At RIA Advisors, we work with a wide range of individuals, families and business clients, providing money management and financial planning services tailored to each client’s needs. Simply put, we’re in the business of helping our clients reach their unique financial objectives. We accomplish this task by taking the time to understand the client’s financial situation, goals and risk tolerance. Based upon this in-depth analysis, we then recommend, develop, implement and monitor their investment portfolio performance.

Yesterday we learned that Exxon (XOM) is in talks with Tesla, Ford, and Volkswagen about supplying lithium. If that headline caught you off guard, here is the back story. Earlier this year, XOM bought the drilling rights for 120k acres of land in the Smackover formation, as shown below. The purpose is not shale oil, as many may suspect, but to produce lithium to feed the rapidly growing demand from EV manufacturers. XOM plans on constructing a lithium processing plant in Arkansas capable of producing 75k-100k metric tonnes annually. For context, the world’s largest producer Albermarle generates 225k metric tonnes annually. Global lithium production is expected to be near 1 million tonnes this year. XOM will be a significant lithium producer if its plans come to fruition.

Making the story more interesting, XOM bought pipeline operator Denbury Inc on July 13. Denbury pipelines will allow Exxon to transport and store carbon emitted from their lithium plant. XOM also has contracts to help CF Industries, Linde, and Nucor capture, move, and store the carbon emitted from their facilities. XOM is becoming much more than a traditional oil and gas company. They are smartly diversifying across many energy sectors to ensure they stay relevant as the world’s choice of energy changes. Per its Chairman and CEO Darren Woods: “ExxonMobil is committed to playing a leading role in the energy transition, and Advancing Climate Solutions articulates our deliberate approach to helping society reach a lower-emissions future.”

What To Watch Today

Earnings

Economy

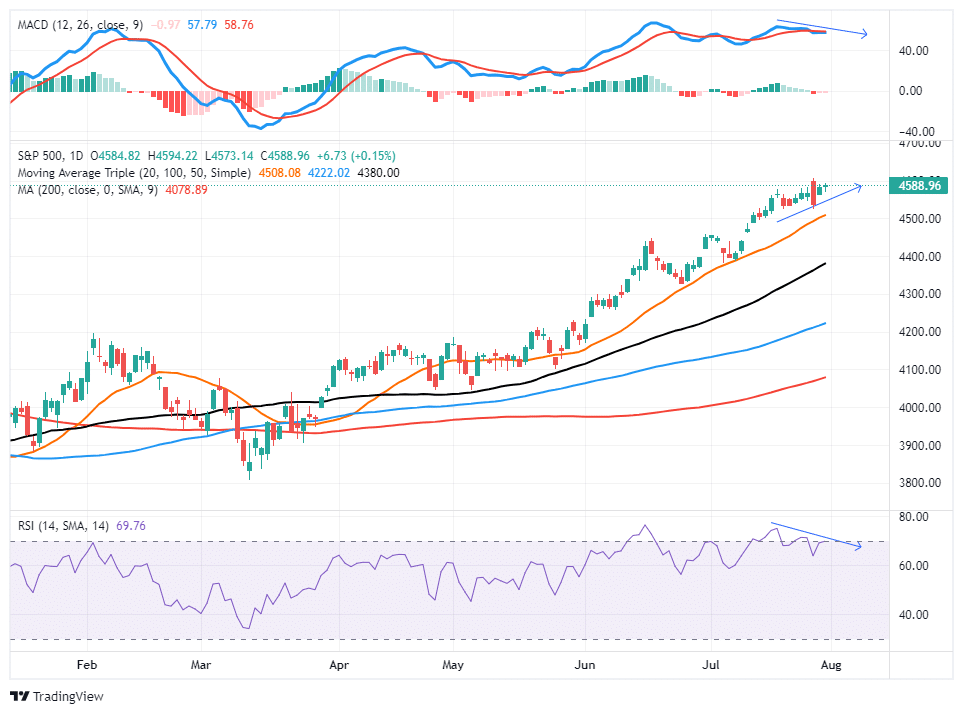

Market Trading Update

As we kick off August, bullish sentiment is so bullish that even Scott Rubner recently made a note:

“I am so bullish, that I am actually bearish now for August. I am looking for a small-ish equity market correction in August. My core behavioral view is that I no longer speak to any “macro” bears. Positioning and sentiment areno longer Pessimistic, and it is Euphoric.”

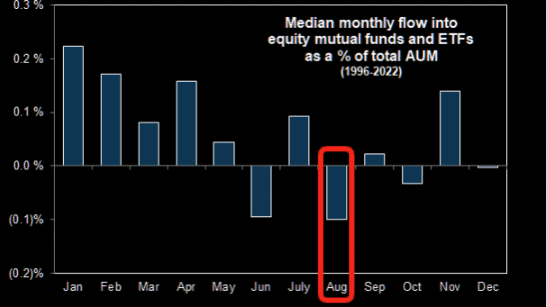

Importantly, that commentary included two charts. The first was the monthly returns of the market, showing that August tends to be one of the weaker months of the year.

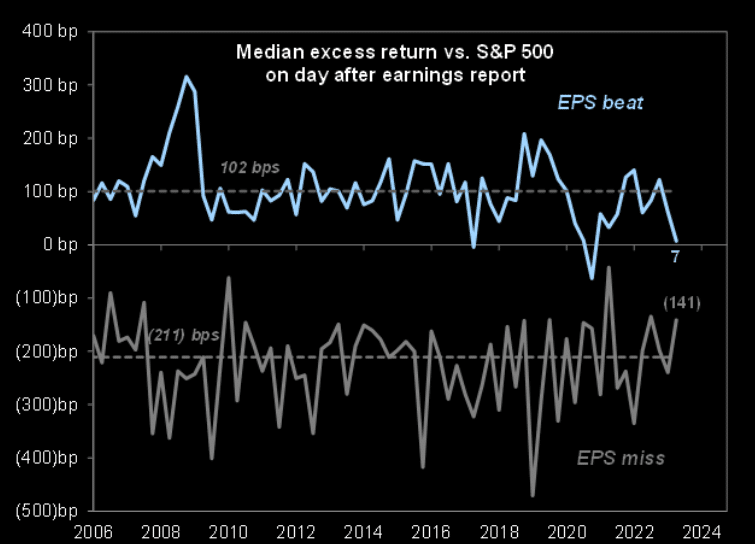

The second, more important, was the median returns of stocks following earnings reports. Notably, while companies have been beating estimates, they aren’t being rewarded as they have been historically due to the preceding price runup. In other words, stocks have already been priced into their earnings reports.

As we move into August, the bulk of earnings are behind us, and the markets will return their focus to the Fed and the economy. Such potentially sets the market up for a short-term correction as recent exuberance cools off.

Another thing we are watching closely is the negative divergence between the market and the Relative Strength Index, which also suggests a near-term correction.

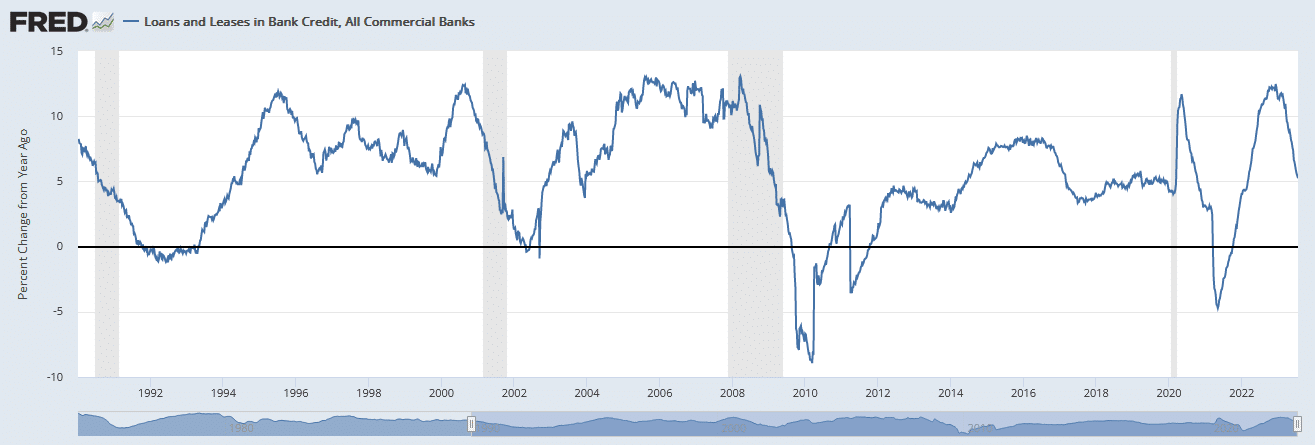

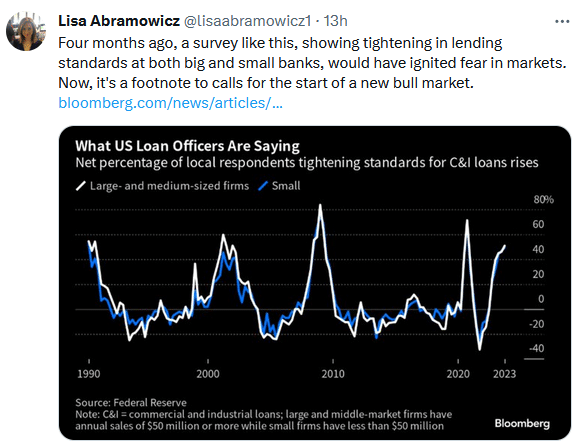

SLOOS Lending Survey

Monday’s Fed SLOOS survey (Senior Loan Officer Opinion Survey) showed that demand for credit continues to weaken. And at the same time, banks are tightening their lending standards. Per the survey:

For loans to households, banks reported that lending standards tightened across all categories of residential real estate (RRE) loans, especially for RRE loans other than government-sponsored enterprise (GSE)-eligible and government loans. Meanwhile, demand weakened for all RRE loan categories. In addition, banks reported tighter standards and weaker demand for home equity lines of credit (HELOCs). Furthermore, standards tightened for all consumer loan categories; demand weakened for auto and other consumer loans, while it remained basically unchanged for credit card loans.

The graph below shows the strong correlation between lending standards and bank lending. Assuming the relatinionship holds, which seems likely, credit is likely to contract in the coming quarter or two. As the second graph shows, negative credit growth has been a hallmark of the last four recessions. This point is not lost on Bloomberg’s Chief Economist as we share below the graphs.

Anna Wang, Chief Economist for Bloomberg Economics sums up the report as follows:

The latest SLOOS explains why Fed Chair Jerome Powell sounded marginally dovish after the July 25-26 FOMC meeting – credit is tight and getting tighter. The transmission of tighter monetary policy to credit conditions has taken longer than in the past, even as the lags have been shorter for industrial production, housing, and risk assets. Nonetheless, the impact is coming – and we expect it to push the economy into a recession toward the end of the year.

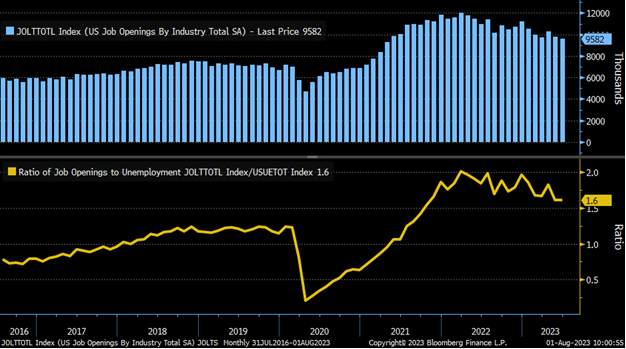

JOLTS And ISM Show The Labor Market Is Loosening

Tuesday’s JOLTS reported that the number of job openings is 9.582 million. While still historically very high, it is well off its 12 million peak and at its lowest since March 2021. The labor market is still tight, albeit finally showing signs of loosening, which will help alleviate wage growth and, ultimately, inflationary pressures. The bar graph below shows there are still more than 1.5 million job openings than existed prior to the pandemic. Similarly, there are more job openings than there are unemployed people.

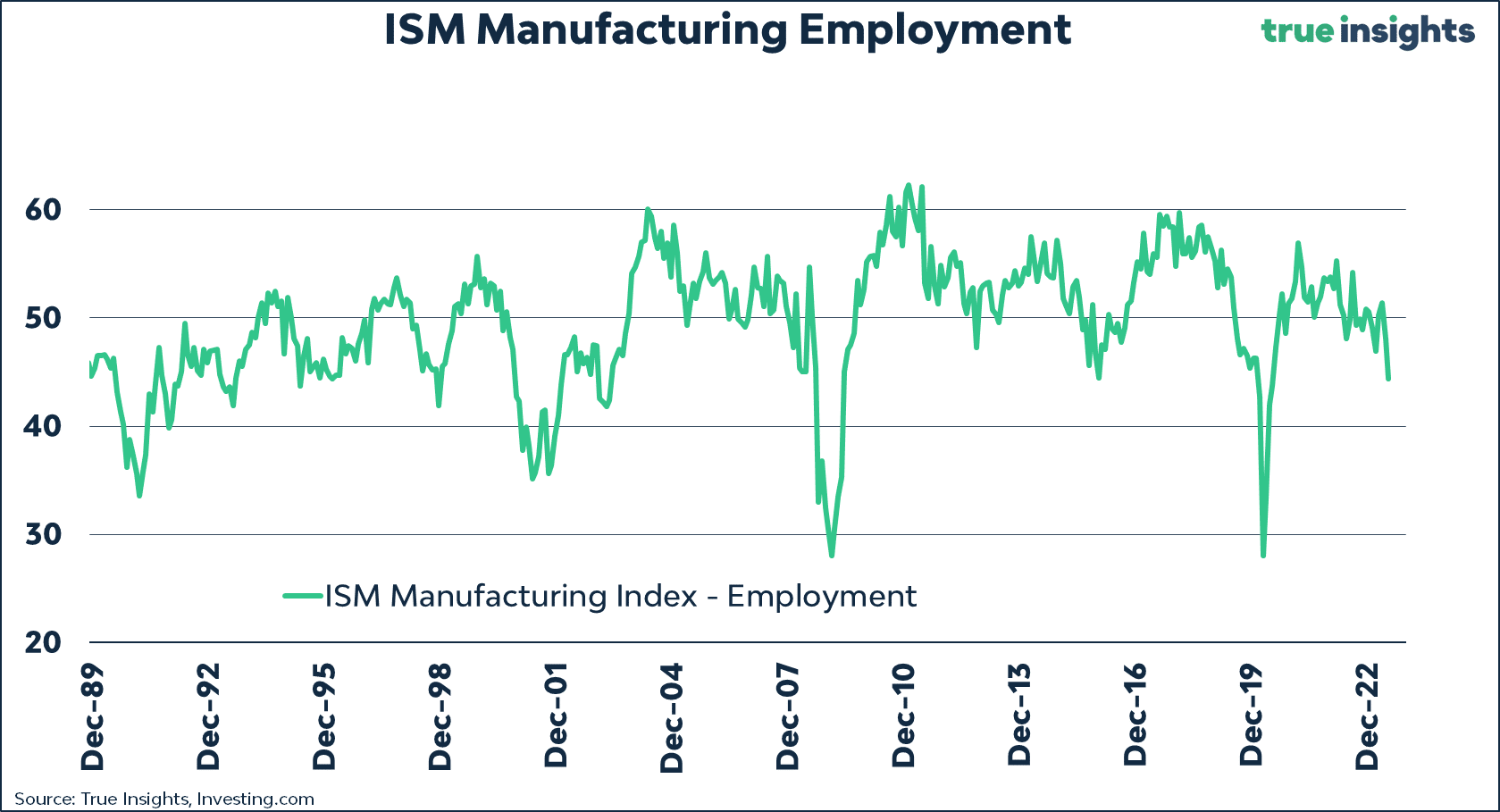

The ISM manufacturing index remains sluggish and at levels that have been commensurate with prior recessions. The broad index rose slightly from last month to 46.4 but was 0.5 below expectations. Most telling in the report is the employment gauge fell to 44.4, pointing to a contraction of the manufacturing workforce. It is the lowest reading since July 2020 and the 2008 recession before that. Also of note, prices paid continue to contract. They now stand at 42.6, up slightly from last month but well below estimates of 44.2. As we have noted, the manufacturing sector remains weak, and the service sectors have thus far buffeted the economy from said weakness. Tomorrow’s ISM service sector survey will provide more data on the state of the service sector.