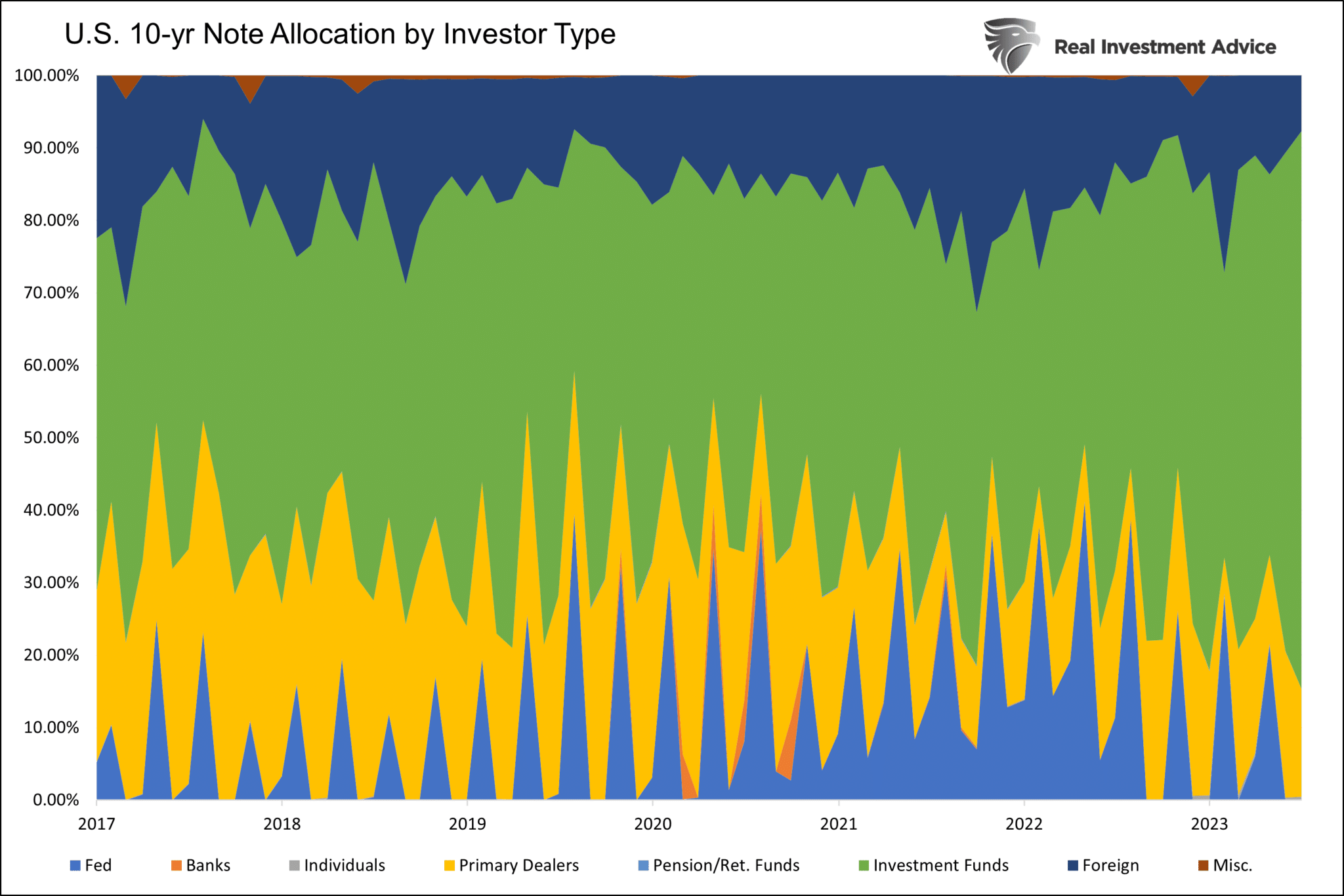

The U.S. Treasury will auction $38 billion of a ten-year note today and $23 billion of a thirty-year bond tomorrow. Often, volatility in the longer maturities perks up as the Treasury’s primary dealers position for the auctions. Per the New York Fed, the 24 primary dealers “are also expected to make markets for the New York Fed on behalf of its official accountholders as needed, and to bid on a pro-rata basis in all Treasury auctions at reasonably competitive prices.” The chart below breakdowns 10-year auction allocations by investor type. On average, since 2017, primary dealers accounted for 22% of the notes.

Before the Treasury auctions occur, the primary dealers trade the upcoming auction bonds in the when-issued (WI) market. This market allows dealers to position themselves so they can fulfill their job. They often get short before the auction with the goal of covering their short position at the auction. If the auction is strongly bid, these dealers usually have to cover their shorts after the auction as they were not granted enough bonds during the auction. Conversely, after a weak auction, they may end up with too many bonds and have to sell after the auction. The pre and post-auction trading of the Treasury bond market, the auction yields versus the WI yield, and various auction statistics can tell us much about the current demand from foreign and domestic investors and primary dealers.

What To Watch Today

Earnings

Economy

Market Trading Update

The correction process continued, which is something we discussed in yesterday’s commentary.

“As noted in yesterday’s “Before The Bell” video, a bit of a rally was expected, given the recent correction process. The short-term oversold condition, as shown by the relative strength index (RSI), suggested a probable bounce. That bounce came yesterday (Monday.) The key will be for the market to break above, and hold, the 20-DMA. If the market fails to climb above that current resistance level, a retest of the 50-DMA becomes more likely. With the MACD “sell signal” still intact and elevated, we would expect continued price weakness over the next few weeks.”

As noted below, the downgrade of regional banks, and the caution of a recession in 2024, led to a further repricing of stocks. This year, the market has rallied strongly on the expectation of “no recession” and increased earnings. However, a recession should lead to a repricing of stocks lower as earnings growth will decline during a recession. For now, the 50-DMA seems a logical level of support, with the selloff yesterday confirming the failure at the 20-DMA. When the market reaches that level we will reevaluate the associated risk/reward levels and determine our next course of action.

Bond Market Volatility

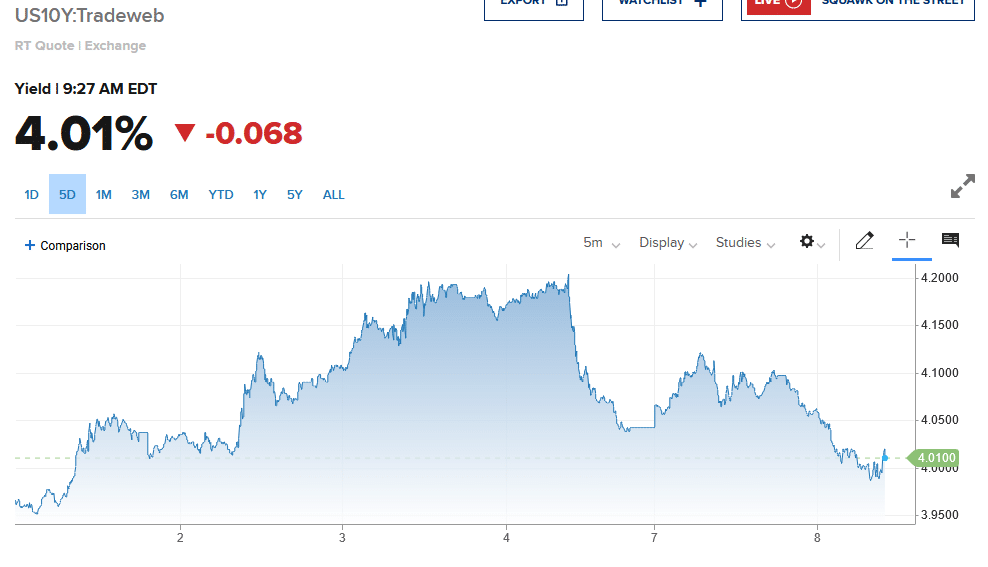

We opened the Commentary with a discussion of the coming Treasury auctions and the volatility that often surrounds auctions. As if large auctions were not enough for primary dealers and investors to deal with this week, there is also the debt downgrade and its potential ramifications. As shown below, despite the auctions and downgrade, the ten-year yield is almost unchanged for the month of August. However, it jumped 20 bps in the first few days and gave them up over the last few. That may not seem like much to stock investors, but for bond investors, it is. As we have seen thus far in August, volatility will probably continue this week and month as CPI on Thursday and the Fed’s annual Jackson Hole Conference later this month will keep traders on edge.

Moody’s Cut Ratings on 10 U.S. Banks

Moody’s cut the ratings of some large banks and put others under review for potential downgrade as they fear profitability pressures will reduce their ability to grow capital. The Fed’s hawkish policy stance, inverted yield curve, and fleeing deposits weigh on many banks’ earnings. Even more problematic, Moody’s expects a recession in early 2024 and, therefore, a pick-up in credit losses. Per the report:

“Risks may be more pronounced if the U.S. enters a recession – which we expect will happen in early 2024 – because asset quality will worsen and increase the potential for capital erosion.”

Bank of New York, US Bancorp, State Street, and Truist were among the larger banks put on review for a potential downgrade. The banking sector traded poorly yesterday on the news, with the Financials ETF (XLF) lower by about 2%.

Eli Lily Surges On Strong Earnings

Eli Lily (LLY) beat sales and earnings expectations, surging nearly 20% despite broad market weakness. Further fueling the stock price, sales of its diabetes drug Mounjaro were much better than expected, and they are seeking FDA approval to sell Mounjaro for obesity treatment. Eli Lily also raised its annual earnings outlook to $9.50-$9.70. Expectations were a dollar lower. Yesterday’s results mark only the fourth quarter in the last ten, where Lily has outperformed expectations.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.