“Call it a gold rush” started a Washington Post article, The Economy (Taylor’s Version), detailing the amount of money Taylor Swift’s tour is making for herself and how much economic activity it generates. For starters, the article estimates that Taylor Swift will personally rake in over $4 billion from her Eras Tour. The following statistics regarding her economic impact are from the linked Washington Post article.

To help appreciate the spending related to Taylor Swift’s tour, consider that those not fortunate enough to get tickets directly must pay an average resale price of $1,611 per SeatGeek. $1,611 just gets you in the doors. Food, hotels, merchandise, transportation, and other spending from her concertgoers is raining on the cities hosting her shows. The Washington Post estimates that each concertgoer will spend, on average, $1,279 per show. Over half or more of that figure is for expenses not going to Taylor Swift, her promoters, or the venue. The graphic below by the California Center For Jobs & The Economy estimates that her six Los Angeles shows may have added $320 million to LA’s GDP. In Seattle, single-day hotel revenue set a record, coming in about $2 million more than any other instance.

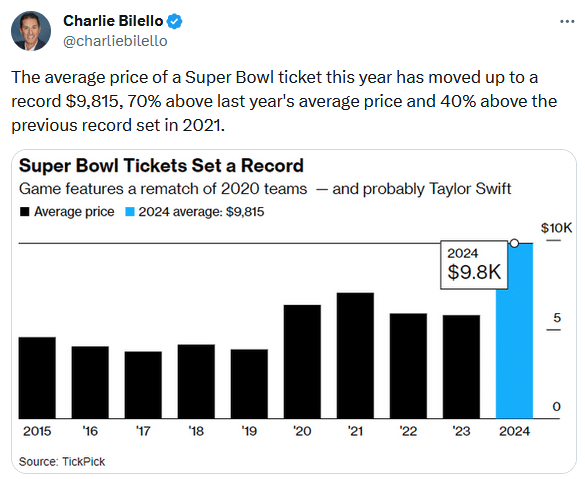

It’s not just tax revenue and local businesses benefitting. Per the article: “There have been longer-term lifts in employment, too. In Los Angeles, Swift’s six-day stop was estimated to generate enough revenue to fund 3,300 new jobs.” There are other benefits as well. For example, Taylor Swift’s relationship with Travis Kelce is worth $331 million for the NFL, per Market Watch. Tickets for this year’s Super Bowl are 70% higher than last year. The Las Vegas location is undoubtedly a draw, but so is the promise of catching Taylor Swift cheering on Travis Kelce and the Chiefs.

What To Watch Today

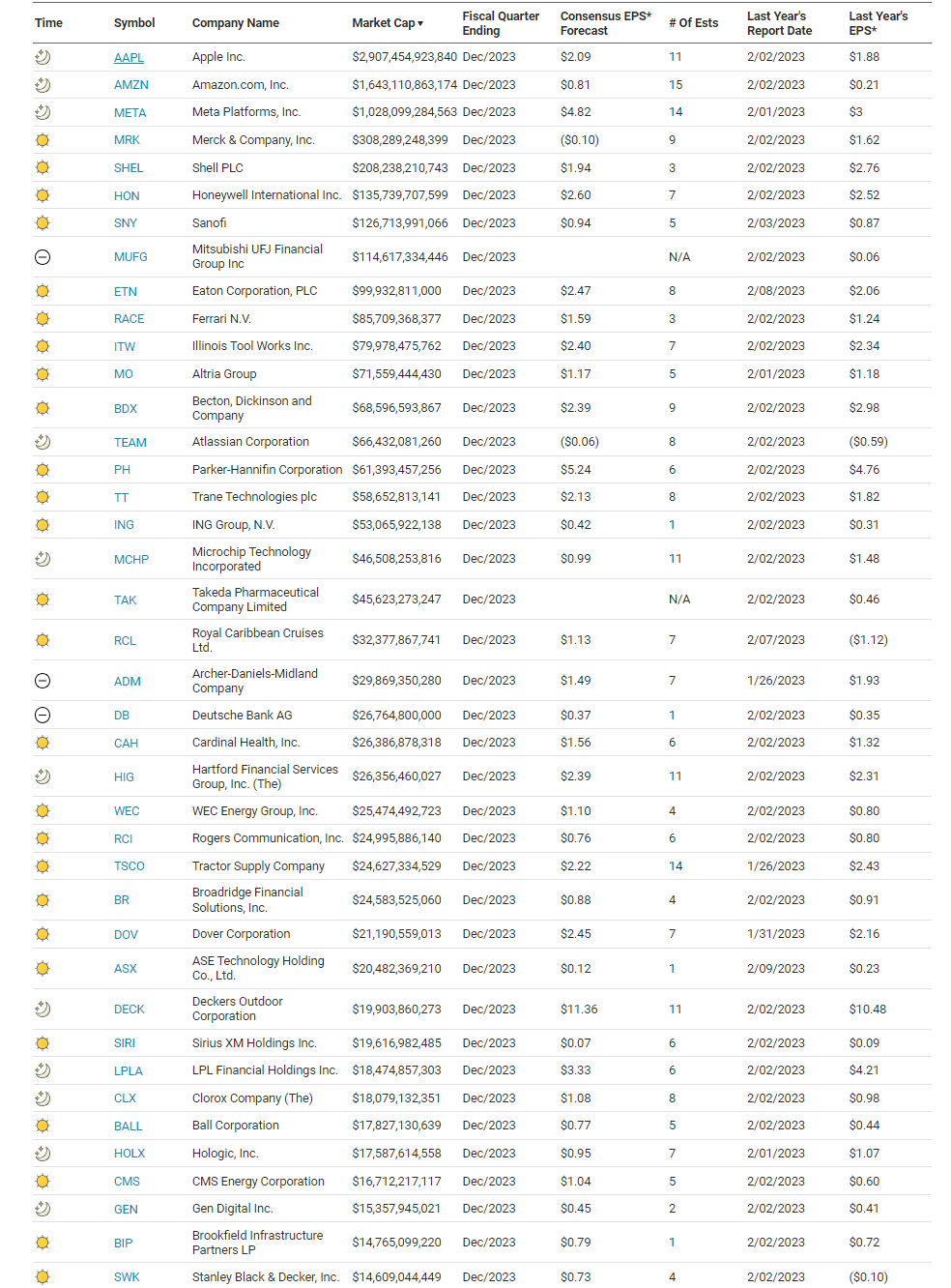

Earnings

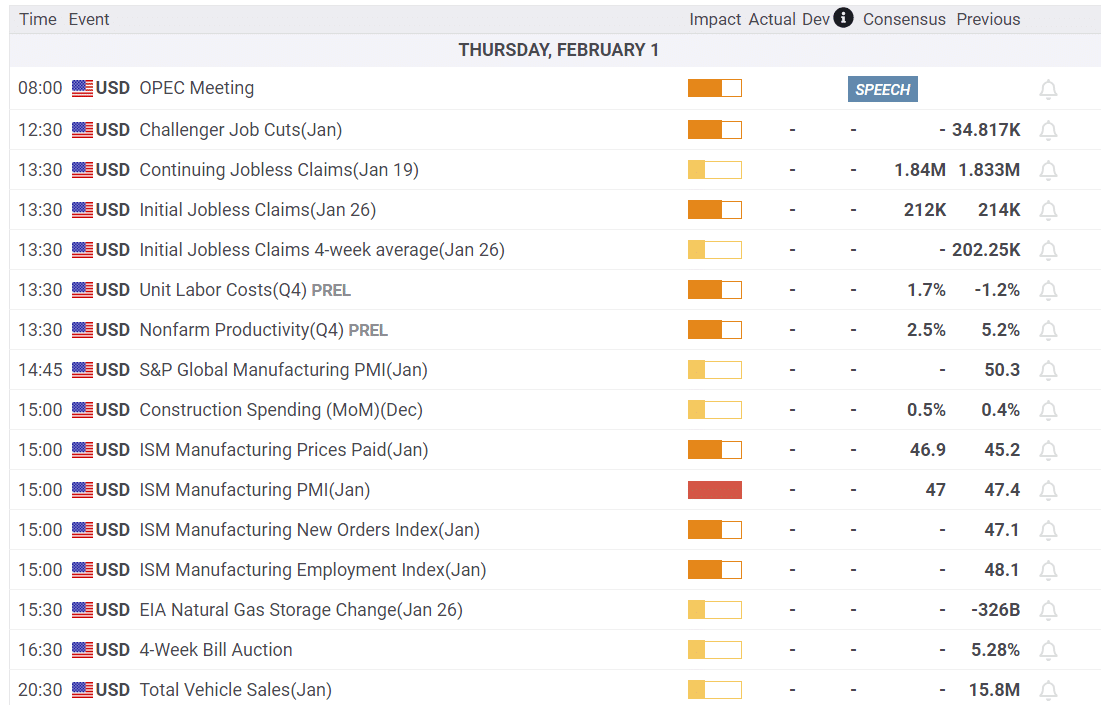

Economy

Market Trading Update

A bit of a hawkish surprise from Jerome Powell yesterday, as he took March rate cuts off the table, sent stocks falling more than 1% for the first time in a while. As we have noted previously, volatility has remained very muted as stock prices ground higher, which sets the table for a decent sell-off.

With the market overbought and deviating above the 50-DMA moving average, we suggested not adding new money to equity exposure until we achieved a better entry point. That correction started yesterday, and we likely have a bit more work to do before we get the next decent opportunity.

With the market sitting on the bottom of the trend channel, and the 20-DMA just below, if the markets can consolidate here and complete the reversal of the overbought condition, that would be bullish. However, a break of the 20-DMA will set the 50-DMA as the next logical target.

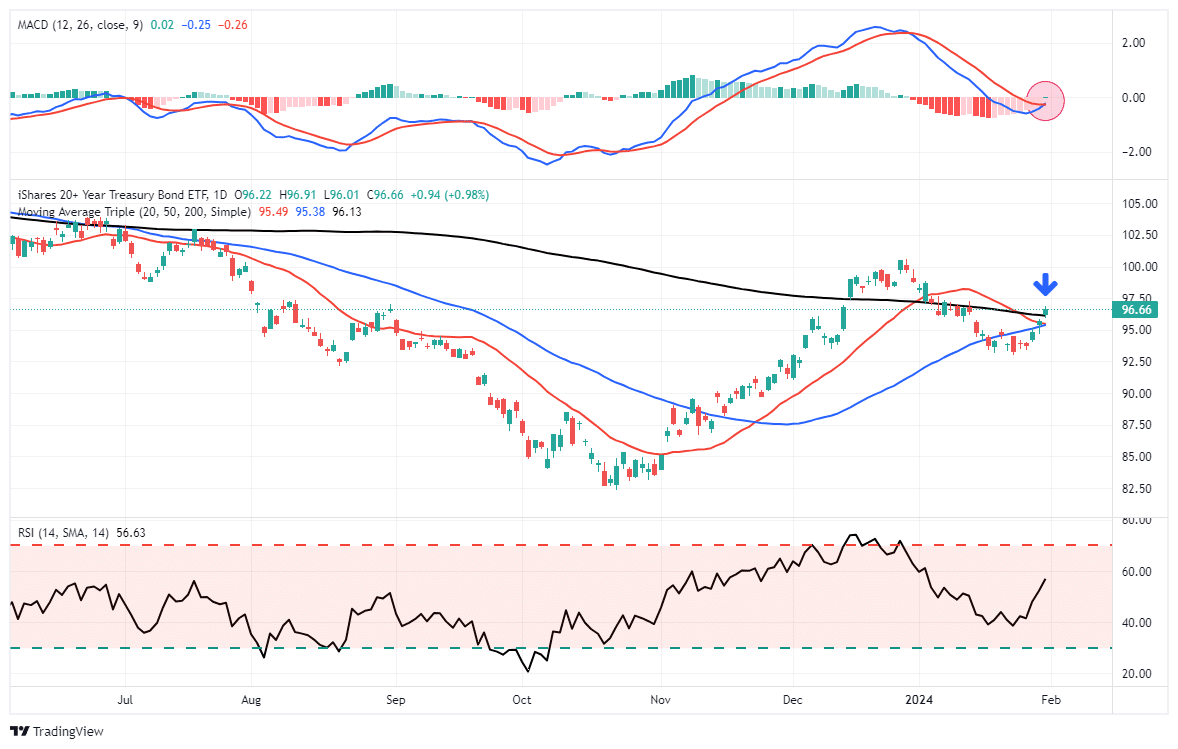

As noted yesterday, Bonds had another solid day as the Treasury funding statement suggested a switch in duration. We added to bonds in the client’s portfolios, and yesterday’s action confirmed that analysis. Bonds have triggered a MACD “buy signal” and taken out important short-term resistance.

Jerome Powell And The Fed

The Fed did not change its Fed Funds target but made many changes to the FOMC statement, as shown below. Of note, “the risks to achieving its employment and inflation goals are moving into better balance.” This signifies that monetary policy will not be as heavily guided by inflation. Accordingly, any weakness in the labor markets, coupled with the continued downward trend in price gains, may result in rate cuts. They removed language discussing rate increases, signifying that the tightening bias is gone. The bottom line from the statement is that they are most likely to cut rates but want to buy time to better ensure inflation is tamed.

The following thoughts and quotes are from Jerome Powell’s press conference:

- “We believe the policy rate is at its peak for the cycle”

- The Fed wants greater confidence that inflation is returning near 2%. They want to see “more good data.” Strong growth and a robust labor market are not stopping inflation from falling. Ergo, growth is not a hindrance to lower prices.

- The press repeatedly asked why the Fed should continue to hold rates higher. Powell repeatedly answered the Fed wants more confidence that “inflation is on a sustainable path to 2%.”

- Unexpected weakness in employment would get them to cut rates sooner.

- They know that flat-to-falling rent prices will work themselves into BLS inflation data. It is in their forecast.

- Regarding soft landing: “I wouldn’t say we’ve achieved that, and I think we have a ways to go.”

- “I don’t think it’s likely that the committee will reach a level of confidence by the time of the March meeting to identify March as the time to cut, but that’s to be seen.”

- The risk is not a resurgence in inflation but that price growth remains stubborn at current levels.

Are The Magnificent 7 Hiding An Earnings Recession?

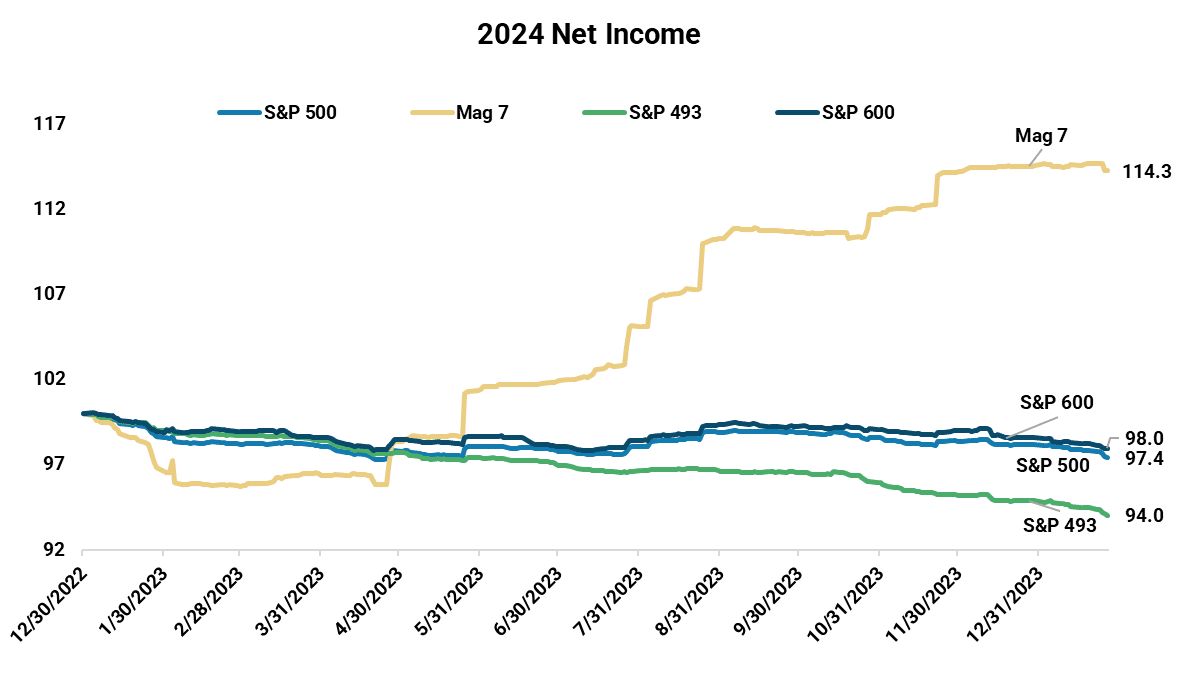

Looking at the market’s performance over the last six months would lead one to believe earnings are doing well. Since bottoming in late October, the S&P 500 is up about 16%. Unfortunately, the recent gain is all about a multiple expansion of the index and the gross earnings outperformance of the Magnificent 7. Since the end of the third quarter, the P/E ratio on the S&P has risen from 23 to 26. The increase is due to rising stock prices and declining earnings. Furthermore, earnings for the index are overstated when considering how dominant the Magnificent 7 stocks are. As shown below, earnings for the Magnificent 7 are up by about 14%, while the S&P 500 has declined by 2%. Stripping out the Magnificent 7, S&P 500 earnings are down 6%.

We often talk about the technical breadth of a market. Recently, the technical breadth has been poor, as witnessed by a few stocks leading the way higher and the share prices for most other stocks languishing. It appears the fundamental breadth is similar!

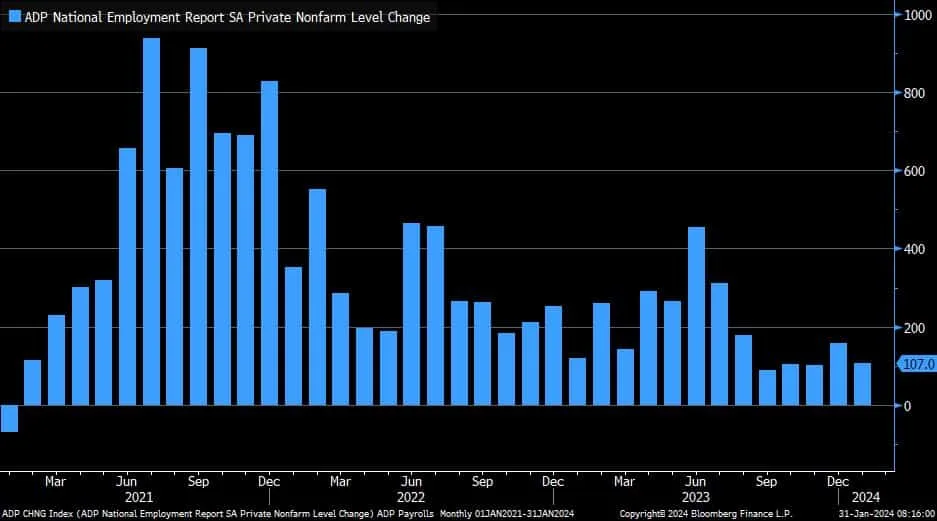

ADP Is Weaker Than Expected

The ADP report, a proxy for Friday’s BLS employment report, disappointed, adding only 107k jobs versus estimates of 162k. Per ADP:

The hiring slowdown of 2023 spilled into January, and pressure on wages continues to ease. The pay premium for job-switchers shrank to a new low last month.

The ADP has recently been reporting much slower job growth than the BLS. As shown below, four of the last five months have been near 100k. On average, the BLS reports the economy added 185k jobs per month over the same period. These two employment gauges were traditionally well correlated. However, since the pandemic, they have diverged. We suspect the BLS will revise their data lower in the coming years to match the ADP more closely. Remember, ADP uses actual client data, while the BLS relies on surveys.

Tweet of the Day

“Want to have better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.