You would think that with the U.S. taking out a top Iranian commander, threats of military action flying between the U.S. and Iran, not to mention the “Selective Service” website crashing over concerns of World War III, the markets would be in full “sell” mode.

https://twitter.com/Hipster_Trader/status/1213312685766520832?s=20

Due to the spread of misinformation, our website is experiencing high traffic volumes at this time. If you are attempting to register or verify registration, please check back later today as we are working to resolve this issue. We appreciate your patience.

— Selective Service (@SSS_gov) January 3, 2020

If you thought that would be the case, you were wrong.

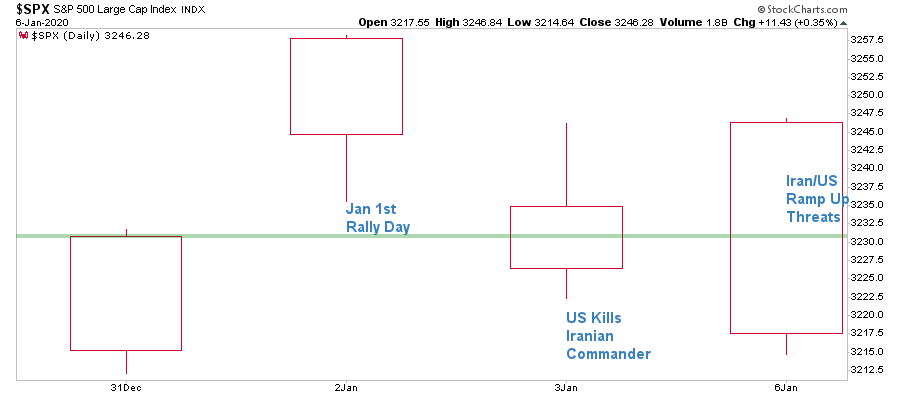

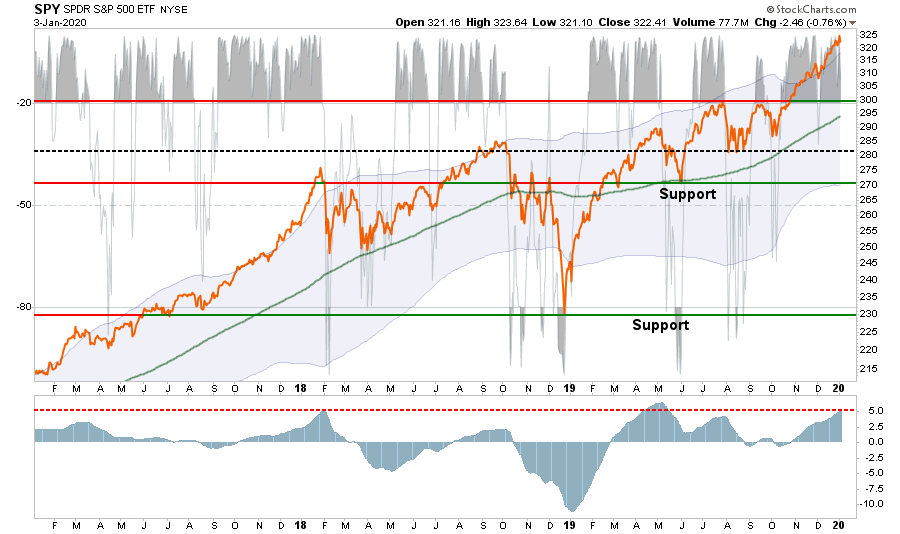

Here is the market from the beginning of the year through yesterday’s close.

The dismissal by the market of the situation with Iran suggests only a couple of things:

- The market sees no inherent risk from Iran other than a lot of “saber rattling,” or

- Given the Federal Reserve’s recent transition to a “do anything” monetary policy stance, all “risks” are being dismissed under the assumption the Fed has become a “cure all” for any market ill.

Since this is a technical post on the financial markets and investing, I won’t get into all the risks inherent from a conflict with Iran. However, if we assume there are indeed “risks” with Iran, then it becomes apparent the market is betting on the Fed.

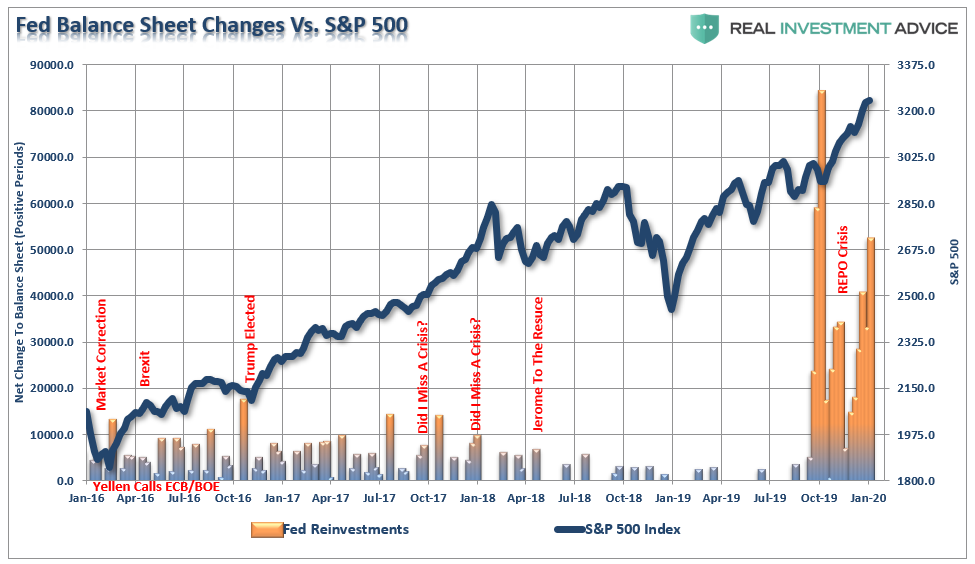

As I noted in this past weekend’s missive, the Fed has been dumping massive amounts of liquidity into the system over the last few weeks. To wit:

“But concerns over potential Iranian conflict quickly abated as the markets returned their focus to the Federal Reserve, and the continued pump of monetary liquidity into the markets.

Currently, we are told there is ‘nothing to worry about’ concerning the financial system. Maybe, but the amount of liquidity being injected dwarfs all previous injections by massive proportions.

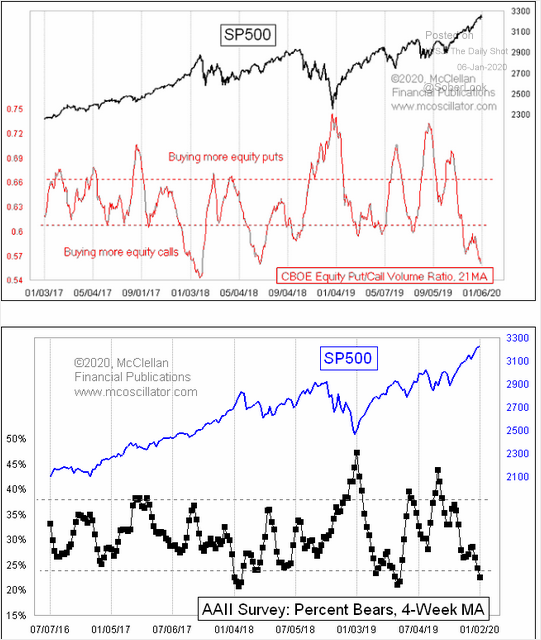

Those injections continue to run unabated currently, which has lulled the markets into a more extreme state of complacency. This can see in the low reading of bearish investors and the suppressed levels of the put/call ratio. Both suggest there is “no fear” of a market correction currently. (h/t Soberlook)

Here is the investor conundrum.

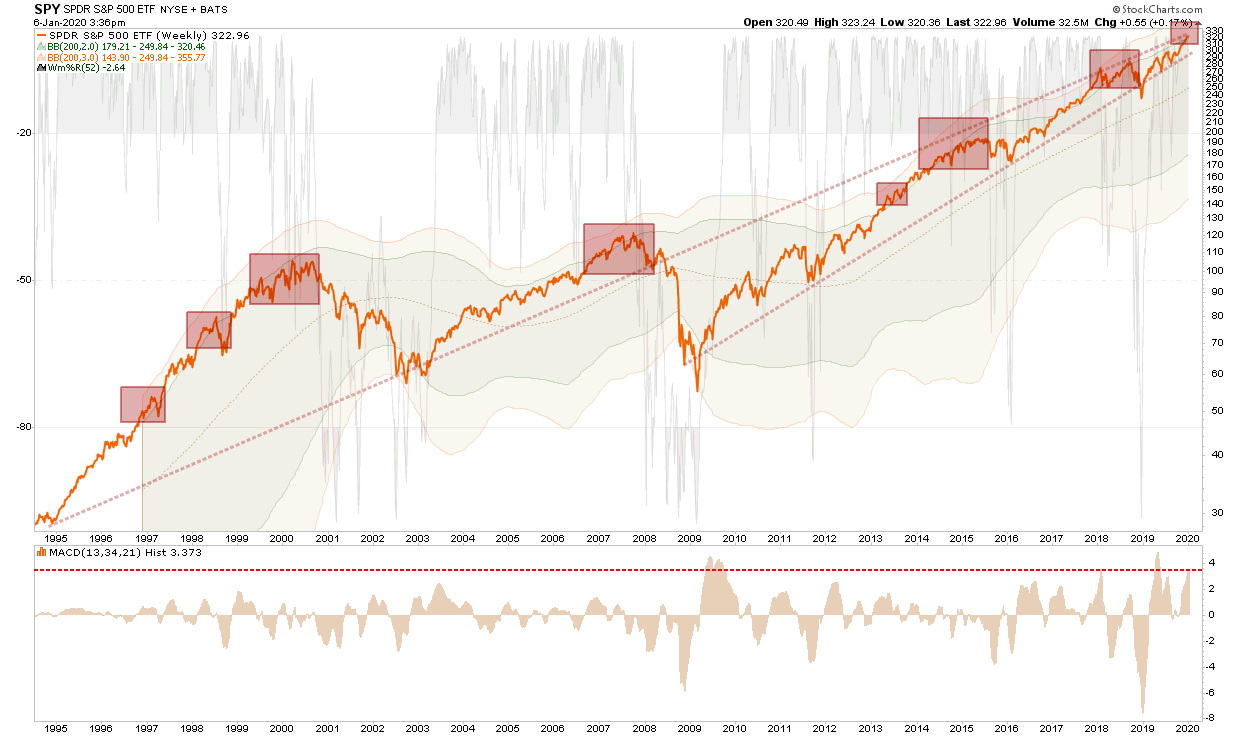

With the market currently on registering of the monthly buy signals, which confirmed the bull market in the S&P 500 had resumed following the 2018 Fed/Trade induced sell-off, there is also the risk of a short-term correction. Previously, when the market was this extended, deviated from longer-term means, and excessively bullish, a correction has always occurred. The problem for investors is maintaining patience in the process.

The chart below shows the issues. When the market becomes more than 2-standard deviations above the 200-WEEK (4-year) moving average, you have gotten a correction, or a deeper mean-reverting event. However, since this a weekly chart, those corrective processes can take some time to occur. This lures investors into thinking “this time is different,” just before an event has tended to reduce their investment capital

Optimistically Cautious Short-Term

In the short-term, our outlook remains optimistically cautious due to the aforementioned ongoing liquidity injections from the Federal Reserve. As we noted to our RIAPro Subscribers yesterday (Try Free For 30-Days):

“The markets remain positively biased but have gotten overly extended in the short-term. We suggest remain long current holdings, but take profits and rebalance risks in positions accordingly. We will likely have a much better entry point in the next couple of months to ‘buy’ into.”

While we remain optimistic on stocks over the next couple of months, as we are in the “seasonally strong period” of the year, there are several risks which need monitoring closely.

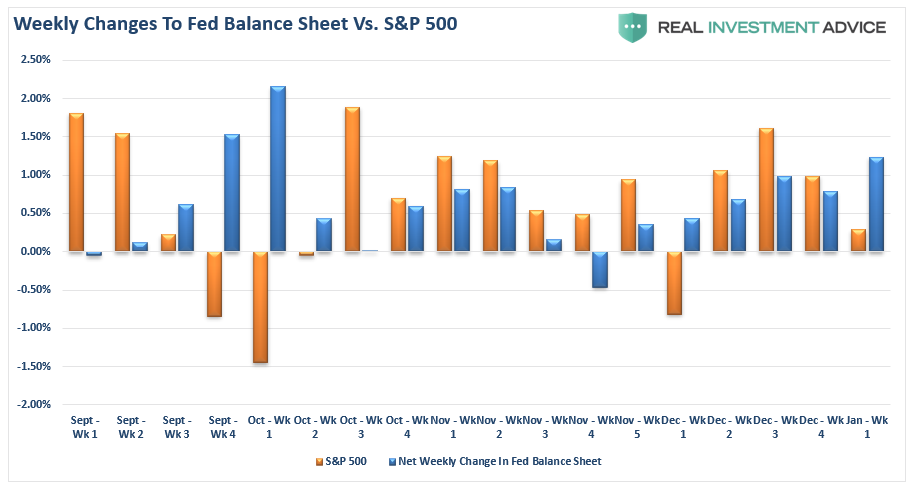

The most obvious risk is a reversal of the Fed’s monetary policy. Currently, the Fed’s balance sheet has almost entirely reversed last year’s decline. Subsequently, changes in the S&P 500 have closely tracked weekly changes to the Fed’s balance sheet. As noted last week:

Of course, it should be expected that if the Fed reverses those flows, then equities will likely follow suit.

Secondly, ultimately, will be valuations.

Yes, I know that “valuations” do not seem to matter currently, however, it is important to realize they will eventually matter, and they will matter a lot.

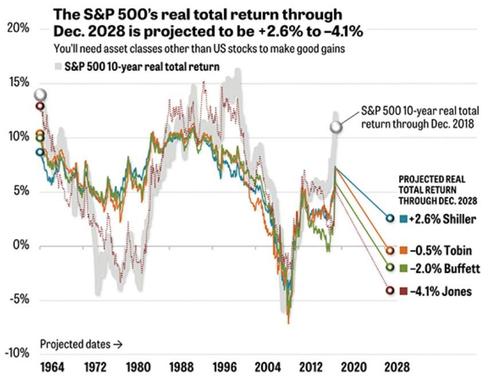

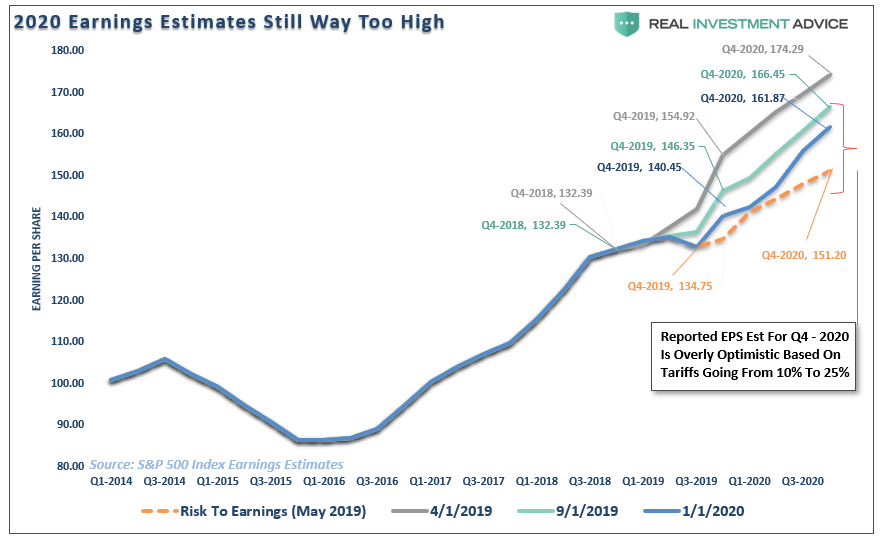

Currently, the S&P 500 trading roughly 20x current reported earnings estimates of $161.87 per share for the end of 2020, based on data from S&P Dow Jones. Going back to the year 1988, on average, the S&P 500 trades for around 16x times trailing earnings estimates. But it isn’t just P/E ratios which are rich. As we discussed yesterday, multiple measures of the markets are trading at levels which have denoted much lower rates of returns going forward.

What this suggests is that for equities to see a continued, and significant, advance in 2020, it will require investors to continue paying higher prices for equity ownership. While this may seem to make sense in a “low-interest rate” world, historically overpaying for earnings growth has often turned out poorly.

In other words, what investors are betting on is that earnings will catch up with price. However, currently, there is no evidence such will be the case as earnings have been repeatedly ratcheted lower since April 2019.

As shown in the chart below, earnings for the entire 2020 period started at $174.29/share. At that time, the beginning of April, the S&P 500 was trading at 2892. While the forward P/E seemed reasonable at 16.5x earnings, which was roughly equal to the long-term average, this assumed earnings estimates were correct. However, with the S&P 500 trading, as of yesterday’s close, at 3246, estimates for 2020 have fallen to just $161.87. That $12 decline in estimates, combined with a 354 point (an 11.8% advance) in the market, brings that forward P/E multiple to a rather expensive 20.05x reported earnings.

Of course, the risk to investors is that earnings growth fails to recover as we head further into 2020. Currently, there is evidence from the manufacturing, employment and wage data which suggests such could indeed be the case.

The Path Ahead

What is clear is that the path ahead for stocks is much less certain than a year ago when we were coming off deeply depressed sentiment levels, and the Fed was rapidly reversing monetary policy from “tightening” to “easing.” With equities now 30% higher than they were then, the Fed mostly on hold in terms of rate cuts, and “repo” operations slated to end in the next couple of months, it certainly seems that expectations for substantially higher market values may be a bit optimistic.

Furthermore, as noted, if signs of economic improvement don’t start to lift expectations for earnings growth into the last half of the year, it could prove problematic given current valuations.

However, if the economy does show improvement, it could result in yields rising on the long-end of the curve, which could also make stocks less attractive. This would effectively keep a lid on just how much risk some investors will be willing to take, and the price they are willing to pay.

One thing is for certain, the sharp rise in stocks in 2019 has left prices at levels that already seem expensive on numerous measures. As such it will required investors to take on increasing levels of risk if prices are going to push higher this year. While this is certainly not an improbability given the current levels of complacency and optimism, it is just worth noting that outcomes of such endeavors have always been poor.

There is one true axiom of the market which is always forgotten.

“The market has a habit of sucking investors in to inflict the most pain possible.”

Just make sure you aren’t one of them.

If you feel you must chase the markets currently, then at least do it with a set of guidelines to follow in case things turn against you. We printed these a couple of weeks ago, but felt there are worth mentioning again.

- Move slowly. There is no rush in adding equity exposure to your portfolio. Use pullbacks to previous support levels to make adjustments.

- If you are heavily UNDER-weight equities, DO NOT try and fully adjust your portfolio to your target allocation in one move.This could be disastrous if the market reverses sharply in the short term. Again, move slowly.

- Begin by selling laggards and losers. These positions are dragging on performance as the market rises and tend to lead when markets fall. Like “weeds choking a garden,” pull them.

- Add to sectors, or positions, that are performing with, or outperforming, the broader market.

- Move “stop loss” levels up to current breakout levels for each position. Managing a portfolio without “stop loss” levels is like driving with your eyes closed.

- While the technical trends are intact, risk considerably outweighs the reward. If you are not comfortable with potentially having to sell at a LOSS what you just bought, then wait for a larger correction to add exposure more safely. There is no harm in waiting for the “fat pitch” as the current market setup is not one.

- If none of this makes any sense to you – please consider hiring someone to manage your portfolio for you. It will be worth the additional expense over the long term.

While we remain optimistic on the markets currently, we are also taking precautionary steps of tightening up stops, adding non-correlated assets, raising some cash, and looking to hedge risk opportunistically.

Just because it isn’t raining right now, doesn’t mean it won’t. Nobody has ever gotten hurt by keeping an umbrella handy.