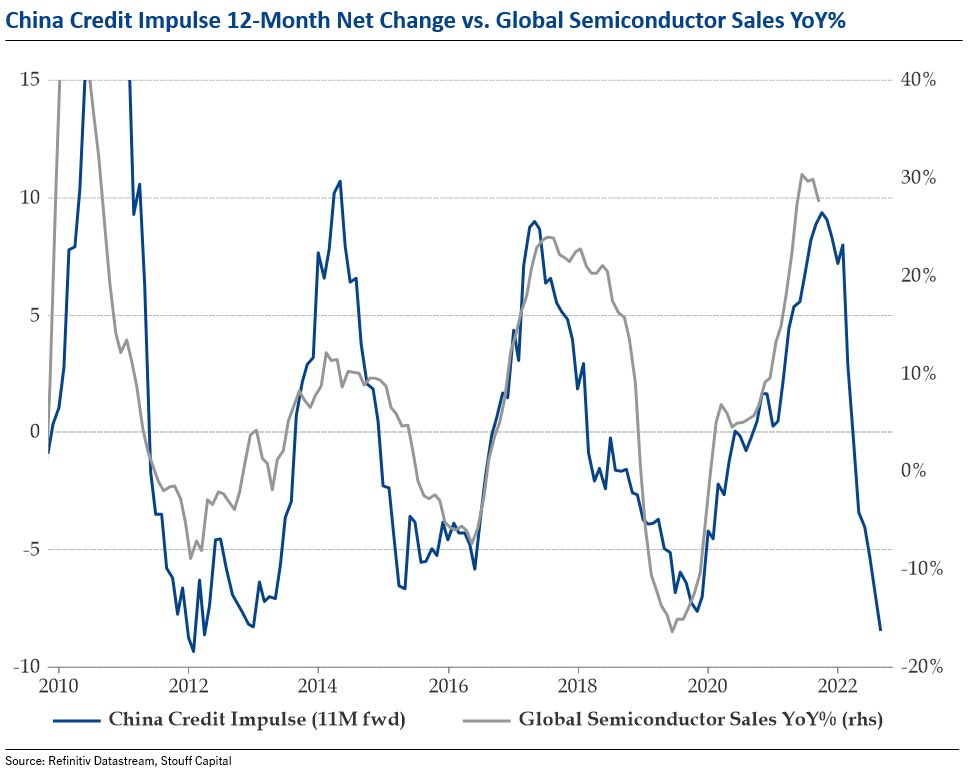

Are Semiconductor Sales Peaking?

Semiconductor stocks have been on a tear lately as chip demand is robust. Further helping the cause, semiconductor manufacturers can’t produce enough chips, which gives them significant pricing power. The graph below warns, investors may be overexuberant. As shown, courtesy of Stouff Capital, semiconductor sales strongly correlate with credit growth in China. Given China produces a large number of goods using chips, the relationship makes sense. Recently, China has clamped down on credit creation resulting in negative credit growth and, not surprisingly, weak economic growth. If the semi-credit relationship holds up, the graph portends semiconductor sales may appreciably underperform sales estimates for 2022. However, the shortage of chips and demand for products using chips, such as cars, provides a decent base of demand for future sales.

Inflation, Inflation, and More Inflation!

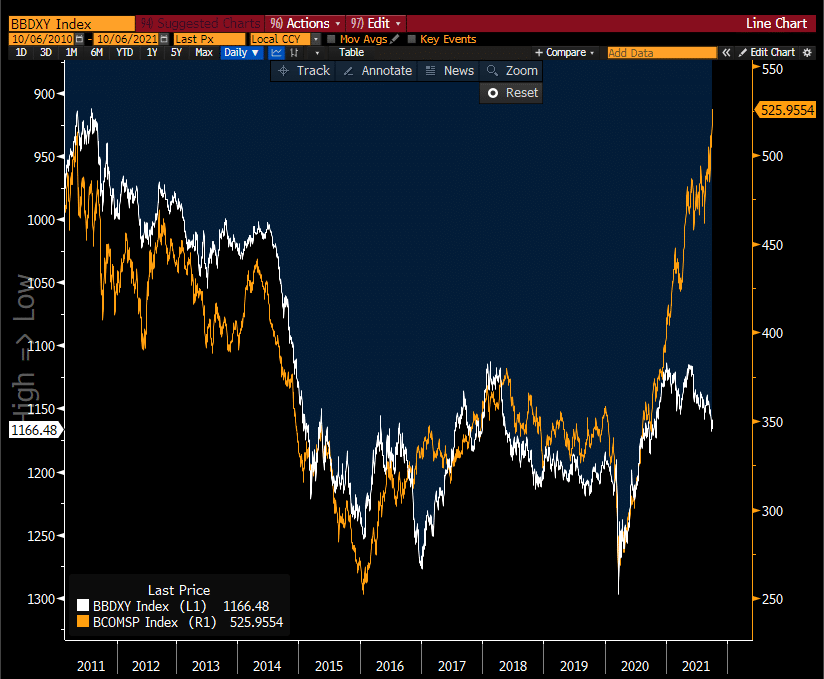

The Dollar and Commodities Are Not Behaving Like Normal

The first graph below charts the dollar in orange and the CRB commodities index in blue. Typically a strong dollar results in weak commodity prices and vice versa. Throughout 2021, commodity prices and the dollar have a positive correlation, as circled. The second graph highlights the abnormal correlation a little better. In the Bloomberg graph, the dollar index (white) is plotted on an inverse scale to the left and Bloomberg’s commodity index to the right. The positive correlation is likely because commodity prices are increasing due to supply line factors and not traditional economic factors.

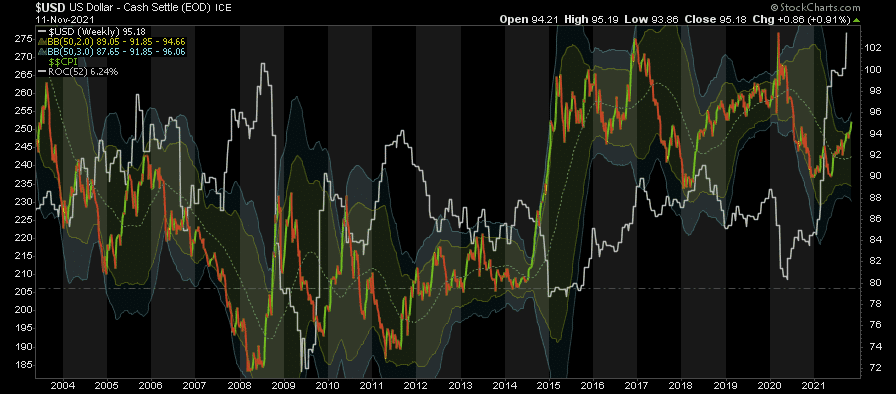

A Stronger Dollar Reflecting Bets The Fed Will Move Faster

“Traders are becoming more certain that inflation, which topped 6% in headline terms last month, will prompt the Fed to accelerate its timetable for liftoff from zero interest rates. Whether the central bank does or doesn’t is an open question, but America’s soaring inflation means the Fed is far more likely to tighten before Japan or the Eurozone.

Marc Chandler at Bannockburn Global Forex, told the Morning Brief in an email that consumer prices above 6% ‘is a shock. I suspect [price inflation] is poised to accelerate in coming months, and the Fed will accelerate tapering to allow it to be prepared for all probabilities, including having to hike rates sooner.’” – Yahoo Finance

Importantly, a stronger dollar will have eventually lead to a “deflationary” impact on the economy as shown. While not always an immediate impact, a stronger dollar leads to lower commodity prices, and other inflationary trends, as foreign demand for U.S. products weaken, and ultimately, the demand for commodities contract (think recession).

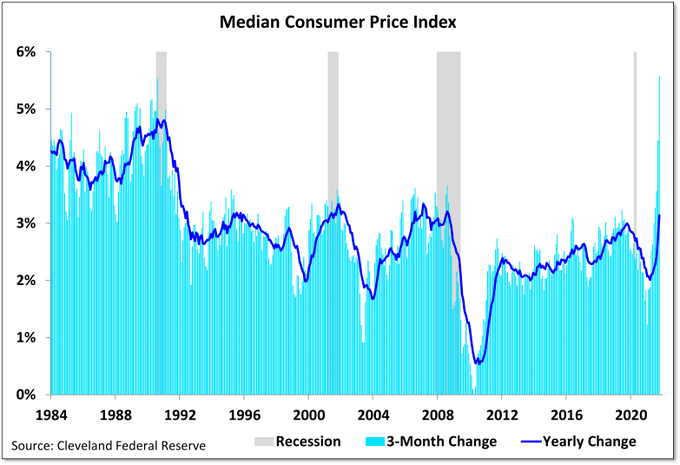

More CPI Worries

The graph below foreshadows that inflation may continue rising. The chart, measuring median CPI, assesses the breadth of inflation. As discussed in recent articles and commentary, the headline CPI figure everyone follows can be swayed by a few items. For instance, “shelter” represents nearly 30% of CPI. The median figure helps assess how the prices of many goods are behaving. As the graph shows, median CPI is now at highs last seen in 2008. More problematic, the 3-month change is running at levels more significant than any seen since at least 1984.

Michael Lebowitz, CFA is an Investment Analyst and Portfolio Manager for RIA Advisors. specializing in macroeconomic research, valuations, asset allocation, and risk management. RIA Contributing Editor and Research Director. CFA is an Investment Analyst and Portfolio Manager; Co-founder of 720 Global Research.

Follow Michael on Twitter or go to 720global.com for more research and analysis.

Customer Relationship Summary (Form CRS)

Also Read