Today’s Commentary focuses on passive investment strategies and how they are making difficult decisions for value investors. Passive investors tend to “buy the market.” By this, we mean they often focus on the largest passive ETFs. Some may buy the well-known index ETFs and call it a day. Other passive investors shift between stock factors like value or growth ETFs or funds focused on the market cap, for example. Within these categories, distortions have evolved as the funds and strategies grow in size. For example, value ETFs tend to favor stocks often considered “value” stocks but do not necessarily have value-like valuations. Often the stocks meet Wall Street’s self-serving classifications but not what a responsible investor would categorize as value.

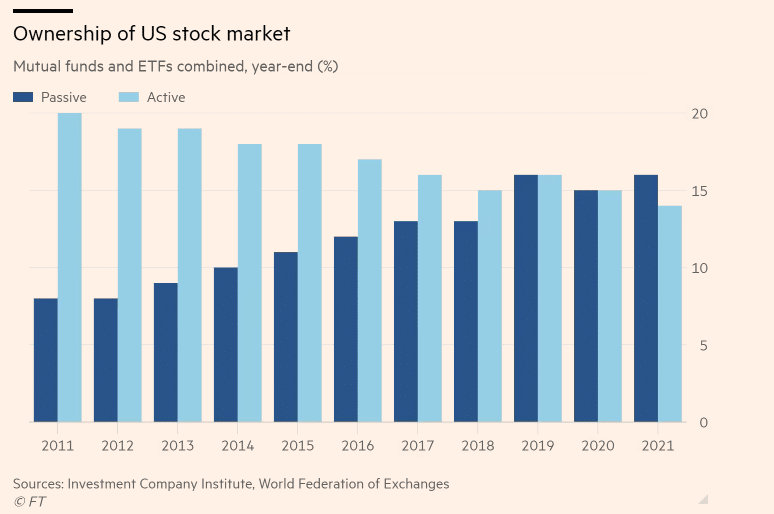

As popular ETFs grow, the stocks they prefer in their respective categories grow even more prominent and further inflate their valuations. But, it leaves those left behind with cheaper valuations and much more potential. The graph below, courtesy of the Financial Times, is dated but shows the steady progression of passively managed funds versus actively managed. The FT also notes that the ten largest ETFs and mutual funds own 66% of fund assets. As a result, value-based judgments of a small number of funds play an outsized role in partially determining winners and losers.

As value investors, we must often decide whether we buy the stock that has been outperforming despite lofty valuations or the cheap stock with tons of potential but not much in the way of recent performance. The sections below continue with more of how passive funds are skewing the market for value stocks and making life difficult for investors.

What To Watch Today

Earnings

Economics

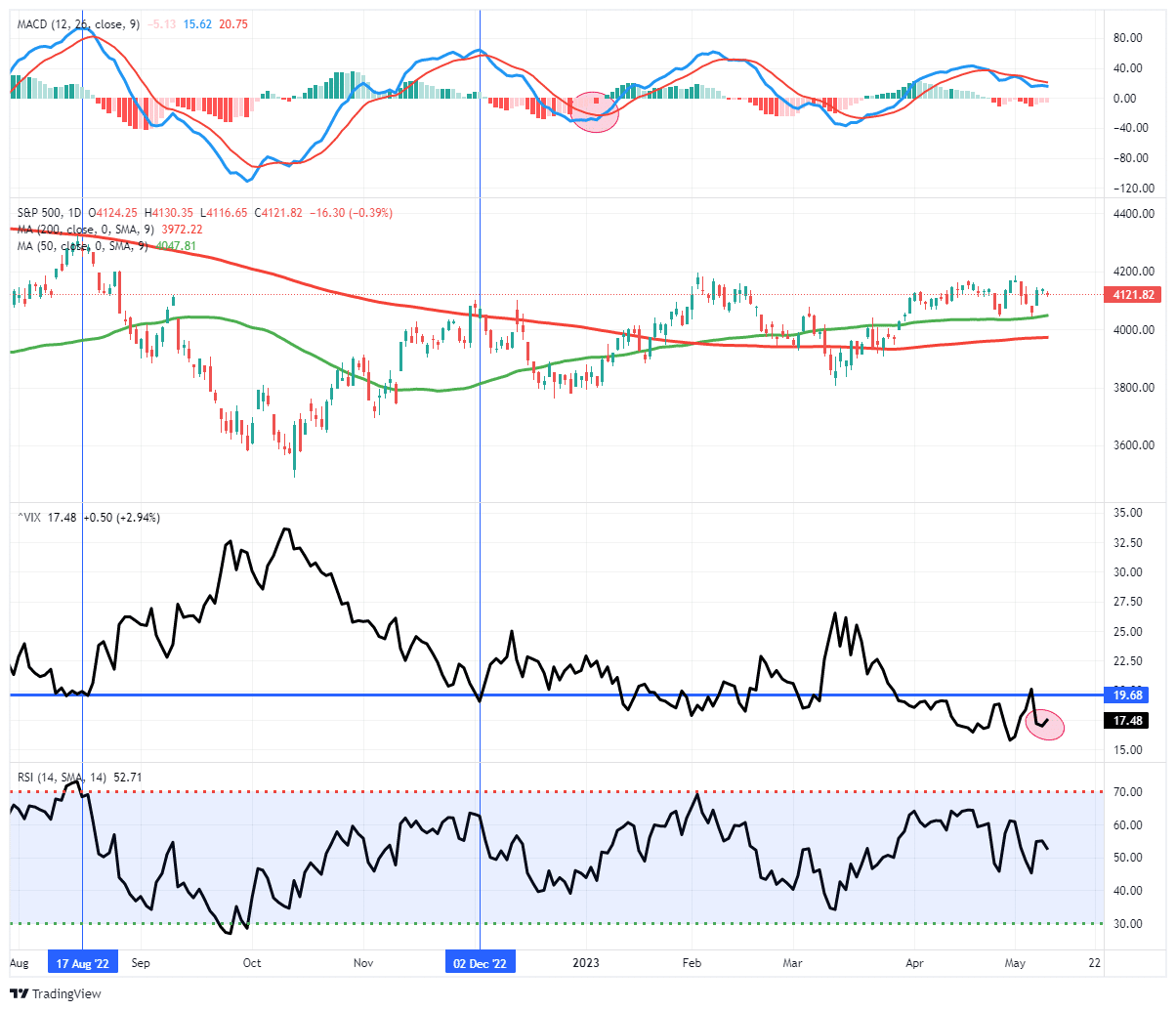

Market Trading Update

Today is the always much anticipated CPI report which will presumably “tell the tale” of the Fed’s next move. The Fed may have to hike rates again if the number is too hot. To cool, and maybe, as the bulls hope, the Fed will begin cutting rates sooner than later. The reality is that today’s report won’t mean a lot in the grand scheme of things. The Fed is likely on pause for now unless inflation is screaming higher, which the input data suggests it won’t be, and there is no reason for them to cut rates with the market and economy functioning on all cylinders.

The reality is that the market remains range bound for now and on a “sell signal,” limiting the current upside. One thing to note is the volatility index continues to drop. I suspect at some point, we may see a pop higher in volatility, coinciding with a sell-off in the market back to the 4000 level. Such will likely present a decent entry point to add some exposures.

The market has been rotating as late between inflation and disinflation trades which is expected. However, in the end, it will likely be the disinflation trades that continue to shine this year. Look to rotate allocations accordingly.

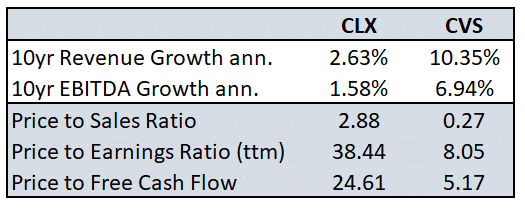

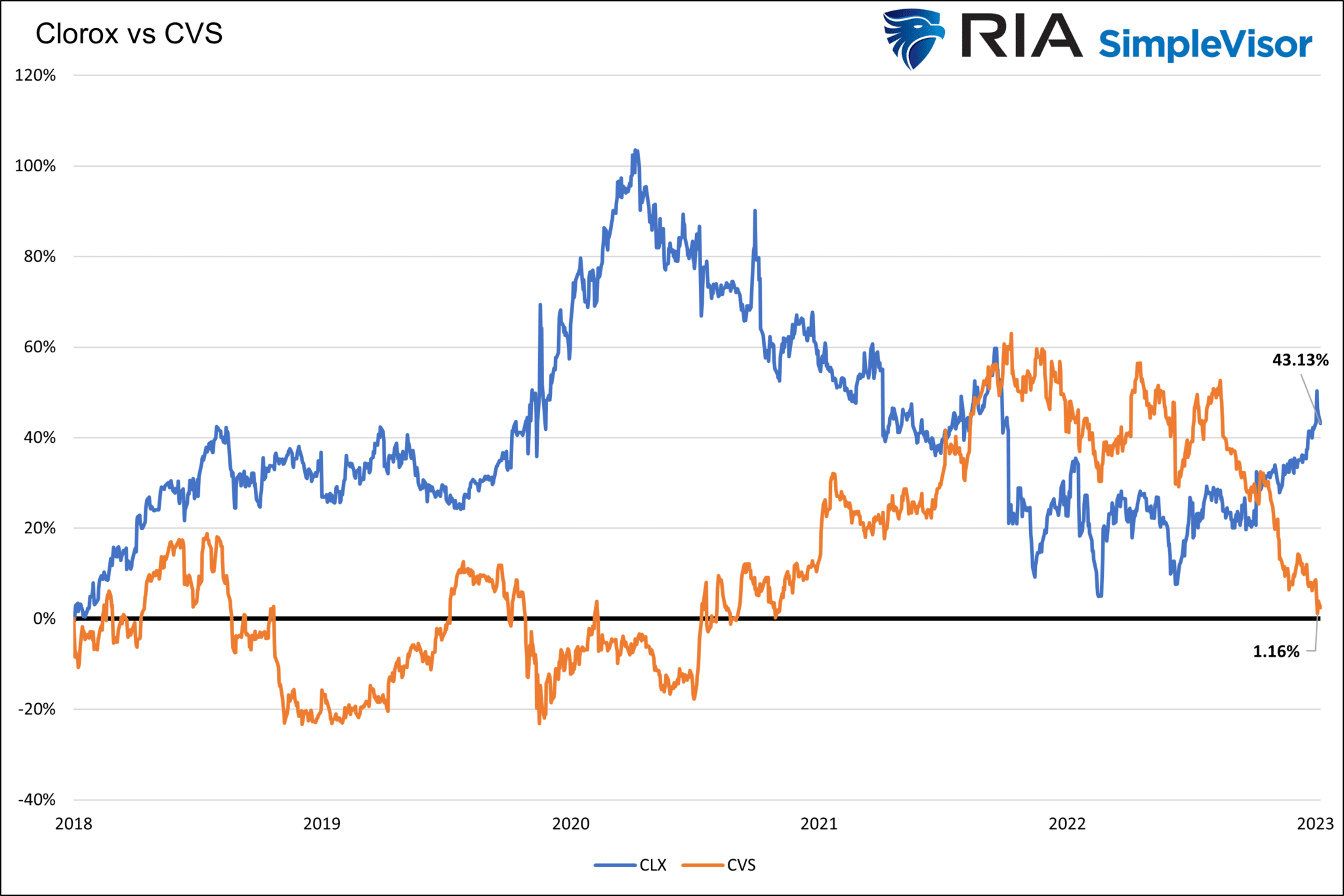

Main Street Value (CLX and CVS)

We lead with a question to appreciate better the value proposition and the problematic decisions investors must make.

Main Street USA has two identical-looking stores next to each other for sale. As a potential store owner, you want to buy a business with the most potential. The purchasing price of the stores is based on their sales. Both stores made $1,000,000 in sales last year. Store A sells for $2.8mm, and store B is $270k. So what do you get in store A worth 10x the price of B? While store A has an operating margin of slightly more than 2x store B, it has only been growing its sales and earnings at about one-fifth of the rate of store B. Most importantly, assuming recent growth rates continue, store A should return the initial $2.8mm investment in 23 years. It will only take store B six years.

Which would you buy?

We presume you chose store B. However, store B is not always the right answer in the stock market. The correct choice is not necessarily the stock that produces the most cash flow per dollar of investment. Instead, it is the stock whose price will rise the most. The data for store A in the example is Clorox (CLX), and store B is CVS. The table shows that despite much more growth over the last ten years, CVS trades at low valuation ratios. CLX, with marginal growth, trades at growth-like valuations.

Regarding our question, do you buy the value stock with high or low valuations? The second graph shows the market has favored CLX and is not focusing on valuations. However, given its limited growth and high valuations, Clorox’s potential for future gains is marginal. Conversely, CVS has significant potential to increase its valuations and, therefore, stock price.

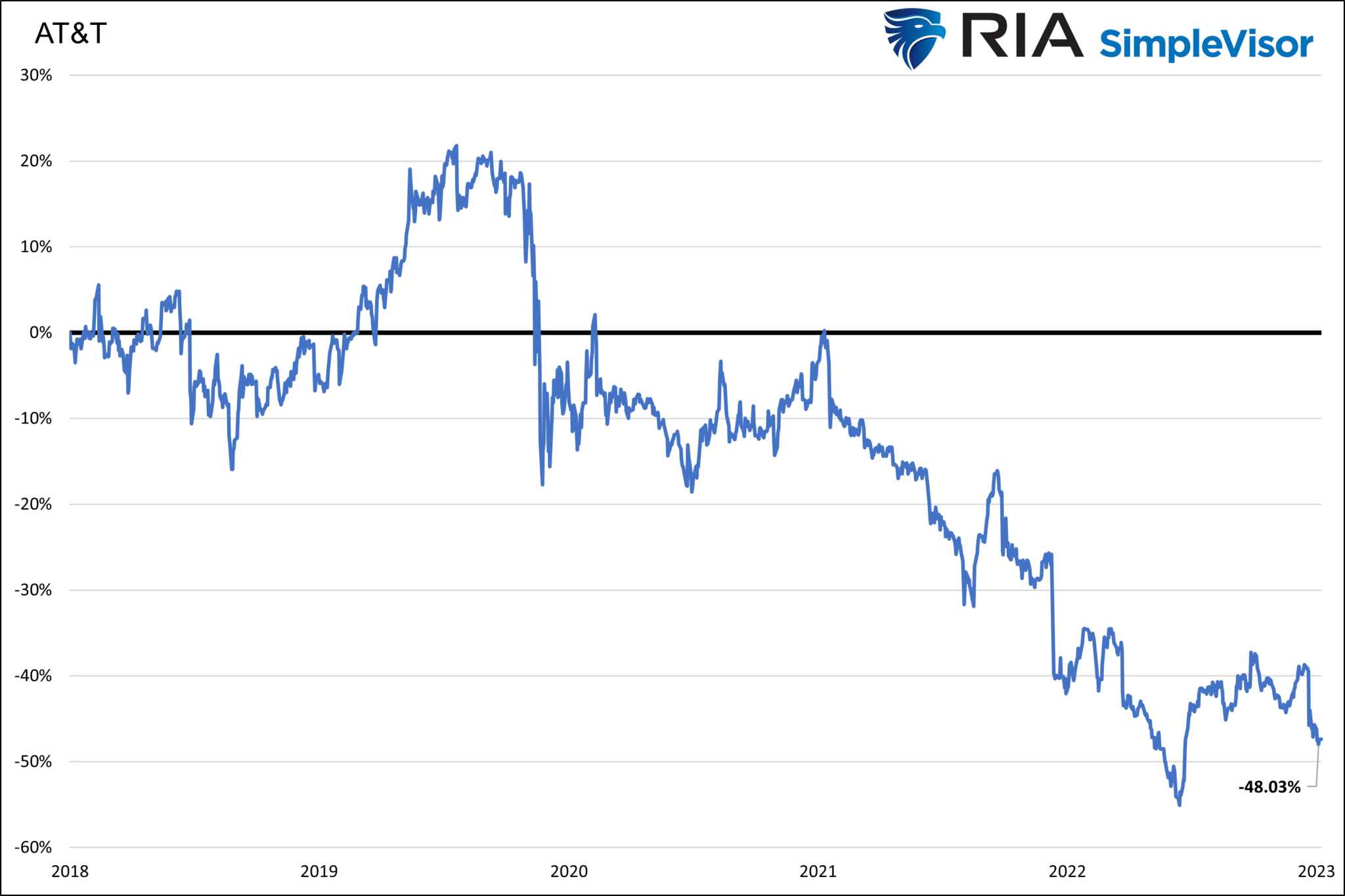

AT&T (T) – Another Lesson in Value

AT&T (T) is a more mature company with a flatter revenue and earnings growth trajectory similar to CLX. However, unlike CLX, T trades at a price to sales of 1.03, price to earnings of 6.73, and price to cash flow of 7.29. T is very cheap. T has an operating profit margin almost double CLX and four times CVS’s. Further, T incentivizes shareholders with a 6.48% dividend yield compared to 2.8% and 3.5% for CLX and CVS, respectively.

T not only has a high dividend and low valuations but is changing to promote more growth and reduce expenses. They recently began streamlining operations by spinning off Warner Media, DirectTV, and AT&T TV. The expectation is that the exit from the very competitive media industry will increase profitability in the near term. Also, T is in the process of upgrading from copper broadband cables to its fiber network. The upfront cost is expensive and drains earnings, but fiber will increase speed, increase customer satisfaction, and lower future maintenance costs.

Even with the changes to their business, T will not grow at CVS rates. Further, they have approximately $138 billion in debt. Higher interest rates are a threat given their debt level, but the company only has $7 billion in maturing debt this year. T is a cash cow providing investors with a lofty dividend yield backed by a 10.8% cash flow yield. For reference, CLX has a cash flow yield of 5%.

As shown below, T stock is down nearly 50% over the last five years. While the chart is likely scaring off investors, the company can reward patient investors with a significant dividend yield and, in time, price appreciation as its efforts to reduce costs and increase profitability pay off.

What’s an Investor to do?

Microsoft just announced they expect to grow 15-18% over the coming years. Compare that to Clorox, which will be lucky to grow at a few percent. Now consider CLX has a higher P/E ratio than MSFT.

In the April 26 Commentary, we looked at another value star, McDonald’s, which offers little earnings, sales growth, and high valuations. To wit:

Despite falling revenue and no earnings growth, the stock has risen nearly 4x since 2014. Buying back about 25% of its shares since 2014 explains some of the price gains. A more significant chunk of the gains can be attributed to valuation expansion. In other words, despite no growth, investors have been willing to pay more for the same dollar of earnings. Since 2014 MCD’s P/E has risen from 17 to 29. Its price to sales (P/S) is 9.3, three times its level in 2014. A price to sales of such a high level is often associated with high-growth potential companies, not low to no-growth firms.

Do we buy the high flyers and hope they can continue to defy valuation gravity? Or do we buy the beaten-down stocks offering investors a lot of potential? In the long run, it’s highly likely true value stocks like T and CVS will beat out non-value value stocks like CLX and MCD. But the distortion we note may continue to grow as passive strategies slowly take market share from active strategies.

We are value-oriented investors. But, in today’s climate, we must play the passive game and hold value stocks with high valuations. At the same time, we can mix in some stocks with deeply discounted valuations with a much more favorable risk/reward ratio.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.