On October 12, 1987, a week before Black Monday, the Wall Street Journal warned of the potential for significant market turmoil. Per the article: The use of portfolio insurance “could snowball into a stunning rout for stocks.” Today, we are increasingly alarmed that another trading tool similar to portfolio insurance could set markets up for a bout of turmoil.

The quote above and a detailed analysis of Black Monday can be found in a Federal Reserve white paper entitled A Brief history of the 1987 Stock Market Crash.

Despite the growing risk to foster market turmoil, 0DTE is a term few investors have heard of.

0DTE stands for zero days to options expiration. These are put-and-call options on individual stocks and indexes that expire within 24 hours. 0DTE options may seem like speculative YOLO (you only live once) bets at first glance. However, when one appreciates how brokers hedge options, they then grasp the potential for these options to generate significant volatility in individual stocks and the market.

Before exploring 0DTE options, it’s worth briefly discussing portfolio insurance’s role in Black Monday 1987.

1987 Portfolio Insurance

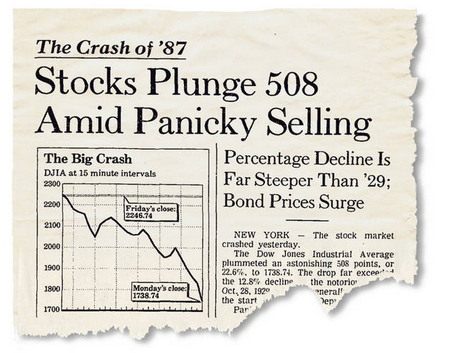

One of our first reactions to hearing of the recent popularity of 0DTE trades was to recall Black Monday and the 22.6% crash of the Dow Jones Industrial Average on October 19, 1987. There are several causes for the turmoil, but the factor that significantly amplified the decline was portfolio insurance.

At the time, institutional investors were buying portfolio insurance from Wall Street brokers to help protect against losses. During market declines, the brokers’ computer algorithms would automatically sell S&P 500 futures contracts short. As the market sold off further, the algorithms would sell more contracts.

As the programs sold, they pushed markets lower, necessitating more portfolio insurance-related selling. Selling begat selling, and a correction turned into an avalanche of panic.

The following quote is from a Wall Street Journal article rehashing the turmoil:

The strategy backfired, probably because too many institutions were doing the same thing at more or less the same time. They pushed stock prices into free fall and individual investors under the bus.

0DTE Options

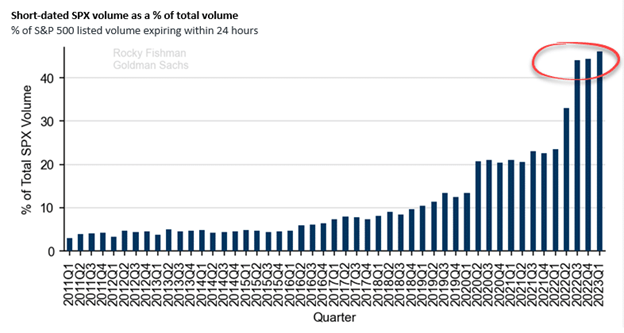

The popularity of 0DTE options is rising precipitously. As the graph below shows, half of the volume of options on S&P 500 futures are 0DTE. That dwarfs the 5-10% share existing before the pandemic.

Individual and institutional investors are using options that have a very short time until expiry for speculative and hedging purposes. It is also likely investors may be using 0DTE options to manipulate markets. Regardless of the objectives, 0DTE options have a similar feature as portfolio insurance; they can significantly intensify market moves.

To reiterate the WSJ quote: “The strategy backfired, probably because too many institutions were doing the same thing at more or less the same time.” Sound familiar?

How Manipulation Creates Signifcant Instability

To help better appreciate the risk of 0DTE options, we walk through a hypothetical example using Tesla stock. This case uses data from the early afternoon on January 25, 2023. After the close that day, Tesla reported its quarterly earnings.

Hypothetical hedge Fund ABC owns 100,000 shares of Tesla stock (TSLA). TSLA was trading for $144, which meant ABC had a $14,400,000 investment in TSLA. With earnings due shortly, ABC wanted a low-cost trade to juice their returns if earnings were better than expected.

One such way is 0DTE options. To do so, they could buy calls with a $160 strike that expired in a day. At the time, the price per 0DTE call was $1.36. Each call option controls 100 shares. If they chose, buying 1,000 calls would give them the right to purchase 100,000 shares at $160. The options cost was $136,000 or about 1% of their total Tesla investment. If TSLA shares flopped on earnings, they would lose 1% on the options. If the stock rose, they would likely sell the options and could easily double or triple their return. More importantly, their calls could force significantly more buying if the stock rose.

Delta Hedging Begets Delta Hedging

As frequently occurs, ABC indirectly buys calls from a Wall Street dealer. Most dealers run managed books meaning they have limited risk-taking tolerance. Accordingly, they often hedge their risks. In this case, the dealer’s risk is an increase in the price of Tesla.

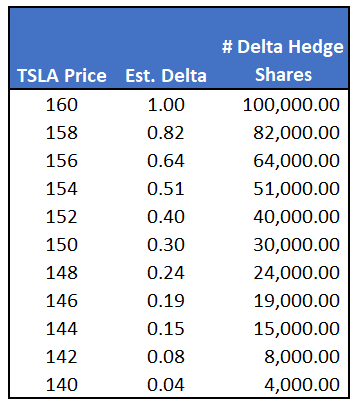

Dealers use a hedging method called delta hedging. An option’s delta estimates how much an option’s value may change for a $1 move up or down in the underlying security. The delta at the time of the trade was .15. For each $1 that TSLA shares rose, the options would increase by 15 cents. The delta increases toward 1.0 as the price approaches the strike price and falls toward zero as the price declines.

The dealer might initially delta-hedge the calls in our scenario by buying 15,000 shares (.15*100,000). As the price rises or falls, the number of shares they own will change according to the delta. The table below approximates the delta for Tesla shares on that day for a range of prices.

If the hedge fund is right and Tesla has excellent earnings, the stock will jump and force the dealer to buy more Tesla. The further it rises, the more shares they must buy. As the dealer and other dealers increase their hedges, the buying pressure on Tesla shares increases and pushes the delta higher. Buying begets buying.

Options on The Market

The Tesla 0DTE example pertains to the movement of one stock. While Tesla’s price may be more volatile than it would have been without 0DTE options, its effect on the broad market is limited.

More concerning, investors are buying 0DTE calls and puts on the S&P 500 and other indexes. Often such options are purchased in advance of potentially market-moving events. Recently, CPI, Fed meetings, and employment reports have drawn sizeable interest from 0DTE traders.

Suppose 0DTE volume is large enough, and options buyers are betting on the same directional market move. In that case, the environment becomes ripe for significant market instability if dealers are forced to aggressively delta hedge. Adding strength to such an event, investors become irrational when markets fall precipitously. A considerable downward move could trigger other investors to panic sell. Selling could beget selling, and a few percent loss could quickly turn into a severe decline.

Summary

If you take one thing away from this article, it is that for every option, there is likely a bank/dealer on the other side of the trade. Risk management protocols force dealers to buy or sell up to 100 shares of the stock or index for each option. It takes little money for a hedge fund to manipulate stock or index prices and, therefore, little money to create market turmoil.

Unlike portfolio insurance, delta hedging is limited as the delta can only go to one or zero. However, a heavy dose of delta hedging could cause panic selling among other market players. Fear can beget fear!

Closing Note

When we calculated the TSLA 0DTE example, Tesla closed the day at 144.43 minutes before the company reported its Q4 earnings. Its shares shot 10% higher the next day on the most volume in six months. 0DTE certainly helped TSLA shareholders!