Equity investors used the acronym TINA to justify buying stocks at excessive valuations. TINA followers believed that when bond yields were near zero, there was no investment alternative but to pay high valuations for stocks. Today, however, there is an alternative. In our recent article, Stocks versus Bonds, we share 150 years of equity valuation and bond yield history. The takeaway: Over the last 150 years, investors faced with CAPE valuations over 30, as they are, were almost always better off buying the ten-year U.S. Treasury. That advice pertains to long-term investors willing to sit with the same allocation of stocks and bonds for a decade.

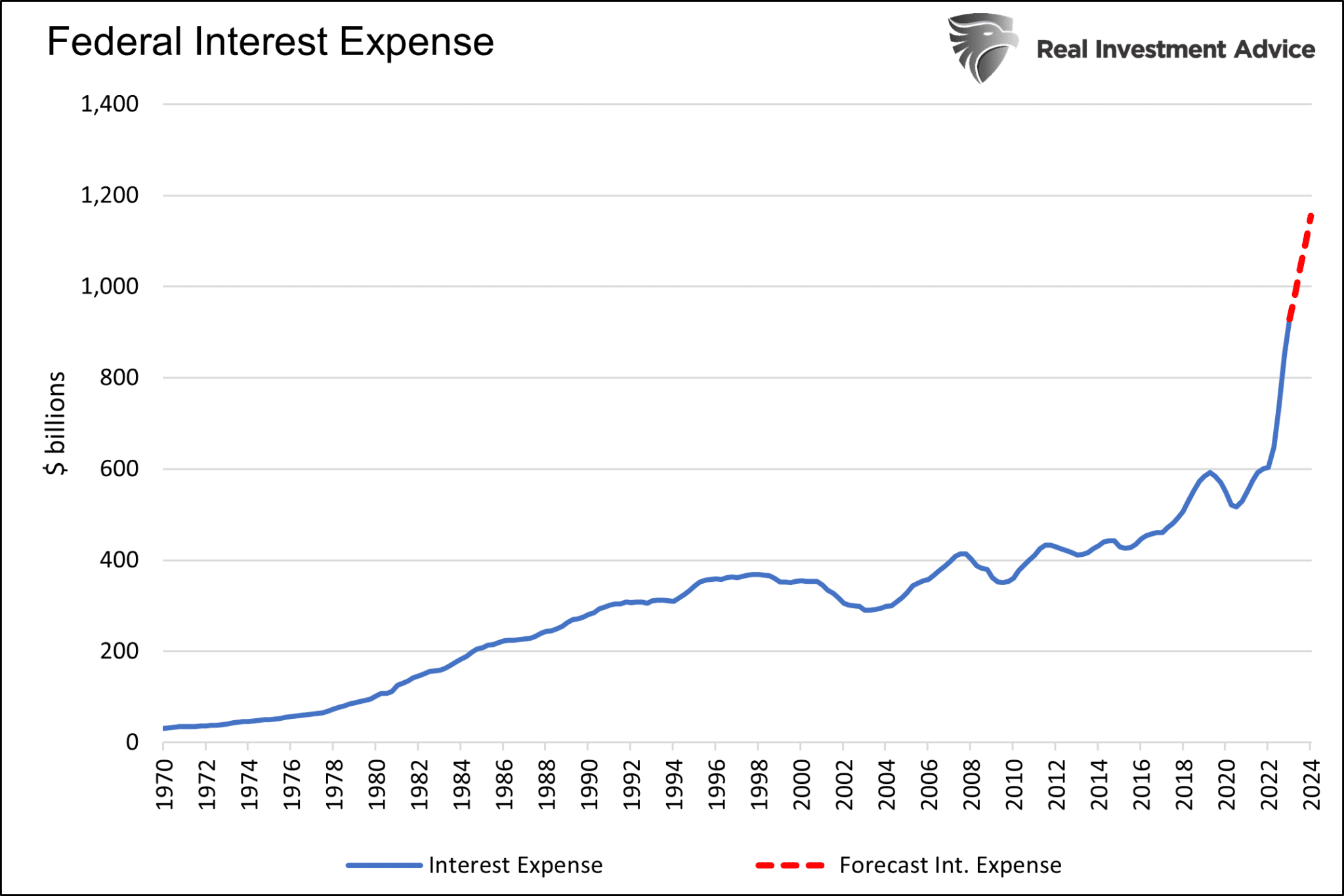

While the long-term advice from the article is to allocate more towards bond holdings, the prospect may seem scary at the moment, with yields rising rapidly on the debt downgrade. Well, we have some excellent news, TINA is back. Unlike the TINA above, this TINA applies to bond yields. The Fed and government have no alternative but to ensure interest rates over the longer term remain very low. The interest expense since 2020 has grown by the same amount as the fifty years prior. Interest rates will not drop immediately, but we are confident the Fed and government understand the harm of their higher-for-longer campaign. As such, rates are likely to be much lower in the future, whether it’s due to a weakening economy or Fed action. There is no alternative!

What To Watch Today

Earnings

Economy

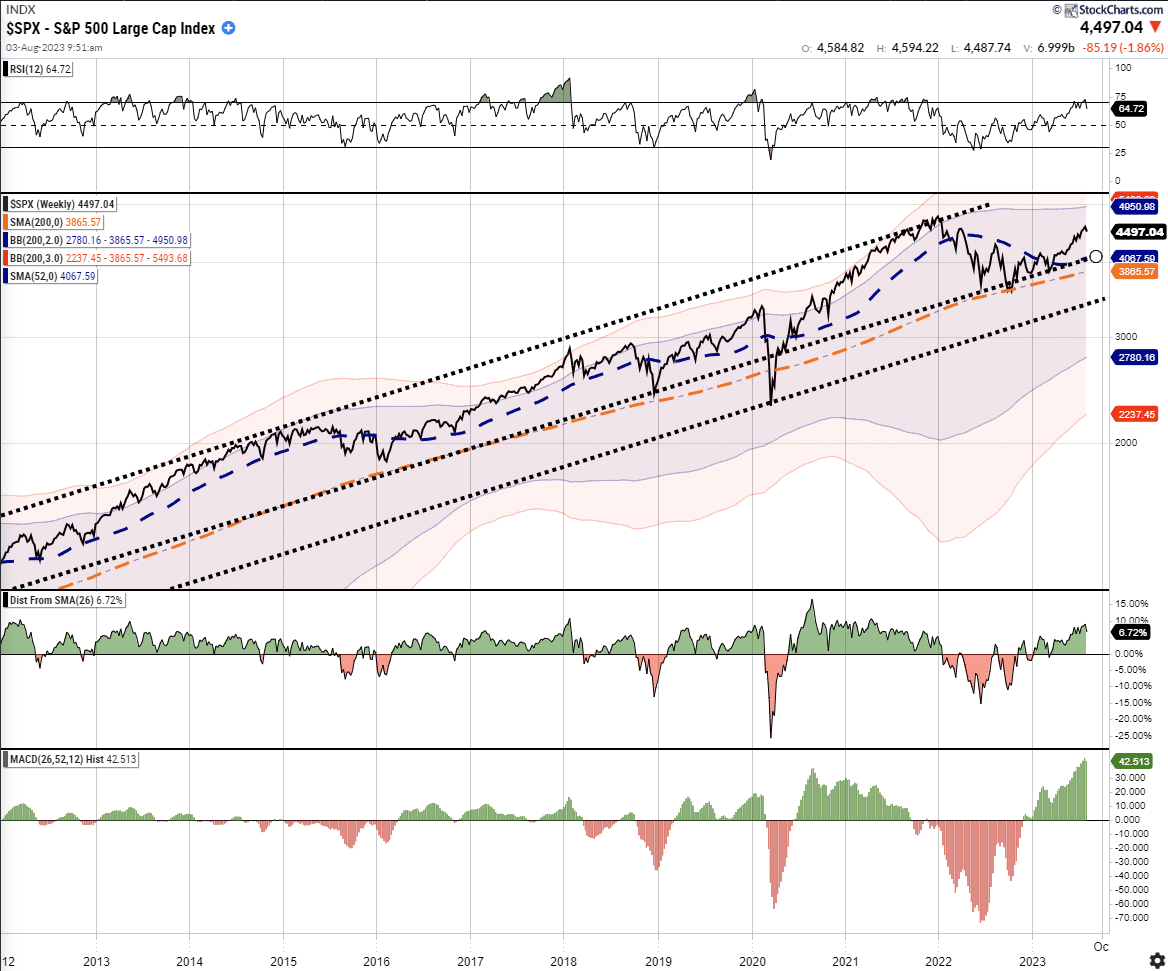

Market Trading Update

The trend is your friend. Over the last few weeks, we have discussed the much-needed correction in the market due to the short-term overbought condition. All that was needed was a catalyst to bring sellers into the market. That catalyst was Fitch’s downgrade of the U.S. debt rating. However, we want to keep an eye on the weekly chart of the S&P 500 for clues as to where the market heads next. Such is particularly the case as we head into the two weakest trading months of the year.

With the market overbought on a weakly basis and well deviated above its 26-week moving average, the current correction certainly has the potential for a larger retracement to the running uptrend line from 2009 which intersects with the 52-week moving average. That is the maximum drawdown expected for any corrective process. The 200-week moving average resides just below that level providing additional support to the bullish trend. Given the market’s current momentum, I suspect the corrective process will be confined to a pullback to the 4200 level. However, it is worth understanding the risk of a drawdown to 4000 is possible. With deviations currently elevated, the fuel for a larger correction is available.

The weekly chart below shows the potential correction levels, with the 13-week moving average providing first support at 4371. The 34-week moving average resides at 4152. Then as noted above, the bullish trend line and the 52-week moving average provide support at 4067, which is likely the maximum drawdown potential for this correction. When we get there, these levels will provide much better risk/reward entry points to add equity exposure. Trade accordingly.

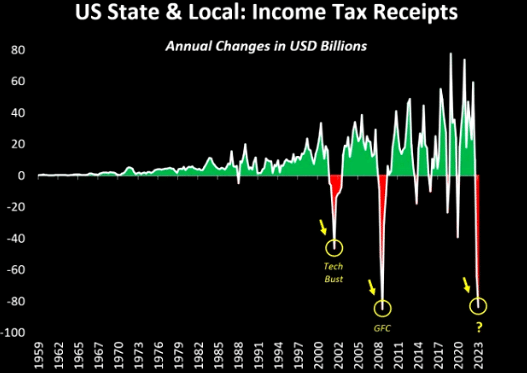

If Employment Is Rising, Why Are Taxes Falling?

The graph below from Tavi Costa is confounding, given the job market’s health. Unemployment is near 50-year lows, and the tightness of the labor markets is virtually unprecedented in recent history. If job and wage gains are as substantial as advertised, why are state and local income tax receipts falling? Further, the stock market is higher, as is interest income. Both should further propel tax receipts for the government. The second graph shows total federal tax receipts are also declining. Every time tax receipts shrunk annually, a recession was already in progress. 1980 was the only time we had a recession, and tax receipt growth stayed positive.

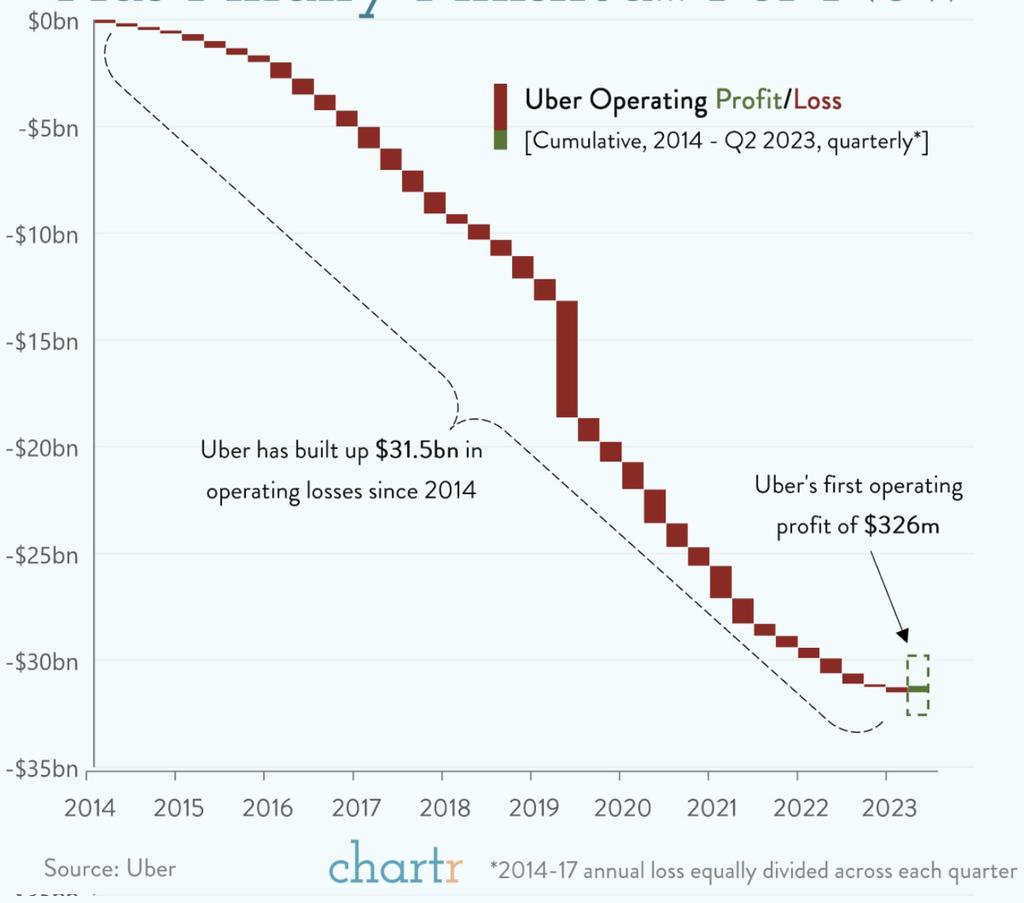

Uber Finally Turns A Profit

“This quarter’s profitability milestone is an important step, but it’s just a step”- Uber CEO

Since its founding in 2013, Uber finally turned a profit, as we share below courtesy of chartr. Uber IPO’d in 2019 with a market value of $75 billion. Since then, its market cap has risen slightly to $93 billion. The valuation has been on the heels of consistent losses. Is the trend finally turning, and is Uber on the way to justifying its market cap?

Got Bonds?

If the SLOOS survey, we highlighted in Wednesday’s Commentary, leads to a credit contraction, a recession may be in the near future, as Bloomberg’s economist suspects. Sentiment in the stock and bond markets is screaming otherwise. High yields denote strong economic activity and sticky inflation. Strong stock performance is predicated on the avoidance of a recession.

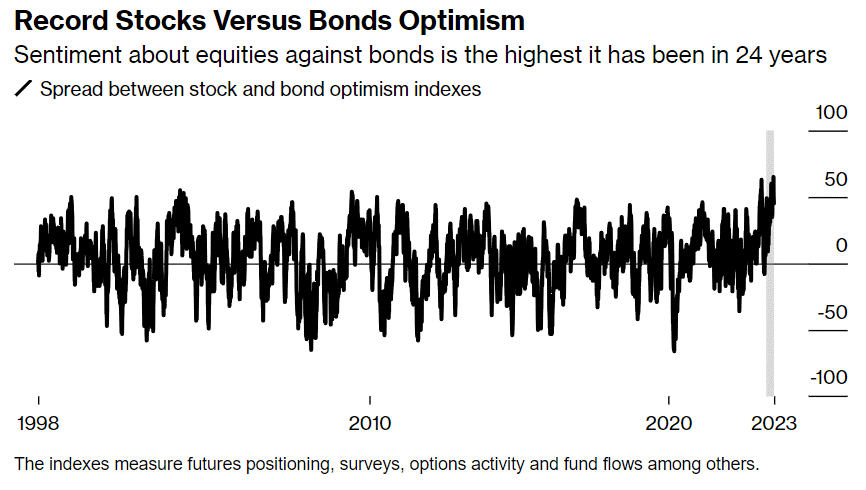

The difference between stock optimism and bond pessimism is the widest in at least 24 years, as shown below. The historical divergence in sentiment serves as a reminder of the old investment saying- “when everyone is on one side of the boat, it’s best to move to the other side.”

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.