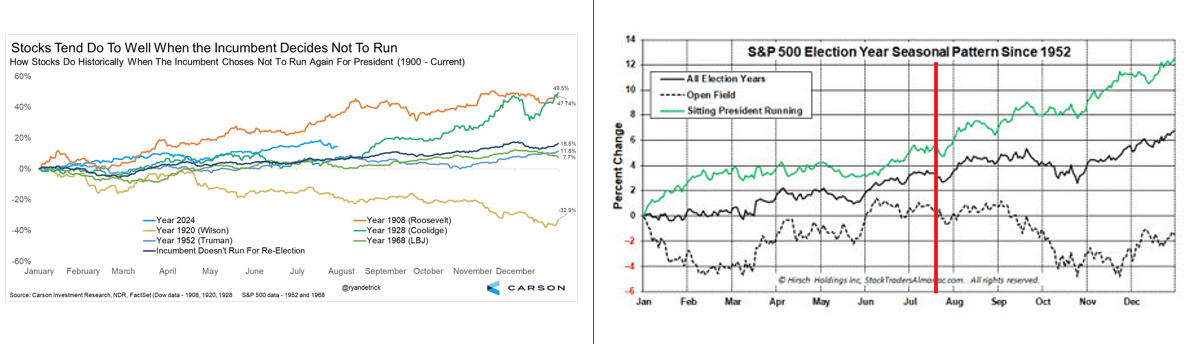

As the election nears, investors will become more anxious about how the market may react to each candidate and their campaign promises. Accordingly, we suspect that shifting polls will breed volatility. Moreover, with President Biden dropping out of the race, this presidential election is unique. Below, we share and discuss two charts to help guide our expectations.

The graph on the left, courtesy of Ryan Detrick, shows that since 1900, there have only been five Presidents, excluding Biden, who have decided not to run for a second term. Four of those five years saw stocks make impressive gains. Furthermore, the average for the five instances is a gain of 16.5%. As of early August, the market is ahead of the average. Given that there have been only five examples over the last 125 years, take the graph results and average with a grain of salt.

The graph on the right may be more salient. It shows that, on average, stocks tend to do well during election years. However, the average is boosted by years in which the sitting President ran for another term. Years like this one, in which neither candidate is the sitting President, have been weak on average. Notably, the market seems to grow the most anxious in the two months leading to the election. Therefore, the simple takeaway from the chart is that markets do not like uncertainty as we have.

What To Watch Today

Earnings

Economy

Market Trading Update

As noted yesterday, the market is decently oversold; however, we remain somewhat cautious with sell signals in place. Following yesterday’s weak economic data, the market sold off as concerns of slower economic growth overshadowed strong earnings from META and ELY. As noted previously, the Fed cuts rates to stave off economic weakness. However, the market has largely ignored the “economic weakness” part, which will impact earnings growth.

While yesterday’s selloff reversed most of Wednesday’s gains, the market held support at the 50-DMA, which continues to act as key support. If the market breaks the 50-DMA, which is possible, the 100-DMA will provide the next support. As noted, the market is oversold enough for a short-term rally. We continue to suggest using rallies to reduce risk and rebalance exposures as needed. Notably, many stocks are reaching levels where good buying opportunities have previously presented themselves.

ISM Provides An Omen For Today’s Employment Report

The ISM Manufacturing survey sent bond yields lower as the odds of a weak employment number today, and a Fed cut in September increased. The broad ISM survey fell further into economic contractionary territory at 46.8, down from 48.5 last month. Most stunning, the employment component fell sharply and is now at its lowest level since mid-2020. The second graph below, courtesy of Rosenberg Research, shows that the employment index is now at levels only seen during recessions.

Also noteworthy was that prices paid were faster than the prior month, but new orders, a good indicator of future activity, fell into contractionary territory. The bond market seems to be ignoring the price component and focusing on employment.

Earnings Expectations and Confidence Diverge

The first graph below, courtesy of Francois Trahan, highlights that consumer confidence is declining, yet EPS expectations are rising. Since personal consumption drives the economy and consumer confidence plays a significant role in personal spending habits, earnings and confidence are typically well correlated.

Trahan’s second set of graphs shows historical instances with similar deviations as we see today. As shown, earnings ultimately fell back in line with declining confidence.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.