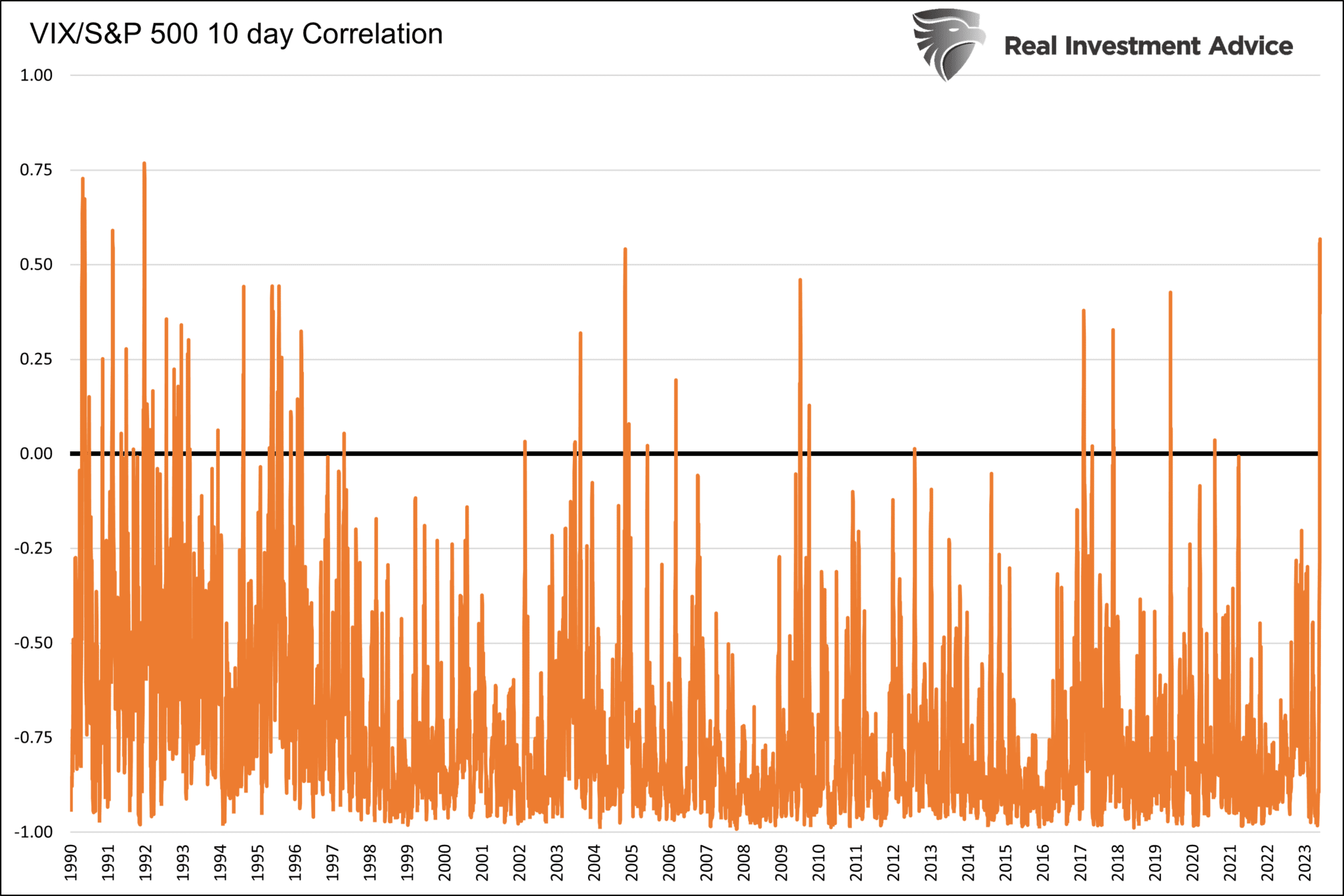

Over the last thirty years, the relationship between stock prices and stock market volatility has been strongly inverse. In other words, lower stock prices are often accompanied by higher volatility and vice versa. Over the last two weeks, the relationship has been flipped on its head. Despite a few moderate declines in stock prices, volatility failed to increase. The recent relationship defies everything we are accustomed to, as volatility and stock prices are tracking each other.

In the 8,424 trading days since 1990, there have only been 180 instances where the 10-day correlation between volatility and stocks has been positive. Only a third of those times had a positive correlation greater than +.25. Since June 16th, the average correlation has been around +.50. Such a high correlation is a five standard deviation event, quite rare indeed! So, what does it portend? While the positive relationship is quite the anomaly, other instances of such positive correlation have not yielded definitive clues about the future. The average 10-day return following daily readings above +.25 is +.35%. Further, there have not been significant stock gains or losses in the short-term periods following positive stock and volatility correlation.

What To Watch Today

Earnings

Economy

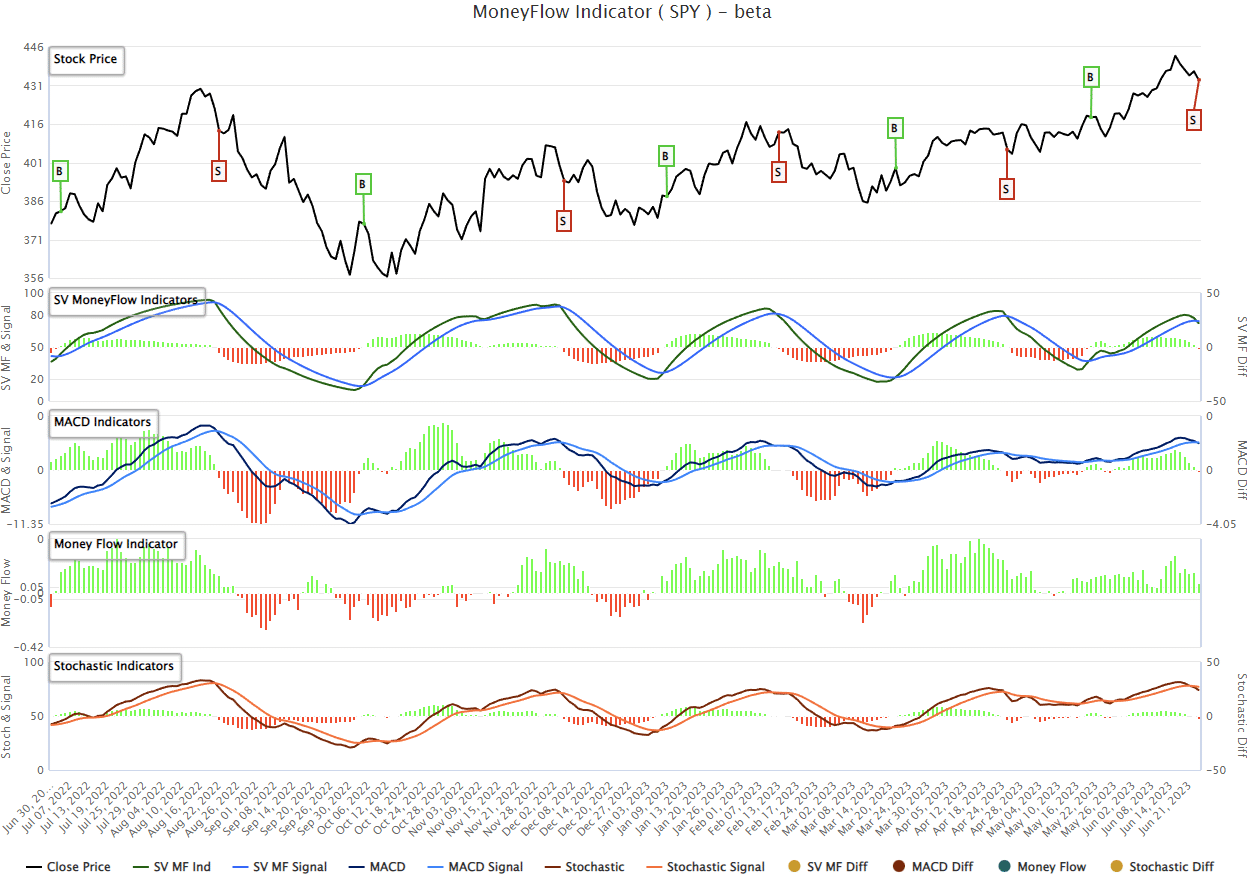

Market Trading Update

With yesterday’s sell-off, there are now confirmed sell signals on the S&P 500 index. While such DOES NOT mean the market is about to crash, it does suggest a period of limited upside. Overbought conditions can be resolved either through a pullback or a consolidation of prices. Notably, as shown by the heat map below, the sector rotation that we discussed a few weeks ago is now taking shape.

As shown, the SPY has triggered a confirmed sell signal.

However, the market is getting oversold enough on a very short-term basis that a reflexive bounce is likely. Look to use any bounce as an opportunity to derisk portfolios for now by rebalancing holdings and raising cash levels.

The most likely target for this correction will be around 4200, which is the 50-DMA. If that target is reached, we will reevaluate the technicals and determine the next course of action from there.

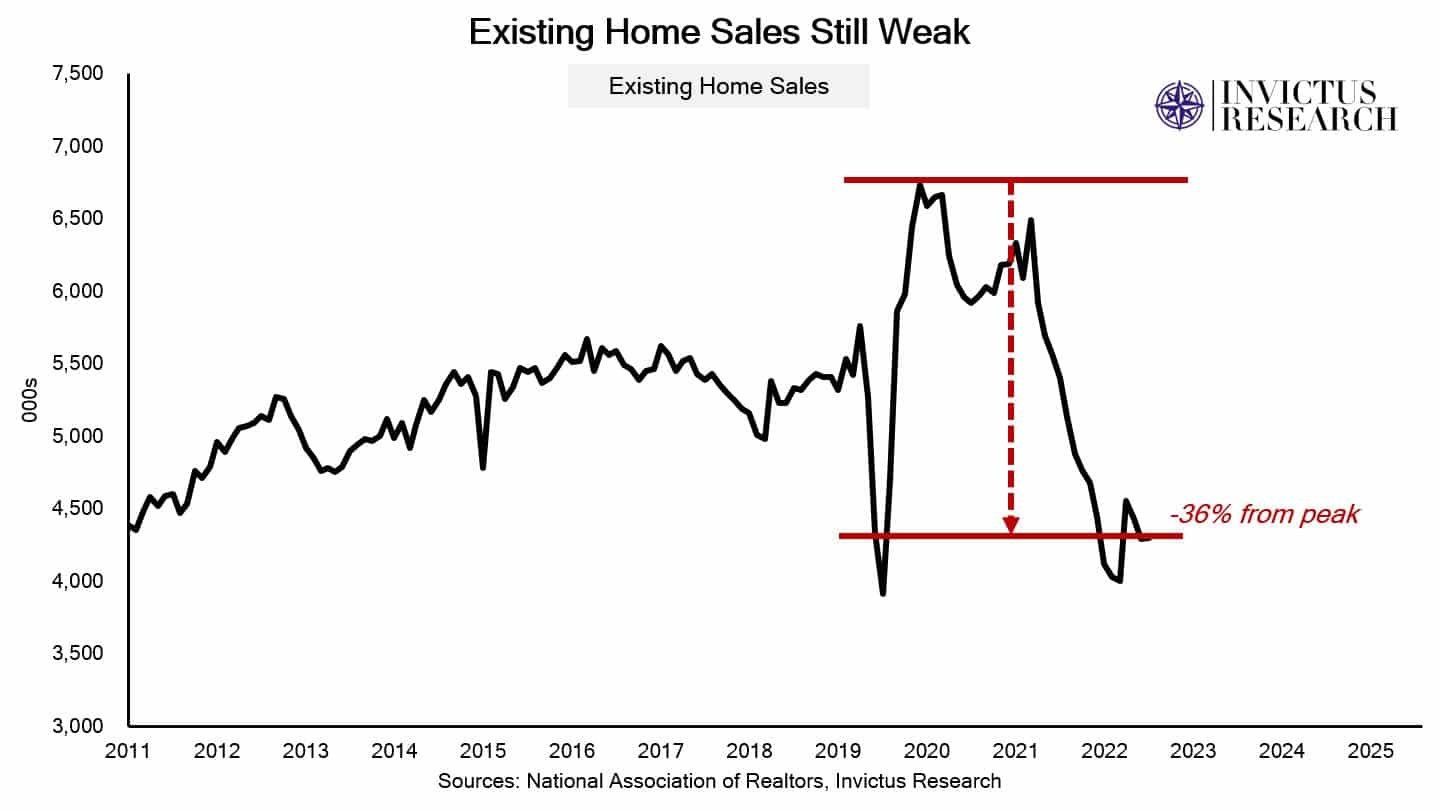

New Home Construction is on Fire, But…

Last week, much ado was made about the solid increases in building permits and housing starts. At the same time, the shares of many of the largest homebuilders rose to record highs. With mortgage rates at very high levels, the data does not appear to make much sense.

The graph below shows that existing home sales remain well off the surge peak during the pandemic. Further, they are hovering near 10-year lows. Consequently, it appears that the stagnant market for existing homes is creating an opportunity for builders to fill the void and meet some of the demand. Per the National Association of Realtors:

Available inventory strongly impacts home sales, too,” Yun added. “Newly constructed homes are selling at a pace reminiscent of pre-pandemic times because of abundant inventory in that sector. However, existing-home sales activity is down sizably due to the current supply being roughly half the level of 2019.

We suspect that lower mortgage rates will incentivize many homeowners to sell existing homes. If such occurs within the next year, the added supply of existing homes with the coming supply of new homes may create a glut of houses on the market. The only question at that point- is the pent-up demand to purchase homes strong enough to meet the supply.

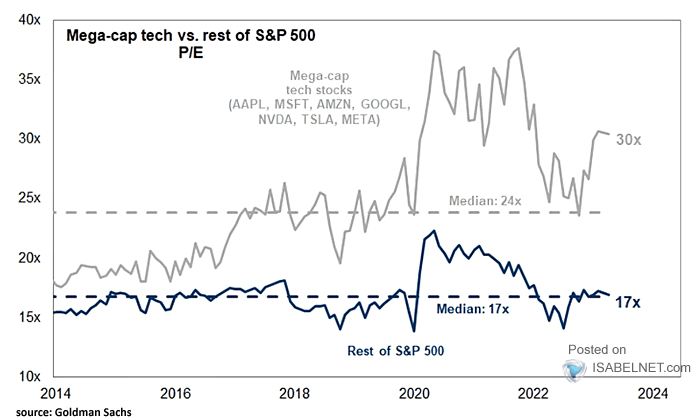

Valuations and MegaCap Distortions

We have shared several graphs and data points over the last month showing how a small number of mega-cap stocks were driving the market higher. The graph below, courtesy of Goldman Sachs and ISABELNET.com, highlights that P/E valuations for the seven mega-cap leaders jumped from 24 to 30 this year. They are now about 25% above the median valuation of the last ten years. At the same time, valuations for the rest of the S&P 500 reside at the 10-year median valuation. Using this time frame and valuation method, the market is expensive. Still, given that most stocks are near median valuations, a correction to the index median does not necessarily mean most S&P 500 stocks have to decline in price.

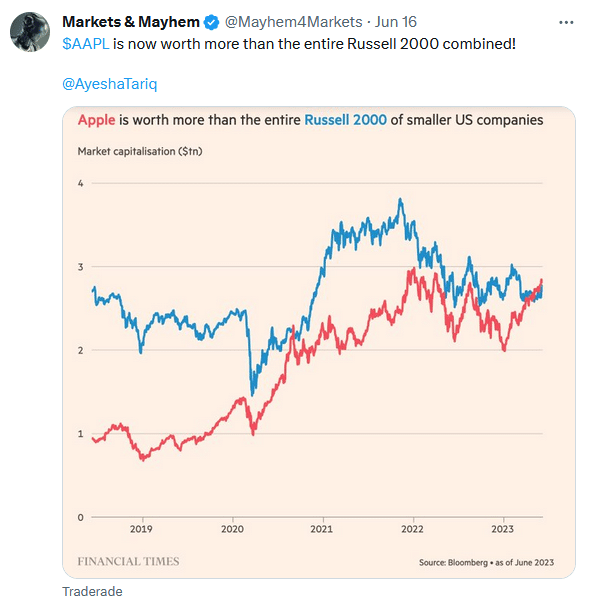

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.