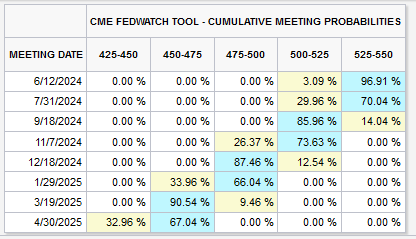

Wednesday’s retail sales and CPI data were weak enough to get investors back on the rate-cut bandwagon. As shown in the CME table below, the market now ascribes an 85% chance the Fed will cut rates in September and reduce them a second time before year-end.

Retail Sales for April were flat (0.00%) below the +0.40% expected and the downwardly revised +0.60% for March. Excluding the volatile autos and gas sales, retail sales were -0.10%, the lowest since January’s -0.80%. The control number, which feeds both GDP and PCE, was -0.30%. We suspect the Atlanta Fed’s GDP Now forecast will be revised sharply lower due to the importance of personal consumption and the fact that there is little data thus far for the quarter.

CPI for the month was +0.30%, the same as the previous month, and .10% bps lower than expected. Core CPI was also +0.30% and .10% lower than March, but in line with expectations. Shelter prices (40% of CPI) and gasoline accounted for almost three-quarters of the monthly CPI number. We know gasoline prices have fallen by nearly 10% in May, and shelter should continue to weaken. This bodes well for the coming CPI report, which helps explain the market reaction to the data.

What To Watch Today

Earnings

Economy

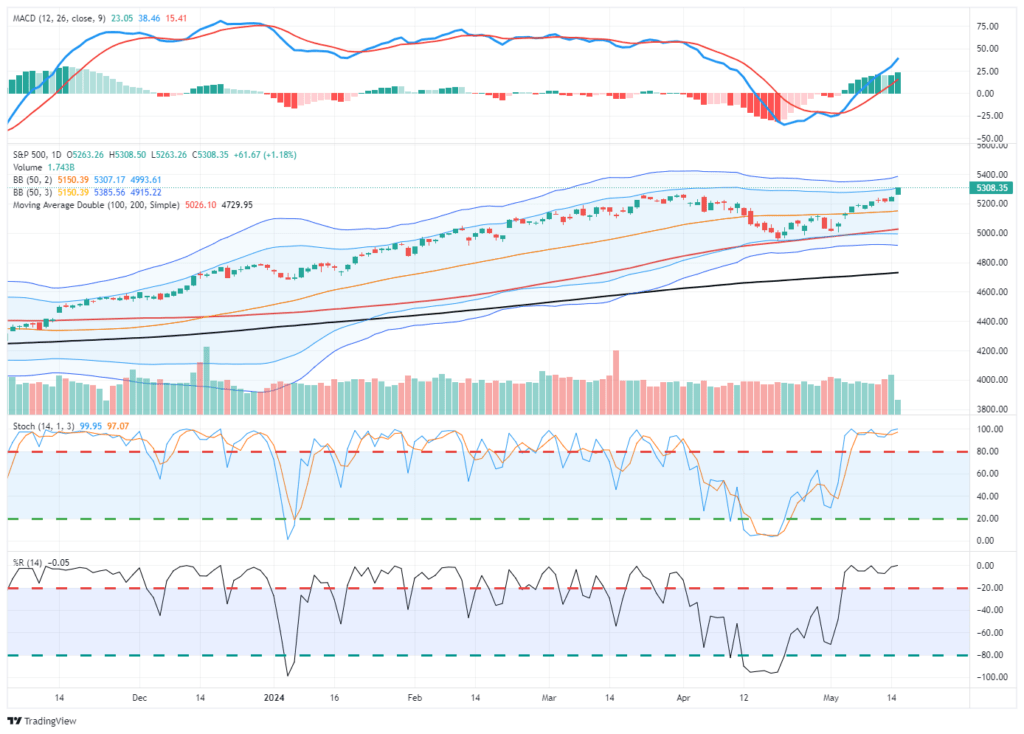

Market Trading Update

Yesterday, we noted that:

“In the short term, the market is decently overbought, which will limit the upside currently. The exception to that statement is this morning’s CPI report, which could lead to a push to new market highs if it is weaker than expected. Given the substantial negative revisions to yesterday’s previous PPI report, today’s CPI report could show some cooling.”

That is what happened, as CPI missed estimates. This, combined with Powell’s recent dovish tones, sent markets into a steady buying binge all day, closing at all-time highs. The deviation above the 50-DMA, combined with overbought conditions, is getting slightly more extreme. While there is no reason to be bearish, continue rebalancing as needed to maintain risk profile tolerances in your portfolio. A pullback to retest the 50-DMA is likely within the next few days to weeks, providing a better opportunity to increase exposures as needed heading into the summer months.

Finding The Next GME and AMC Short Squeeze

Yesterday’s Commentary discussed the recent surge of Game Stop (GME) and AMC Entertainment (AMC). Essentially, coordinated buying is forcing a significant number of short investors to buy and cover their shorts.

A couple of readers asked how they might find the next short squeeze. As we shared yesterday, SimpleVisor provides the short interest ratio for most stocks; however, for the time being, it cannot scan for stocks with high ratios. In the meantime, we ran a scan on FinViz, looking for stocks with a market cap greater than $2 billion and with more than 25% of its shares available to the market (float) being shorted. This ratio is different than the short-interest ratio we presented in the Commentary. It uses the number of shares short versus the average daily trading volume. The table below shares our results and shows both the short interest ratio and the percentage of shares of short sales versus the float of the stock.

There are almost two shares short of DJT for every share available. However, its short-interest ratio is low as the average volume traded is 3x of the available shares. Considering both short measurements, ABR appears to be most susceptible to a short squeeze based solely on this data.

Greg Valliere – Inside Washington

Greg Valliere is a Washington insider with over 40 years of experience analyzing and assessing the political landscape. Given that the coming election will likely have a big impact on markets, we have decided to occasionally share snippets from his daily “Morning Bullets” throughout the remainder of the election season. We aim to keep you abreast of the latest thinking in Washington’s inner circles.

OF ALL THE REASONS WHY BIDEN IS SLIPPING, the most obvious is a renewed public anxiety over inflation. Voters see prices surging for virtually everything, and the White House now is resigned to a summer without rate cuts from the Federal Reserve — and more trade friction with China.

THIS ELECTION OUTLOOK COULD BE REVERSED IN AN INSTANT if there’s a fresh scandal, some new gaffe, a health crisis, or a sudden geopolitical eruption. Accordingly, we haven’t made a final call. But for now, Wall Street and Washington are planning for a Trump presidency, which seems like an increasingly safe bet. Joe Biden is the clear underdog,

THERE’S SOME RELIEF at the White House to see Israeli troops prevailing against Hamas, but the likelihood of a simmering guerrilla war in the region has only increased the bitterness between Biden and Benjamin Netanyahu, which may never dissipate, complicating the a deep division among Democrats over the war.

Tweet of the Day

For more information on this Tweet, please read yesterday’s Commentary.

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read