A test of the 200-dma is coming. The only questions are when and what will cause it?

Two weeks ago in the Real Investment Report (subscribe for free email delivery), I discussed the rather long span of 6-straight positive return months.

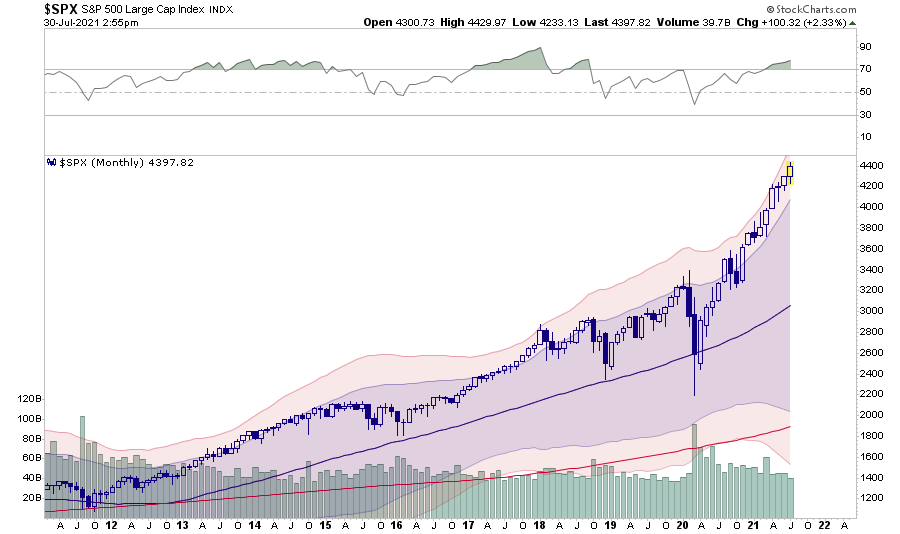

“An additional ‘red flag’ is the S&P 500 has had positive returns for 6-straight months. As shown in the 10-year monthly chart below, such streaks are a rarity, and when they do occur, they are usually met by a month, or more, of negative returns.“

(It is also worth noting that when the 12-Month RSI is this overbought, larger corrective processes have occurred.)

The problem with monthly data is that it is very slow to turn. While such deviations can last a while, the critical point is they do not last forever.

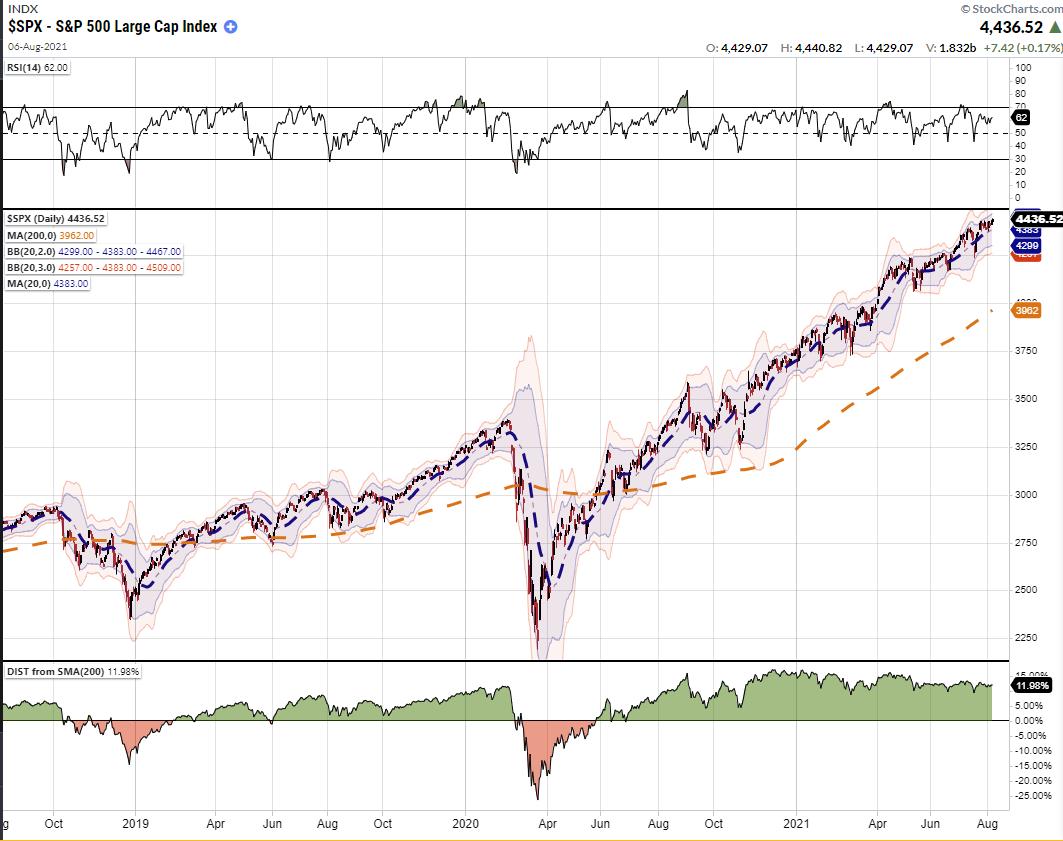

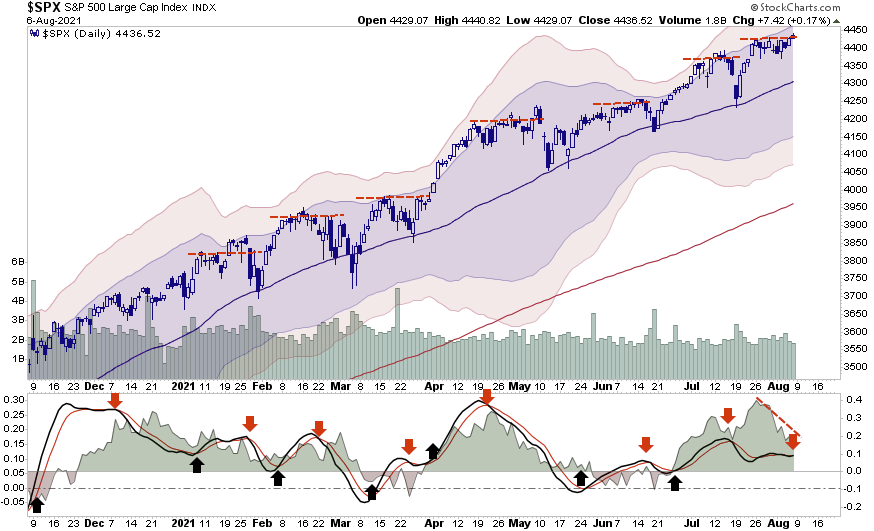

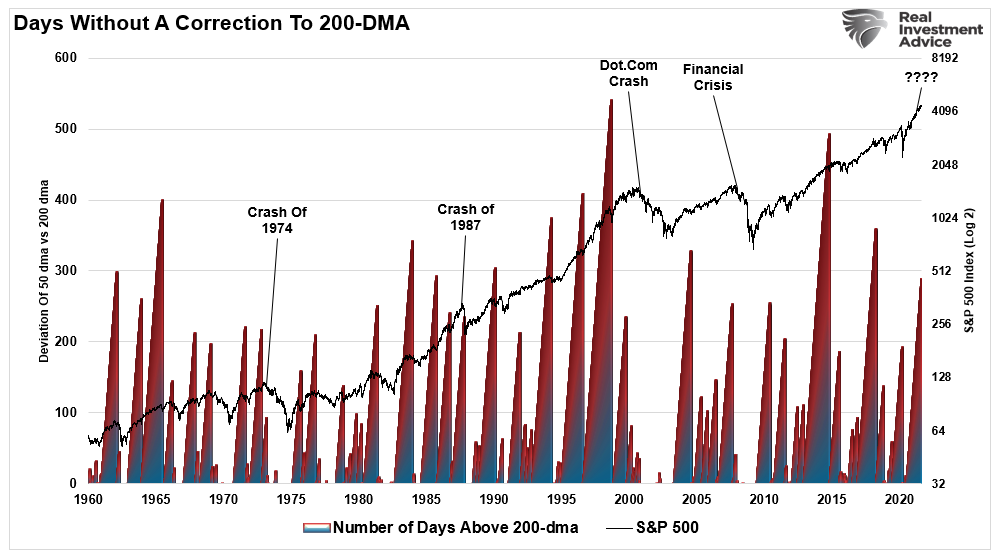

I got several email questions about the current deviation of the market from the 200-dma. Currently, the market has well deviated from a widely watched level of support.

While the current level of deviation is not the highest on record, it is very close.

Is this something we should be immediately concerned about?

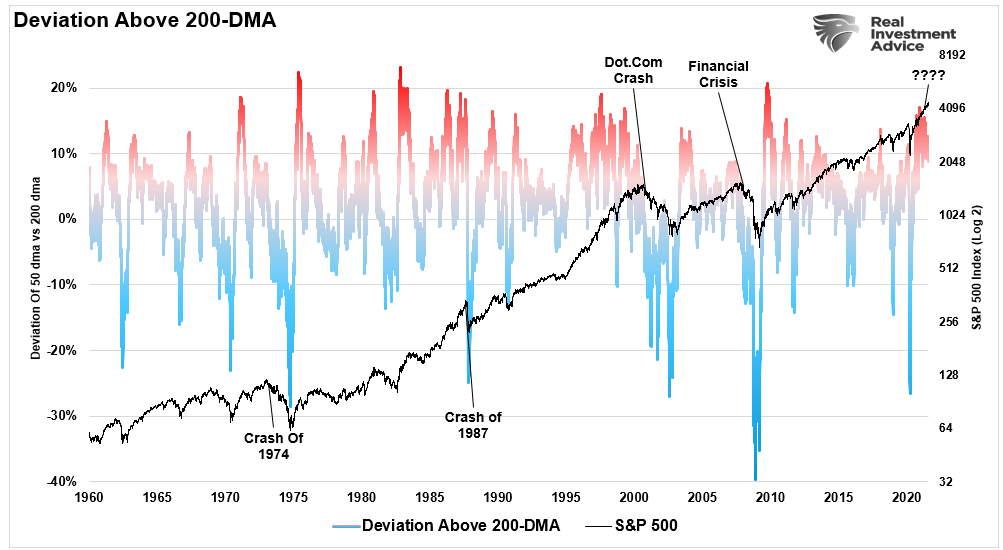

Using daily data back to 1960, I constructed some different variations on the theme of deviations from the 200-dma to try and answer that question.

Why Is The 200-DMA Important

Let’s start with the basics.

The 200-day moving average, as denoted in the chart above, is a technical indicator used to analyze long-term trends. The line represents the average closing price over the last 200 days. Each day, the average changes as the latest data point are added, and the first removed creating a new average price.

Given the 200-dma represents a longer-term holding period for stocks today, it is a more important indicator for “risk” management and capital preservation. As IBD notes:

“Making a decision on when to sell stocks to lock in a profit can be very tough, especially when you’ve amassed long or short-term capital gains. Watching the stock’s behavior at the 200-day moving average can help you decide when it’s time to take at least some partial profits.”

One of the bigger mistakes that investors repeatedly make is not having a “sell discipline.” They often hold a stock that is losing money hoping it will come back which weighs on portfolio performance due to “opportunity cost.” Or, often worse, they turn a large gain into a loss trying to avoid paying “capital gains” tax.

These are easy mistakes to correct using the 200-dma and can improve portfolio performance over time.

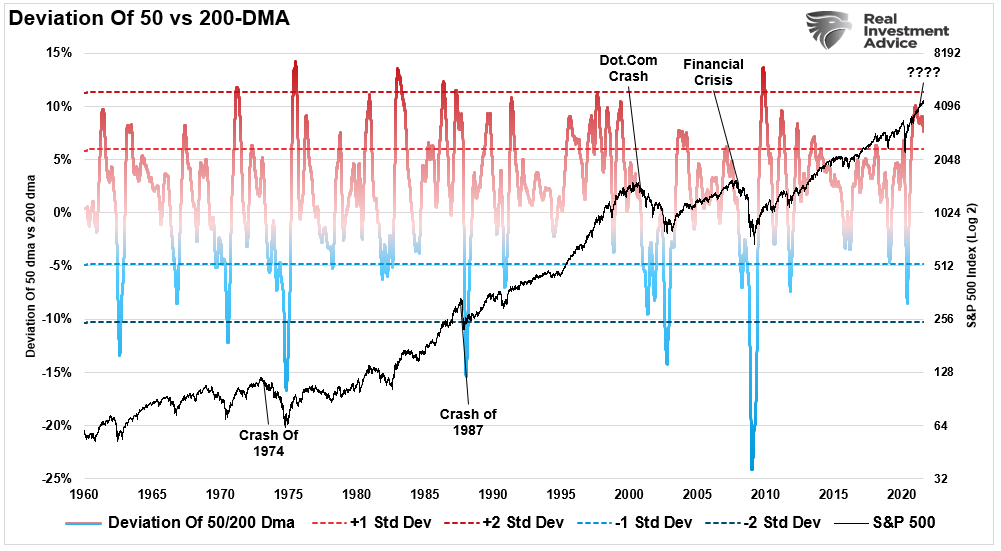

Deviations Above The 200-DMA

In the short term, fundamentals don’t matter. Such is because over a few days, weeks, or even months, what drives prices higher or lower is the psychology of investors. As such, we can look at technical deviations to determine how exuberant or not the market currently is.

For moving averages to exist, prices must trade both above and below that average. As such, moving averages act like gravity on prices. When prices deviate too far from the moving average, eventually, prices will revert to, or beyond, that average.

“Reversion to the mean is the iron rule of the financial markets” – John C. Bogle

We can visualize the reversion in the chart below of the S&P 500 index versus its 200-dma. With the index currently more than 11% above its 200-dma, such should be a short-term warning to investors. Looking back historically whenever deviations exceed 10% above the 200-dma, a correction generally ensues.

Deviations Of Averages

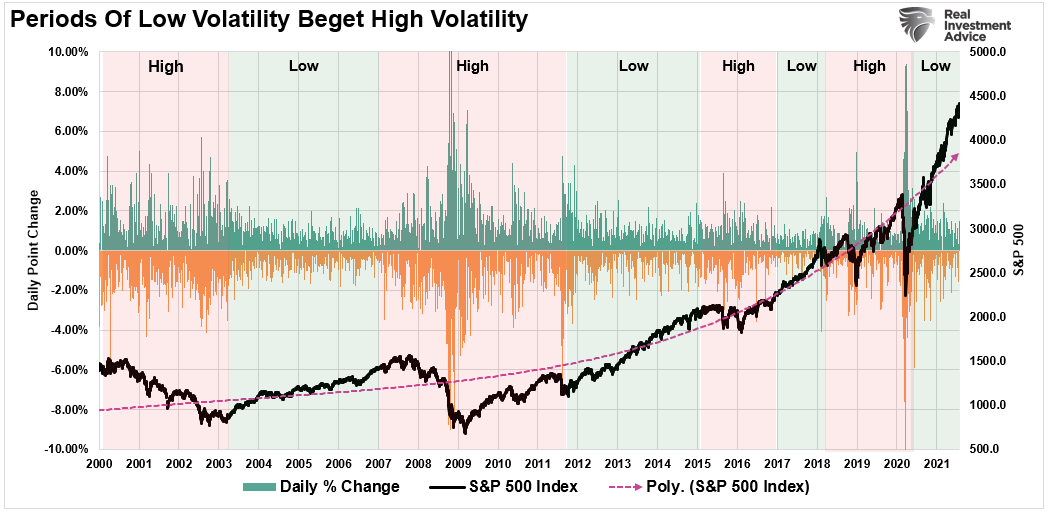

Since last November, the market has exhibited a period of extremely low volatility. During that period, the 50-dma has acted as an important support for the market as speculative buyers use minor “dips” to chase markets. Interestingly, these spurts of “dip buying” create a short-lived advance, price stagnation, and then a retest of the 50-dma.

Of course, the suppressed level of volatility is always a warning. As discussed just recently, “Stability Leads To Instability.” To wit:

“Given the volatility index is a function of the options market, we can also view these alternating periods of ‘stability/instability’ by looking at the daily price changes of the index itself.“

The following chart says much the same. Currently, the 50-day moving average is also significantly deviated above the 200-dma. Such suggests that not only will prices retest the 50-dma, but there is a rising probability that price will revert to the 200-dma.

Notably, technical deviations in the short term do NOT mean the market will “crash” tomorrow. Markets can remain deviated for quite some time. However, when the deviations begin to diverge from the price index negatively, such has previously preceded more important corrections and bear markets.

It is something worth paying attention to.

A Long Time Without A Test Of The 200-DMA

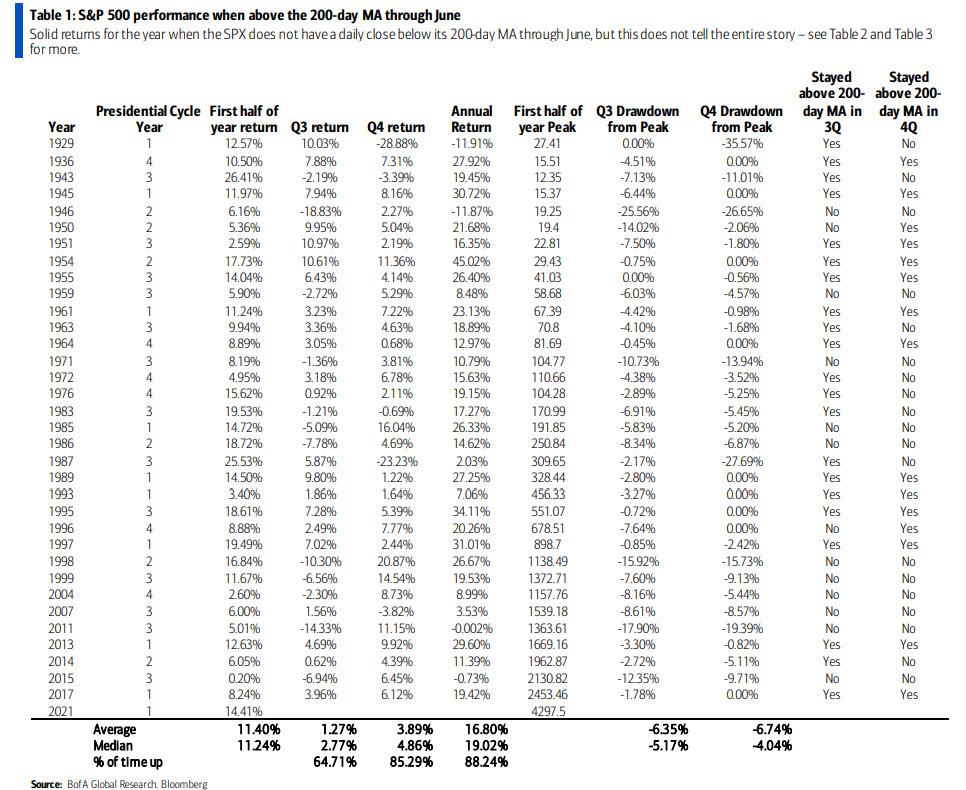

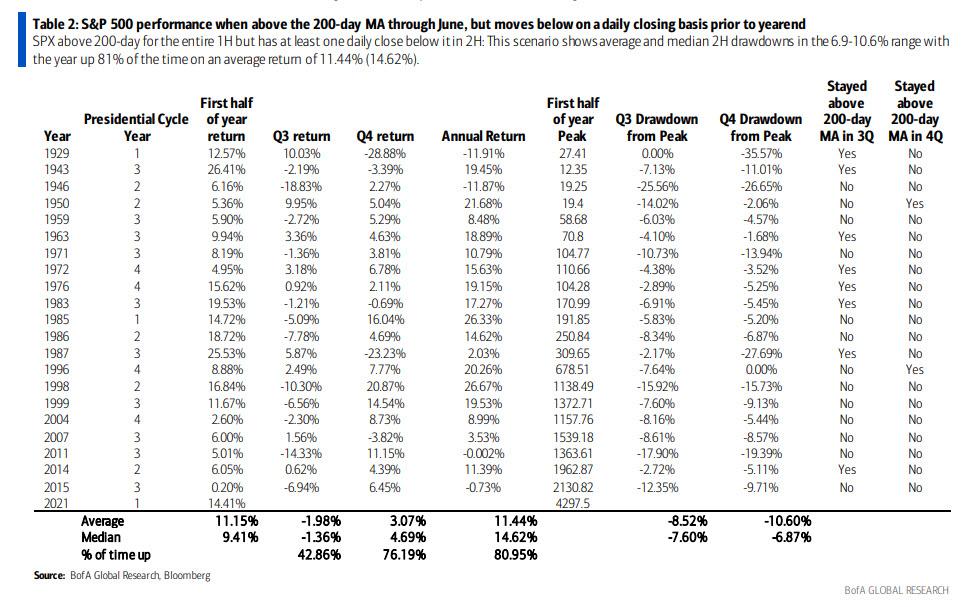

In a recent note from BofA (via Zerohedge):

- The SPX has not had a daily close below its 200-day moving average (MA) in 2021. This has happened through June in 35 out of 93 years (38% of the time) from 1929-2021. For years the SPX did not close below its 200-day MA through June, the average first half (1H) return is 11.40% (11.24%). That extends to an average annual return of 16.80% (19.02% median). The SPX is up 88% of the time for the year in which that occurs. But, SPX above 200-day MA for entire year only occured 13 times

- The SPX stayed above its 200-day MA for an entire calendar year only 13 times (14% of the time) going back to 1929. This means the SPX revisited its 200-day MA in the second half of the year in 21 out the 35 years in years where the SPX did not close below its 200-day in the first half.

Coming In The Second Half?

- SPX more likely to test its 200-day MA in 2H 2021. History reveals it is difficult for the SPX to stay above its 200-day MA for an entire calendar year. This scenario shows average and median 2H drawdowns in the 6.9-10.6% range. However, the year remains up 81% of the time on an average return of 11.44% (14.62%). Such means the SPX could end 2021 near current levels if a move below the 200-day MA occurs.

As BofA concludes:

“If the SPX stays above its 200-day, 2021 would mark the 14th year it did so since 1929.“

In other words, it is possible the S&P could remain above the 200-dma for the rest of the year. The visualization of such deviations suggests an elevated risk it won’t.

The Fly In The Ointment

As we have discussed over the last couple of weeks, the biggest single risk to the market currently is the Fed. As noted in “Awaiting The Fed:”

“Jerome Powell has already set the table for tapering bond purchases by noting ‘substantial progress’ towards the Fed’s goal of full employment and price stability. The July jobs report, on the surface, was robust, providing that evidence.

We think the Fed may openly discuss the issue of reducing its monetary support at the upcoming ‘Jackson Hole Summit.’ Such could even include a general timeline to the reduction process in an attempt to maintain market stability.”

Our view was supported by Raghuram Rajan for Project Syndicate:

“Fed Chair Jerome Powell’s announcement last week that the economy had made progress toward the point where the Fed might end its $120 billion monthly bond-buying program was good news. Phasing out quantitative easing (QE) is the first step toward monetary-policy normalization, which itself is necessary to alleviate the pressure on asset managers to produce impossible returns in a low-yield environment.”

The Biggest Risk

The biggest risk for the financial markets remains the contraction of liquidity fueling the rise in asset prices. Given the economy is already slowing, as forecasted by falling yields and flattening yield curve, the overly bullish, extended, deviated, and overvaluation of markets is problematic.

Investors are currently highly leveraged and over-allocated to equity risk. The low volatility regime of markets has given rise to more extreme levels of complacency which will fuel a “rush for the exits” when something breaks.

For investors, pay attention to 50-dma. If it is violated with conviction, a test of the 200-dma will not be far behind.

As Jason Zweig previously penned:

“Where ignorance is bliss, ‘tis folly to be wise,” wrote the British poet Thomas Gray. One of these days, perhaps sooner rather than later, stocks will stop going up. The importance of understanding what you own will reassert itself. For the time being, though, investors who used to think of themselves as wise may continue to look foolish.”