On July 24th, the Nasdaq 100 will reduce the weightings of its top seven holdings to try to better balance the top-heavy market cap-weighted index. At the same time, the rebalance will increase the weighting of many other smaller Nasdaq 100 stocks. We suspect that the large index funds will adjust their holdings appropriately in the pre-market session or during the daily session on the 24th. One would presume the rebalance would negatively affect the performance of the top Nasdaq 100 stocks, but thus far, based on trading after the new weights were announced on Monday, the reweighting of the index may prove to be a nothing burger. Microsoft and NVIDIA, the stocks that face the largest decline in their respective weightings, have outperformed the market since the details were announced.

The table, courtesy of Goldman Sachs, shows the top 25 Nasdaq 100 companies by market cap. Highlighted in red is the weight of each stock today versus the new pro forma weight. The table also provides context for how much the change might affect the stocks. In the far right column, it presents the estimated dollar impact as a percentage of the average daily trading volume for the last three months. Microsoft and NVIDIA shares will have the largest declines in their weightings. Broadcom, Pepsi, Costco, and Adobe are the top four beneficiaries. In the aggregate, the top seven Nasdaq 100 stocks will lose 11.8% of their weighting due to the rebalance but will still account for a hefty 43.7% of the Nasdaq 100 index.

What To Watch Today

Earnings

Economy

Market Trading Update

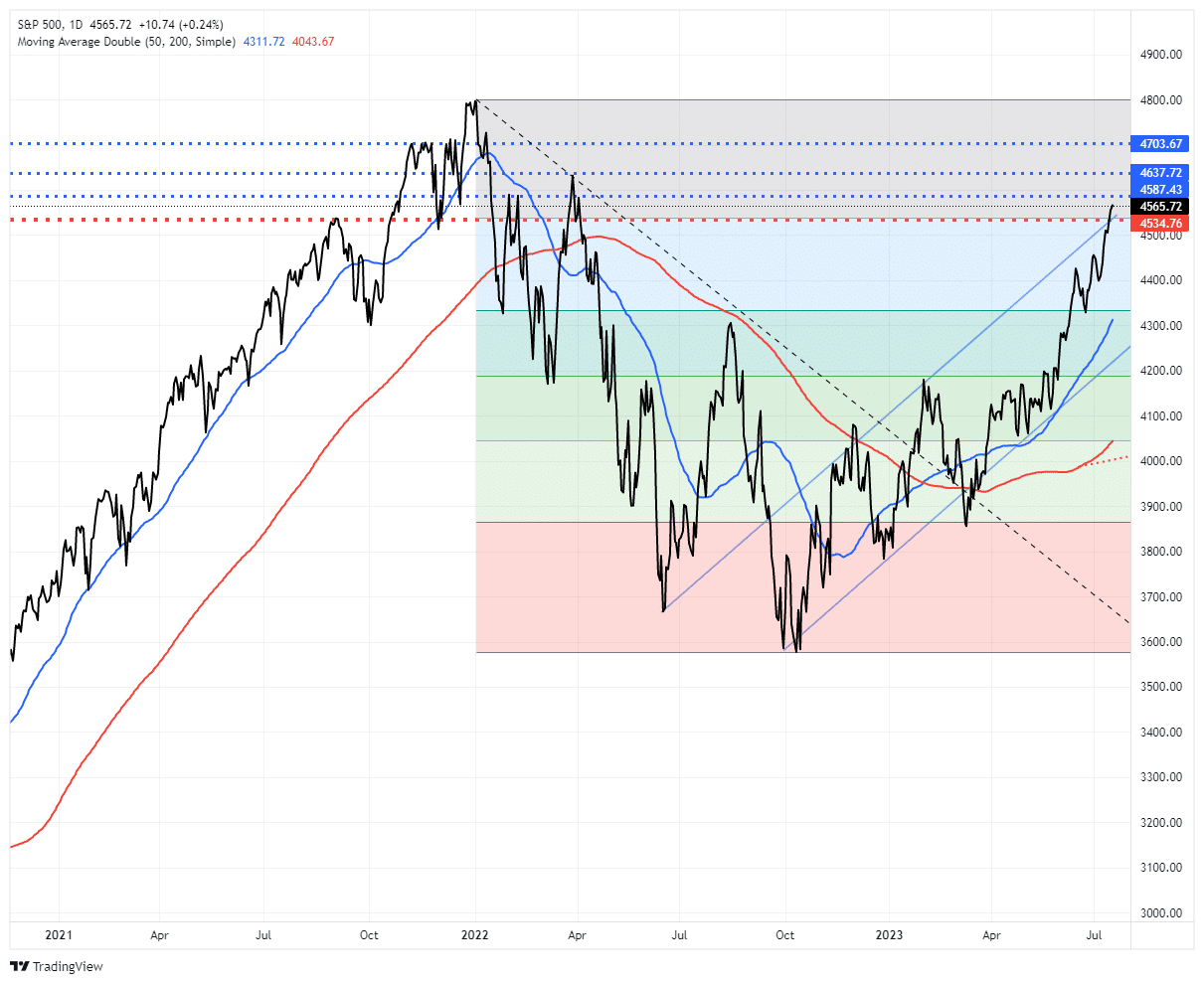

New all-time highs are coming. Given the fundamental and economic backdrop, I know that seems hardly logical, but that is what the technicals now suggest. The market has decisively cleared its 78.6% retracement of last year’s decline. Historically, when that occurs, new highs are a likely outcome. The combined momentum of the market, rising bullish sentiment, and the need to chase performance by managers are contributing to the seemingly unstoppable rally from the October lows. However, we must remember that market advances can only go so far before an eventual correction occurs. My best guess is that if the markets are going to reach all-time highs this year, we will likely have a correction first along the way. As shown, there is only minor resistance between here and the previous high. Any pullback to the 50-dma is likely a good entry point to increase exposure on a better risk/reward basis.

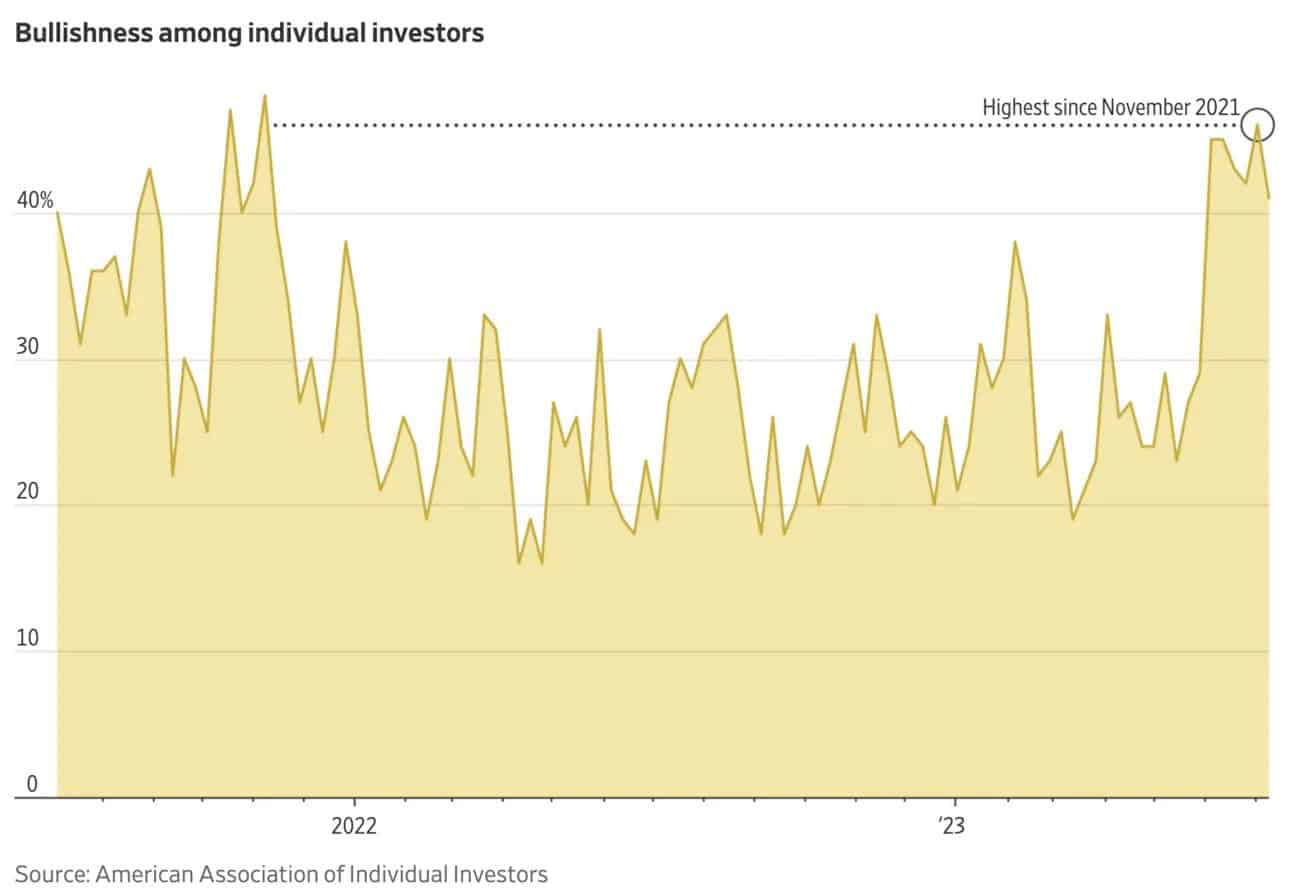

Investor Sentiment Rises, Gains Seem Easy, but 2021 Offers Caution

Despite the seemingly endless drift higher in stock prices, the graphs below offer us a reason for caution. The first graph shows that investor sentiment is now as bullish as it was in November 2021. The second graph, courtesy of @Macrocharts, shows the S&P 500 has gone 37 trading days without a 1% decline. The last time it ran up such a streak was in November 2021. Despite the fading sentiment in November 2021, the markets rose that December. Also, the lack of a 1% decline streak was broken. However, starting in the first days of January 2022, the market was not kind to investors.

The speculative mentality of late 2021 and today is similar. However, the economic and monetary policy environments are vastly different.

The bulls can claim that inflation is no longer a massive headwind, whereas it was just starting to kick up in late 2021. Further, in late 2021, it was increasingly probable the Fed would start to hike rates in 2022 and halt QE. Today, rates are very high, but the likelihood is that they will reduce rates or keep them stable over the next year at the worst.

Bears can claim that economic growth is weakening, the yield curve is steeply inverted, and the lag effects of prior rate hikes are slowly but surely working through the economy. Further, while the market seems to think rate cuts are positive, they almost always occur during recessions and have typically been troublesome for stock prices.

The main purpose of the stock market is to make fools of as many men as possible. – Bernard Baruch

Initial Jobless Claims are Set for Liftoff

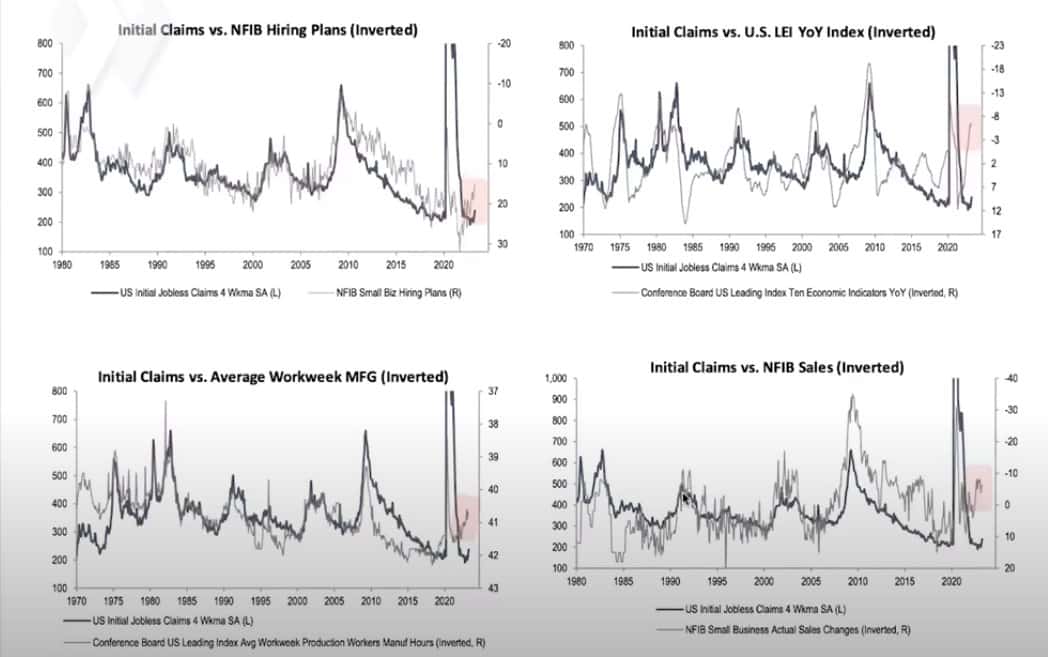

The picture below is from a pitchbook by Michael Kantrowitz of Piper Sandler. He firmly believes that the lag effects of prior rate hikes are slow in the making, but we mustn’t forget about them. The E in his HOPE framework, which helps show the progression of economic data into recessions, is employment. For more on HOPE, please check out our article, Janet Yellen Should Focus on HOPE. The article’s takeaway is that employment is always the last significant economic indicator to turn negative before a recession. Weekly initial jobless claims data is the best real-time look we have regarding employment trends. Most other labor data are monthly.

The graphs below show that initial claims strongly correlate with NFIB (small business) hiring plans and sales, leading economic indicators, and the average manufacturing workweek. All four graphs show that initial claims have slowly ticked up. But more importantly, the indicators warn the trend will continue and possibly at a quicker rate.

Headlines can be Deceiving

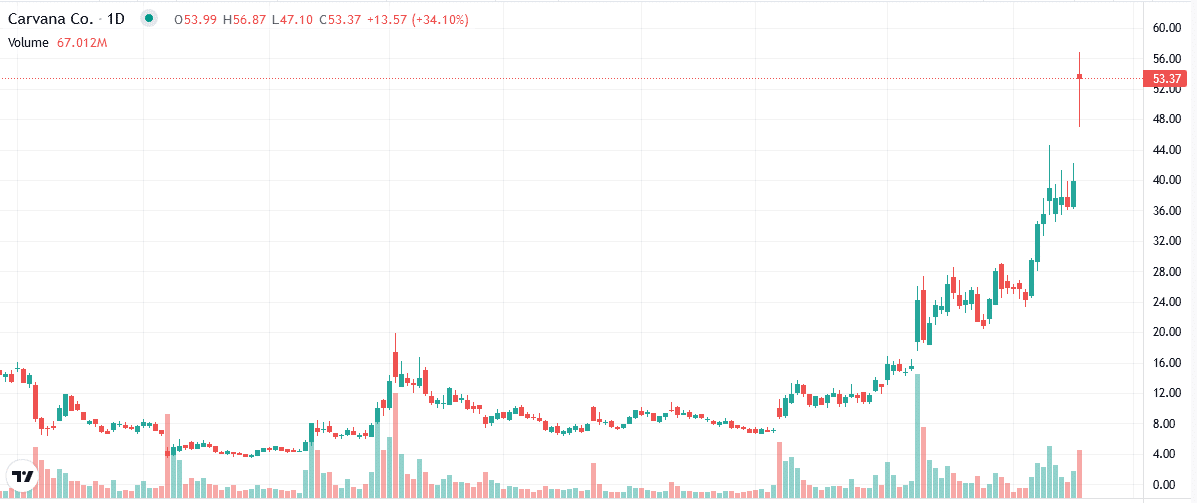

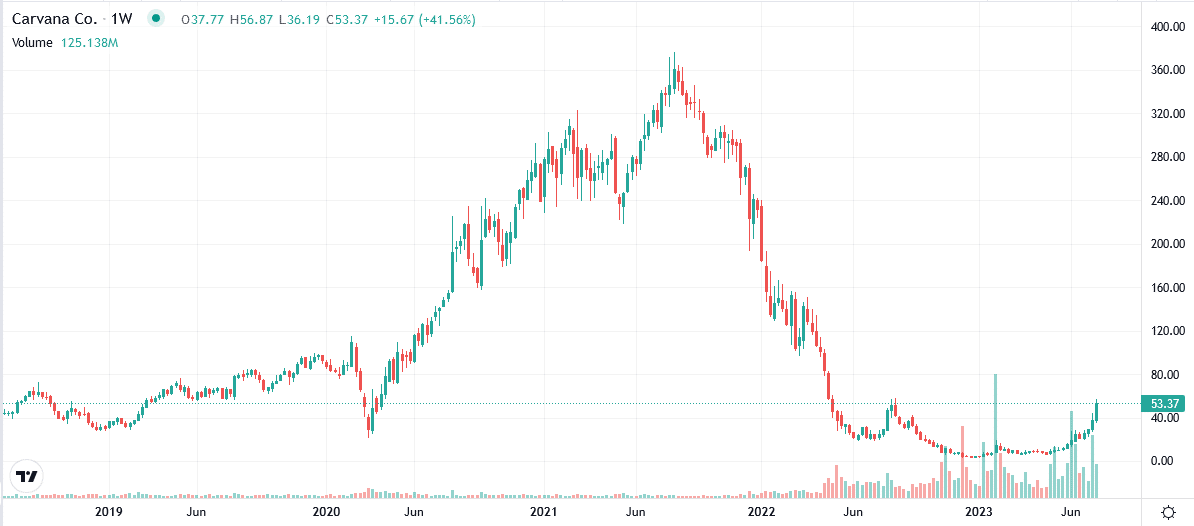

Carvana (CVNA) Stock Surges 1,100% This Year in Windfall for Investors- Bloomberg

The Carvana headline above, and many others like it, tell the story of stock flying higher. Many readers may feel the urge to jump on board. The headlines, however, are a bit deceiving. The first graph below shows Carvana is indeed up over 1000% from its sub $4 price in late December 2022. The second graph provides context for the recent price surge. Since hitting $376 in August 2021, the stock is still down 85%.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.