Amazon is facing an existing FTC problem that escalated last week. On Tuesday, the Federal Trade Commission and 17 state attorney generals filed a lawsuit against Amazon for anti-competitive practices in its online marketplace. According to the press release,

The complaint alleges that Amazon violates the law not because it is big, but because it engages in a course of exclusionary conduct that prevents current competitors from growing and new competitors from emerging. By stifling competition on price, product selection, quality, and by preventing its current or future rivals from attracting a critical mass of shoppers and sellers, Amazon ensures that no current or future rival can threaten its dominance.

Amazon’s FTC problem has been culminating for years. Lina Khan, the sitting chair of the FTC, had her sights set on Amazon long before she began her role at the FTC. A lengthy note written by Khan was published by the Yale Law Journal in 2017, outlining her case for an updated antitrust framework in which the focus lies on Amazon’s dominance in the online marketplace. Although the FTC investigation into Amazon was launched in 2019, before Khan joined the FTC, this lawsuit certainly puts her assertions to the test. The following excerpt highlights the parallels between her 2017 paper and the press release above.

The titan in e-commerce is Amazon—a company that has built its dominance through aggressively pursuing growth at the expense of profits and that has integrated across many related lines of business. As a result, the company has positioned itself at the center of Internet commerce and serves as essential infrastructure for a host of other businesses that now depend on it. This Note argues that Amazon’s business strategies and current market dominance pose anticompetitive concerns that the consumer welfare framework in antitrust fails to recognize.

What To Watch Today

Earnings

- No notable earnings releases today

Economy

Market Trading Update

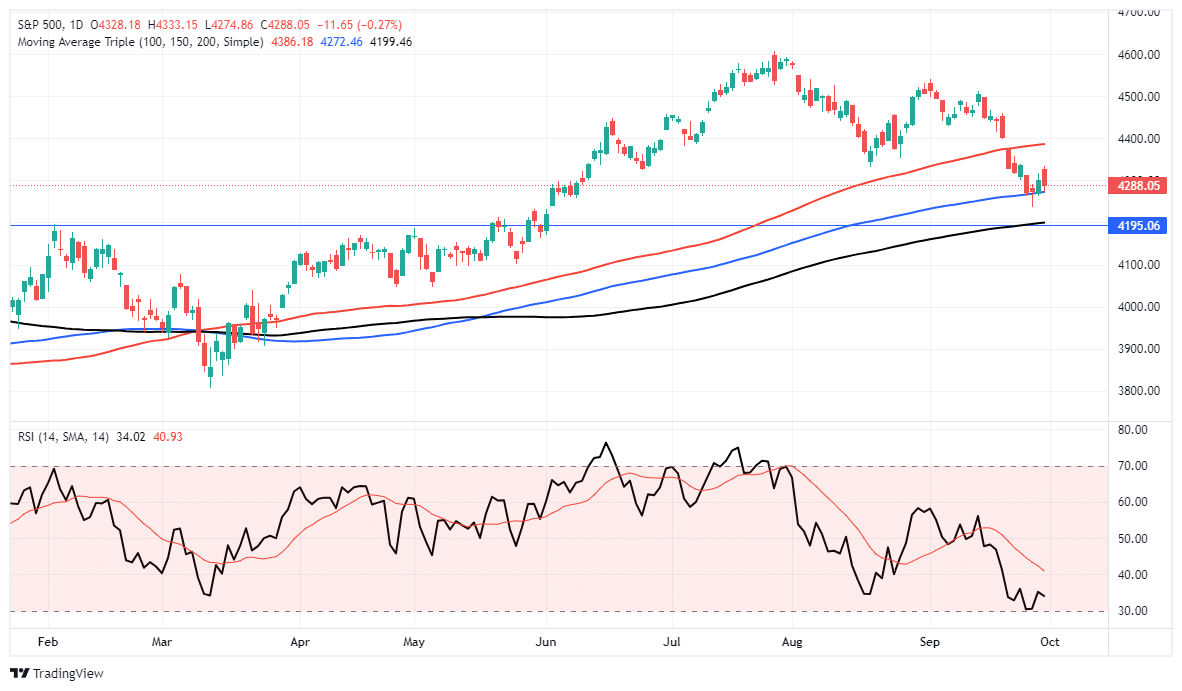

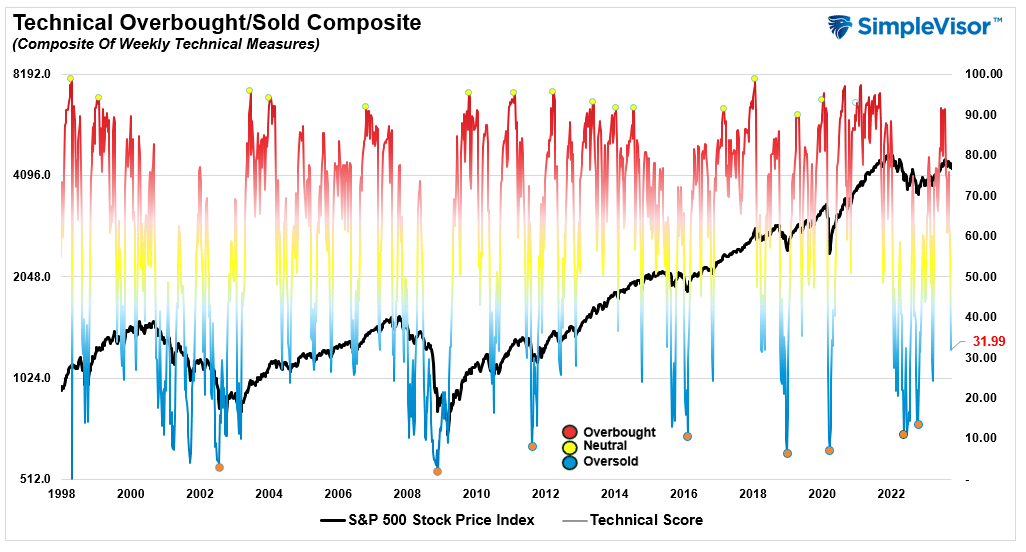

The Q3 earnings season is about to get underway as October starts. Last week, the market took a hit. While many attributed the decline in stocks and rise in bond yields to the recent Fed projections of “higher for longer,” the action seemed more akin to end-of-the-quarter rebalancing for fund managers. Furthermore, September 30th marked the fiscal year-end for about 20% of fund managers who needed to make distributions and redemptions. Nonetheless, the market declined, with only minor support holding the market in place.

The market held support at the 150-DMA, which is acting as minor support. A violation of that level will see the markets quickly test the 200-DMA. If this market will maintain its bullish footing, it must hold support and begin to firm up next week.

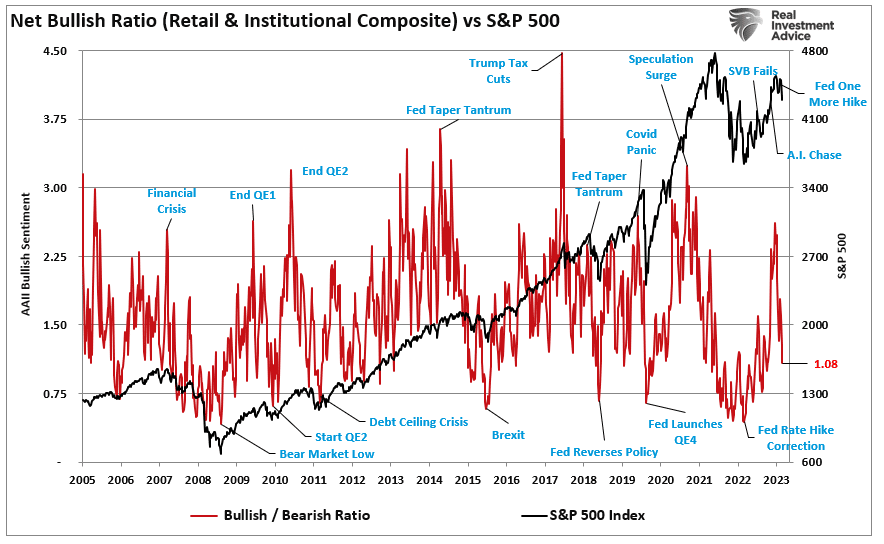

There is currently very negative sentiment and technical support, which suggest that a reflexive rally could begin sooner rather than later.

The chart below shows the relatively sharp decline from the more exuberant bullish sentiment we saw in June and July. Historically, when the combined readings of retail and professional sentiment reached current levels, such formed the basis for a reflexive rally.

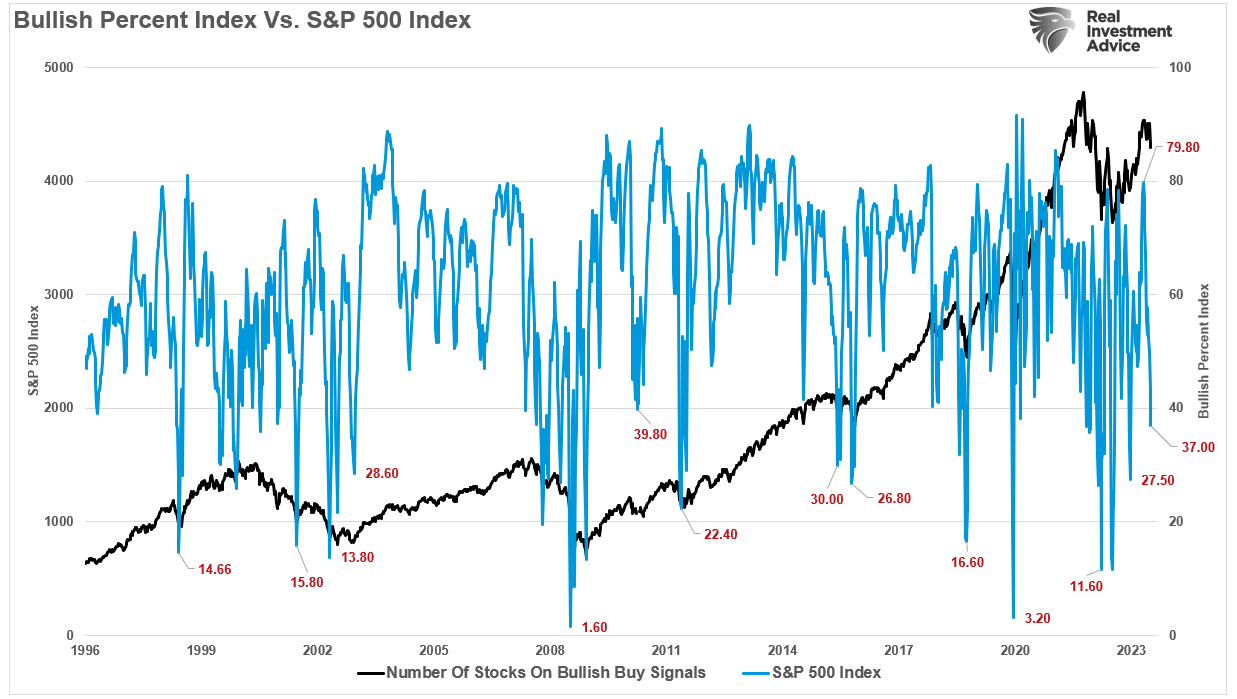

The same holds for the number of stocks on “bullish buy signals.” During more bullish markets, readings below 40 have coincided with near-term market bottoms.

Furthermore, our technical gauge, comprised of weekly readings of the Williams %R, RSI, MACD, and other measures, is reaching more deeply oversold levels. Again, when combined with a high level of leverage and negative sentiment, such is usually the point where markets do the opposite of what everyone expects.

With such negative readings, a rally is becoming more probable. However, the risk of a Government shutdown could delay that rally a bit longer. Trade carefully for now.

The Week Ahead

The focus of this week will be on employment. The economic data starts this morning with the ISM manufacturing PMI, which the consensus expects to increase to 47.9 from 47.6 in August. Tomorrow, we’ll get the latest round of JOLTs data. Economists expect job openings to fall to 8.5 million from 8.8 million last month. The ADP report on Wednesday and the BLS report on Friday will give us an updated look into the health of the labor markets. Current expectations are for employment growth of 158k, following 187k in August. Current expectations are for the unemployment rate to fall to 3.7% from 3.8% in August.

In addition to the economic data, there are a handful of Fed member speeches throughout the week. Notably, Fed Chair Jerome Powell will speak this morning at 11:00 a.m.

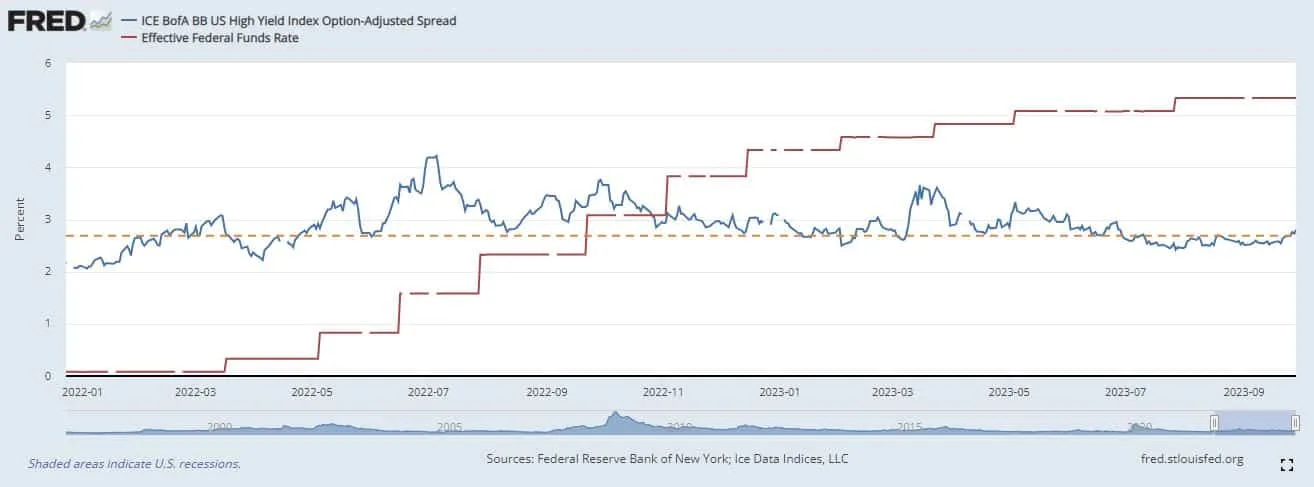

High Yield Spreads Have Barely Budged

High-yield credit spreads remain unusually narrow given the Fed’s monetary policy tightening over the last year and a half. On the day of the initial Federal Funds rate hike last year, high-yield credit spreads were at 2.69%. Even after 1.5 years and multiple subsequent rate hikes leading to rates that are now 5% higher, high-yield bonds are paying only 2.8% above treasuries.

The Fed has repeatedly communicated that it will stand by its restrictive policy until inflation is under control. The longer policy is restrictive, the greater the risk to high-yield bonds. Yet, as shown below, this increasing risk still isn’t priced in. In fact, high-yield spreads have barely budged. We suspect it will take a credit event to spark a flight to safety, and spreads will widen quickly in that case. Funds leaving high-yield would likely flow into treasuries as investors seek safety, depressing yields and boosting returns to treasury bond investors.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.