In Part 2, we continue our exploration of retirement income planning truth with Jim Otar. We draw from the later chapters of Jim Otar’s new book about retiree income challenges. (Read Part 1 Here)

Luck Is More Than A Four-Letter Word!

Where one retires in a market cycle is the spin of a roulette wheel.

Many investors are convinced the ‘when’ of retirement is a complex concept.

Once comprehensive planning (preferably years before) lays the groundwork, timeframes crystallize, and end dates become less nebulous. As time closes in on the ‘right’ year, month, day, a stir in the retiree’s gut, perhaps considered nature’s timing, motivates action.

Unfortunately, markets don’t always cooperate with holistic financial planning because where one retires in a stock trend, either a tailwind or headwind, is, unfortunately out of our control.

What are the warning signs of imminent diminishing luck? Jim explains:

Retirees Shouldn’t Ignore The Red Flags Of Retirement Income Planning.

After a portfolio withdrawal rate, luck is the second-largest determinant to portfolio longevity.

Jim identifies several warning signals. One is based on technical analysis, which employs moving-average crossovers. RIA’s investment team incorporates technical analysis. Also, to determine if a poor sequence of returns was experienced at the beginning of retirement, Jim recommends a fourth-year portfolio withdrawal review.

Readers may recall from Part 1 that a poor series of returns early into retirement results in rapid depreciation of capital and subsequently tough to overcome. Our team prefers a three-year analysis of portfolio distributions, which is a year sooner than Jim’s rule; however, the sentiment and concern are the same.

Valuations Ultimately Matter.

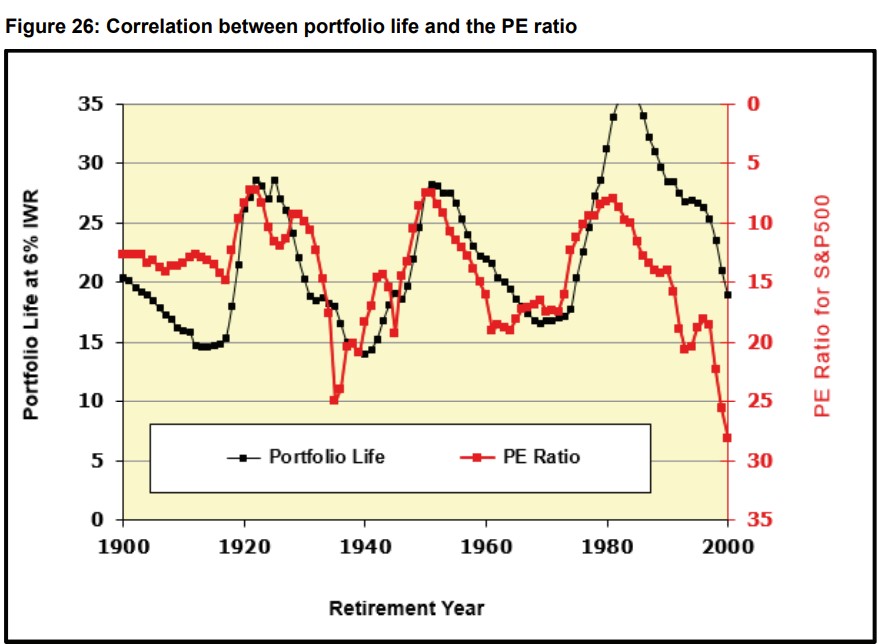

Jim’s number one warning sign is the S&P 500’s price-to-earnings ratio because a strong correlation exists between portfolio life and average market PEs.

In his illustration below, an unsustainable portfolio withdrawal rate (for a 60/40 allocation), such as 6% and lofty PEs do not mix. Generally, the higher the PE, the greater the risk of a shorter portfolio life. In the graph below, Jim uses a 6% portfolio distribution, which may be feasible when PEs are roughly 10X.

However, a 6% withdrawal rate for an extended period is dangerous to portfolio longevity when PEs exceed 10X. Keep in mind, the Shiller PE at the time of this writing is 31X.

So, what should a retiree do in the face of current conditions? Reassess his or her portfolio withdrawal rate as soon as possible!

Jim’s Retirement Guidelines Are as Follows:

- If the IWR (Initial Withdrawal Rate) is larger than 6%, portfolio life will be short;

- However, if the IWR is near sustainable (between 3.5% and 4%), the data is too scattered for a reliable formula to estimate the portfolio life; and

- Assuming the IWR is below sustainable, i.e., under 3.5%, then you have –in effect- an

accumulation portfolio, and it should provide lifelong income.

Again, to stay on track, and remain confident in your distribution strategy, complete a portfolio withdrawal rate checkup every three years.

Sum your cumulative net portfolio gains minus withdrawals, including advisor fees, if applicable. If a surplus exists, which means you’ve experienced more gains than withdrawals, consider an annual pay raise! Work closely with a financial planner to determine specifics and create ‘what-if’ scenarios to test withdrawal-rate parameters.

The Initial Four-Year Checkup.

According to Jim, retirees should review portfolio withdrawals after the initial four-year distribution period to identify a poor early start. He uses four years to match cyclical or shorter-term trends in markets.

To ensure clients remain on track in the face of the ongoing pandemic, we initiate portfolio withdrawal reviews every three years.

Monitor Your PERSONAL Sustainable Withdrawal Rate.

The SWR is the maximum amount of money a retiree may withdraw from a variable asset portfolio for a lifetime with an acceptable risk of depletion. A popular financial ‘rule of thumb’ is the 4% portfolio withdrawal rule.

Recently, some of the most influential academics shed new light on the 4% rule and determined it closer to a 2.4% rule. This development will be an unwelcome surprise to many older Americans who primarily generate retirement paychecks from investment portfolios.

Realistically, this whole SWR thing is an educated guess at best, which is why monitoring is mandatory. Jim suggests every five years or soon after a life-altering event or imminent large expenditure, such as long-term care. At RIA, we stick with the three-year checkup overall. Either way, retirees need to examine their SWRs on a scheduled basis.

Every Client Is Unique

Furthermore, every client is unique. Every retiree household maintains its own SWR. Financial publications depending on their input variables, outline acceptable withdrawal rates from 2-6%. Financial planning Monte Carlo simulations that incorporate historical asset class and market data will most likely allow for overly-optimistic withdrawal rates and ostensibly, nasty surprises later.

It’s a financial professional’s responsibility to study trends, valuations and adjust financial planning software inputs for forward-looking returns so a retiree may deal realistically with the likelihood of lower future SWRs.

Our group examines and uses valuation metrics to adjust asset class returns as warranted. For example, in early 2018, we adjusted downward portfolio returns—a timely decision in hindsight. Today, RIA clients with financial plans are prepared to retire with little inconvenience because we set their spending and lifestyle expectations in the face of future lower portfolio returns.

Also, per Jim, the SWR is based on a specific degree of ‘acceptable’ risk within a given time horizon, but the definition of acceptable varies widely. For example, one academic study allows a 25% failure in their SWR tables. However, that is not an acceptable metric for real life. To deal with the conundrum of ‘acceptable’ risk, Jim examines what goals the money needs to achieve.

Needs, Wants, and Wishes.

Essential expenses are those necessary for survival. They are the needs. The probability of portfolio depletion must be zero for these expenses. Think housing, insurance, taxes, and most of the expenses that keep you and yours alive! What do you think the ‘acceptable’ risk is here? You are correct: Zero.

For basic or lifestyle expenses (wants) such as vacations and additional non-essential spending, Jim’s tenet is the probability of portfolio depletion should not exceed 10%. Discretionary aspirations (wishes) such as donations, multiple vacations, financial assistance to relatives can be considered just as long as needs are 100% assured, and portfolio depletion for ‘wants’ doesn’t exceed 10%.

Jim Suggests Annuities As Lifelines.

When it comes to risk management, annuities hold advantages over variable asset portfolios. Annuities can establish a ‘personalized pension,’ a bolster to Social Security, and a guaranteed income for single and joint lives. Market risk, longevity risk is mitigated, and the peace of mind from never running out of money or turbulence of markets increases.

No need to run stress tests, Monte Carlo simulations for adverse market conditions because lifelong payments are guaranteed regardless of market cycles and portfolio performance.

At RIA, we believe all annuities should be planned, not sold. Comprehensive financial planning must be undertaken first to determine whether a guaranteed income stream is required to complement Social Security.

Specifically, income annuities are solely designed to provide a stream of income now or later that recipients cannot outlive. These annuities are simple to understand and generally lower cost compared to their variable and indexed brethren.

Deferred income products where owners and/or annuitants can wait at least 5 years before withdrawals, may participate in market index gains (subject to caps) and have an opportunity to receive higher non-guaranteed annual income withdrawals depending on market performance.

Withdrawals can never be less than the guaranteed withdrawal benefit established by the insurance company but may be higher depending on annual market returns. As with all annuities, there is never stock market risk. The purest form of annuity is the SPIA. It’s the “Ivory Soap” of insurance products.

Single-Premium Immediate Annuities – “The Pension Replacement.”

SPIAs are splendidly simple – Provide a life insurance company a lump sum, and they pay you or you and a spouse for life. That’s it. I consider SPIAs the best replacement for the pension your company no longer provides. You, as an employee, must create a pension on your own.

The Rationale for Income Annuities In Retirement

There are several valid reasons to allocate a portion of an investment portfolio to an income annuity. I’ll list them in the order of importance:

- Above-average life expectancies. On average, American males live to 76.1 years; females add 5 years to 81.1. If you or you and a spouse have a family history of longevity and enjoy excellent health along with life-prolonging habits like exercise and a healthy diet, a SPIA may be a viable addition to a traditional stock and bond portfolio.

- Retirement plan survival deficiency. Life has a way of altering good financial intentions. If lucky, you have a solid 20 years to save uninterrupted. Along that path may come unexpected life changes like divorce, a major illness, job loss, and let’s not forget the portfolio-busting bear markets or worse. If working longer, saving more, part-time employment in retirement, and smart Social Security decisions don’t dramatically improve the probability of financial plan success, then a SPIA can be purchased to ensure, along with Social Security, your household never runs out of money.

- A legacy intent. Studies indicate that purchasing an inflation-indexed SPIA at retirement reduces portfolio depletion and allows for a larger inheritance for those who believe leaving a legacy to children and grandchildren is an important goal.

Although SPIAs are simple in theory, consumers have difficulty grasping how they provide return or yield. Prospective SPIA owners should swap the word “return” for the concept of payout.

A Simple Illustration.

An investor purchases a high-quality $100,000 bond for five years that pays 2.25% annually. Easy, right? The bond purchaser earns $2,250 every year for five years, then at the end of the period or upon maturity, $100,000 is returned. Obviously, the return is the interest earned.

Consider now $100,000 in a SPIA. Not so easy. A couple provides $100,000 to an insurance company and expects payments to begin the following month. Here, there’s no return per se; there’s a payout rate that distributes principal and interest. From there, the internal rate of return can be calculated. Not to be morbid; however, the insurance company’s best thing is income recipients pass early or within age ranges the life insurance actuaries expect.

The worst that can occur for the organization is that income recipients live long lives. Way beyond the years the mathematics dictate. SPIAs are primarily designed to manage or hedge longevity risk.

Back To My Example

A 65-year-old male and his 62-year-old spouse invest $100,000 in a non-qualified (after-tax) SPIA with an increasing payout option (indexed for inflation at 3% per annum) and will receive every month beginning next month, $291.01. The taxable portion of each payment (interest) will be $80.61, the remainder – a return of principal. Thus, the tax exclusion ratio is 72.3%.

The 12-month income figure is $3,492.12, which makes the annuity payout rate of 3.49%. The internal rate of return or IRR after 21 years is .012%, after 25 years – 1.722%, 30 years – 3.101%. You get the picture. The longer you live, the greater the “return” on an SPIA. The IRR here is negative for 20 years and shorter timeframes.

The SPIA, along with Social Security, generates a combined lifetime income stream, which should permit a lower withdrawal rate from a stock and bond portfolio, especially through sequences of low or poor market returns, thus reducing the risk of portfolio depletion.

The use of a SPIA allows retirees to increase stock allocations, especially if capital isn’t required to be distributed during corrections and bear markets due to the guaranteed income the SPIA provides.

Gary Mettler, the author of the book “Always Keep Your Hands Up!” exclusively about SPIAs, shared his 35-years “in the SPIA business” perspective:

“SPIAs exist to keep you from going broke. While going broke may happen towards the end of life at age 85+, it can happen very early on too. Adverse changes in mental health, business collapse, marriage failure, unreimbursed casualty losses, medical/care costs, litigation expense, etc. you want to make sure you continue to receive an uninterrupted flow of retirement income. After all, at age 60+, you no longer have time to make up for portfolio losses.”

RIA’s Rules or Financial Guardrails for the Purchase of SPIAs:

- Nothing happens without comprehensive planning. A financial plan will expose portfolio longevity concerns that may require the use of income annuities. Working longer, part-time employment, downsizing, boosting savings, and maximizing Social Security may be sufficient to improve portfolio survivability. If not, annuitizing a portion of a portfolio will ensure lifetime income. If there’s a 30% or greater probability of outliving retirement assets, purchasing a SPIA makes sense.

- Think of SPIAs primarily as “longevity insurance.” It can take many years, possibly decades, to exceed your original investment in a SPIA. Living a very long life, 35 years or longer through retirement, makes SPIAs a smart choice. Put your life expectancy to the test at livingto100.com.

- Inflation-adjusted SPIAs vs. fixed SPIAs – When to choose. Fixed SPIAs are not adjusted for inflation. Income remains the same throughout the payout period. So, why would I choose a fixed SPIA over one that accounts for inflation? At a 3% inflation rate, the fixed SPIA provides a 45% larger initial retirement date payout than the inflation-adjusted selection for my retiring couple. In other words, with the fixed SPIA, there’s a greater chance of recovering and exceeding their $100,000 investment in a shorter timeframe when compared to the 21 years required for the inflation-adjusted alternative. Your choice would depend on your: 1). Personal expectations of inflation throughout retirement, 2). Life expectancy assessment. The longer your life expectancy, the greater the benefits of an inflation-adjusted option. Professor Wade Pfau provides back-up to this analysis in his blog post “Efficient Frontiers: Inflation Assumptions, Fixed SPIAs, & Inflation-Adjusted SPIAs.”

Are SPIAs Right For You?

The guidelines provided are designed to illustrate how single-premium immediate annuities can be incorporated into a holistic retirement income strategy.

I hope you gain from the wisdom of Jim Otar because he helped me gain a fresh perspective on retirement income planning.

Richard Rosso, MS, CFP, CIMA is the Head of Financial Planning for RIA Advisors. He is also a contributing editor to the “Real Investment Advice” website and published author of “Random Thoughts Of A Money Muse.” Follow Richard on Twitter

Customer Relationship Summary (Form CRS)

Also Read